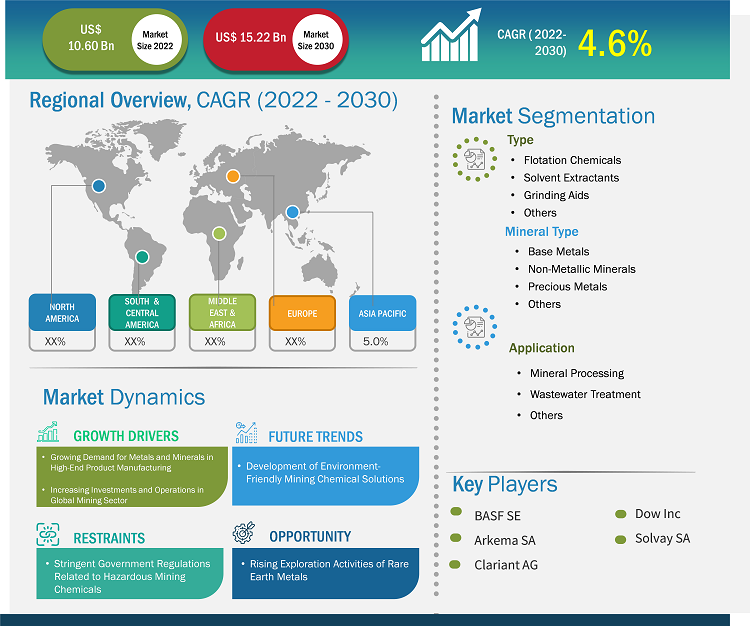

The market size is expected to grow from US$ 10.60 billion in 2022 to US$ 15.22 billion by 2030; it is estimated to register a CAGR of 4.6% from 2022 to 2030.

Market Insights and Analyst View:

The mining chemicals are used in applications such as mineral processing, wastewater treatment, and others. Different chemicals are used in the mining processes, depending on mineral and ore type. The mining chemicals are used in chemical processes to separate the desired mineral particles from the ore. They also help upgrade low mineral concentrations into pure metals. Different mining chemicals include flotation chemicals such as frothers, flocculants, depressants, collectors, and others; solvent extractants; grinding aids; and dust control or suppression chemicals. A few dust control or suppression chemicals used in the mining industry are calcium chloride, magnesium chloride, lignin sulfonate, asphalt emulsion, oil emulsion, and polymeric emulsion. Various benefits of mining chemicals, the strong growth of the mining industry, and the increase in demand for different metals and minerals drive the growth of the mining chemicals market.

Growth Drivers and Challenges:

Upsurging demand for metals and minerals in high-end product manufacturing drives the growth of the global mining chemicals market. The demand for metals, rare earth elements, and minerals in manufacturing high-end products is driven by advancements in the automotive, aerospace, and electronics industries. The higher demand for metals prompts increased mining activity to extract and produce the required raw materials, ultimately leading to extensive use of mining chemicals to access ore deposits, eliminate impurities, and fragment rocks. In addition, with the growing demand for metals, mining companies increasingly focus on improving safety measures and operational efficiency. This includes advancing mining explosive technologies and formulations that can optimize blasting operations. Precious metals such as gold and platinum are sought for their properties, such as conductivity in the electrical & electronics industry. In the automotive industry, sports and other high-end vehicles are manufactured using lightweight metals such as aluminum, titanium, and high-strength steel. The demand for aluminum has significantly increased in the past few years due to the rising production of lightweight materials for internal combustion engines and electric vehicles.

Stringent government regulations related to hazardous mining chemicals restrain the mining chemicals market growth. The mining industry operates in a complex web of national, regional, and local regulatory frameworks. Each jurisdiction may have its own set of laws, regulations, and guidelines related to mining operations, safety standards, environmental protection, and community engagement. Navigating these regulatory requirements can be time-consuming and resource-intensive for mining companies. In addition, obtaining permits for mining operations can be a lengthy and bureaucratic procedure in many countries. It is mandatory for mining companies to submit comprehensive applications, conduct environmental impact assessments, and fulfill specific criteria to secure necessary permits. Several governments have banned some hazardous chemicals, such as cyanide and sulfuric acid, from utilization in mining operations to mitigate adverse effects on human health and the environment.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Mining Chemicals Market: Strategic Insights

Market Size Value in US$ 10.60 billion in 2022 Market Size Value by US$ 15.22 billion by 2030 Growth rate CAGR of 4.6% from 2022 to 2030 Forecast Period 2022-2030 Base Year 2022

Shejal

Have a question?

Shejal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Mining Chemicals Market: Strategic Insights

| Market Size Value in | US$ 10.60 billion in 2022 |

| Market Size Value by | US$ 15.22 billion by 2030 |

| Growth rate | CAGR of 4.6% from 2022 to 2030 |

| Forecast Period | 2022-2030 |

| Base Year | 2022 |

Shejal

Have a question?

Shejal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Report Segmentation and Scope:

The "Global Mining Chemicals Market" is segmented on the basis of type, mineral type, application, and geography. Based on type, the market is segmented into flotation chemicals, solvent extractants, grinding aids, and others. The market for the flotation chemicals segment is further segmented into frothers, flocculants, depressants, collectors, and others. By mineral type, the global mining chemicals market is segmented into base metals, non-metallic minerals, precious metals, and others. By application, the market is segmented into mineral processing, wastewater treatment, and others. By geography, the market is segmented into North America (the US, Canada, and Mexico), Europe (Germany, France, Italy, the UK, Russia, and the Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and the Rest of Asia Pacific), the Middle East & Africa (South Africa, Saudi Arabia, the UAE, and the Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and the Rest of South & Central America).

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

Segmental Analysis:

Based on type, the mining chemicals market is segmented into flotation chemicals, solvent extractants, grinding aids, and others. The flotation chemicals segment held the largest market share in 2022, and the market for the segment is expected to grow significantly from 2022 to 2030. Flotation chemicals are mining chemicals used to adjust the floatability of minerals in the mineral froth flotation process. They can increase the difference in wettability between various minerals, thus achieving the separation of gangue minerals and useful minerals. Most of the minerals are hydrophilic. Therefore, it is necessary to artificially adjust the flotation behavior of ore for mineral separation. The concentrators can selectively increase the hydrophilic or hydrophobic nature of certain minerals by adding a flotation reagent. Further, grinding aids are also one of the major types in the market. The grinding aids are substances that result in increased grinding efficiency and reduced power consumption when added to the mill charge. Grinding aids help to reduce ore cohesion and adhesion throughout the grinding circuit, increasing throughput and eliminating production bottlenecks. As high-grade ore deposits are becoming depleted, mining companies are tapping into lower-quality ore. Accessing these ore bodies is often a complex and difficult process. Hence, advanced chemistries and more energies are needed to process and extract the most valuable elements of ore.

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

Regional Analysis:

Based on geography, the mining chemicals market is segmented into five key regions—North America, Europe, Asia Pacific, South & Central America, and the Middle East & Africa. Asia Pacific dominated the global market, and the regional market accounted for ~ US$ 6.01 billion in 2022. Asia Pacific marks the presence of major mining companies such as Mitsubishi Materials Corporation, Jiangxi Copper Co Ltd, Aluminum Corporation of China Ltd, Coal India Limited, China Molybdenum Co Ltd, BHP, and others. The region has ten major surface mining projects—Green mine (China), Sangatta mine (Indonesia), Heidaigou mine (China), Oyu Tolgoi Copper-Gold mine (Mongolia), Gevra OC mine (India), Letpadaung Copper mine (Myanmar), Li mine (Thailand), FTB Project (Thailand), and Pasir mine (Indonesia). According to the report published by the US Geological Survey in 2022, China was the largest supplier of 25 non-fuel mineral commodities to several countries globally in 2021. Additionally, China is the producer of 16 critical minerals out of 25 listed minerals. The demand for mining chemicals is directly proportional to the mining operations and mineral exploration activities in the region. Therefore, growth in mining operations bolsters the demand for mining chemicals in Asia Pacific. Middle East & Africa is another major contributor holding more than 13% of global market share. The rise in mining production rates for minerals, metals, and nonmetals in the Middle East & Africa drives the demand for mining chemicals across the region. A report published by the Mineral Council South Africa in 2022 revealed that the value of mining production in South Africa grew from US$ 57.0 billion in 2021 to US$ 61.0 billion in 2022. The value of total sales generated from iron ore in South Africa accounted for US$ 5.4 billion in 2022, representing a rise of 47.3% compared to 2019.

Industry Developments and Future Opportunities:

The following are initiatives taken by the key players operating in the mining chemicals market:

- In October 2023, BASF SE mining solutions launched two new product brands—Luprofroth and Luproset—to complement its growing flotation portfolio. Luprofroth is for growing frothers, whereas Luproset is for flotation modifiers. These brands aim to communicate the company's flotation portfolio clearly and consistently, demonstrating its commitment to innovation and becoming a full solution provider for the mining industry.

- In October 2023, BASF SE and the Catholic University of the North partnered to enhance research, development, and innovation in mining, fostering collaboration between academia, students, and industry experts and establishing a technical service laboratory at UCN.

- In November 2022, BASF SE and Moleaer formed a strategic partnership to enhance copper recovery in the mining industry. The partnership will leverage BASF SE's LixTRA leaching aid and Moleaer's nanobubble technology, aiming to double global copper demand by 2035.

- In October 2023, Clariant's Oil and Mining Services opened a state-of-the-art Eagle Ford Technology, Sales & Operations Center in San Antonio, TX, focusing on North American oilfield services.

- In December 2021, Solvay expanded its Mount Pleasant facility in Tennessee due to increasing demand for its ACORGA and ACORGA OPT copper solvent extraction products. The copper market is expected to grow, particularly in the construction, infrastructure, manufacturing, and automotive segments.

- In December 2022, Deepak Fertilisers and Petrochemicals Corporation Limited (DFPCL) demerged its fertilizer and mining chemicals business in a move described as a strategic shift from commodity to specialty. The proposed corporate restructuring is expected to help create strong independent business platforms within the larger DFPCL brand umbrella.

- In December 2021, Solvay launched an exclusive digital knowledge hub, the Mining Chemicals Handbook, which provides 24/7 access to relevant mining chemical application information.

COVID-19 Pandemic Impact:

The COVID-19 pandemic adversely affected almost all industries in various countries. Lockdowns, travel restrictions, and business shutdowns in North America, Europe, Asia Pacific (APAC), South & Central America, and the Middle East & Africa (MEA) hampered the growth of several industries, including the chemicals & materials industry. The shutdown of manufacturing units of companies disturbed global supply chains, manufacturing activities, and delivery schedules. Various companies reported delays in product deliveries and a slump in their product sales in 2020. The negative impact of the pandemic on the growth of the mining industry reduced the demand for mining chemicals. Mining projects and mineral exploration activities were halted and delayed due to the pandemic initially, hindering the market for mining chemicals. During the pandemic, supply chain disruptions, raw material and labor shortages, and operational difficulties created demand and supply gaps, adversely affecting the market growth.

Various industries are coming on track after supply constraints affecting these industries are resolving gradually. Moreover, the rising demand for mining chemicals is substantially promoting the growth of the mining chemicals market.

Competitive Landscape and Key Companies:

Orica Ltd, Kemira Oyj, BASF SE, Clariant AG, Dow Inc, AECI Ltd, Nouryon Chemicals Holding BV, Betachem Pty Ltd, Solvay SA, and Arkema SA are among the players operating in the global mining chemicals market. Players operating in the global market focus on providing high-quality products to fulfill customer demand. Also, they focus on adopting various strategies such as new product launches, capacity expansion, partnerships, and collaborations to stay competitive in the market.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Type, Mineral Type, and Application

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

Based on mineral type, base metal segment is the fastest-growing segment. Copper, aluminum, lead, zinc, and nickel are a few base metals., The rising demand for different metals from various industries drives the need for mining chemicals for metal processing.

Asia Pacific mining chemicals market is expected to surge due to growing mining activities and presence of mineral reserves in the region. Asia Pacific marks the presence of major mining companies such as Mitsubishi Materials Corporation, Jiangxi Copper Co Ltd, Aluminum Corporation of China Ltd, Coal India Limited, China Molybdenum Co Ltd, BHP, and others. The demand for mining chemicals is directly proportional to the mining operations and mineral exploration activities in the region.

The major players operating in the global mining chemicals market are Orica Ltd, BASF SE, Clariant AG, Solvay SA, and Arkema SA among others.

Based on the type, the flotation chemicals segment accounted for the largest revenue share, as it is the most flexible, effective, and convenient chemicals for controlling the flotation process. Flotation chemicals are mining chemicals used to adjust the floatability of minerals in the mineral froth flotation process.

The List of Companies - Mining Chemicals Market

- Orica Ltd

- Kemira Oyj

- BASF SE

- Clariant AG

- Dow Inc

- AECI Ltd

- Nouryon Chemicals Holding BV

- Betachem Pty Ltd

- Solvay SA

- Arkema SA

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to Mining Chemicals Market

Dec 2023

Construction Additives Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type [Cement Additives, Concrete Admixtures (Precast Concrete and Ready-Mix Concrete), Paints and Coatings Additives, Adhesives and Sealants Additives, Plastic Additives, Bitumen Additives, and Others], and Application (Residential, Commercial, Infrastructure, and Others)

Dec 2023

Oil Pollution Remediation Materials Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type [Physical Remediation (Booms, Skimmers, and Adsorbent Materials), Chemical Remediation (Dispersants and Solidifiers), Thermal Remediation, and Bioremediation]

Dec 2023

Greenhouse and Mulch Film Market

Size and Forecast (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Product Type (Greenhouse Films and Mulch Films), Material (LLDPE, LDPE, HDPE, EVA, PHA, PVC, PC, and Others), and Application (Vegetable Farming, Horticulture, Floriculture, and Others)

Dec 2023

Plastic for SLS 3D Printing Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Type (Polyamide, Thermoplastic Polyurethane (TPU), Polyether Ether Ketone (PEEK), and Others) and End-Use Industry (Healthcare, Aerospace & Defense, Automotive, Electronics, Others)

Dec 2023

Carbon Fiber-Based SMC BMC Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Resin Type (Polyester, Vinyl Ester, Epoxy, and Others) and End-Use Industry (Automotive, Aerospace, Electrical and Electronics, Building and Construction, and Others)

Dec 2023

Thermoplastic Adhesive Films Market

Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Material (Polyethylene, Polyamide, Thermoplastics Polyurethane, Polyester, Polypropylene, Polyolefins, Copolyamides, Copolyesters, and Others); Technology (Cast Film and Blown Film); Application (Membrane Films, Barrier Films, and Blackout Films); End Use (Textile, Automotive, Electrical and Electronics, Medical, Ballistic Protection, Lightweight Hybrid Construction, and Others)