Acteurs clés du marché des systèmes de protonthérapie et prévisions jusqu'en 2031

Taille et prévisions du marché des systèmes de protonthérapie (2021-2031), part de marché mondiale et régionale, tendances et analyse des opportunités de croissance : Couverture du rapport : Par type d’installation (salle unique et salles multiples), application (cancer du cerveau et du système nerveux central, cancer de la tête et du cou, cancer de la prostate, cancer du sein, cancer du poumon, cancer gastro-intestinal et autres) et zone géographique (Amérique du Nord, Europe, Asie-Pacifique, Amérique du Sud et centrale, Moyen-Orient et Afrique)

- Statut : Données publiées

- Code du rapport : TIPHE100001160

- Catégorie : Sciences de la vie

- Nombre de pages : 150

- Formats de rapport disponibles :

- Date de dernière mise à jour : May 30, 2024

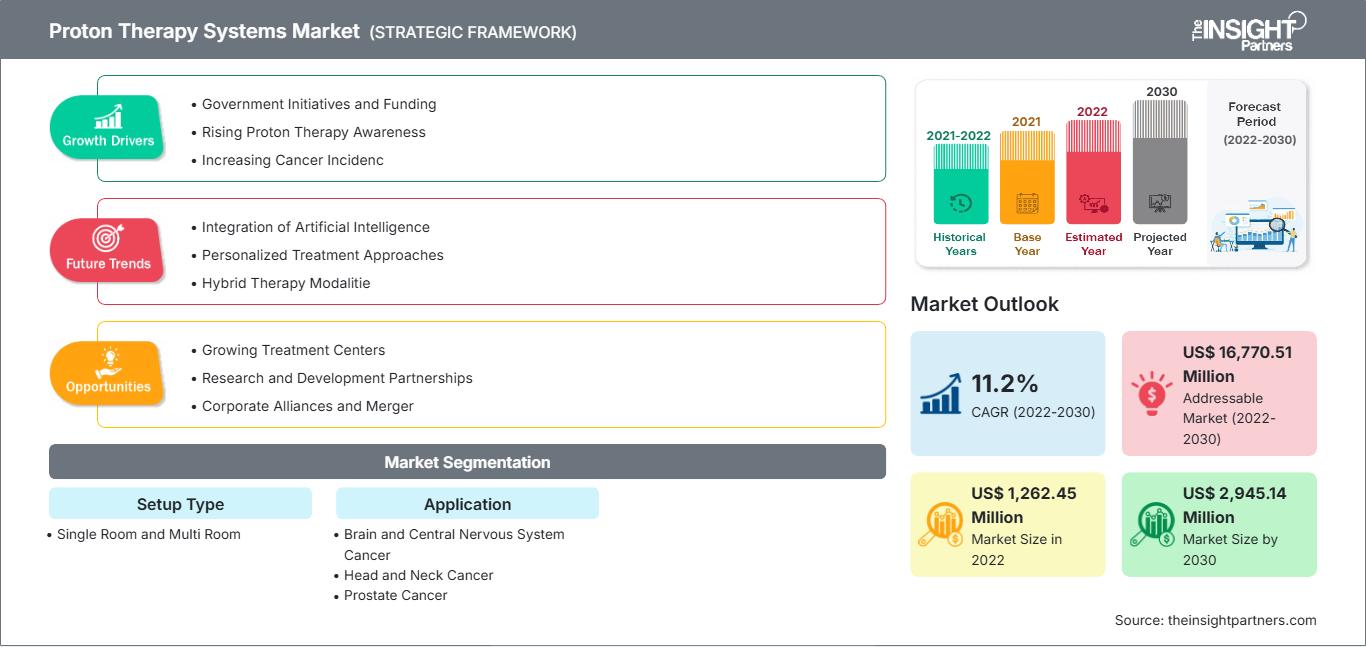

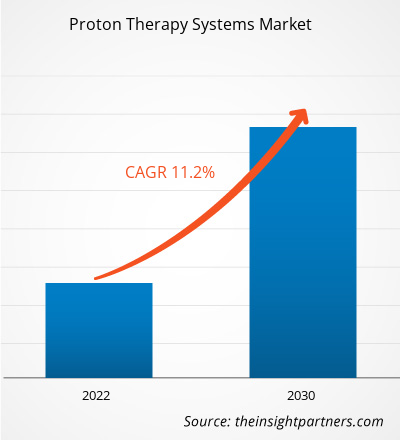

Le marché des systèmes de protonthérapie devrait atteindre 3 012 millions de dollars américains d’ici 2031. Ce marché devrait enregistrer un TCAC de 12,2 % entre 2025 et 2031.

Perspectives du marché et point de vue des analystes :

Les prévisions du marché des systèmes de protonthérapie peuvent aider les acteurs de ce marché à définir leurs stratégies de croissance.

