Strategie di mercato degli aghi cardiovascolari, principali attori, opportunità di crescita, analisi e previsioni entro il 2028

Previsioni del mercato degli aghi cardiovascolari fino al 2028 - Impatto del COVID-19 e analisi globale per tipo (aghi a corpo tondo e aghi da taglio), applicazione (chirurgia a cuore aperto e procedure sulle valvole cardiache), utilizzo (monouso e multiuso) e utente finale (ospedali e cliniche, centri chirurgici ambulatoriali e centri cardiovascolari) Geografia

- Stato : Edito

- Codice del report : TIPRE00004729

- Categoria : Scienze della vita

- Numero di pagine : 171

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 14, 2024

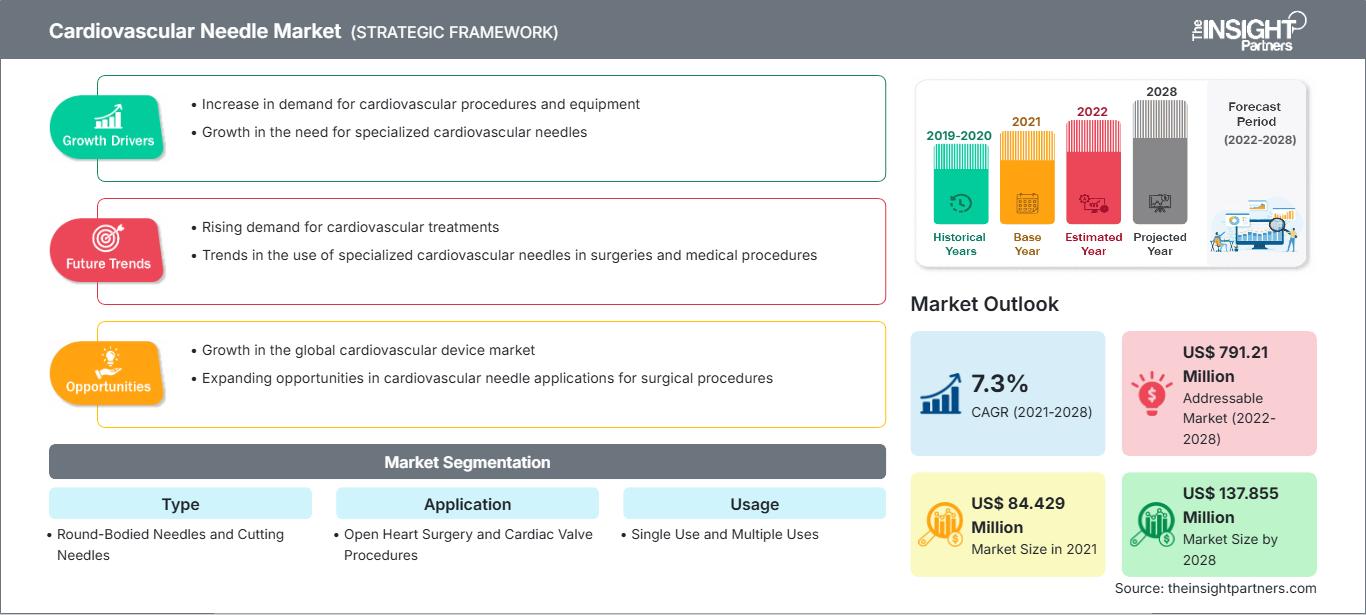

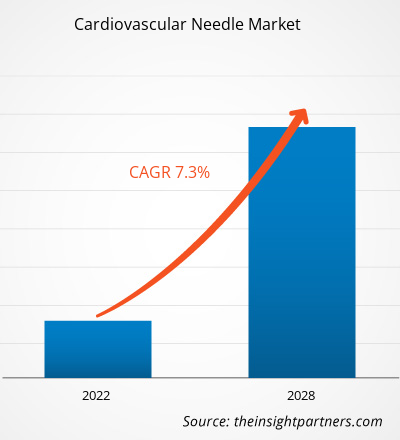

Il mercato degli aghi cardiovascolari è stato valutato a 84,429 milioni di dollari nel 2021 e si prevede che raggiungerà i 137,855 milioni di dollari entro il 2028; si prevede una crescita a un CAGR del 7,3% dal 2021 al 2028.

Gli aghi cardiovascolari vengono utilizzati durante interventi chirurgici a cuore aperto, interventi di sostituzione delle valvole cardiache, interventi di trapianto cardiaco, interventi di bypass aorto-coronarico e così via. Questi aghi sono di due tipi: aghi monouso o senza cruna e aghi multiuso o con cruna. Gli aghi cardiovascolari sono realizzati con nuove leghe di acciaio inossidabile che contengono alte concentrazioni di nichel, Surgalloy ed Ethalloy.

Il mercato degli aghi cardiovascolari è stato segmentato in base a tipologia, applicazione, utilizzo, utente finale e area geografica. Il mercato, per area geografica, è principalmente segmentato in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa e Sud e Africa. America Centrale. Il rapporto offre approfondimenti e analisi approfondite del mercato degli aghi cardiovascolari, ponendo l'accento su parametri quali tendenze di mercato, progressi tecnologici e dinamiche di mercato, oltre a un'analisi del panorama competitivo dei principali attori del mercato a livello mondiale.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato degli aghi cardiovascolari: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

Approfondimenti di mercato: la crescente prevalenza di malattie cardiovascolari stimola la crescita del mercato degli aghi cardiovascolari

Le malattie cardiovascolari (MCV) sono disturbi del cuore e dei vasi sanguigni e la categoria include malattie cerebrovascolari, coronaropatie, cardiopatie reumatiche e altre patologie. Il consumo di tabacco, una dieta non sana e l'inattività fisica, che aumentano il rischio di infarti e ictus, sono alcuni dei principali fattori legati allo stile di vita che portano alle MCV. Altri fattori di rischio che causano queste malattie includono ipertensione, diabete e livelli elevati di colesterolo. Le MCV sono tra le prime 10 cause di morte in tutto il mondo. Secondo l'Organizzazione Mondiale della Sanità (OMS), le malattie cardiovascolari sono la prima causa di morte in tutto il mondo. È probabile che le malattie cardiovascolari (MCV) rimangano la principale causa di morbilità e mortalità in tutto il mondo. Secondo i dati dell'OMS, circa 17,9 milioni di persone nel mondo sono morte per malattie cardiovascolari nel 2016, pari al 31,0% della mortalità totale registrata in quell'anno. Tra questi, circa l'85% dei decessi è stato dovuto ad infarto e ictus. I depositi di grasso attorno ai vasi sanguigni, che impediscono al sangue di fluire verso il cuore o il cervello, sono una delle principali cause di infarto e ictus. L'emorragia dei vasi o la formazione di coaguli di sangue nel cervello sono altre cause di ictus.

Secondo le statistiche europee sulle malattie cardiovascolari del 2017, le malattie cardiovascolari causano rispettivamente 3,9 milioni e oltre 1,8 milioni di decessi in Europa e nell'Unione Europea (UE) ogni anno. Pertanto, queste malattie rappresentano rispettivamente il 45,0% e il 37,0% della mortalità totale in Europa e nell'UE. Inoltre, secondo le statistiche dell'American Heart Association (AHA) del 2019, 121,5 milioni di adulti negli Stati Uniti, ovvero circa il 50% della popolazione adulta statunitense, soffre di malattie cardiovascolari ogni anno. Secondo il Journal of the American College of Cardiology, l'Asia presenta una prevalenza sempre più elevata di ipertensione, diabete e livelli elevati di colesterolo. Paesi come Giappone, Cina e India contribuiscono in modo significativo all'incidenza totale di malattie cardiovascolari nella regione. Pertanto, il significativo aumento dell'incidenza di malattie cardiovascolari in tutto il mondo sta contribuendo all'elevata domanda di dispositivi diagnostici e terapeutici per il trattamento delle malattie cardiovascolari, che sta trainando la crescita del mercato degli aghi cardiovascolari.

