Markt für Hämatologieanalysatoren und Reagenzien – Erkenntnisse durch globale und regionale Analyse – Prognose bis 2031

Historische Daten : 2021-2022 | Basisjahr : 2021 | Prognosezeitraum : 2023-2031Marktgröße und Prognose für Hämatologie-Analysegeräte und -Reagenzien (2021–2031), Analyse globaler und regionaler Anteile, Trends und Wachstumschancen – Berichtsabdeckung: Nach Produkt und Dienstleistung (Hämatologieprodukte und -dienstleistungen, Hämostaseprodukte und -dienstleistungen sowie Immunhämatologieprodukte und -dienstleistungen), Anwendung (Anämie, Blutkrebs, hämorrhagische Erkrankungen, infektionsbedingte Erkrankungen, Erkrankungen des Immunsystems und andere Anwendungen) und Endbenutzer (Krankenhauslabore, kommerzielle Dienstleister, staatliche Referenzlabore sowie Forschungs- und akademische Institute) und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00003261

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

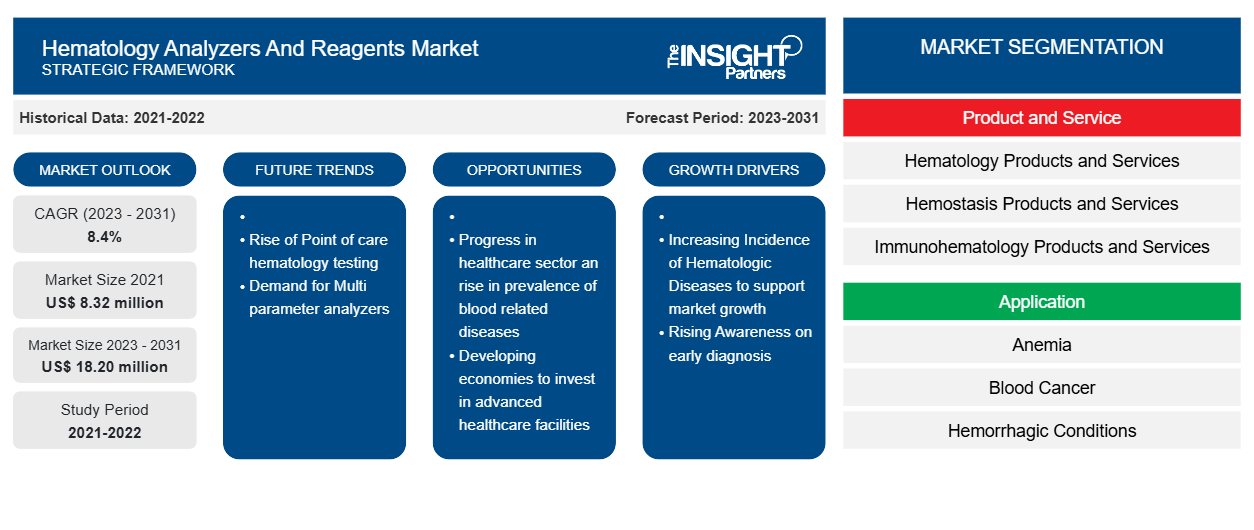

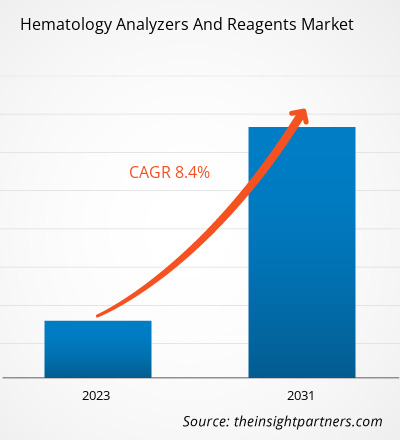

Die Größe des Marktes für Hämatologieanalysatoren und -reagenzien wurde auf 8,32 Millionen US-Dollar im Jahr 2021 und XX Millionen US-Dollar im Jahr 2023 geschätzt und soll bis 2031 18,20 Millionen US-Dollar erreichen; bis 2031 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 8,4 % erwartet. Die zunehmende Einführung intelligenter Point-of-Care-Geräte wird voraussichtlich weiterhin ein wichtiger Markttrend für Hämatologieanalysatoren und -reagenzien bleiben.

HÄMATOLOGIE-ANALYSATOREN UND REAGENZIEN Marktanalyse

Die Akteure auf dem Markt für Hämatologieanalysatoren und -reagenzien sind hart umkämpft und haben neue Produkte und Reagenzien auf den Markt gebracht. So brachte HORIBA Medical im Januar 2024 die neueste automatisierte Hämatologieplattform HELO 2.0 mit hohem Durchsatz auf den Markt. Die Plattform ist CE-zertifiziert (European In Vitro Diagnostic Devices Regulation, IVDR) und wartet derzeit auf die Zulassung durch die US-amerikanische Food and Drug Administration (FDA). HELO 2.0 ist die nächste Generation der High-End-Hämatologie-Reihe und wurde in Absprache mit Kunden entwickelt, um alle Anforderungen an vollautomatisierte Hämatologie mit hohem Durchsatz zu erfüllen. HELO 2.0 bietet eine hochflexible und effiziente modulare Hämatologielösung, die vollständig skaliert und konfiguriert werden kann, um den unterschiedlichen Anforderungen mittlerer bis großer Labore gerecht zu werden. Ebenso brachte Siemens Healthineers im Mai 2023 zwei Lösungen für Hämatologietests mit hohem Volumen auf den Markt: den Atellica HEMA 570 Analyzer und den Atellica HEMA 580 Analyzer. Die Fähigkeit des Labors, die Testergebnisse der Patienten schnell zu prüfen und freizugeben, wird durch die weit verbreitete Verwendung von CBC-Tests und den zunehmenden Personalmangel beeinträchtigt. Die Analysegeräte Atellica HEMA 570 und Atellica HEMA 580 bieten integrierte Automatisierung und Intelligenz, um die Arbeitsabläufe effizienter zu gestalten und schnellere Patientenergebnisse zu liefern. Die Einführung solcher neuer Produkte treibt das Wachstum des Marktes für Hämatologieanalysegeräte und -reagenzien voran.

HÄMATOLOGIE-ANALYSATOREN UND REAGENZIEN Marktübersicht

Das Wachstum des Marktes für Hämatologieanalysatoren und Reagenzien wird auf die zunehmende Zahl hämatologischer Erkrankungen und den technologischen Fortschritt bei Hämatologieanalysatoren zurückgeführt. Die hohen Preise für High-End-Systeme dürften das Wachstum des Marktes jedoch hemmen.

