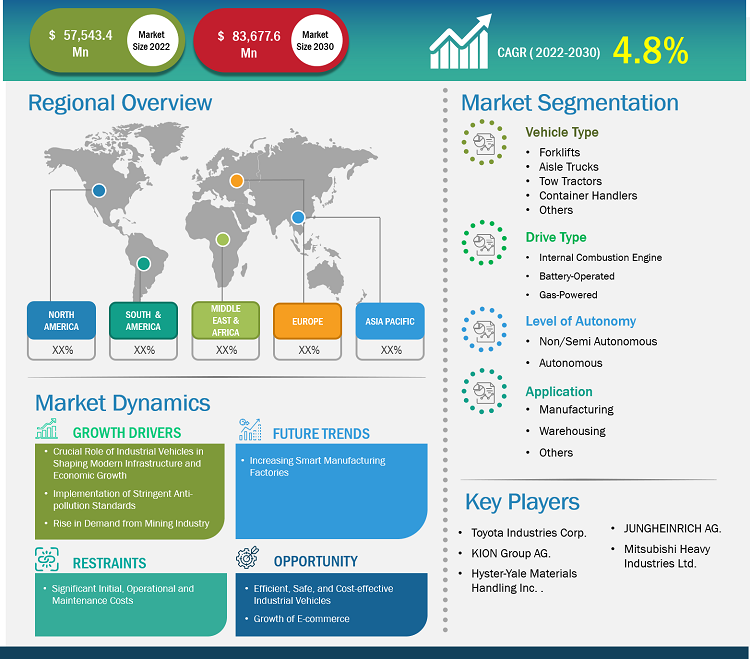

The industrial vehicles market was valued at US$ 57,543.40 million in 2022 and is projected to reach US$ 83,677.60 million by 2030; it is expected to register a CAGR of 4.8% from 2022 to 2030.

Analyst Perspective:

The report includes the global industrial vehicles market forecast by five major regions—North America, Europe, Asia Pacific (APAC), the Middle East & Africa (MEA), and South America (SAM). The global e-commerce industry is rising at a constant pace, which has encouraged companies to automate their warehouse with the help of several material-handling vehicles. The e-commerce industry is the major contributor to the growing demand for forklifts and other material-handling equipment. According to the United Nations Conference on Trade and Development (UNCTAD), in 2022, the global e-commerce industry's retail sales reached US$ 5.9 trillion, an increase of 9.26% compared to 2021. The average e-commerce spending per individual was ~US$ 737.51 in 2022. China has the largest e-commerce market across the globe. In 2022, China's e-commerce sales stood at US$ 1.3 trillion and are projected to reach US$ 2 trillion by 2025. Thus, the expansion of the e-commerce sector has created massive opportunities for the industrial vehicles market growth in Asia Pacific.

According to the World Industrial Vehicle Statistics Association (WITS), more than 2.34 million material-handling vehicles and equipment sales were recorded during 2021. The material handling industry saw a 43.0% increase in orders in 2021 compared to the previous year, 2020. Among the 2.34 million material handling units, ~68.8% or 1.61 million units were recorded as electric-powered forklifts. Electric forklift demand is increasing at a rapid pace with a surge in consumer popularity. With a surge in the number of orders, the demand for industrial vehicles such as forklifts, aisle trucks, and pallet trucks has increased. Thus, rising demand for material handling equipment and vehicles across the globe across the manufacturing sector drives the global industrial vehicles market growth.

Key factors bolstering the North America industrial vehicles market size include the expansion of logistics & transportation and e-commerce industries. Online shopping in the US has increased in recent years. Total US e-commerce sales reached US$ 1.03 trillion in 2022, an increase from US$ 518.5 billion in 2018. Many logistics giants in the market, such as UPS, FedEx, USPS, XPO Logistics, and Amazon, recognized the increasing demand for industrial vehicles in their warehouses. These companies have made significant investments in warehouse establishment and in automating their logistics operations. For instance, in November 2023, United Parcel Service opened the largest warehouse in Louisville, Kentucky, with an area of ~20 acres. This warehouse is made for storage and package handling, with a significant investment of US$ 79 million for the establishment of over 3,000 automated robots and industrial vehicles. These robots and industrial vehicles will handle several warehouse tasks, such as lifting and transportation of goods from one place to another, by reducing the requirement of manual labor.

Market Overview:

The industrial vehicles market encompasses a diverse range of specialized vehicles designed for use in various industrial applications. These vehicles are engineered to perform specific tasks within industrial settings, contributing to the efficiency, productivity, and safety of operations across different sectors. The market comprises a broad array of industrial vehicles specifically designed to meet the specific needs of manufacturing facilities, warehouses, construction sites, logistics operations, and other industrial environments. Industrial vehicles are also designed with a focus on addressing particular industrial challenges. This includes vehicles optimized for tasks such as material handling, heavy lifting, transportation of goods, excavation, and other specialized functions essential to industrial processes.

The industrial vehicles market is witnessing advancements in technology and innovation, with manufacturers constantly improving the capabilities and features of vehicles such as forklifts. This adaptability to evolving industry needs and technological advancements can bolster the market by attracting businesses seeking more efficient and advanced solutions for industrial mobility. Governments of various countries are investing in automating the manufacturing business in Europe. For instance, in July 2021, the UK government announced an investment of US$ 59.3 million (GBP 53 million) to drive the development of digital manufacturing technologies. Out of which, US$ 28.10 million (GBP 25 million) will be invested in setting up five new industry-sponsored research centers to support the development of cutting-edge digital solutions in order to transform manufacturing businesses. The remaining amount will be invested in a digital supply chain innovation hub and provided to 37 individual projects to digitalize and transform manufacturing supply chains. Thus, the growing government support to boost automation is expected to fuel the growth of the industrial vehicles market during the forecast period.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Industrial Vehicles Market: Strategic Insights

Market Size Value in US$ 57,543.40 million in 2022 Market Size Value by US$ 83,677.60 million by 2030 Growth rate CAGR of 4.8% from 2022 to 2030 Forecast Period 2022-2030 Base Year 2022

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Industrial Vehicles Market: Strategic Insights

| Market Size Value in | US$ 57,543.40 million in 2022 |

| Market Size Value by | US$ 83,677.60 million by 2030 |

| Growth rate | CAGR of 4.8% from 2022 to 2030 |

| Forecast Period | 2022-2030 |

| Base Year | 2022 |

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Market Driver:

Implementation of Stringent Anti-pollution Standards Drives Industrial Vehicles Market

Stringent anti-pollution standards, such as European (Stage V) and North American (Tier 4 Final), are being implemented for industrial vehicles across the globe. These standards, introduced on January 1, 2019, place additional restrictions on nitrogen oxide (NOx) and particulate pollutant emissions from non-road vehicles—including those used in agriculture, construction sites, and industrial settings. The driving force behind these regulations is the urgent need to address public health concerns, improve air quality, and mitigate the impact of vehicle emissions on climate change. One of the notable responses to these environmental challenges is the accelerated electrification of industrial vehicles. This shift toward electrification is driven by the imperative to meet the emission targets set by these stringent standards. Electric and hybrid alternatives are increasingly preferred where various site vehicles are used in the construction industry, including excavators, mobile cranes, diggers, and bulldozers, as well as agricultural vehicles such as tractors and combine harvesters.

Electric and hybrid industrial vehicles help manufacturers and operators comply with stringent emission standards. These vehicles produce significantly lower levels of NOx and particulate pollutants, aligning with the regulations set by Stage V in Europe and Tier 4 Final in North America. The reduction of harmful emissions from industrial vehicles contributes to the improvement of air quality, positively impacting public health. As urbanization continues to grow, the deployment of cleaner and more sustainable industrial vehicles becomes crucial for mitigating the impact of vehicle emissions on densely populated areas. Also, the rising awareness of environmental issues and the increasing emphasis on sustainability drive the demand for cleaner and more efficient industrial vehicles. Companies that prioritize environmentally friendly practices and comply with emission standards are likely to attract a broader customer base and secure long-term market viability. The transition to electric and hybrid alternatives not only ensures compliance with regulations but also aligns with the broader goals of improving air quality, addressing climate change, and meeting consumer preferences for sustainable practices. Thus, the implementation of stringent anti-pollution standards associated with industrial vehicles drives the market.

