Dimensioni, crescita e domanda del mercato della cura delle ferite entro il 2034

Dimensioni e previsioni del mercato della cura delle ferite (2021-2034), quota di mercato globale e regionale, trend e analisi delle opportunità di crescita. Copertura del rapporto: per prodotto (medicazioni avanzate per ferite, cura chirurgica delle ferite, cura tradizionale delle ferite e dispositivi per la terapia delle ferite), tipo di ferita (ferite croniche e ferite acute) e utente finale (ospedali, cliniche specializzate, assistenza domiciliare e altri).

- Stato : Dati rilasciati

- Codice del report : TIPRE00029834

- Categoria : Scienze della vita

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : March 19, 2026

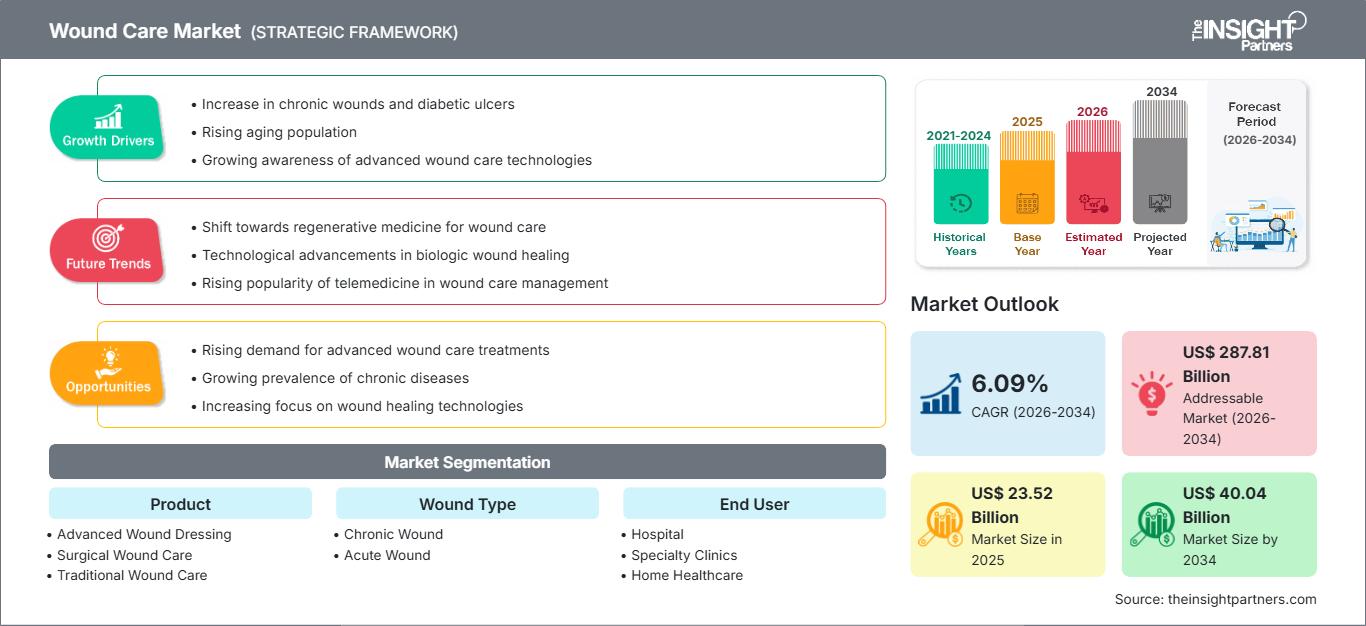

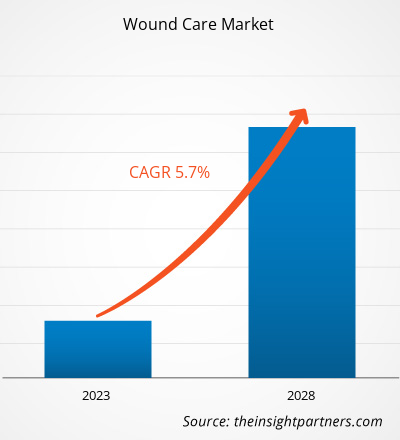

Si prevede che il mercato globale della cura delle ferite raggiungerà un valore di 40,04 miliardi di dollari entro il 2034, rispetto ai 23,52 miliardi di dollari del 2025. Si prevede inoltre che il mercato registrerà un tasso di crescita annuo composto (CAGR) del 6,09% nel periodo di previsione 2026-2034.

Tra le principali dinamiche di mercato si annoverano la crescente prevalenza globale di patologie croniche come diabete e obesità, il rapido invecchiamento della popolazione e la conseguente predisposizione alle ulcere da pressione, nonché un significativo cambiamento tecnologico verso medicazioni bioattive e intelligenti. Inoltre, si prevede che il mercato trarrà vantaggio dall'aumento del volume degli interventi chirurgici a livello mondiale, dall'espansione dei centri specializzati nella cura delle ferite e dalla crescente integrazione di strumenti digitali per il monitoraggio e la valutazione a distanza delle lesioni.

Analisi di mercato sulla cura delle ferite

L'analisi del mercato della cura delle ferite indica una transizione strategica verso protocolli di guarigione personalizzati e proattivi. Le tendenze di approvvigionamento suggeriscono una crescente preferenza per la gestione avanzata delle ferite rispetto alle medicazioni tradizionali, poiché i sistemi sanitari danno priorità alla riduzione dei ricoveri ospedalieri e alla diminuzione dei costi complessivi del trattamento. Si stanno aprendo opportunità strategiche nello sviluppo della medicina rigenerativa e dei sostituti cutanei bioingegnerizzati, che offrono risultati clinici superiori per le ferite croniche difficili da guarire rispetto alle terapie convenzionali. L'analisi evidenzia inoltre che il successo sul mercato dipende sempre più dalla capacità di orientarsi in complessi sistemi di rimborso e di dimostrare un chiaro valore farmacoeconomico. La differenziazione competitiva si concentra ora su soluzioni di cura integrate che combinano prodotti fisici con software di tracciamento digitale, consentendo ai medici di monitorare i processi di guarigione in tempo reale e di intervenire precocemente per prevenire le infezioni.

Panoramica del mercato della cura delle ferite

La cura delle ferite si sta evolvendo dalla semplice gestione degli infortuni a un campo altamente specializzato di terapia rigenerativa. Sebbene storicamente dominato da semplici garze e bende, il settore si è espanso in segmenti ad alto valore aggiunto come la terapia a pressione negativa per le ferite (NPWT), le medicazioni antimicrobiche e i farmaci biologici a base cellulare. Gli operatori di mercato spaziano da conglomerati multinazionali diversificati a società biotecnologiche di nicchia focalizzate sull'ingegneria tissutale. Il crescente peso delle ulcere del piede diabetico e delle ulcere venose degli arti inferiori, sia nelle economie sviluppate che in quelle emergenti, ha spostato l'attenzione verso ambienti umidi per la guarigione delle ferite e il controllo delle infezioni. Con il passaggio dell'assistenza sanitaria verso contesti ambulatoriali e domiciliari, i produttori stanno innovando con dispositivi portatili e di facile utilizzo e piattaforme di telemedicina per la cura delle ferite, al fine di garantire la continuità delle cure. Ad esempio, il mercato statunitense rappresenta un panorama maturo ma dinamico, caratterizzato da un'elevata spesa sanitaria e da una forte enfasi su risultati clinici avanzati. Il mercato è trainato da una solida infrastruttura di cliniche specializzate nella cura delle ferite e da un numero significativo di pazienti che necessitano di cure complesse per infezioni del sito chirurgico e ulcere croniche.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato della cura delle ferite: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo report.Questo campione GRATUITO includerà un'analisi dei dati, che spazierà dalle tendenze di mercato alle stime e alle previsioni.

Fattori trainanti e opportunità del mercato della cura delle ferite

Fattori trainanti del mercato:

- Aumento della prevalenza delle malattie croniche: l'impennata globale del diabete e delle malattie cardiovascolari è una delle cause principali, poiché queste patologie compromettono significativamente il naturale processo di guarigione, portando a una maggiore incidenza di ferite croniche complesse e non cicatrizzanti.

- Progressi tecnologici nelle medicazioni avanzate: le innovazioni nella scienza dei materiali, come gli idrocolloidi, gli alginati e gli antimicrobici a base di argento, stanno trainando la crescita del mercato offrendo una gestione dell'umidità e una protezione dalle infezioni superiori rispetto ai prodotti tradizionali.

- Aumento della popolazione geriatrica: con l'invecchiamento della popolazione mondiale, aumenta la predisposizione a fragilità cutanee e problemi di mobilità legati all'età, con conseguente incremento dei casi di ulcere da pressione e insufficienza venosa che richiedono cure a lungo termine.

Opportunità di mercato:

- Espansione delle soluzioni per l'assistenza sanitaria domiciliare: esiste un'importante opportunità per lo sviluppo di dispositivi portatili per la terapia a pressione negativa (NPWT) e di medicazioni avanzate di facile applicazione, progettate per l'uso a domicilio, in risposta alla crescente preferenza per l'assistenza decentrata.

- Integrazione di intelligenza artificiale e monitoraggio digitale: le mosse strategiche verso strumenti di valutazione delle ferite basati sull'IA e medicazioni intelligenti con sensori integrati offrono un percorso verso una crescita ad alto margine, migliorando l'accuratezza diagnostica e l'aderenza del paziente alla terapia.

- Mercati emergenti in Asia-Pacifico e America Latina: il rapido miglioramento delle infrastrutture sanitarie e la crescente diffusione del turismo medico in queste regioni offrono un potenziale inesplorato per i marchi di alta gamma nel settore della cura delle ferite, consentendo loro di affermarsi e ampliare le proprie reti di distribuzione.

Analisi di segmentazione del mercato della cura delle ferite

La quota di mercato della cura delle ferite viene analizzata in diversi segmenti per fornire una comprensione più chiara della sua struttura, del potenziale di crescita e delle tendenze emergenti. Di seguito è riportato l'approccio di segmentazione standard utilizzato nella maggior parte dei report di settore:

Per prodotto:

- Medicazioni avanzate per ferite: un segmento in forte crescita che comprende medicazioni in schiuma, idrocolloidali e in pellicola, progettate per mantenere un ambiente ottimale per la guarigione.

- Cura delle ferite chirurgiche: si concentra su suture, punti metallici e adesivi tissutali utilizzati principalmente in sala operatoria per garantire una chiusura sicura delle ferite.

- Cura tradizionale delle ferite: il segmento fondamentale che comprende bende, cerotti medicali e garze, utilizzati principalmente per lesioni minori.

- Dispositivi per la terapia delle ferite: includono tecnologie avanzate come la terapia a pressione negativa (NPWT) e le apparecchiature per l'ossigenoterapia iperbarica.

In base al tipo di ferita:

- Ferite croniche: includono ulcere del piede diabetico, ulcere da pressione e ulcere venose degli arti inferiori, che richiedono protocolli di trattamento specializzati e a lungo termine.

- Ferita acuta: comprende incisioni chirurgiche e lesioni traumatiche come ustioni e lacerazioni che in genere seguono un normale processo di guarigione.

Da parte dell'utente finale:

- Ospedale: il principale canale per la cura delle patologie acute e la gestione di ferite chirurgiche complesse, grazie a strutture di degenza all'avanguardia.

- Cliniche specializzate: Centri in espansione dedicati alla cura ambulatoriale delle ferite, che offrono competenze specialistiche e modalità terapeutiche avanzate.

- Assistenza sanitaria domiciliare: un segmento emergente trainato dal passaggio al monitoraggio remoto e dall'utilizzo di dispositivi portatili per la cura delle ferite.

- Altri: include strutture di assistenza a lungo termine e centri di chirurgia ambulatoriale focalizzati sul recupero post-operatorio.

Per area geografica:

- America del Nord

- Europa

- Asia Pacifico

- Sud e Centro America

- Medio Oriente e Africa

Ambito del rapporto sul mercato della cura delle ferite

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 23,52 miliardi di dollari |

| Dimensioni del mercato entro il 2034 | 40,04 miliardi di dollari USA |

| Tasso di crescita annuo composto (CAGR) globale (2026-2034) | 6,09% |

| Dati storici | 2021-2024 |

| periodo di previsione | 2026-2034 |

| Segmenti trattati |

Per prodotto

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori nel mercato della cura delle ferite: comprenderne l'impatto sulle dinamiche di business

Il mercato della cura delle ferite è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

Analisi della quota di mercato della cura delle ferite per area geografica

Attualmente il Nord America detiene la quota maggiore del mercato globale, grazie a infrastrutture mediche all'avanguardia e all'elevata adozione di terapie innovative. Tuttavia, si prevede che la regione Asia-Pacifico registrerà la crescita più rapida nei prossimi anni, grazie ai crescenti investimenti nel settore sanitario e all'ampia base di pazienti diabetici. Anche i mercati emergenti in Sud e Centro America, Medio Oriente e Africa offrono numerose opportunità inesplorate per le aziende consolidate che desiderano introdurre soluzioni avanzate ed economicamente vantaggiose per la cura delle ferite.

Il mercato della cura delle ferite sta attraversando una profonda trasformazione, passando da applicazioni passive di medicazione a interventi biologici attivi. La crescita è trainata dalla crescente necessità di prevenzione delle infezioni, dall'aumento delle procedure chirurgiche ambulatoriali e dall'espansione dei modelli di assistenza sanitaria basati sul valore. Di seguito è riportato un riepilogo delle quote di mercato e delle tendenze per regione:

America del Nord

- Quota di mercato: domina il panorama globale grazie a sistemi di rimborso consolidati e alla presenza di importanti leader del settore.

-

Fattori chiave:

- Elevata incidenza di ulcere croniche correlate all'obesità e di complicanze diabetiche.

- Solide attività di ricerca e sviluppo nel campo della medicina rigenerativa e dei sostituti cutanei.

- Ampia disponibilità di centri specializzati per la cura delle ferite e di strutture di assistenza infermieristica qualificata.

- Tendenze: crescente adozione di sistemi intelligenti per il monitoraggio delle ferite e spostamento strategico verso dispositivi monouso per la terapia a pressione negativa.

Europa

- Quota di mercato: Detiene una quota significativa, grazie a sistemi sanitari altamente sviluppati e a rigorosi standard normativi per i dispositivi medici.

-

Fattori chiave:

- Un invecchiamento demografico rapido che richiede una gestione intensiva delle lesioni da pressione.

- Un governo forte si concentra sulla riduzione delle infezioni nosocomiali (HAI).

- Percorsi clinici ben definiti per l'utilizzo di terapie bioattive e antimicrobiche.

- Tendenze: crescente attenzione alla sostenibilità e ai materiali ecocompatibili per la cura delle ferite, unitamente all'espansione dei servizi infermieristici territoriali per la gestione delle ferite.

Asia-Pacifico

- Quota di mercato: la regione in più rapida crescita, trainata dalle enormi popolazioni di Cina e India e dal miglioramento dell'accesso alle moderne cure mediche.

-

Fattori chiave:

- L'aumento esponenziale della prevalenza del diabete sta portando a un'impennata delle ulcere del piede diabetico.

- Iniziative governative volte a modernizzare le infrastrutture sanitarie e le cliniche mediche rurali.

- Aumento del reddito disponibile e maggiore consapevolezza riguardo ai prodotti avanzati per la guarigione delle ferite.

- Tendenze: Forte crescita nella produzione di materiali per la cura delle ferite a basso costo e rapida transizione dalle tradizionali garze alle medicazioni avanzate in schiuma e pellicola.

America meridionale e centrale

- Quota di mercato: un mercato emergente con un settore sanitario privato in crescita in paesi come Brasile e Argentina.

-

Fattori chiave:

- Il crescente numero di traumi e incidenti stradali richiede un'assistenza medica d'urgenza per le ferite.

- Ammodernamento delle strutture chirurgiche e maggiore attenzione alla cura post-operatoria.

- Una popolazione di classe media in crescita alla ricerca di servizi medici di alta qualità.

- Tendenze: espansione delle reti di distribuzione multinazionali e crescente domanda di prodotti specializzati per la cura delle ustioni e di adesivi tissutali.

Medio Oriente e Africa

- Quota di mercato: Mercato in via di sviluppo, focalizzato sulla formalizzazione dei protocolli di cura delle ferite e sulla riduzione della dipendenza da forniture mediche importate.

-

Fattori chiave:

- Elevata prevalenza di malattie legate allo stile di vita nella regione del Consiglio di Cooperazione del Golfo (CCG).

- Investimenti strategici in città mediche e ospedali specializzati all'avanguardia.

- Crescente attenzione alla gestione delle catastrofi e alla cura dei traumi nelle regioni colpite da conflitti.

- Tendenze: Implementazione delle linee guida nazionali per la gestione delle ferite e attenzione alle medicazioni ad alta assorbenza adatte ai climi aridi.

Elevata densità di mercato e concorrenza

La concorrenza si sta intensificando a causa della presenza di leader affermati come 3M (Solventum) e Smith & Nephew. Colossi globali come Convatec Group PLC, insieme a innovatori specializzati come Integra LifeSciences e MIMEDX Group, contribuiscono a un panorama altamente competitivo incentrato sull'efficacia clinica e sul rapporto costi-efficacia.

Questo contesto competitivo spinge i fornitori a differenziarsi attraverso:

- Risultati clinici basati sull'evidenza: enfasi sulla più rapida guarigione delle ferite e sulla riduzione del rischio di infezioni attraverso rigorosi studi clinici per garantire l'inclusione nei prontuari ospedalieri.

- Integrazione dell'ecosistema digitale: sviluppo di app e piattaforme proprietarie che collegano i prodotti per la cura delle ferite con le cartelle cliniche elettroniche (EHR) per un monitoraggio continuo del paziente.

- Catene di approvvigionamento integrate verticalmente: Gestire la produzione di materie prime, come polimeri specializzati e tessuti biologici, per garantire il controllo della qualità e un approvvigionamento etico.

- Diversificazione del portafoglio: andare oltre le medicazioni ed esplorare settori affini come la terapia compressiva, la nutrizione per la guarigione delle ferite e gli strumenti avanzati per il debridement.

Opportunità e mosse strategiche

- Partnership strategiche per la salute digitale: collaborare con aziende tecnologiche per integrare l'imaging delle ferite basato sull'intelligenza artificiale e l'analisi predittiva nei flussi di lavoro clinici standard.

- Concentrarsi sul rimborso basato sul valore: sviluppare modelli di condivisione del rischio con le compagnie assicurative in cui il pagamento sia legato al raggiungimento di traguardi importanti nella guarigione delle ferite, piuttosto che al volume del prodotto.

- Espansione nel settore dei farmaci biologici e bioattivi: investire nell'acquisizione di startup specializzate in terapie a base di cellule staminali e innesti di pelle di pesce per conquistare il segmento ad alto margine delle ferite croniche.

Le principali aziende operanti nel mercato della cura delle ferite sono:

- Smith e nipote

- Ethicon USA LLC

- Convatec Group Plc

- BAXTER International Inc.

- COLOPLASTO COME

- Paul HARTMANN AG

- MEDTRONIC PLC

- 3M COMPANY

- MIMEDX

- Integra LifeSciences Holdings Corporation

Nota: le aziende elencate sopra non sono classificate in un ordine particolare.

Notizie e recenti sviluppi del mercato della cura delle ferite

- Nel dicembre 2025, Solventum ha annunciato di aver completato l'acquisizione di Acera Surgical (Acera). Questa società privata di bioscienze si concentra sullo sviluppo e la commercializzazione di materiali completamente ingegnerizzati per la cura rigenerativa delle ferite.

- Nell'aprile 2025, Convatec, azienda leader nel settore dei prodotti e delle tecnologie medicali, ha confermato i piani per il lancio iniziale sul mercato di ConvaNiox™ alla fine del 2025, prima del suo rilascio commerciale completo nel 2026. Questa innovativa tecnologia per la cura delle ferite si basava sull'ossido nitrico, un potente agente antimicrobico e antibiofilm, ed era supportata da solide evidenze cliniche. Con l'ampliamento della produzione, il prodotto è stato inizialmente reso disponibile per il trattamento delle ulcere del piede diabetico (DFU), dove ha dimostrato risultati clinici eccezionali, riducendo l'area della ferita tre volte più velocemente e aumentando la guarigione delle DFU del 60% rispetto al trattamento standard in uno studio clinico randomizzato e controllato.

Copertura e risultati del rapporto sul mercato della cura delle ferite.

Il rapporto "Dimensioni e previsioni del mercato della cura delle ferite (2021-2034)" fornisce un'analisi dettagliata del mercato, coprendo le seguenti aree:

- Dimensioni e previsioni del mercato della cura delle ferite a livello globale, regionale e nazionale per tutti i principali segmenti di mercato coperti dall'ambito

- Tendenze del mercato della cura delle ferite, nonché dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave.

- Analisi PEST e SWOT dettagliata

- Analisi del mercato della cura delle ferite, con particolare attenzione alle principali tendenze di mercato, al quadro globale e regionale, ai principali operatori, alle normative e ai recenti sviluppi del mercato.

- Analisi del panorama industriale e della concorrenza, con particolare attenzione alla concentrazione del mercato, all'analisi tramite mappa termica, ai principali operatori e ai recenti sviluppi nel mercato della cura delle ferite.

- Profili aziendali dettagliati

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative