Asymptomatic Cases Held Largest Share of Gastric Cancer Diagnostic Procedure Market in 2022

According to The Insight Partners research study on "Gastric Cancer Diagnostic Procedure Market Forecast to 2028 – COVID-19 Impact and Global Analysis – by Healthcare Provider, Symptom Type, Body Fluid, Procedure, Offering, and Disease Indication,” the gastric cancer diagnostic procedure market is expected to grow from US$ 1,307.96 million in 2022 to US$ 1,912.03 million by 2028; it is estimated to record a CAGR of 6.5% from 2022 to 2028. A rise in the prevalence of gastrointestinal diseases and surging cases of Helicobacter pylori infection are the factors that contribute to the market growth. However, the shortage of medical laboratory professionals hinders the gastric cancer diagnostic procedure market growth.

Rise in Prevalence of Gastrointestinal Diseases Boosts Gastric Cancer Diagnostic Procedure Market

According to the American College of Gastroenterology, gastroesophageal reflux disease (GERD) is one of the most common gastrointestinal (GI) diseases, and ~20% of the US population suffers from the condition. According to the Hereditary Diffuse Gastric Cancer (HDGC) study by the National Library of Medicine, ~1–3% of gastric cancer cases are hereditary. HDGC has a global population incidence of ~5–10/100 births. Despite declining incidence and mortality during the last decades, stomach cancer is perceived as one of the main health challenges worldwide. According to the GLOBOCAN, stomach cancer caused ~800,000 deaths (accounting for 7.7% of all cancer-related deaths) in 2020. The disease ranks as the fourth leading cause of cancer deaths in both genders combined. ~1.1 million new cases of stomach cancer were diagnosed in 2020, accounting for 5.6% of all cancer cases. Asia accounts for ~75% of the new stomach cancer cases and deaths reported globally. Western countries, such as the US and Canada, report high GI disease incidence rates, which can be attributed to increasing obesity in the adult population and less consumption of dietary fiber. According to data released by the Centers for Disease Control and Prevention, in December 2022, physicians’ offices in the US record ~37.2 million cases of digestive system diseases. Thus, the increasing prevalence of GI disease results in a high risk of developing gastric cancer, which drives the growth of the gastric cancer diagnostic procedures market.

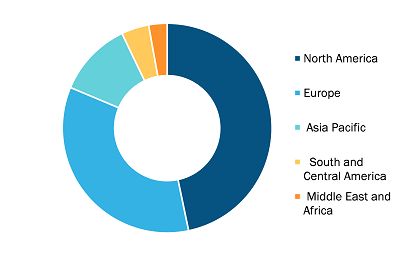

Gastric Cancer Diagnostic Procedure Market, by Region, 2022 (%)

Gastric Cancer Diagnostic Procedure Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Healthcare Provider (Diagnostic Laboratories, Hospitals, Cancer Research Institutes, Oncology Specialty Clinics); Symptom Type (Symptomatic, Asymptomatic); Body Fluid (Blood, Urine, Saliva, Stomach Wash/Gastric Juice, Tissue); Procedure (Endoscopic Procedures, Biopsy & Tissue Tests, Lab Tests, In-Vitro Diagnostic Tests, Imaging Tests, Molecular Diagnostics, Multiplexing Molecular Diagnostics & Immunoassays); and Geography

Gastric Cancer Diagnostic Procedure Market Insights & Growth Scope 2034

Download Free Sample

Based on healthcare provider, the gastric cancer diagnostic procedure market is segmented diagnostic laboratories, hospitals, cancer research institutes, oncology specialty clinics, and others. In 2022, the hospitals segment accounted for the largest market share. However, the diagnostic laboratories segment is expected to register the highest CAGR during 2022–2028. In hospitals, several options are available to manage and treat gastric cancer, including surgeries, chemotherapy, and radiation (provided either before or after surgery). Advancements in gastric cancer treatments offered by hospitals boost the gastric cancer diagnostic procedure market for the hospitals segment. For instance, Texas Center for Proton Therapy offers proton therapy that uses precisely targeted proton beams that deliver high doses of radiation to destroy cancerous cells, reducing recurrence rates for many cancer cases. It is a noninvasive technique and reduces side effects.

The COVID-19 pandemic had a detrimental impact on cancer care. According to the National Center for Biotechnology Information (NCBI), the pandemic led to delays in diagnosis. Most hospitals deprioritized non-COVID-19 treatments in 2020. For instance, hospitalization for chemotherapy declined by 60% in England in the second and third quarters of 2020. However, increased adoption of recently launched products in several countries and increased diagnosis rate are anticipated to fuel market growth. For instance, in October 2021, Agilent Technologies Inc. received CE-IVD mark approval for the PD-L1 IHC 28-8 pharmDx, which is meant to provide options for the first-line treatment of adult patients with HER2-negative advanced or metastatic gastric, gastroesophageal junction, or esophageal cancers.

Atlas-Link Biotech Co Ltd, Bio-Rad Laboratories Inc, MiRXES Pte Ltd, Agilent Technologies Inc, F. Hoffmann-La Roche Ltd, bioMerieux SA, Thermo Fisher Scientific Inc, Illumina Inc, Vela Diagnostics Holding Pte Ltd, and Myraid Genetics Inc. are among the key companies operating in the gastric cancer diagnostic procedure market.

The report segments the gastric cancer diagnostic procedure market as follows:

The gastric cancer diagnostic procedure market is segmented on the basis of healthcare provider, symptom type, body fluid, procedure, offering, disease indication, and geography. Based on healthcare provider, the market is segmented into diagnostic laboratories, hospitals, cancer research institutes, oncology specialty clinics, and others. By symptom type, the gastric cancer diagnostic procedure market is bifurcated into symptomatic and asymptomatic. In terms of body fluid, the gastric cancer diagnostic procedures market is divided into blood, urine, saliva, stomach wash/gastric juice, tissue, and others. In terms of procedure, the market is segmented into endoscopic procedures, biopsy & tissue tests, lab tests, in-vitro diagnostic tests, imaging tests, molecular diagnostics, multiplexing molecular diagnostics & immunoassays, and others. The endoscopic procedures segment is further bifurcated into esophagogastroduodenoscopy (EGD) and endoscopic ultrasound (EUS). Based on offering, the gastric cancer diagnostic procedures market is segmented into instruments, reagents & consumables (including kits), and services. In terms of disease indication, the market is bifurcated into early gastric cancer and gastric cancer advanced types.

Based on geography, the gastric cancer diagnostic procedure market is segmented into North America (the US, Canada, and Mexico), Europe (the UK, Germany, France, Italy, Spain, and Rest of Europe), Asia Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia Pacific), the Middle East & Africa (the UAE, Saudi Arabia, South Africa, and Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America).

Contact Us

Phone: +1-646-491-9876

Email Id: sales@theinsightpartners.com