Un système de protonthérapie est un dispositif médical de pointe utilisé pour administrer un traitement de radiothérapie de haute précision aux tumeurs. Ces systèmes, de grande taille, comprennent un accélérateur (cyclotron), un système de transport du faisceau, un système de sélection de l'énergie et un portique rotatif d'irradiation. Grâce à son efficacité dans le traitement de certains types de cancer, la protonthérapie connaît une demande croissante à l'échelle mondiale. La demande accrue de traitements de pointe, liée à l'augmentation de l'incidence du cancer, et le soutien gouvernemental croissant aux centres de protonthérapie stimulent la croissance du marché des systèmes de protonthérapie. Cependant, le coût élevé et l'encombrement important de ces systèmes freinent cette croissance. Par ailleurs, l'adoption croissante d'approches thérapeutiques personnalisées, associée aux progrès technologiques, devrait engendrer de nouvelles tendances sur le marché des systèmes de protonthérapie dans les années à venir.

Facteurs de croissance :

La demande croissante de traitements de pointe, conjuguée à l'augmentation de l'incidence du cancer, stimule la croissance du marché.

Selon le Centre international de recherche sur le cancer (CIRC), les cancers du poumon, du sein et de la prostate présentaient les taux d'incidence les plus élevés en 2022. Ces maladies ont des taux standardisés selon l'âge de 23,6, 47,1 et 29,4 cas pour 100 000 habitants, respectivement. D'après les estimations du CIRC, le nombre total de cas de cancer devrait passer de 19,98 millions en 2022 à 23,71 millions en 2030 et à 30,97 millions en 2045. Divers cancers, tels que les cancers de la tête et du cou (nez, bouche, œil et larynx) et les cancers du cerveau, nécessitent des traitements précis, ce qui engendre une forte demande pour des approches thérapeutiques avancées comme la protonthérapie à modulation d'intensité (IMPT). Dans les radiothérapies conventionnelles, comme la radiothérapie aux rayons X, les tissus sains entourant la tumeur reçoivent également une dose de rayonnement, ce qui provoque des effets secondaires et peut induire des cancers secondaires. Cependant, la protonthérapie permet de traiter efficacement les tumeurs complexes du cerveau et de la région cervico-faciale tout en minimisant les dommages collatéraux aux tissus environnants. Ainsi, la forte prévalence du cancer et la demande croissante de traitements de pointe stimulent la demande en radiothérapie protonique, alimentant la croissance du marché des systèmes de protonthérapie.

Personnalisez ce rapport selon vos besoins.

Bénéficiez d'une PERSONNALISATION GRATUITEMarché des systèmes de protonthérapie : Perspectives stratégiques

-

Découvrez les principales tendances du marché présentées dans ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Retenue:

Les systèmes de protonthérapie sont coûteux et nécessitent une grande surface.

Un système de protonthérapie est un dispositif médical de pointe utilisé pour le traitement des tumeurs par irradiation de haute précision. Cet appareil imposant se compose d'un accélérateur (cyclotron), d'un système de transport du faisceau, d'un système de sélection de l'énergie et d'un portique rotatif d'irradiation, ce qui engendre des surfaces importantes et un coût élevé. Selon l'Université de Pennsylvanie (Oncolink), les cyclotrons des systèmes de protonthérapie peuvent peser jusqu'à 200 tonnes et mesurer de 1,8 à 3,7 mètres de diamètre. Le portique peut peser jusqu'à 100 tonnes et mesurer 12 mètres de diamètre. D'après une étude publiée en 2021 dans IOPscience, même une configuration compacte (salle unique) occupe une surface de 100 m², tandis que les systèmes de protonthérapie multi-salles nécessitent une surface de 200 à 400 m².

De plus, les systèmes de protonthérapie nécessitent d'importants investissements. Par exemple, un système monosalle peut coûter entre 30 et 50 millions de dollars américains. Le coût des systèmes multi-portiques peut atteindre 300 millions de dollars américains, et ils ne sont généralement installés que dans les grands hôpitaux et les centres hospitaliers universitaires. Par conséquent, les exigences élevées en matière d'investissement et les vastes surfaces d'installation figurent parmi les facteurs qui freinent la croissance du marché des systèmes de protonthérapie.

Segmentation et portée du rapport :

L'analyse du marché des systèmes de protonthérapie a été réalisée en considérant les segments suivants : type d'installation et application.

Le marché est segmenté, selon le type d'installation, en salles uniques et salles multiples. Le segment des salles multiples détenait la plus grande part de marché des systèmes de protonthérapie en 2022. Par ailleurs, le segment des salles uniques devrait enregistrer un TCAC plus rapide au cours de la période de prévision.

Le marché, par application, est segmenté en cancers du cerveau et du système nerveux central, cancers de la tête et du cou, cancers de la prostate, cancers du sein, cancers du poumon, cancers gastro-intestinaux et autres. Le segment des cancers du cerveau et du système nerveux central détenait la plus grande part de marché des systèmes de protonthérapie en 2022 et devrait enregistrer le taux de croissance annuel composé (TCAC) le plus élevé au cours de la période de prévision.

Analyse régionale :

En termes de répartition géographique, le rapport sur le marché des systèmes de protonthérapie couvre l'Amérique du Nord, l'Europe, l'Asie-Pacifique, l'Amérique du Sud et centrale, ainsi que le Moyen-Orient et l'Afrique. En 2022, l'Amérique du Nord détenait la plus grande part de marché. L'adoption croissante des dispositifs médicaux les plus récents, la forte prévalence du cancer et les innovations des principaux acteurs contribuent à la croissance du marché des systèmes de protonthérapie en Amérique du Nord. Selon les estimations de l'American Cancer Society, les États-Unis ont enregistré environ 1,95 million de nouveaux cas de cancer et environ 610 000 décès liés à cette maladie en 2023, soit une augmentation significative par rapport aux 1,6 million de cas et 600 000 décès recensés en 2020. D'après le Particle Therapy Co-Operative Group, fin 2023, les États-Unis comptaient le plus grand nombre de systèmes de protonthérapie au monde, avec 46 centres de traitement.

Aperçu régional du marché des systèmes de protonthérapie

Les analystes de The Insight Partners ont analysé en détail les tendances régionales et les facteurs influençant le marché des systèmes de protonthérapie tout au long de la période prévisionnelle. Cette section aborde également les segments de marché et la répartition géographique des systèmes de protonthérapie en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu'en Amérique du Sud et centrale.

Rapport sur le marché des systèmes de protonthérapie : portée

| Attribut du rapport | Détails |

|---|---|

| Taille du marché en 2024 | XX millions de dollars américains |

| Taille du marché d'ici 2031 | 3 011,5 millions de dollars américains |

| TCAC mondial (2025 - 2031) | 12,2% |

| Données historiques | 2021-2023 |

| Période de prévision | 2025-2031 |

| Segments couverts |

Par type de configuration

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché des systèmes de protonthérapie : comprendre son impact sur la dynamique commerciale

Le marché des systèmes de protonthérapie connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux. Cette demande est alimentée par l'évolution des préférences des consommateurs, les progrès technologiques et une meilleure connaissance des avantages du produit. Face à cette demande grandissante, les entreprises diversifient leur offre, innovent pour répondre aux besoins des consommateurs et tirent parti des tendances émergentes, ce qui contribue à la croissance du marché.

- Obtenez un aperçu des principaux acteurs du marché des systèmes de protonthérapie

Évolutions du secteur et perspectives d'avenir :

Voici quelques développements stratégiques opérés par les principaux acteurs du marché des systèmes de protonthérapie, tels que présentés dans les communiqués de presse des entreprises :

- En janvier 2024, OncoRay a lancé le prototype d'un système de protonthérapie guidé par IRM corps entier, permettant le suivi en temps réel des tumeurs mobiles grâce à l'imagerie par résonance magnétique (IRM) pendant le traitement. L'IRM facilite la visualisation des tumeurs avec un contraste accru, ce qui constitue son principal avantage par rapport aux modalités d'imagerie conventionnelles. Ce meilleur contraste permet de mieux délimiter la tumeur par rapport aux tissus sains environnants et de définir avec une plus grande précision le volume à irradier.

- En décembre 2023, le groupe médical HKSH a inauguré un nouveau centre de protonthérapie au sein du HKSH Eastern Medical Centre, situé à A Kung Ngam, Shau Kei Wan, Hong Kong. Ce nouveau centre est doté d'un système de protonthérapie de pointe et de deux salles de traitement ultramodernes. Le système comprend deux portiques de protonthérapie semi-rotatifs, un système de transport de faisceau de dernière génération et un accélérateur de particules à synchrotron.

Paysage concurrentiel et entreprises clés :

Varian Medical Systems Inc, Sumitomo Heavy Industries Ltd, Hitachi Ltd, Ion Beam Applications SA, Mevion Medical Systems, Provision Healthcare LLC, ProTom International, Optivus Proton Therapy Inc, Advanced Oncotherapy plc et B dot Medical Inc figurent parmi les entreprises majeures présentées dans le rapport sur le marché des systèmes de protonthérapie. Ces sociétés s'attachent à développer de nouvelles technologies, à moderniser leurs produits existants et à étendre leur présence géographique afin de répondre à la demande croissante des consommateurs à travers le monde.

Analyste de recherche chevronnée, Mme Mrinal cumule plus de 8 ans d'expérience en veille stratégique et conseil dans le secteur des sciences de la vie. Dotée d'un esprit stratégique et d'un engagement indéfectible envers l'excellence, elle a acquis une expertise approfondie en prévision pharmaceutique, en évaluation des opportunités de marché et en élaboration de benchmarks sectoriels. Son travail consiste à fournir des informations exploitables permettant à ses clients de prendre des décisions stratégiques éclairées.

La principale force de Mme Mrinal réside dans sa capacité à traduire des données quantitatives complexes en données décisionnelles pertinentes. Son sens de l'analyse est essentiel à l'élaboration de stratégies de mise sur le marché (GTM) et à la découverte d'opportunités de croissance dans les secteurs pharmaceutique et des dispositifs médicaux. Consultante de confiance, elle s'attache constamment à rationaliser les processus et à établir les meilleures pratiques, favorisant ainsi l'innovation et l'efficacité opérationnelle de ses clients.

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires