家庭用品市場レポート 2030 - セグメント、地域、動向、最近の動向、戦略的洞察

家庭用品市場の規模と予測(2020年 - 2030年)、世界および地域シェア、トレンド、成長機会分析レポートの対象範囲:製品タイプ(調理器具、ベーキング用品、食器、キッチン家電、バスルーム必需品、その他)および流通チャネル(スーパーマーケット、ハイパーマーケット、専門店、オンライン小売、その他)別

- ステータス : 出版

- レポートコード : TIPRE00030119

- カテゴリー : 消費財

- ページ数 : 150

- 利用可能なレポート形式 :

- 最終更新日 : June 12, 2024

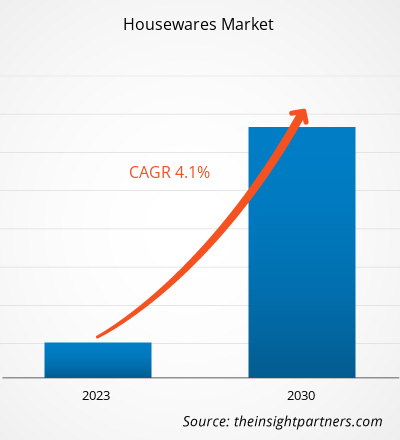

[調査レポート] 家庭用品市場規模は2022年に3,214億米ドルと評価され、2030年までに4,425億1,000万米ドルに達すると予想されており、2022年から2030年にかけて4.1%のCAGRを記録すると予測されています。

市場洞察とアナリストの見解:

家庭用品とは、家庭内で調理、ベーキング、家の整理整頓などに使用される製品やアイテムです。家庭用品市場は、ライフスタイルの変化や自宅で過ごす時間の増加などの要因により着実に成長しており、機能的で見た目に美しい家庭用品の需要が高まっています。COVID-19パンデミックの間、人々は家で過ごす時間が増え、生活空間の改善に投資しました。さらに、eコマースやオンラインショッピングプラットフォームの台頭により、消費者は自宅からさまざまな家庭用品にアクセスして購入することが容易になりました。これらの要因と、家庭用品企業が提供する革新的なデザインや持続可能なオプションが相まって、家庭用品市場の拡大に有利に働いています。

成長の原動力と課題:

ライフスタイルの劇的な変化と共働き世帯の増加により、可処分所得が増加し、世帯の生活水準が向上しました。可処分所得の増加に伴い、消費者は便利な生活をサポートする家庭用品やその他の電化製品に多額のお金を費やしています。彼らは、個性に訴えるユニークなスタイルの新製品を購入する傾向があり、その結果、購入頻度が高くなります。さらに、単身世帯の急増により住宅改修の必要性が高まり、キッチン家電、調理器具、ベーキング用品、食器、バスルーム必需品などの家庭用品の需要が高まっています。

さらに、都市化の進展により、住宅ユニット、そして最終的には家庭用品の需要が高まっています。米国国勢調査局と米国住宅都市開発省によると、米国は2021年に約130万戸の住宅の建設を完了しましたが、約170万戸の住宅の建設が進行中でした。同様に、ヨーロッパ諸国での都市化の進展により、住宅に対する大きな需要が生まれています。欧州委員会によると、欧州連合では2015年から2021年にかけて住宅建築許可が42.3%増加しました。2021年には、フランス、ドイツ、ポーランドがヨーロッパで最も多くの住宅建設着工数を占めました。このように、さまざまな国で住宅ユニットの建設が増加していることで、家庭用品の需要がさらに高まっています。このように、家庭用品の購入の増加と世帯数の増加が、家庭用品市場の成長を促進しています。

しかし、家庭用品市場は、発展途上国で営業している多くの未開拓の小規模な民間企業や露天商のために、非常に細分化され、無秩序になっています。ビジネススタンダードに掲載された記事によると、2020年の時点で、インドのキッチン用品市場の80%は未組織でした。地元の中小企業は、調理器具、耐熱皿、浴室アクセサリー、食器などの家庭用品を製造するために低品質の原材料を使用しています。低品質の原材料を使用すると、損傷しやすい低品質の最終製品になります。また、メーカーはこれらの製品を低価格で提供しているため、大多数の消費者は手頃な価格と入手のしやすさからこれらの製品を購入します。この要因により、大手家庭用品メーカーの顧客基盤が縮小しています。

さらに、組織化されていない家庭用品市場では、現地メーカーが規制基準を遵守していないことが多く、品質問題を引き起こし、家庭用品に対する消費者の認識を阻害する可能性があります。さらに、偽造品の流通により、主要企業のブランドイメージが損なわれる可能性があります。このように、運営と規制の統一性の欠如が家庭用品市場の成長を妨げています。

要件に合わせてレポートをカスタマイズする

このレポートの一部、国レベルの分析、Excelデータパックなど、あらゆるレポートを無料でカスタマイズできます。また、スタートアップや大学向けのお得なオファーや割引もご利用いただけます。

家庭用品市場:戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

レポートのセグメンテーションと範囲:

世界の家庭用品市場は、製品タイプ、流通チャネル、および地域に基づいてセグメント化されています。製品タイプに基づいて、市場は調理器具とベーキング用品、食器、キッチン家電、バスルーム必需品、その他に分類されます。流通チャネル別では、市場はスーパーマーケットとハイパーマーケット、専門店、オンライン小売、その他に分類されます。地域別に見ると、世界の家庭用品市場は、北米、ヨーロッパ、アジア太平洋、中東およびアフリカ、南米および中米に大まかに分類されています。

セグメント分析:

製品タイプに基づいて、家庭用品市場は、調理器具とベーキング用品、食器、キッチン家電、バスルームの必需品、その他に分類されます。食器セグメントは、2022年から2030年の間に最高のCAGRを記録すると予想されています。食器セグメントには、食器、カトラリー、ガラス製品、サーブウェアなどの製品が含まれます。家庭用品市場における食器の需要の急増は、COVID-19パンデミック中の食習慣の変化に起因する可能性があります。自宅で食事をする人が増えるにつれて、人々は自宅での食事の体験を向上させるため、美しく機能的な食器に注目し始めました。毎日の食事から特別な集まりまで、消費者は食事の体験を高める食器セットを求めています。さらに、ユニークで職人技のデザインに対する評価が高まっていることも、食器の需要を促進する上で重要な役割を果たしています。消費者は、食事の場に個性と個性をもたらす手作りで芸術的にインスピレーションを受けた食器にますます惹かれています。このように、よりパーソナライズされ、見た目が印象的な食器の選択への移行は、食器部門の家庭用品市場の発展に貢献しています。Vivo - Villeroy & Boch Group、Corelle、Pyrex、Luminarc、Schott Zwiesel は、食器市場で活動している著名な企業の一部です。

地域分析:

家庭用品市場は、北米、ヨーロッパ、アジア太平洋、中南米、中東アフリカの5つの主要地域に分かれています。2022年の世界の家庭用品市場はアジア太平洋地域が独占し、この地域の市場規模は1,206.3億米ドルに達しました。ヨーロッパは2番目に大きな貢献者で、世界市場の23%以上のシェアを占めています。アジア太平洋地域は、2022年から2030年にかけて5%を超える大幅なCAGRを記録すると予想されています。都市化の進展と中流階級の可処分所得の増加は、先進的なキッチン家電やスタイリッシュな食器など、モダンで便利な家庭用品の需要を押し上げる主な要因です。

家庭用品市場の地域別分析

予測期間を通じて家庭用品市場に影響を与える地域的な傾向と要因は、Insight Partners のアナリストによって徹底的に説明されています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東、アフリカ、南米、中米にわたる家庭用品市場のセグメントと地理についても説明します。

- 家庭用品市場の地域別データを入手

家庭用品市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2022年の市場規模 | 3,214億米ドル |

| 2030年までの市場規模 | 4,425.1億米ドル |

| 世界のCAGR(2022年 - 2030年) | 4.1% |

| 履歴データ | 2020-2021 |

| 予測期間 | 2023-2030 |

| 対象セグメント |

製品タイプ別

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業プロフィール |

|

市場プレーヤーの密度:ビジネスダイナミクスへの影響を理解する

家庭用品市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認識の高まりなどの要因により、エンドユーザーの需要が高まり、急速に成長しています。需要が高まるにつれて、企業は提供品を拡大し、消費者のニーズを満たすために革新し、新たなトレンドを活用し、市場の成長をさらに促進しています。

市場プレーヤー密度とは、特定の市場または業界内で活動している企業または会社の分布を指します。これは、特定の市場スペースに、その規模または総市場価値と比較して、どれだけの競合相手 (市場プレーヤー) が存在するかを示します。

家庭用品市場で事業を展開している主要企業は次のとおりです。

- ブラッドショーホーム株式会社

- デンビー陶器株式会社

- HF クアーズ株式会社

- インターイケアホールディングBV

- ハッツラー製造株式会社

免責事項:上記の企業は、特定の順序でランク付けされていません。

- 家庭用品市場のトップキープレーヤーの概要を入手

COVID-19パンデミックの影響:

COVID-19パンデミックは当初、製造ユニットの閉鎖、労働力不足、サプライチェーンの混乱、金融不安により、世界の家庭用品市場の足を引っ張った。COVID-19の発生による経済減速により、さまざまな業界で事業が中断し、家庭用品の供給が抑制された。さらに、さまざまな店舗が閉鎖され、家庭用品の販売が制限された。しかし、2021年にはさまざまな国で以前に課された制限が解除され、ビジネスは勢いを増し始めた。さらに、さまざまな国の政府によるCOVID-19ワクチン接種キャンペーンの実施により状況が緩和され、世界中でビジネス活動が増加した。家庭用品市場を含むいくつかの市場は、ロックダウンと移動制限の緩和後に成長を報告した。

競争環境と主要企業:

Bradshaw Home Inc、Denby Pottery、HF Coors Co Inc、Inter Ikea Holding Bv、Hutzler Manufacturing Co Inc、TTK Prestige Ltd、Newell Brands Inc、BSH Hausgerate GmbH、Kohler Co、およびHaier US Appliance Solutions Incは、世界の家庭用品市場で活動している著名な企業です。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応