The autotransfusion devices market is expected to grow from US$ 1,000.26 million in 2021 to US$ 1,331.99 million by 2028; it is estimated to grow at a CAGR of 4.2% from 2021 to 2028.

Organ transplantation is a surgical procedure performed in case of organ failure. Usually, organ transplantation is conducted for organs such as the heart, liver, and kidney; however, with rising cases of chronic diseases, transplantation is needed for other organs such as lungs, pancreas, cornea, and vascular tissues. These procedures generally take hours, and there is a lot of blood loss, and autotransfusion is one of the valuable methods to prevent blood loss. According to the United Network for Organ Sharing (UNOS), organ transplants conducted in the US have continuously increased, with over 41,000 transplants performed in 2021. Similarly, according to World Transplant Registry data, Spain accounted for 20% of all organ donations in the EU in 2019 and 6% of worldwide donations. Australia's organ donor rate has improved in recent years, rising to 21.8 donors per million population in 2019.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Autotransfusion Devices Market: Strategic Insights

Market Size Value in US$ 1,000.26 Million in 2021 Market Size Value by US$ 1,331.99 Million by 2028 Growth rate CAGR of 4.2% from 2021 to 2028 Forecast Period 2021-2028 Base Year 2021

Akshay

Have a question?

Akshay will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Autotransfusion Devices Market: Strategic Insights

| Market Size Value in | US$ 1,000.26 Million in 2021 |

| Market Size Value by | US$ 1,331.99 Million by 2028 |

| Growth rate | CAGR of 4.2% from 2021 to 2028 |

| Forecast Period | 2021-2028 |

| Base Year | 2021 |

Akshay

Have a question?

Akshay will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Similarly, Canada has 22.2 donors per million population and is steadily improving, partially attributed to the figure of "Donation Physicians" - intensive care doctors who are responsible for organ donation. According to the World Transplant Registry, China had 5,818 donors in 2019, or 4.1 per million population and India had 715 donors or 0.5 per million population in 2019. On the other hand, Russia had a slightly higher rate of 5.1 donors per million people. The public-private partnership in collaboration with transplant coordinators has made a significant contribution to the improvement of organ transplantation. Both developing and developed countries have seen an increase in organ transplant surgeries. For example, developing countries such as India and Singapore are emerging as medical tourism destinations in Asia Pacific. Countries are progressing in terms of providing better and advanced medical treatments. Thus, the rising need for organ transplantation is among the key factors driving the demand for transplant diagnostics such as autotransfusion devices.

The autotransfusion process involves the reinfusion of the patient's blood. Blood is collected from the peritoneal cavity or thorax region. The process can be carried out before surgery or during and after the surgery using the autotransfusion system. Medical procedures, like joint replacement, spinal surgeries, and cardiac, among others, require autotransfusion. It helps to reduce the risk of infection, and also it eliminates the problems and complications associated with the banking and administration of homologous donor blood. It helps to prevent the transmission of transfusion-related blood-borne diseases in patients.

Market Insights

Technological Developments in Autotransfusion Devices

Autotransfusion devices are usually deployed during long-hour surgeries, such as kidney transplantation, and in cases of emergencies. These surgeries are associated with the chances of excessive blood loss, which makes it difficult to make up the blood loss with new blood, especially in case of rare blood groups. Owing to the ample demand, the key players in the autotransfusion devices market offer advanced and fully automated autotransfusion devices that reduce human interventions. For instance, in April 2021, LivaNova PLC's B-Capta has been approved by the US Food and Drug Administration. During complex paediatric and adult cardiopulmonary bypass surgeries, this device aids in the rapid and accurate monitoring of venous and blood gas parameters. Similarly, in April 2019, BD launched their BD BACTEC quality control media worldwide to help identify contaminated platelet units during transfusions.

Moreover, many companies employed strategic activities such as acquisitions, partnership and others to capture the market. For instance, Medtronics acquired AV Medical Technologies, in October 2019. In December 2019, Getinge purchased Applikon Biotechnology, a global leader in the development and supply of innovative bioreactor systems from the laboratory to the industrial scale. Thus, such advancements are likely to bring new trends in the autotransfusion devices market in the coming years.

Application–Based Insights

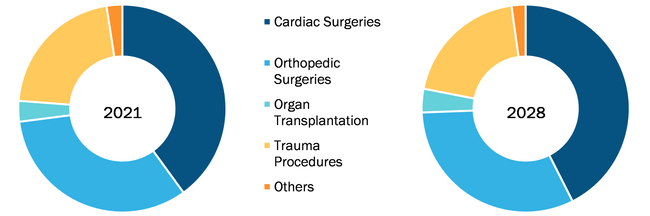

Based on application, the autotransfusion devices market is segmented into cardiac surgeries, orthopedic surgeries, organ transplantation, trauma procedures, and others. The cardiac surgeries segment held the largest share of the market in 2021, while the organ transplantation segment is also estimated to register the highest CAGR in the market during the forecast period.

Autotransfusion Devices Market, by Application – during 2021–2028

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

The autotransfusion devices market players adopt organic strategies such as product launch and expansion to expand their footprint and product portfolio globally and meet the growing demand. The developments by the companies in the autotransfusion devices market have been characterized as organic and inorganic developments. Various companies are focusing on organic strategies, such as product launch and expansion. Inorganic growth strategies witnessed in the autotransfusion devices market were partnerships and collaborations. These growth strategies have aided the autotransfusion devices market players in the expansion of their businesses and enhanced their geographic presence. Additionally, growth strategies such as acquisitions and partnerships helped in strengthening their customer base and increasing the product portfolio. The companies have maximized their growth with several inorganic strategies to enhance the autotransfusion devices market value and position in the autotransfusion devices market. Organic developments hold 66.67% of the total strategic developments in the autotransfusion devices market. Whereas inorganic strategies account for 33.33% of the growth of the companies.

The autotransfusion devices market has been segmented as follows:

The autotransfusion devices market is segmented based on type, application, and end user. Based on type, the autotransfusion devices market is bifurcated into products and accessories. The autotransfusion devices market, based on application, is segmented into cardiac surgeries, orthopedic surgeries, organ transplantation, trauma procedures, and others.

The autotransfusion devices market, based on end user, is divided into hospitals, specialty clinics, and ambulatory surgical centers.

Company Profiles in Autotransfusion Devices Market

- BD

- Braile Biomedica

- Fresenius SE & Co. KGaA

- Haemonetics Corporation

- LivaNova PLC

- Medtronic

- Redax S.p.A.

- SARSTEDT AG and Co. KG

- Teleflex Incorporated

- Zimmer Biomet

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Type, Application, End User

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

Argentina, Australia, Brazil, Canada, China, France, Germany, India, Italy, Japan, Mexico, RoAPAC, RoE, RoMEA, RoSCAM, Saudi Arabia, South Africa, South Korea, Spain, United Arab Emirates, United Kingdom, United States

Frequently Asked Questions

The accessories segment dominated the global autotransfusion devices market and held the largest revenue share of 55.66% in 2021.

The intraoperative autotransfusion systems segment dominated the global autotransfusion devices market and held the largest revenue share of 71.70% in 2021

Key factors that are driving the growth of this market are rapid increase in chronic diseases, rise in transplant, and difficulty in obtaining blood of rare groups.

The autotransfusion process involves the reinfusion of the patient's blood collected from the peritoneal cavity or thorax region. The process can be accomplished before surgery or during and after the surgery using the autotransfusion system. Medical procedures, such as joint replacement, spinal surgeries, and cardiac surgery require autotransfusion. It helps reduce the risk of infection, and abolishes the problems and complications associated with the banking and administration of homologous donor blood. It also prevents transmission of transfusion-related blood-borne diseases in patients.

The organ transplantation segment dominated the global autotransfusion devices market and held the largest revenue share of 3.22% in 2021.

The ambulatory surgery centers segment dominated the global autotransfusion devices market and accounted for the largest revenue share of 30.12% in 2021.

The autotransfusion devices market majorly consists of the players such as Medtronic; Fresenius SE & Co. KGaA; Teleflex Incorporated; BD; Zimmer Biomet; Braile Biomedica; Haemonetics Corporation; SARSTEDT AG and Co. KG; LivaNova PLC; Redax S.p.A. among others.

Global autotransfusion devices market is segmented by region into North America, Europe, Asia Pacific, Middle East & Africa and South & Central America. In North America, the U.S. is the largest market for autotransfusion devices. The US is estimated to hold the largest share in the autotransfusion devices market during the forecast period. The growth of the market is attributed to factors such as increasing prevalence of cancer in the US, and cancer awareness initiatives undertaken by local governments and global health organizations. In addition, growth involvement of rare blood groups, rising number of transplant procedures and rising prevalence of chronic diseases in the region stimulate the growth of autotransfusion devices market in North America. On the other hand, need for reinfusion of blood, and advancements in healthcare facilities and infrastructure in the Asia Pacific are expected to account for the fastest growth of the region during the coming years.

The List of Companies - Autotransfusion Devices Market

- Medtronic

- Fresenius SE & Co. KGaA

- Teleflex Incorporated

- BD

- Zimmer Biomet

- Braile Biomedica

- Haemonetics Corporation

- SARSTEDT AG and Co. KG

- LivaNova PLC

- Redax S.p.A.

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to Autotransfusion Devices Market

Mar 2022

Colonoscopes Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Product Type (Fiber Optic Colonoscopy Devices, Video Colonoscopy Devices); Application (Colorectal Cancer, Lynch Syndrome, Ulcerative Colitis, Crohn's Disease, Polyp); End User (Hospitals, Ambulatory Surgery Center, Others), and Geography

Mar 2022

Noninvasive Fat Reduction Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Technology (Cryolipolysis, Laser Lipolysis, Ultrasound, and Others), End User (Hospitals, Dermatology Clinics & Cosmetic Clinics, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Mar 2022

Medical Ultrasound Flow Meter Market

Size and Forecast (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Implementation Type (Clamp-On, Inline, and Others), Technology (Doppler, Transit Time, and Hybrid), Application (Heart and Lung Machines, Extracorporeal Membrane Oxygenation, Perfusion, Organ Transportation Systems, and Others), End User (Hospitals and Clinics, Ambulatory Surgical Centers, Research Laboratories, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Mar 2022

Rapid Test Kits Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Rapid Antigen Testing, Rapid Antibody Testing, and Others), Product (Over-the-Counter Rapid Testing Kit and Professional Rapid Testing Kit), Technology (Lateral Flow Assay, Solid Phase, Agglutination, Immunospot Assay, and Cellular Component-Based), Application (Blood Glucose Testing, Infectious Disease Testing, Pregnancy and Fertility, Cardiometabolic Testing, and Others), End User (Hospital and Clinics, Home Care, Diagnostics Centers, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Mar 2022

Osteoarthritis Therapy Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Therapy Type [Transcutaneous Electrical Nerve Stimulation (TENS), Occupational Therapy, Physical Therapy, Platelet-Rich Plasma Therapy and Stromal Vascular Fraction, Prolotherapy, and Others], Disease Indication (Knee Osteoarthritis, Spine Osteoarthritis, Foot and Ankle Osteoarthritis, Shoulder Osteoarthritis, Hand Osteoarthritis, and Others), End User (Hospitals & Clinics, Specialty Clinics, Ambulatory Surgical Centers, Homecare, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Mar 2022

Bariatric Surgeries Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Type [Adjustable Gastric Bands (AGB), Sleeve Gastrectomy, Gastric Bypass, Biliopancreatic Diversion with Duodenal Switch (BPD-DS), and Others], End User (Hospitals and Ambulatory Surgical Centers), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Mar 2022

Post-Acute Care Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Service Type (Skilled Nursing Facilities, Inpatient Rehabilitation Facilities, Long-Term Care Hospitals, Home Health Agency, and Others), Age (Elderly, Adult, and Others), Disease Conditions (Amputations, Wound Management, Brain Injury and Spinal Cord Injury, Neurological Disorders, and Others), and Geography

Mar 2022

Lung Cancer Therapy Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Therapy Type (Noninvasive and Minimally Invasive), Indication (Non-Small Cell Lung Cancer and Small Cell Lung Cancer), End User (Hospitals, Oncology Clinics, Research Centers, and Others), and Geography (North America, Europe, Asia Pacific, South & Central America, and Middle East & Africa)