Dispositivi iperplastici prostatici benigni Strategie di mercato, principali attori, opportunità di crescita, analisi e previsioni entro il 2028

Dati storici : 2021-2024 | Anno base : 2025 | Periodo di previsione : 2026-2034Previsioni di mercato dei dispositivi per l'iperplasia prostatica benigna fino al 2028 - Impatto del COVID-19 e analisi globale per prodotto (resettoscopi, laser urologici, dispositivi di ablazione a radiofrequenza, stent prostatici e impianti), tipo di procedura (terapia transuretrale a microonde, resezione transuretrale della prostata, ablazione transuretrale con ago della prostata, chirurgia laser, chirurgia urolift e altri) e utente finale (ospedali, cliniche, centri chirurgici ambulatoriali e altri) e geografia

- Stato : Pending

- Codice del report : TIPRE00025704

- Categoria : Scienze della vita

- Numero di pagine : 150

- Formati di report disponibili :

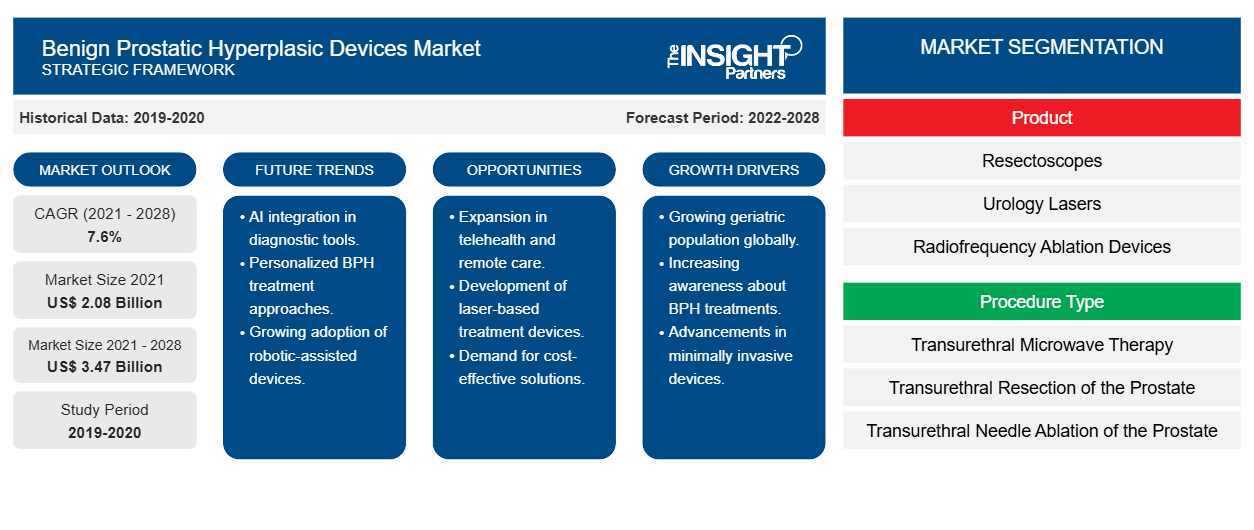

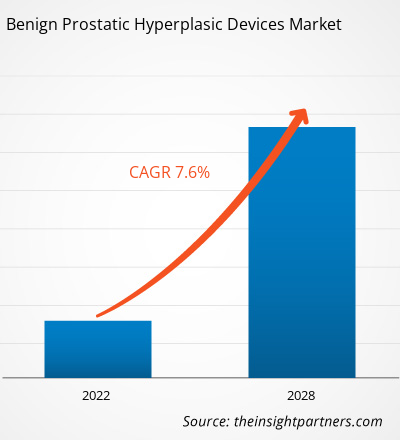

[Rapporto di ricerca] Si prevede che il mercato dei dispositivi per l'iperplasia prostatica benigna crescerà da 2.078,78 milioni di dollari nel 2021 a 3.467,31 milioni di dollari entro il 2028; si stima che crescerà a un CAGR del 7,6% dal 2022 al 2028.

Iperplasia prostatica benigna (IPB) è un ingrossamento della prostata causato da una crescita cellulare eccessiva nella prostata. L'IPB è una condizione benigna (non cancerosa) della prostata. Le condizioni non cancerose di solito non sono fatali e non si diffondono (metastatizzano) ad altre parti del corpo. L'IPB non aumenta il rischio di cancro alla prostata; a meno che non manifesti sintomi, l'IPB non è considerata un problema di salute. Quasi tutti gli uomini avranno una crescita della prostata entro i 70 anni. Invecchiare, avere più grasso sulla pancia (noto anche come obesità addominale) e non fare abbastanza esercizio fisico aumentano il rischio di sviluppare l'IPB.

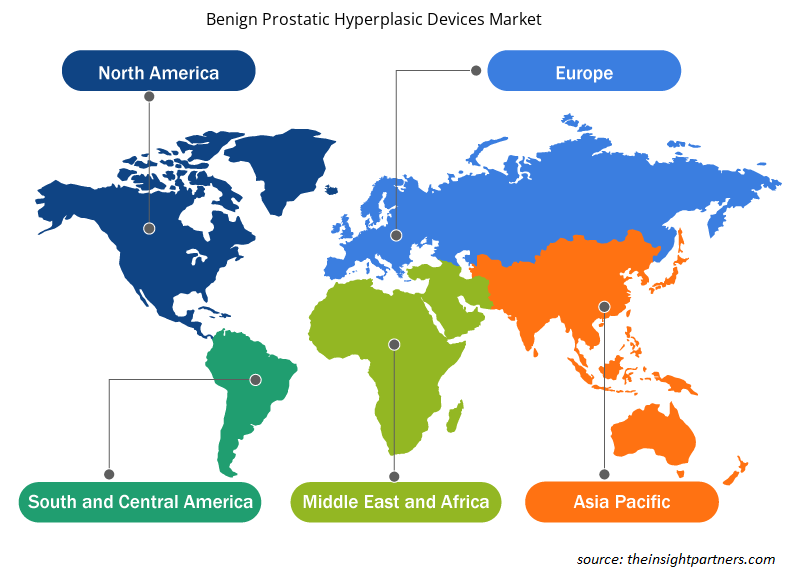

Il mercato dei dispositivi per iperplasia prostatica benigna è segmentato in prodotto, tipo di procedura, utente finale e area geografica. Per area geografica, il mercato è ampiamente segmentato in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud e Centro America. Questo rapporto offre approfondimenti e analisi approfondite del mercato, sottolineando parametri quali tendenze di mercato, dinamiche di mercato e analisi competitiva dei principali attori del mercato a livello mondiale.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato dei dispositivi per l'iperplasia prostatica benigna: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Approfondimenti di mercato

L'aumento della prevalenza dell'iperplasia prostatica benigna, unito all'aumento dei fattori di rischio e all'incremento degli investimenti, dei fondi e delle sovvenzioni per la ricerca sul trattamento dell'iperplasia prostatica benigna, guideranno il mercato dei dispositivi per l'iperplasia prostatica benigna.

Secondo il National Center for Biotechnology Information (NCBI), la BPH è uno dei disturbi più comuni negli uomini anziani e la causa principale dei sintomi del tratto urinario inferiore (LUTS). Dopo i 40 anni, la prevalenza della BPH aumenta, raggiungendo un picco del 60% all'età di 90 anni. Secondo gli studi autoptici, la prevalenza istologica della BPH è rispettivamente dell'8%, del 50% e dell'80% nella quarta, sesta e nona decade di vita di un uomo. È stato anche dimostrato che la vecchiaia è un fattore di rischio per l'insorgenza e la progressione della BPH clinica in studi osservazionali condotti in Europa, negli Stati Uniti e in Asia. Secondo le statistiche del Krimpen and Baltimore Longitudinal Study of Aging, la prostata cresce a un tasso del 2,0%-2,5% all'anno negli uomini anziani. L'ingrossamento continuo della prostata è un fattore di rischio per lo sviluppo di LUTS e le prostate più grandi sono associate a un ingrossamento prostatico benigno (BPE), che innesca il rischio di sviluppare BPH clinica e incontinenza urinaria.NCBI), BPH is one of the most common disorders in older men and the leading cause of lower LUTS). After the age of 40, the prevalence of BPH rises, reaching a peak of 60% by the age of 90. According to autopsy studies, the histological prevalence of BPH is 8%, 50%, and 80% in the fourth, sixth, and ninth decades of a man's life, respectively. Old age has also been shown to be a risk factor for the onset and progression of clinical BPH in observational studies conducted in Europe, the US, and Asia. According to statistics from the Krimpen and Baltimore Longitudinal Study of Aging, the prostate grows at a rate of 2.0% to 2.5% per year in older men. Continued prostate enlargement is a risk factor for developing LUTS, and larger prostates are associated with a benign prostatic enlargement (BPE), which triggers the risk of developing clinical BPH and urine incontinence.

Secondo i dati NCBI, si è scoperto che l'aumento dell'adiposità ha una correlazione positiva con il volume della prostata. In numerosi gruppi di studio, il peso corporeo, l'indice di massa corporea (BMI) e la circonferenza della vita hanno mostrato una correlazione positiva con il volume della prostata. Inoltre, i dati epidemiologici mostrano che l'obesità può aumentare la necessità di un intervento chirurgico per la BPH e di iniziare il trattamento per la BPH.NCBI data, increased adiposity is found to have a positive correlation with prostate volume. In numerous study groups, body weight, body mass index (BMI), and waist circumference have been seen to have a positive correlation with prostate volume. Additionally, epidemiological data shows obesity may raise the necessity of BPH surgery and initiating BPH treatment.

Secondo l'American Journal of Men's Health (AJMH), nel 2019, a livello globale, ci sono stati 11,26 milioni di nuovi casi e 1,86 milioni di anni vissuti con disabilità (YLD) dovuti a BPH nel 2019. L'incidenza di BPH è aumentata del 105,7% e YLD è aumentata del 110,6% in tutto il mondo durante il periodo 1990-2019. L'incidenza assoluta e i numeri YLD sono aumentati notevolmente in tutto il mondo durante questo periodo, principalmente a causa dell'aumento della popolazione e dell'invecchiamento. Secondo le stime della UROLOGY FOUNDATION, nel Regno Unito, la prevalenza di BPH aumenta dal 50% tra gli uomini di età compresa tra 50 e 60 anni al 90% tra gli uomini di età pari o superiore a 80 anni. Alcuni uomini sviluppano una ritenzione acuta improvvisa, ovvero l'incapacità di urinare. L'opzione di trattamento per la BPH include interventi chirurgici come la resezione transuretrale della prostata (TURP), la prostatectomia aperta e trattamenti minimamente invasivi come l'ablazione transuretrale con ago (TUNA). Nei trattamenti minimamente invasivi come l'ablazione a radiofrequenza, la terapia laser e gli impianti, vengono utilizzati dispositivi per l'iperplasia prostatica benigna. Pertanto, l'aumento della prevalenza dell'iperplasia prostatica benigna e l'aumento dei fattori di rischio stanno rafforzando la domanda di dispositivi per l'iperplasia prostatica benigna. AJMH), in 2019, globally, there were 11.26 million new cases and 1.86 million Years Lived with Disability (YLD) due to BPH in 2019. The incidence of BPH increased by 105.7%, and YLD increased by 110.6% worldwide during 1990–2019. The absolute incidence and YLD numbers increased considerably worldwide during this period, primarily due to population increase and aging. As per the estimates by UROLOGY FOUNDATION, in the UK, the prevalence of BPH rises from 50% among men aged 50–60 to 90% among men aged 80 and above. Some men develop sudden acute retention, i.e., the inability to pass urine. The treatment option for BPH includes surgeries such as transurethral resection of the prostate (TURP), open prostatectomy, and minimally invasive treatments such as transurethral needle ablation (TUNA). In minimally invasive treatments such as radiofrequency ablation, prostatic hyperplasic devices are used. Thus, the increase in the prevalence of benign prostatic hyperplasia and increasing risk factors are bolstering the demand for benign prostatic hyperplasic devices.

Approfondimenti sui prodotti

In base al prodotto, il mercato dei dispositivi iperplastici prostatici benigni è segmentato in resettoscopi, dispositivi di ablazione a radiofrequenza , laser urologici, stent prostatici e impianti. È probabile che il segmento dei resettoscopi deterrà la quota di mercato maggiore nel 2022. Tuttavia, si prevede che il segmento dei laser urologici registrerà il CAGR più elevato durante il periodo di previsione a causa dell'elevata domanda da parte dei medici e delle crescenti iniziative degli operatori di mercato nel lancio e nell'espansione del prodotto.prostatic hyperplasic devices market is segmented into resectoscopes, ablation devicesprostatic stents, and implants. The resectoscopes segment is likely to hold the largest market share in 2022. However, the urology lasers segment is anticipated to register the highest CAGR during the forecast period due to the high demand by physicians and the rising initiatives of market players in the launch and product expansion.

Informazioni sul tipo di procedura

In base al tipo di procedura, il mercato dei dispositivi iperplastici prostatici benigni è segmentato in terapia transuretrale a microonde, resezione transuretrale della prostata, ablazione transuretrale con ago della prostata, chirurgia laser, chirurgia urolift e altri. Nel 2022, è probabile che il segmento della resezione transuretrale della prostata deterrà la quota maggiore del mercato. Inoltre, si prevede che lo stesso segmento assisterà a una crescita della sua domanda al CAGR più rapido dal 2022 al 2028, grazie al suo accesso visivo e pratico alla prostata, alla capacità di rimozione immediata del tessuto in eccesso, alla capacità della resezione transuretrale della prostata (TURP) di combinarsi con altre procedure.

Informazioni per l'utente finale

In base all'utente finale, il mercato dei dispositivi per iperplasia prostatica benigna è segmentato in ospedali, cliniche, centri chirurgici ambulatoriali e altri. Nel 2022, è probabile che il segmento degli ospedali deterrà la quota maggiore del mercato. Inoltre, si prevede che il segmento delle cliniche assisterà a una crescita della sua domanda al CAGR più rapido dal 2022 al 2028, a causa di un aumento del numero di cliniche a un costo inferiore per il trattamento, facile accessibilità e flessibilità con tempi di attesa brevi.

Sviluppi organici come lanci di prodotti e approvazioni sono strategie ampiamente adottate dai player globali del mercato dei dispositivi per iperplasia prostatica benigna. Di seguito sono elencati alcuni dei recenti sviluppi chiave del mercato:

- Ad aprile 2022, Teleflex Incorporated ha lanciato in Giappone il sistema UroLift per il trattamento della BPH o prostata ingrossata. Il sistema è stato reso disponibile per l'acquisto subito dopo il lancio.

- Ad aprile 2020, Olympus ha annunciato l'approvazione di iTind, il suo dispositivo medico non chirurgico, per la chirurgia mininvasiva della BPH. Si tratta di un dispositivo di apertura temporanea dell'uretra che ha ricevuto una classificazione De Novo dalla FDA ed è un dispositivo medico di Classe II.

Mercato dei dispositivi per l'iperplasia prostatica benigna - Segmentazione

Il mercato globale dei dispositivi per iperplasia prostatica benigna è suddiviso in prodotto, tipo di procedura, utente finale e area geografica. In base al prodotto, il mercato è suddiviso in resettoscopi, dispositivi di ablazione a radiofrequenza, laser urologici , stent prostatici e impianti. In base al tipo di procedura, il mercato è suddiviso in terapia transuretrale a microonde, resezione transuretrale della prostata, ablazione transuretrale con ago della prostata, chirurgia laser, chirurgia urolift e altri. In base all'utente finale, il mercato è differenziato in ospedali, cliniche, centri chirurgici ambulatoriali e altri. In base all'area geografica, il mercato è suddiviso in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud e Centro America.

Ambito del rapporto di mercato sui dispositivi per l'iperplasia prostatica benigna

Approfondimenti regionali sul mercato dei dispositivi per l'iperplasia prostatica benigna

Le tendenze regionali e i fattori che influenzano il mercato dei dispositivi iperplastici prostatici benigni durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato dei dispositivi iperplastici prostatici benigni in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato dei dispositivi per l'iperplasia prostatica benigna

Ambito del rapporto di mercato sui dispositivi per l'iperplasia prostatica benigna

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2021 | 2,08 miliardi di dollari USA |

| Dimensioni del mercato entro il 2028 | 3,47 miliardi di dollari USA |

| CAGR globale (2021 - 2028) | 7,6% |

| Dati storici | 2019-2020 |

| Periodo di previsione | 2022-2028 |

| Segmenti coperti |

Per Prodotto

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato: comprendere il suo impatto sulle dinamiche aziendali

Il mercato dei dispositivi per iperplasia prostatica benigna sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato dei dispositivi per l'iperplasia prostatica benigna sono:

- KARL STORZ SE & Co. KG

- Richard Wolf GmbH

- Società Olimpo

- Studio dentistico Urologix, LLC.

- Società scientifica di Boston

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni la panoramica dei principali attori del mercato dei dispositivi per l'iperplasia prostatica benigna

Mercato dei dispositivi per l'iperplasia prostatica benigna - Profili aziendali

- KARL STORZ SE & Co. KG

- Richard Wolf GmbH

- Società Olimpo

- Studio dentistico Urologix, LLC.

- Società scientifica di Boston

- Farfalla

- TELEFLEX Incorporata

- Società quotata in borsa OmniGuide Holdings, Inc.

- Tecnologie laser convergenti

- ProArc

- Società Olimpo

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi storica (2 anni), anno base, previsione (7 anni) con CAGR

- Analisi PEST e SWOT

- Valore/volume delle dimensioni del mercato - Globale, Regionale, Nazionale

- Industria e panorama competitivo

- Set di dati Excel

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative

Ottieni un campione gratuito per - Mercato dei dispositivi per l'iperplasia prostatica benigna

Ottieni un campione gratuito per - Mercato dei dispositivi per l'iperplasia prostatica benigna