Segmental Analysis:

Based on vehicle type, the industrial vehicles market analysis has been carried out by considering the following segments: forklifts, aisle trucks, tow tractors, container handlers, and others (pellet trucks, reach trucks, order pickers, and stackers). Among these, the forklifts segment dominates the industrial vehicles market share owing to the rapid growth of the logistics & transportation sector. According to the Global Logistics Association, in 2021, the global logistics industry was valued at US$ 8.6 trillion and is expected to reach US$ 13.5 billion by 2027. In 2021, ~45% of the global logistics industry was concentrated in Asia Pacific. Also, the logistics industry in North America share was ~24% in 2020 across the globe, followed by Europe. Asia Pacific is the fastest-growing region for the industrial vehicles market, owing to rising e-commerce industry sales. In 2022, in Asia Pacific, the logistics sector spending reached ~US$ 4.9 trillion and is projected to record a CAGR of 5.9% from 2022 to 2027. China has the largest share in Asia Pacific, representing 54.1% of the logistics sector spending. This is primarily owing to economic growth in the manufacturing and automotive sectors. Industrial vehicles are widely used in the logistics sector for material handling from one place to another owing to the increasing e-commerce sector with favorable government policies and regional trade initiatives. Aisle trucks, tow tractors, container handlers, pallet trucks, reach trucks, order pickers, and stackers are also used in the e-commerce logistics industry across the globe.

Regional Analysis:

The scope of the industrial vehicles market report focuses North America (US, Canada, and Mexico), Europe (Spain, UK, Germany, France, Italy, and Rest of Europe), Asia Pacific (South Korea, China, India, Japan, Australia, and Rest of Asia Pacific), Middle East & Africa (South Africa, Saudi Arabia, UAE, and Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America).

In terms of revenue, Asia Pacific dominated the industrial vehicles marketshare. Europe is the second-largest contributor to the global industrial vehicles market, followed by North America. The North America industrial vehicles market is driven by increasing building & construction activities and rising sales of commercial vehicles. According to the American Automotive Policy Council (AAPC) Report, Fiat Chrysler Automobiles N.V., Ford Motors, and General Motors are heavily investing in the manufacturing of commercial vehicles in the US market. Automotive manufacturing in the US is the eighth largest economy globally and added ~US$ 2.64 trillion in value in 2021. Manufacturing motor vehicles and their parts represent 6% of the total manufacturing. The automotive sector contributes more than US$ 1.0 trillion to the US economy annually, representing 4.9% of GDP.

Growing building and construction investments, including government investment toward infrastructure developments, are driving the demand for industrial vehicles in North America. For instance, in August 2021, the US Ministry of Transportation and Infrastructure invested ~US$ 837.0 million for the highway expansion project between Western Canada in Alberta and BC. This project includes the construction of bridges and the expansion of two lanes to four-lane highways. Construction vehicles help the crews to perform several construction activities quickly and more efficiently. These vehicles are used for digging trenches to haul construction materials such as stone or aggregate using different construction vehicles. Various industrial vehicles are designed for specific tasks to perform multiple functions in the construction sites. Such infrastructure development projects require various industrial vehicles, including forklifts, cranes, road rollers, and dump trucks. Thus, the automotive industry is expanding with a rise in construction projects across different countries in North America, which drives the industrial vehicles market.

Key Player Analysis:

KION Group AG; Toyota Industries Corporation; MITSUBISHI HEAVY INDUSTRIES, LTD.; Komatsu Limited, Konecranes; Anhui Heli Co., Ltd.; Hyster-Yale Materials Handling, Inc.; Jungheinrich AG; Crown Equipment Corporation; and Clark Material Handling Company are among the key players covered in the industrial vehicles market report. The report includes growth prospects in light of current industrial vehicles market trends and driving factors influencing the market.

Recent Developments:

Inorganic and organic strategies such as mergers and acquisitions are highly adopted by companies in the industrial vehicles market. The market initiative is a strategy adopted by companies to expand their footprint across the world and to meet the growing customer demand. The market players present in the market are mainly focusing on product and service enhancements by integrating advanced features and technologies into their offerings. A few recent developments by key industrial vehicles market players are listed below:

|

|

|

September-2023 | Jungheinrich and Mitsubishi Logisnext Americas collaboratively launched Rocrich AGV Solutions. Through this solution, the company aims to provide automation solutions for warehouses and production facilities in the North American market. | North America |

July-2023 | Vedanta Aluminium, India's largest aluminum manufacturer, has increased its electric lithium-ion forklift fleet, making it the country's largest fleet. Vedanta Aluminium exhibits its commitment to sustainability by having 44 units functioning in Odisha and Chhattisgarh. | Asia Pacific |

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Type, Drive Type, and Application

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

KION Group AG; Toyota Industries Corporation; MITSUBISHI HEAVY INDUSTRIES, LTD.; Komatsu Limited, Konecranes; Anhui Heli Co., Ltd.; Hyster-Yale Materials Handling, Inc.; Jungheinrich AG; Crown Equipment Corporation; and Clark Material Handling Company are the key market players operating in the global industrial vehicle market.

The ongoing digital transformation of production processes and business models in industrial companies presents a significant growth trend for the industrial vehicle market in upcoming years. With the increasing interconnection of machinery and equipment, along with the integration of sensors, there is a wealth of data being generated. By harnessing the power of big data and artificial intelligence, these companies can achieve greater transparency, efficiency, and cost reduction.

The market for industrial vehicles in Asia Pacific is segmented into India, China, Japan, and South Korea. The market for industrial vehicles in Asia Pacific is likely to register the highest CAGR over the forecasted period, owing to the rapid development of construction projects. Investment by governments and companies in these countries' mining, oil & gas exploration, and renewable energy sectors is growing rapidly. The region supplies 10–15% of global oil and gas (O&G) needs.

The integration of autonomous industrial vehicles such as autonomous industrial vehicles (IVs) represents a transformative phase in the industrial vehicle market, fueled by improved efficiency, reduced maintenance costs, and enhanced safety records. Autonomous industrial vehicles, operating within geofenced topographies and adhering to specific rules, address one of the persistent challenges in industrial vehicle operations—wear and tear.

The modern economic landscape relies heavily on an expansive and intricate infrastructure network. This infrastructure encompasses a wide spectrum, ranging from the construction of roads and bridges to the efficient functioning of freight trains, cargo ships, internet provision, and electrical grids. In the US, the commitment to infrastructure development is evident in the substantial federal spending on highway and street projects, which reached approximately US$ 1.7 billion in 2021. The scale of the country's highway network is staggering, totaling four million statute miles—enough road to circumnavigate the Earth's equator 160 times. As urban centers undergo rapid expansion, the demand for infrastructural development is also increasing.

The List of Companies - Industrial Vehicles Market

- KION Group AG

- Toyota Industries Corporation

- MITSUBISHI HEAVY INDUSTRIES LTD

- Komatsu Limited

- Konecranes

- Anhui Heli Co Ltd

- Hyster-Yale Materials Handling Inc

- Jungheinrich AG

- Crown Equipment Corporation

- Clark Material Handling Company

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to Industrial Vehicles Market

Feb 2024

Connected Vehicle Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis By Technology (5G, 4G/LTE, 3G & 2G), Connectivity (Integrated, Tethered, Embedded), Application (Telematics, Infotainment, Driving assistance, Others) and Geography

Feb 2024

Hydrogen Fuel Cell Train Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Technology (Proton Exchange Membrane Fuel Cell, Phosphoric Acid Fuel Cell, and Others), Component (Hydrogen Fuel Cell Pack, Batteries, Electric Traction Motors, and Others), Rail Type (Passenger Rail, Commuter Rail, Light Rail, Trams, Freight, and Others) and Geography

Feb 2024

Automotive High Voltage Cable Market

Forecast to 2030 - Global Analysis by Vehicle Type [Battery Electric Vehicles (BEV), Plugin Hybrid Electric Vehicles (PHEV), and Plugin Hybrid Vehicles (PHV)], Conductor Type (Copper and Aluminum), and Core Type (Multi Core and Single Core)

Feb 2024

40-Ft Electric Boat Market

Forecast to 2030 - Global Analysis by Propulsion (Pure Electric, Hybrid, and Sail Electric), Battery Type (Nickel-Based, Lead-Acid, and Lithium-Ion), Application (Fishing, Recreational, and Others), Voltage Architecture (12 V, 24 V, and 48 V), and Boat Type (Trawlers, Catamarans, Yachts, Power Cruisers, and Others)