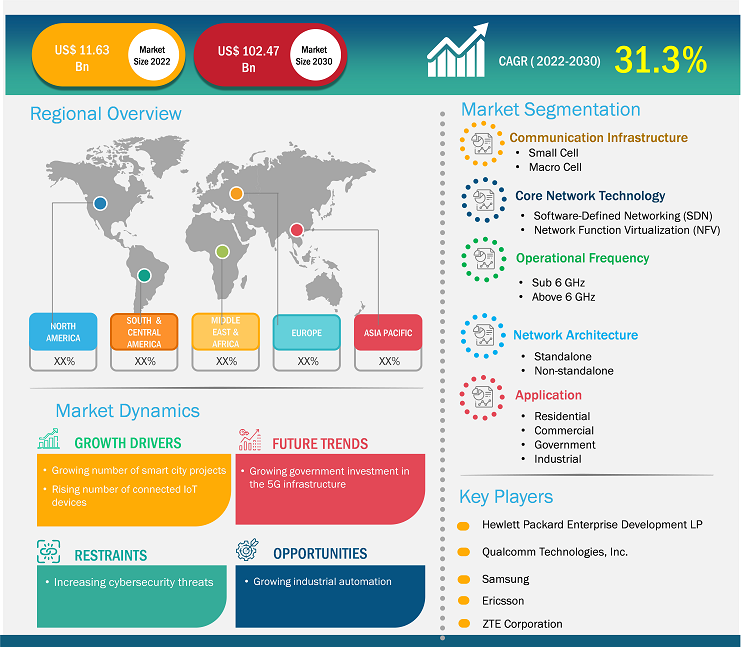

The 5G infrastructure market size is expected to grow from US$ 11.63 billion in 2022 to US$ 102.47 billion by 2030; it is estimated to grow at a CAGR of 31.3% from 2022 to 2030.

Analyst Perspective:

The growing number of smart city projects worldwide is raising the demand for 5G as it can provide faster communication infrastructure, analytics, IoT, and automation for environmental protection, improve traffic, and public safety. Also, the rising number of connected IoT devices is propelling the growth of the 5G infrastructure market. Furthermore, the growing industrial automation is raising the demand for 5G. The 5G technology provides features such as lower latency, higher reliability, and increased speed, which support emerging technologies and their innovative approaches and applications in smart factories, thus creating an opportunity for the growth of the 5G infrastructure market. In addition, the growing investment by the governments of different countries in the 5G infrastructure will also propel market growth in the forecasted period.

Market Overview:

5G infrastructure is the network of macro and small-cell base stations consisting of edge computing capabilities which are required for the functionality of the fifth-generation technology standard for cellular networks. Low latency coverage for big data streams is made possible by 5G infrastructure, and this is beneficial for applications such as augmented reality, semi-autonomous vehicles, and Internet of Things devices. There are two types of 5G network infrastructure: non-standalone (NSA) infrastructures that still rely on some 4G LTE equipment and standalone 5G infrastructures that have their own cloud-native network core connecting to 5G New Radio (NR) technologies.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

5G Infrastructure Market: Strategic Insights

Market Size Value in US$ 11.63 billion in 2022 Market Size Value by US$ 102.47 billion by 2030 Growth rate CAGR of 31.3% from 2022 to 2030 Forecast Period 2022-2030 Base Year 2022

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

5G Infrastructure Market: Strategic Insights

| Market Size Value in | US$ 11.63 billion in 2022 |

| Market Size Value by | US$ 102.47 billion by 2030 |

| Growth rate | CAGR of 31.3% from 2022 to 2030 |

| Forecast Period | 2022-2030 |

| Base Year | 2022 |

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

5G Infrastructure Market Driver:

Growing Industrial Automation is Providing an Opportunity for the Growth of the 5G Infrastructure Market

The demand for automation is increasing in various industries worldwide. High-speed wireless communication is essential to automation and interconnectivity because it serves as a link between machines, sensors, and users and seamless, scalable connectivity. Additionally, it links automated guided vehicles (AGVs), robotics, drones, and the Internet of Things (IoT). Also, rising factory automation enhances the productivity and quality of the product while decreasing the overall production cost. Furthermore, industrial automation guarantees consistent and superior-quality results, which helped it gain high demand in various industries, such as automotive, manufacturing, and others, for qualitative manufacturing. Moreover, the adoption of automation fulfills the need for mass production in industries with several features, such as improved quality, minimal human intervention, and lesser labor expenses. Additionally, the demand for quicker and more secure communication has increased due to the growth of Industry 4.0. All the automation devices can be connected to the fifth-generation (5G) cellular network, which provides the stability and speed needed to retrieve and process data. 5G technology automates monotonous, labor-intensive, and dangerous tasks in smart factories, raising its demand in the market. Also, Production lines in smart factories can be remotely monitored and operated without the need for workers or operators on the factory floor. Real-time remote monitoring is made simple by 5G technology's decreased latency and faster data transmission rates. Thus, the growing industrial automation worldwide is creating an opportunity for the 5G infrastructure market growth in the forecasted period.