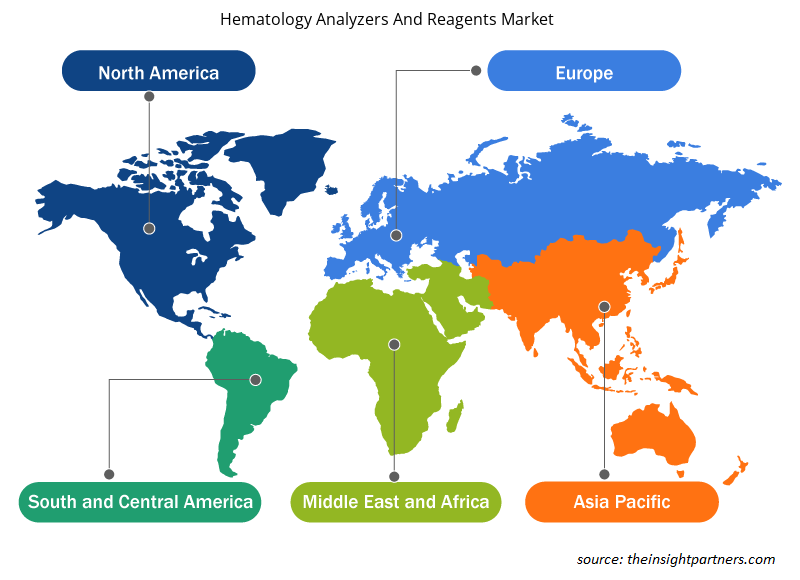

Der globale Markt für Hämatologieanalysatoren und -reagenzien ist nach Regionen unterteilt in Nordamerika, Europa, Asien-Pazifik, Mittlerer Osten und Afrika sowie Süd- und Mittelamerika. Nordamerika ist der größte Anteilseigner und Asien-Pazifik der am schnellsten wachsende Markt für Hämatologieanalysatoren und -reagenzien. Schätzungen zufolge wird der Markt für Hämatologieanalysatoren und -reagenzien in den USA den größten Anteil haben. Das Marktwachstum in den USA wird voraussichtlich aufgrund der steigenden Anzahl von Blutuntersuchungsverfahren, der hohen Prävalenz hämatologischer Erkrankungen, der steigenden Anzahl von Diagnose- und Blutuntersuchungszentren sowie des Zugangs zu gut entwickelter Infrastruktur und anderen Faktoren zunehmen.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlose Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Hämatologieanalysatoren und Reagenzien: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

HÄMATOLOGIEANALYSATOREN UND REAGENZIEN Markttreiber und Chancen

Zunehmende Häufigkeit hämatologischer Erkrankungen begünstigt den Markt

Laut den Centers for Disease Control and Prevention (CDC) werden in den USA jährlich etwa 12 von 100.000 Männern und 400 Jungen mit Hämophilie A geboren. Darüber hinaus berichtet die Leukemia & Lymphoma Society (LLS), dass in den USA alle 3 Minuten eine Person mit Lymphom, Leukämie oder Myelom diagnostiziert wird. Im Jahr 2023 werden in den USA voraussichtlich insgesamt 184.720 Menschen mit Leukämie, Lymphom oder Myelom diagnostiziert. Darüber hinaus werden neue Fälle von Lymphom, Leukämie und Myelom voraussichtlich 9,4 % der 1.958.310 neuen Krebsfälle ausmachen, die im Jahr 2023 in den USA diagnostiziert werden. Die steigende Prävalenz hämatologischer Erkrankungen erhöht den Bedarf an Bluttransfusionen sowie Blutbilduntersuchungen zur Überwachung der Normalität, was den Bedarf an Hämatologie-Analysegeräten und -Reagenzien weiter ansteigen lässt. Die zunehmende Zahl blutbedingter Erkrankungen treibt das Wachstum des Marktes für Hämatologieanalysatoren und -reagenzien voran.

Fortschritte im Gesundheitssektor und Anstieg der Prävalenz von Blutkrankheiten in Schwellenländern – eine Chance auf dem Markt für Hämatologieanalysatoren und -reagenzien

Die Zahl der hämatologischen Erkrankungen nimmt in Entwicklungsländern aufgrund der veränderten Lebensgewohnheiten der Bevölkerung deutlich zu. Darüber hinaus trägt die steigende Prävalenz anderer Gesundheitsprobleme aufgrund verringerter körperlicher Aktivitäten und steigender Stresslevel ebenfalls zum Anstieg der Fälle hämatologischer Erkrankungen in diesen Ländern bei. Entwicklungsländer sind bestrebt, ihre Gesundheitseinrichtungen und -dienste deutlich zu verbessern. So arbeitet beispielsweise die Hemophilia Federation India (HFI) als gemeinnützige Organisation eng mit der World Federation of Hemophilia (WFH) zusammen, um das Bewusstsein für Hämophilie und die verfügbaren erschwinglichen Behandlungen dafür zu schärfen und die Diagnose der Krankheit zu verbessern. Darüber hinaus ist das professionelle Team von RED LAPI bestrebt, die Diagnose und Behandlung von Hämophilie in Lateinamerika zu verbessern. Solche Entwicklungen auf dem Markt für Hämatologieanalysatoren und -reagenzien in Entwicklungsländern im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Lateinamerika bieten Chancen für das zukünftige Wachstum der Marktteilnehmer.

HÄMATOLOGIEANALYSATOREN UND REAGENZIEN Marktbericht Segmentierungsanalyse

Wichtige Segmente, die zur Ableitung der Marktanalyse für Hämatologieanalysatoren und -reagenzien beigetragen haben, sind Produkt und Service, Ursache, Anwendung und Endbenutzer.

- Basierend auf Produkt und Service ist der Markt für Hämatologieanalysatoren und -reagenzien in Hämatologieprodukte und -services, Hämostaseprodukte und -services sowie Immunhämatologieprodukte und -services segmentiert. Hämatologieprodukte und -services sind weiter unterteilt in Instrumente, Reagenzien und Verbrauchsmaterialien sowie Services. Ebenso ist das Segment Hämostaseprodukte und -services weiter unterteilt in Instrumente, Reagenzien und Verbrauchsmaterialien sowie Services. Das Segment Immunhämatologieprodukte und -services des Marktes für Hämatologieanalysatoren und -reagenzien ist ebenfalls weiter unterteilt in Instrumente, Reagenzien und Verbrauchsmaterialien sowie Services. Das Segment Hämatologieprodukte und -services hatte 2023 einen größeren Marktanteil.

- Nach Anwendung ist der Markt in Anämie, Blutkrebs, hämorrhagische Erkrankungen, infektionsbedingte Erkrankungen, Erkrankungen des Immunsystems und andere Anwendungen unterteilt. Das Segment Anämie hatte im Jahr 2023 den größten Marktanteil.

- In Bezug auf den Endverbraucher ist der Markt in Krankenhauslabore, kommerzielle Dienstleister, staatliche Referenzlabore sowie Forschungs- und akademische Institute segmentiert. Das Segment der Krankenhauslabore dominierte den Markt im Jahr 2023.

Hämatologieanalysatoren und Reagenzien Marktanteilsanalyse nach Geografie

Der geografische Umfang des Marktberichts über Hämatologieanalysatoren und -reagenzien ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Südamerika/Süd- und Mittelamerika.

In Nordamerika sind die USA der größte Markt für die Herstellung von Hämatologie-Analysegeräten und Reagenzien. Das Wachstum des US-Marktes wird vor allem durch günstige Forschungskonstellationen, eine steigende Nachfrage nach Blut und Blutbestandteilen sowie eine hohe Verbreitung automatisierter Hämatologie-Instrumente vorangetrieben.

Zunehmende Verbreitung hämatologischer Erkrankungen wie Leukämie, Hämophilie und Anämie in den USA. Die Schätzungen der American Cancer Society für Leukämie in den USA für 2024 lauten wie folgt:

- Etwa 62.770 neue Fälle von Leukämie (alle Arten) und 23.670 Todesfälle durch Leukämie (alle Arten)

- Etwa 20.800 neue Fälle von akuter myeloischer Leukämie (AML). Die meisten davon betreffen Erwachsene.

- Etwa 11.220 Todesfälle durch AML. Fast alle davon betreffen Erwachsene.

Das steigende Bewusstsein für eine frühzeitige Diagnose bei Patienten dürfte eine der wichtigsten Antriebskräfte für den Markt für Hämatologieanalysatoren und -reagenzien sein. Der asiatisch-pazifische Raum dürfte in den kommenden Jahren die höchste durchschnittliche jährliche Wachstumsrate aufweisen.

Regionale Einblicke in den Markt für Hämatologieanalysatoren und Reagenzien

Die regionalen Trends und Faktoren, die den Markt für Hämatologieanalysatoren und -reagenzien während des Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie für Hämatologieanalysatoren und -reagenzien in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für Hämatologieanalysatoren und -reagenzien

Umfang des Marktberichts zu Hämatologieanalysatoren und Reagenzien

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2021 | 8,32 Millionen US-Dollar |

| Marktgröße bis 2031 | 18,20 Millionen US-Dollar |

| Globale CAGR (2023 - 2031) | 8,4 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2023–2031 |

| Abgedeckte Segmente |

Nach Produkt und Service

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte für Hämatologieanalysatoren und -reagenzien: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Hämatologieanalysatoren und -reagenzien wächst rasant, angetrieben durch die steigende Endverbrauchernachfrage aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten auf dem Markt für Hämatologieanalysatoren und -reagenzien tätigen Unternehmen sind:

- Klinische Diagnoselösungen, Inc.

- Shenzhen Mindray Biomedizinische Elektronik Co., Ltd.

- Danaher

- BIO-RAD LABORATORIES INC.

- Abbott

- Diatron

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für Hämatologieanalysatoren und -reagenzien

Marktnachrichten und aktuelle Entwicklungen zu Hämatologieanalysatoren und Reagenzien

Der Markt für Hämatologieanalysatoren und -reagenzien wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Im Folgenden finden Sie eine Liste der Entwicklungen und Strategien auf dem Markt für Hämatologieanalysatoren und -reagenzien:

- HORIBA Medical hat neue Produkte seiner Hämatologie-Produktfamilie Yumizen auf den Markt gebracht. Das Unternehmen stellte zwei kompakte Hämatologie-Tischanalysatoren vor, Yumizen H500 und Yumizen H550, die eine verbesserte Leistung, neue Funktionen und mehr Vorteile bieten. Diese Analysatoren wurden entwickelt, um einen schnellen und umfassenden Hämatologiebericht mit einem hohen Durchsatz von 60 Tests pro Stunde, 40 Röhrchen-Autonomie mit kontinuierlicher Beladung, dringendem manuellen Modus sowie Multianalysemodi und Sampling für laufende Proben zu liefern. (Quelle: HORIBA Medical, 2022)

- Mindray hat eine revolutionäre Hämatologie-Analysegeräteserie auf den Markt gebracht, die BC-700-Serie, die sowohl Tests des kompletten Blutbilds (CBC) als auch der Blutsenkungsgeschwindigkeit (ESR) umfasst. Die Serie umfasst zwei Modelle mit offenen Fläschchen, BC-700/BC-720, und zwei Modelle mit Autoloader, BC-760/BC-780. Diese Serie wurde entwickelt, um Labore mit mittlerem Volumen mit fortschrittlichen Diagnosetechnologien auszustatten, die in Premiumprodukten zum Einsatz kommen. (Quelle: Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Pressemitteilung, 2022)

Marktbericht zu Hämatologieanalysatoren und Reagenzien – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für Hämatologieanalysatoren und -reagenzien (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Projekts abgedeckt sind

- Marktdynamik wie Treiber, Beschränkungen und wichtige Chancen

- Wichtige Zukunftstrends

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Globale und regionale Marktanalyse mit wichtigen Markttrends, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen

- Detaillierte Firmenprofile

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Historische Analyse (2 Jahre), Basisjahr, Prognose (7 Jahre) mit CAGR

- PEST- und SWOT-Analyse

- Marktgröße Wert/Volumen – Global, Regional, Land

- Branchen- und Wettbewerbslandschaft

- Excel-Datensatz

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends

Exklusive Berichtsrabatte freischalten

Jetzt anfragen

Kostenlose Probe anfordern für - Markt für Hämatologieanalysatoren und Reagenzien

Kostenlose Probe anfordern für - Markt für Hämatologieanalysatoren und Reagenzien