Rising Number of Orders and Production of Narrow Body Aircraft to Fuel C-Parts Market Growth During Forecast Period

According to our latest study, "C-Parts Market Size and Forecast (2021–2031), Global and Regional Share, Trend, and Growth Opportunity Analysis – by Material Type, End-Use Industry, Product Type, Fastener Type, and Geography," the market was valued at US$ 158.46 billion in 2024 and is expected to reach US$ 212.80 billion by 2031; it is estimated to record a CAGR of 4.4% from 2025 to 2031. The report includes growth prospects owing to the current C-parts market trends and their foreseeable impact during the forecast period.

Raw materials used in the manufacturing of C-parts include steel, bronze, copper, polymers, plastics, composites, etc. These materials are used in the manufacturing of C-parts owing to their load-bearing capacity, strength, and thermal conductivity. The key raw material suppliers in the Asia Pacific C-parts market ecosystem include Remington Industries; Tata Steel; China Baowu Group; Nippon Steel; ArcelorMittal; Ansteel Group; HBIS Group; Shagang Group; POSCO Holdings; Shougang Group; BASF; The Dow Chemical Company; First Quantum Minerals; JSW Steel; Jindal Steel; Grainger Industrial Supply; Hubbard Supply Co.; Industrial Metal Supply Co.; Murphy and Nolan, Inc.; Metric Metal; American Metals Inc.; Norfolk Iron & Metal; Mill Steel Company; Southern Copper & Supply; Farmers Copper; Versa-Bar; and Aviva Metals.

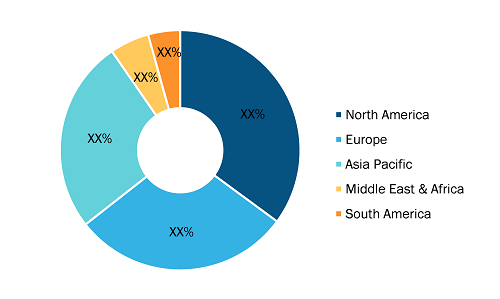

C-Parts Market Analysis — by Region (%, 2024)

C-Parts Market Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: ByMaterial Type (Steel or Stainless Steel, Plastic or Composites, Cast Iron, Steel Alloys, and Others), End-Use Industry (Automotive, Aerospace & Defense, Energy & Power, Semiconductors, and Others), Product Type (Fasteners, Bearings, and Others), Fastener Type (Nuts, Bolts, Screws, Washers, and Others), and Geography

C-Parts Market Growth & Scope Report | Size & Forecast 2031

Download Free Sample

Source: The Insight Partners Analysis

The manufacturers procure raw materials from the preferred suppliers through direct or indirect sales channels to manufacture different types of fasteners, bearings, including nuts & bolts, screws, washers, spherical bearings, and others. Manufacturers also comply with the C-parts products with domestic and international regulatory standards through several certifying bodies such as ATEX, NEC, IECEx, CEC, etc, which specify their requirements at each stage of the value chain.

The end users of C-parts include industrial vehicles, wind energy, forklifts, material handling, agriculture, railways, automotive, aerospace & defense, construction machinery, power generation, oil & gas exploration, and gear drives. Aftermarket services play a vital role in the value chain. These services involve the use of C-parts to ensure the longevity of the end users mentioned above. C-parts are routinely replaced during routine maintenance, repairs, and customization, making their availability and quality paramount in aftermarket operations. Aftermarket is gaining traction in a variety of industries, including aerospace, healthcare, and manufacturing, where there is a high risk of failure or declining operational efficiencies due to constant heavy loads. Various associations involved with C-parts include the Automobile Spare Parts Dealer’s Association, the Fastener Manufactures Association of India, the Fasteners Association of India, The National Fastener Distributors Association (NFDA), World Bearing Association (WBA), and Eastern India Ball Bearing Merchants Association (EIBBMA).

Fastenal Co; W W Grainger Inc.; ERIKS; RS Group Plc; Kaman Corp.; Würth Industrie Service GmbH & Co. KG; Ningbo yi pian hong fastener Co., Ltd; Bossard Holding AG; MCMASTER-CARR; Fabory; Nederland B.V. Bailey International LLC; and Exim & Mfr Enterprise are among the key players profiled in the C-parts market report. In addition to these players, several other essential market players have also been studied and analyzed to get a holistic view of the global C-parts market and its ecosystem.

The scope of the C-parts market report focuses on North America (the US, Canada, and Mexico), Europe (Germany, France, Italy, the UK, Russia, and the Rest of Europe), Asia Pacific (Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific), Middle East & Africa (South Africa, Saudi Arabia, the UAE, and the Rest of MEA), and South America (Brazil, Argentina, and the Rest of SAM). Asia Pacific accounted for the largest C-parts market share in 2024, followed by North America and Europe, respectively.

North America accounted for the second-largest share of the global C-parts market in 2024, with the US holding the largest North America C-parts market share in 2024; it is expected to continue to retain its dominance during the forecast period. The C-parts market in the US is evolving, with strong growth in sectors such as automotive, aerospace, and construction. Advancements in technologies such as 3D printing, automation, and electrification are driving demand for more specialized, lightweight, and sustainable C-parts. For instance, 3D printing has the potential to reduce material costs by up to 50% and decrease time-to-market by up to 64%, offering significant efficiencies in production processes. Increasing demand for sustainable and eco-friendly products is also influencing the adoption of C-parts. Manufacturers are increasingly seeking parts made from recyclable or renewable materials. For example, fasteners with corrosion-resistant coatings are becoming more common to extend product lifespans and reduce environmental impact.

Canada was the second largest shareholder in the global C-parts market in 2024. In 2023, total revenue for the manufacturing sector in Canada accounted for ~US$ 825.2 billion, an increase of 5% as compared to the previous year, 2022. The increasing government investments in the advanced manufacturing sector are driving the demand for C-parts. In 2023, the government invested US$ 177 million for the expansion of next-generation manufacturing. Advanced manufacturing typically involves high-tech processes such as automation, robotics, 3D printing, and precision machining. C-parts are essential to the efficient functioning of these operations, as they are typically low-cost, high-volume, and non-critical components. Canada's automotive sector has particularly invested in the electric vehicle (EV) segment. In 2023, more than US$ 90 billion was invested in Canada for electric vehicle-related manufacturing. The Canadian federal government invested US$ 7.5 million in 35 projects through the Zero-Emissions Vehicles Awareness Initiative (ZEVAI). In 2024, capital expenditures in the Canadian automotive industry are projected to surpass US$ 6 billion, with a substantial portion allocated to machinery and equipment. In May 2022 and April 2023, Canada ranked as the second-largest destination for US civil aircraft, engines, and parts exports, receiving ~US$ 8.99 billion worth of these items. Thus, increasing exports in the automotive and aerospace sectors across Canada drive the C-parts market growth.

Contact Us

Phone: +1-646-491-9876

Email Id: sales@theinsightpartners.com