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

Segmental Analysis:

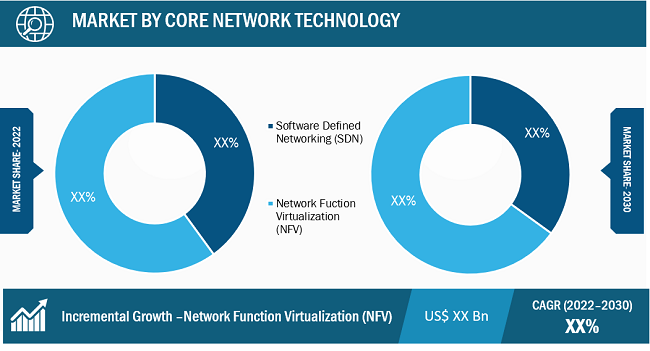

Based on core network technology, the 5G infrastructure market is segmented into software-defined networking (SDN) and network function virtualization (NFV). The network function virtualization (NFV) segment held the largest 5G infrastructure market share in 2022 and is anticipated to register the highest CAGR during 2022-2030. The NFV reduces the need for dedicated hardware for the deployment and management of networks by offloading network functions into the software, which can run on industry-standard hardware and can be managed from anywhere within the operator's network. Thus, all the above factors are fueling the segment's growth in the 5G infrastructure market.

Regional Analysis:

North America is expected to witness significant growth in the 5G infrastructure market in the forecasted period. In the region, the US will hold the largest 5G infrastructure market share in 2022 and will register the highest CAGR during 2022-2030. The digital industrial revolution, i.e., Industry 4.0, is helping to ease manufacturing operations, mass customization, increased speed, better quality, and improved productivity in factories. Because of this, automobile, retail, mechanical engineering, and electronics sectors are installing different industrial automation solutions to increase productivity. In 2021, in Italy, mechanical engineering will be the main consumer of automation, contributing 16% of the total share, packaging will contribute 10%, the food industry will contribute 9%, and logistics will contribute 7%. Thus, the rising adoption of factory automation solutions further boosts the market growth in the forecasted period.

Also, governments in various countries are investing in automating the manufacturing business in the region. For instance, in July 2021, the UK government announced an investment of US$ 59.3 million (£53 million) to drive the development of digital manufacturing technologies. Out of which, US$ 28.10 million (£25 million) will be invested in setting up five new industry-sponsored research centers to accelerate the development of cutting-edge digital solutions that can transform manufacturing businesses. The remaining amount will be invested in a digital supply chain innovation hub and will also be provided to 37 individual projects to digitalize and transform manufacturing supply chains. Thus, the growing government support will further boost the growth of the 5G infrastructure market growth in North America.

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

Key Player Analysis:

Cisco Systems, Inc.; Huawei Technologies Co., Ltd.; Intel Corporation; Fujitsu Ltd.; NEC Corporation; Hewlett Packard Enterprise Development LP; Qualcomm Technologies, Inc.; Samsung; Telefonaktiebolaget LM Ericsson; and ZTE Corporation are among the key 5G infrastructure market players. These 5G infrastructure market players are focused on continuous product development and innovation.

Recent Developments:

Inorganic and organic strategies such as product launches, partnerships, collaboration, and mergers and acquisitions are highly adopted by companies in the 5G infrastructure market. A few recent key market developments by these companies are listed below:

- In November 2023, Huawei announced the launch of its “5.5G” intelligent core network solution. This new core network solution applies intelligence, as well as intent-driven technologies, to the core network, helping operators build service, network, and operations and maintenance (O&M) intelligence.

- In September 2023, Siemens announced the launch of a private 5G infrastructure developed in-house for industry users. The solution enables industrial companies to build their own local 5G networks that provide optimal support for automation applications. According to Siemens, Private 5G Infrastructure, by building their own 5G networks, industrial companies are launching the next stage of connected production.

- In July 2023, Ericsson and Intel announced a strategic collaboration to utilize Intel’s 18A process and manufacturing technology for Ericsson’s future next-generation optimized 5G infrastructure. As part of the agreement, Intel will manufacture custom 5G SoCs (system-on-chip) for Ericsson to create highly differentiated leadership products for future 5G infrastructure. Additionally, Ericsson and Intel will expand their collaboration to optimize 4th Gen Intel Xeon Scalable processors with Intel vRAN Boost for Ericsson’s Cloud RAN (radio access network) solutions to help communications service providers increase network capacity and energy efficiency while gaining greater flexibility and scalability.

- In February 2023, Viettel and Qualcomm Technologies, Inc. announced that they have completed the first versions of Viettel's 5G Distributed Unit (DU) and Radio Unit (RU) based on the Qualcomm® X100 5G RAN Accelerator Card and Qualcomm® QRU100 5G RAN Platform, respectively. At MWC Barcelona 2023, Viettel unveiled prototypes of their DU and RU, powered by Qualcomm 5G RAN Platforms, adding to their comprehensive product portfolio, including the Core Network and OCS System. These new O-RAN compatible products boast leading energy efficiency with exceptional performance featuring mmWave to massive MIMO, 64T64R capabilities to 4T4R radios, integrated 300 Gbps Ethernet interface, and support for advanced features such as Dynamic Spectrum Sharing (DSS).

- In February 2023, Astella Technologies Limited launched commercial-grade 5G infrastructure software products, including the 5G core network and 5G integrated small cells for both sub-6 and mmWave frequency bands in the Mobile World Congress 2023.

- In February 2023, Nokia announced that it is extending its private 5G partnership with IT infrastructure firm Kyndryl for an additional three years. Under this partnership, the companies will focus on developing and delivering LTE, 5G private wireless services, and Industry 4.0 solutions to customers worldwide.

- In October 2022, Ericsson announced that they have entered into a long-term strategic 5G contract with Indian communications service provider (CSP) Reliance Jio Infocomm Ltd. (Jio) to roll out 5G Standalone (SA) in India. Under this collaboration, Ericsson’s energy-efficient 5G Radio Access Network (RAN) products and solutions (from the Ericsson Radio System portfolio) and E-band microwave mobile transport solutions will be deployed in the 5G network for Jio. All products and solutions are deployed on new-build 5G SA networks, designed to maximize the benefits of 5G to CSPs and their customers – whether individual subscribers or enterprise and industry customers.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Communication Infrastructure, Core Network Technology, Operational Frequency, Network Architecture, and End User

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

The List of Companies

- Cisco Systems, Inc.

- Huawei Technologies Co. , Ltd.

- Intel Corporation

- MediaTek Inc.

- NEC Corporation

- Affirmed Networks Inc.

- VMware, Inc.

- Samsung Corporation

- Telefonaktiebolaget LM Ericsson

- ZTE Corporation

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to 5G Infrastructure Market

Apr 2024

Robotic Crawler Camera System Market

Size and Forecast (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Component [Hardware (Cameras, Crawlers, Cable Drums, Control Units, and Others), Software, and Service], Application (Drain Inspection, Pipeline Inspection, and Tank Void Capacity or Conduit Inspection), and End User (Residential, Commercial, Municipal, and Industrial)

Apr 2024

Inertial Sensor for Land Defense Systems Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Technology (FOG, MEMS, and Others) and Application (Stabilization Missile Systems, Stabilization Turret-Cannon Systems, Land Navigation Including Land Survey, Missile GGM-SSM, Stabilization Active Protection System, Stabilization of Optronics System, and Others)

Apr 2024

Drone Lithium Battery Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis By Battery Type (Li-ion, Li-Po, and Li-S), Battery Capacity (Below 3,000 mAh; 3,000–5,000 mAh; and Above 5,000 mAh), Drone MTOW (Below 100 Kgs, 100–200 Kgs, and Above 200 Kgs), Wing Type (Fixed Wing and Rotary Wing), and End Use (Military and Commercial)

Apr 2024

ASRS for Garments on Hangers Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis By Type (Garment Rail System, Garment Conveyor, Garment Property Storage, and Others) and Application (Warehousing and Logistics, Retail 3PL, Hotels, Hospitals and Institutes, and Others)

Apr 2024

Analog to Digital Converter Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Type (Integrating Analog to Digital Converters, Delta-Sigma Analog to Digital Converters, Successive Approximation Analog to Digital Converters, Ramp Analog to Digital Converters, and Others), Resolution (8-Bit, 10-Bit, 12-Bit, 14-Bit, 16-Bit, and Others), and Application (Industrial, Consumer Electronics, Automotive, Healthcare, Telecommunication, and Others)

Apr 2024

Laser Distance Sensor Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Distance (Between 2 and 10 Meters, Between 11 and 100 Meters, Between 101 and 200 Meters, and Between 201 and 500 Meters), Accuracy (1 mm at 2 Sigma, 3 mm with 2 Sigma, and 5 mm at 2 Sigma), and End User (Manufacturing, Construction, Automotive and Robotics, Aerospace and Defense, Geospatial Industry, and Others)

Apr 2024

Rugged Tablet Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis By Type (Fully Rugged Tablet, Semi Rugged Tablet, and Ultra Rugged Tablet); Operating System (Android, Windows, and iOS); and Application (Aerospace & Defense, Automotive, Construction, Energy & Utilities, Manufacturing, Oil & Gas, and Others)

Apr 2024

Rear Door Heat Exchanger Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Type (Active and Passive) and End User (Data Center, IT and Telecommunication, Semiconductor, Education, Government, and Others)