Approfondimenti basati sulla tipologia

In base alla tipologia, il mercato degli aghi cardiovascolari è segmentato in aghi a corpo tondo e aghi taglienti. Il segmento degli aghi a corpo tondo rappresenterà una quota di mercato maggiore nel 2021 e si prevede che il segmento degli aghi taglienti registrerà un CAGR più elevato nel mercato durante il periodo di previsione.

Approfondimenti basati sull'applicazione

In base all'applicazione, il mercato degli aghi cardiovascolari è segmentato in chirurgia a cuore aperto e procedure valvolari cardiache. Si prevede che il segmento della chirurgia a cuore aperto deterrà una quota di mercato maggiore nel 2021 e si stima che registrerà un CAGR più elevato nel periodo 2021-2028. La crescita del segmento della chirurgia a cuore aperto è attribuita all'aumento degli interventi chirurgici a cuore aperto in tutto il mondo.

Informazioni basate sull'utilizzo

In base all'utilizzo, il mercato degli aghi cardiovascolari è segmentato in monouso e multiuso. Si stima che il segmento monouso rappresenti una quota di mercato maggiore nel 2021. Si stima che il mercato per questo segmento crescerà a un CAGR più elevato dal 2021 al 2028.

Informazioni basate sull'utente finale

In base all'utente finale, il mercato degli aghi cardiovascolari è segmentato in ospedali e cliniche, centri chirurgici ambulatoriali e centri cardiovascolari. Il segmento ospedali e cliniche deterrà la quota di mercato maggiore nel 2021; Si stima inoltre che registrerà il CAGR più elevato del mercato durante il periodo di previsione.

La pandemia di COVID-19 è diventata la sfida più significativa a livello mondiale. Poiché questa pandemia ha messo a dura prova i sistemi sanitari di tutto il mondo, dare priorità alle risorse limitate è stato essenziale per ridurre al minimo i ricoveri ospedalieri. I pazienti cardiochirurgici non solo necessitano di risorse vitali in terapia intensiva, ma rientrano anche potenzialmente nella categoria a più alto rischio di complicanze da COVID-19. Pertanto, la maggior parte degli ospedali e dei reparti chirurgici ha preso in considerazione l'annullamento o il rinvio di interventi chirurgici elettivi, compresi quelli cardiovascolari. Pertanto, si prevede che l'impatto del COVID-19 sarà in qualche modo negativo sul mercato degli aghi cardiovascolari nel breve termine. Tuttavia, nel lungo termine, con l'affermarsi del calendario vaccinale e la diminuzione del tasso di trasmissione, i sistemi sanitari torneranno alla normalità e la domanda di aghi cardiovascolari aumenterà, il che sosterrà il mercato.

Acquisizioni, collaborazioni, partnership, lanci di prodotti ed espansioni sono strategie comunemente adottate dalle aziende per espandere la propria presenza a livello mondiale e soddisfare la crescente domanda. Gli operatori del mercato degli aghi cardiovascolari hanno adottato principalmente la strategia dell'innovazione di prodotto per soddisfare la mutevole domanda dei clienti in tutto il mondo, il che li aiuta anche a mantenere il loro marchio a livello globale.

Approfondimenti regionali sul mercato degli aghi cardiovascolari

Le tendenze regionali e i fattori che influenzano il mercato degli aghi cardiovascolari durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la geografia del mercato degli aghi cardiovascolari in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America meridionale e centrale.

Ambito del rapporto sul mercato degli aghi cardiovascolari

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2021 | US$ 84.429 Million |

| Dimensioni del mercato per 2028 | US$ 137.855 Million |

| CAGR globale (2021 - 2028) | 7.3% |

| Dati storici | 2019-2020 |

| Periodo di previsione | 2022-2028 |

| Segmenti coperti |

By Tipo

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato degli aghi cardiovascolari: comprendere il suo impatto sulle dinamiche aziendali

Il mercato degli aghi cardiovascolari è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Mercato degli aghi cardiovascolari Panoramica dei principali attori chiave

- Ethicon (Johnson & Johnson Services, Inc.)

- Mani, Inc

- Barber of Sheffield

- FSSB aghi chirurgici GmbH

- Medtronic

- Aurolab

- Teleflex Incorporated

- Meril Life Sciences Pvt. Ltd.

- CP Medical

- SMB Corporation of India

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative