自動車用ファブリック市場の分析と予測 - 規模、シェア、成長、トレンド 2030 年

自動車用ファブリック市場の規模と予測(2020年 - 2030年)、世界および地域別シェア、トレンド、成長機会分析レポートの対象範囲:コンポーネント別(カーペット、ヘッドライナー、フードライナー、断熱材、シート表皮材など)および素材別(繊維、人工皮革、本革、人工スエード)

- ステータス : 出版

- レポートコード : TIPRE00006211

- カテゴリー : 化学薬品および材料

- ページ数 : 143

- 利用可能なレポート形式 :

- 最終更新日 : June 17, 2024

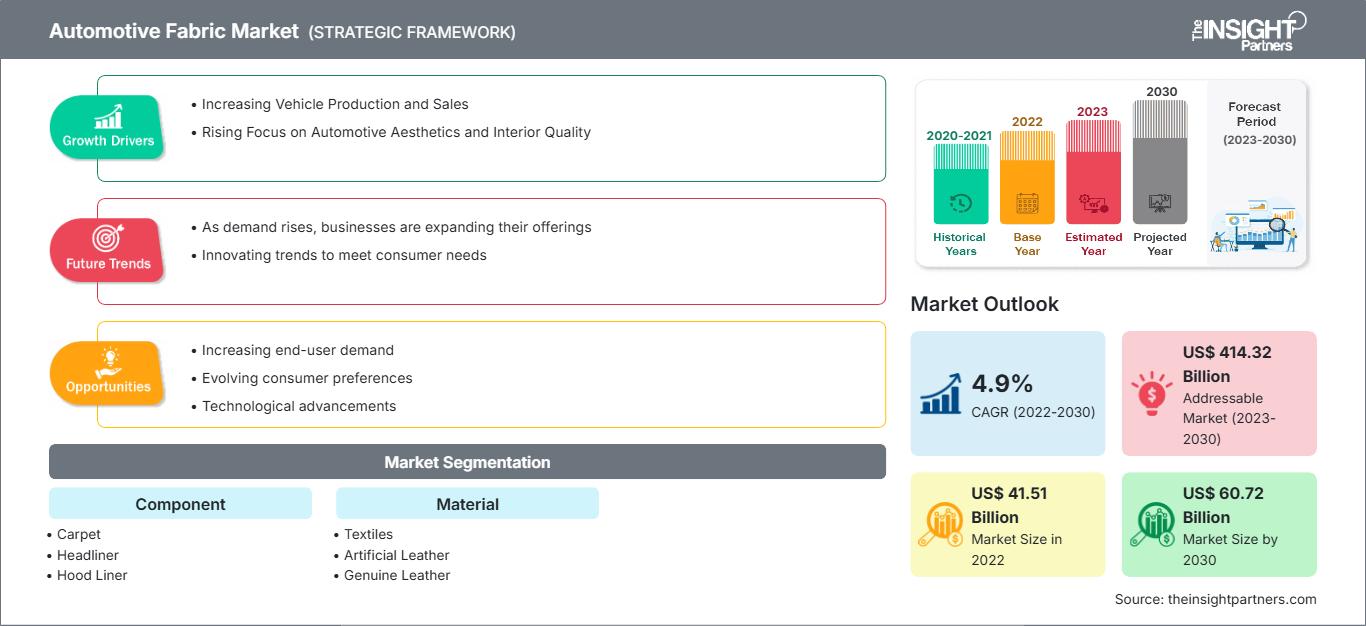

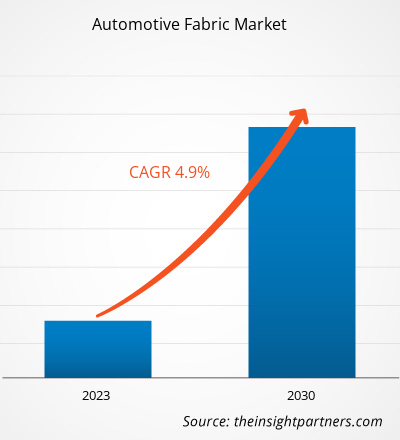

[調査レポート] 自動車用ファブリックの市場規模は2022年に415億1,383万米ドルと評価され、2030年までに607億2,234万米ドルに達すると予測されています。また、2022年から2030年にかけて4.9%のCAGRを記録することが見込まれています。

市場分析

自動車用ファブリックは、織物、不織布、コーティングされた形で利用できるファブリックの種類です。これらのタイプのファブリック材料は非常に柔軟で、紫外線や低温亀裂に対する耐性、耐久性、軽量設計などの機能を備えています。自動車用ファブリックは、座席の快適さを提供するだけでなく、全体的な美的体験を促進します。市場の成長は、優れた快適さと高品質の素材への好みとともに、技術の進歩によって強く推進されています。自動車の生産が増加するにつれて、自動車アクセサリーの需要も増加しており、今後数年間で自動車用ファブリック市場の成長に貢献すると予想されています。

成長の原動力と課題

自動車製造能力の向上と電気自動車の需要の高まりは、世界の自動車産業の成長を後押しするいくつかの要因です。自動車は、ドイツ、イタリア、英国などを含むヨーロッパ諸国のGDPに大きく貢献しているため、ヨーロッパの主要産業の1つです。消費者が品質と美観を重視するため、自動車の内外装の美観と特性の開発への重点が高まり、自動車用ファブリックの需要を促進しています。さまざまな国の政府は、車内の安全性を促進するために、シートベルト、エアバッグ、アンチロックブレーキシステムの義務的な取り付けと使用を含む厳格な安全規制を課しており、高性能で安全な自動車用ファブリック材料の需要を押し上げています。このように、自動車生産台数の増加と自動車の美観への関心の高まりが、自動車用ファブリック市場の成長を牽引しています。

ポリ塩化ビニル(PVC)とポリウレタン(PU)は、合成皮革の製造に最も多く使用されている合成プラスチックポリマーです。プラスチックを用いた合成皮革の製造プロセスは、環境に優しい方法とは言えません。ほとんどの合成皮革に使用されているプラスチックの製造プロセスは、比較的エネルギーを大量に消費し、化学物質を大量に使用するプロセスであり、大量の廃棄物も発生します。そのため、PVCとPUの有害な影響に加え、合成皮革は皮革に比べて耐久性が低いため、自動車用ファブリック市場の成長は抑制されています。

要件に合わせてレポートをカスタマイズ

レポートの一部、国レベルの分析、Excelデータパックなどを含め、スタートアップ&大学向けに特別オファーや割引もご利用いただけます(無償)

自動車用ファブリック市場: 戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

レポートのセグメンテーションと範囲

「世界の自動車用ファブリック市場の分析と2030年までの予測」は、世界の市場動向と成長機会に重点を置いた専門的かつ詳細な調査です。このレポートは、部品、材質、地域に基づいて詳細な市場セグメンテーションを行い、世界市場の概要を提供することを目的としています。レポートでは、世界中の自動車用ファブリックの消費量に関する主要な統計と、主要地域および国における需要を提供しています。さらに、レポートでは、主要地域および国における自動車用ファブリック市場の業績に影響を与えるさまざまな要因の定性的な評価も提供しています。また、自動車用ファブリック市場の主要プレーヤーとその主要な戦略的展開に関する包括的な分析も含まれています。市場ダイナミクスの分析も含まれており、主要な推進要因、市場動向、有利な機会を特定するのに役立ちます。これにより、主要な収益ポケットを特定するのに役立ちます。

エコシステム分析とポーターの5つの力の分析は、世界の自動車用ファブリック市場の360度のビューを提供し、サプライチェーン全体と市場の成長に影響を与えるさまざまな要因を理解するのに役立ちます。

セグメント分析

世界の自動車用ファブリック市場は、コンポーネントと材料に基づいて分割されています。コンポーネントに基づいて、自動車用ファブリック市場は、カーペット、ヘッドライナー、フードライナー、断熱材、シートカバー材料、およびその他に分類されます。材料に基づいて、市場は繊維、人工皮革、本革、人工スエードに分類されます。さらに、カーペットセグメントは2022年に自動車用ファブリック市場の大きなシェアを占めました。ポリエステル、ポリアミド、ポリプロピレン、アラミドは、自動車の内装を美しくするカーペットのデザインにおいて、繊維素材として好んで使用されています。ヘッドライナーは、柔らかな手触りと均一な魅力を提供し、内装全体のスタイリングを引き立てるトリコットニット生地で構成されています。ボンネットライナーは、適切な遮音要素を備えた薄い断熱材層で構成されており、ボンネットの断熱不良によるエンジンからの騒音を防ぎます。防音・断熱は、エンジンカバー、アンダートレイ、ボンネットなど、様々な自動車部品に搭載されている重要な機能の一つです。三層ラミネートポリエステルは、多くの種類のカーシートのシート生地として使用されています。

素材別では、2022年にはテキスタイルセグメントが大きなシェアを占めました。自動車用テキスタイルは、自動車、電車、バス、その他の車両に様々な用途があります。自動車用テキスタイルは、糸繊維、フィラメント、その他の生地など、様々なタイプのテキスタイルコンポーネントで構成されています。人工皮革は、フェイクレザーや合成皮革とも呼ばれ、ポリ塩化ビニル(PVC)またはポリウレタン(PU)を使用してデザインされています。本革は、自動車業界では内装部品に使用される高価な布地素材と認識されています。合成スエードの需要は伸び続けており、高級自動車部品のデザインによく使用されています。消費者のライフスタイルの変化、高級ドライブやカーシェアリングサービスへの嗜好の高まりにより、人工スエード市場は世界的に活況を呈しています。

地域分析

このレポートでは、北米、ヨーロッパ、アジア太平洋(APAC)、中東およびアフリカ(MEA)、南米および中米の5つの主要地域に関して、世界の自動車用ファブリック市場の詳細な概要を提供しています。アジア太平洋地域は自動車用ファブリック市場で大きなシェアを占め、2022年には200億米ドル以上の価値が見込まれています。アジア太平洋地域は自動車製造の中心地であり、多くの国際的および国内企業がこの地域で事業を展開しています。国際自動車工業会(IOM)の報告書によると、アジア太平洋地域のさまざまな国では、2021年に約4,673万台の自動車が生産されました。ヨーロッパ市場は2030年までに100億米ドルを超えると予想されています。自動車産業は、ドイツ、イギリス、イタリアを含む多くのヨーロッパ諸国のGDPに大きく貢献しているため、ヨーロッパの主要産業です。自動車用ファブリックは、自動車のカーペット、トランクエリア、内装トリム、防音、断熱材などに広く使用されています。北米の自動車用ファブリック市場は、2022年から2030年にかけて約4%のCAGRを記録すると予想されています。北米には、アウディAG、バイエリッシェ・モトーレン・ヴェルケAG、ステランティスNV、フォード・モーター・カンパニー、本田技研工業株式会社、ヒュンダイ・モーター・カンパニー、メルセデス・ベンツ、フォルクスワーゲン・グループなど、定評のある自動車メーカーが存在します。そのため、自動車産業の拡大により、今後数年間、北米における自動車用ファブリックの需要が拡大すると予測されています。

業界の発展と将来の機会

自動車用ファブリック市場で活動する主要企業が行っているさまざまな取り組みは以下の通りです。

- 2023年9月、Apex Millsは米国スチュアートにあるHanesBrands Inc.の施設を買収しました。この買収は、エラストマーの編み物、染色、仕上げ能力の拡大に貢献しました。

- 2022年3月、Lear Corpはローマ企業であるThagora Technology SRLの買収を完了しました。この買収により、Lear Corpは拡張可能なスマート製造技術を自社のコンピテンシーに加えることができました。

- 2022年2月、Lear CorpはKongsberg Automotiveのインテリアコンフォートシステム事業部門の完全買収を発表しました。この買収により、Learのシート部品の能力が強化され、製品ラインナップが拡大しました。

自動車用ファブリック市場の地域別分析

予測期間全体を通して自動車用ファブリック市場に影響を与える地域的な傾向と要因は、The Insight Partnersのアナリストによって徹底的に説明されています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東・アフリカ、中南米における自動車用ファブリック市場のセグメントと地域についても説明します。

自動車用ファブリック市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| の市場規模 2022 | US$ 41.51 Billion |

| 市場規模別 2030 | US$ 60.72 Billion |

| 世界的なCAGR (2022 - 2030) | 4.9% |

| 過去データ | 2020-2021 |

| 予測期間 | 2023-2030 |

| 対象セグメント |

By コンポーネント

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

自動車用ファブリック市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

自動車用ファブリック市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認知度の高まりといった要因により、エンドユーザーの需要が高まり、急速に成長しています。需要の増加に伴い、企業は製品ラインナップの拡充、消費者ニーズへの対応、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

- 入手 自動車用ファブリック市場 主要プレーヤーの概要

COVID-19パンデミックの影響/地政学的シナリオの影響/景気後退の影響

COVID-19パンデミック以前、世界中の多くの国が経済成長を報告していました。主要メーカーは自動車用ファブリックの研究開発に投資し、幅広い顧客基盤に対応するために、合併・買収戦略を通じて地理的範囲の拡大にも注力していました。COVID-19パンデミック以前は、自動車業界からの需要増加により、自動車用ファブリックメーカーは製造において着実な成長を報告していました。自動車用ファブリックメーカーは、環境に優しく、耐久性があり、お手入れが簡単なファブリックの開発に重点を置いていました。米国国際貿易委員会(USITC)によると、自動車産業の脆弱性の高さにより、米国の自動車販売台数は2019年と比較して2020年に15%減少しました。パンデミックの間、サプライチェーンの混乱、原材料と労働力の不足、運用上の困難により需要と供給のギャップが生じ、自動車用ファブリック市場の成長に悪影響を及ぼしました。メーカーは、サプライヤーから原材料や材料を調達する際に課題があると報告し、それによって自動車用ファブリックの生産率に影響を与えました。

さらに、サプライチェーンの深刻な混乱と熟練労働者の不足によって引き起こされた生産不足は、多くの地域、特にアジア太平洋、ヨーロッパ、北米で需要と供給のギャップを生み出しました。自動車産業からの需要の変動により、前述の地域で需要と供給のギャップも記録されました。2021年には、ワクチン接種率の上昇がさまざまな国の全体的な状況の改善に貢献し、化学および材料業界にとって好ましい環境につながりました。自動車業界で事業を展開する企業の販売業務。

競合状況と主要企業

自動車用ファブリック市場で事業を展開する主要企業としては、Lear Corp、Bader GmbH & Co KG、BOXMARK Leather GmbH & Co KG、AUNDE Group SE、Grupo Empresarial Copo SA、Classic Soft Trim Inc、Dual Borgstena Textile Portugal Unipessoal Lda、Shawmut Corp、Apex Mills Corp、Seiren Co Ltd などがあります。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応