Hip Implants Dominated Pediatric Orthopedic Implants Market Based on Type in the forecast Period 2022-2030

According to our new research study on "Pediatric Orthopedic Implants Market Forecast to 2030 – Global Analysis – by Type, Application, and End User," the pediatric orthopedic implants market size was valued at US$ 3,812.77 million in 2022 and is projected to reach US$ 8,502.17 million by 2030. It is estimated to register a CAGR of 10.5% during 2022–2030.

Based on type, the pediatric orthopedic implants market is segmented into hip implants, spine implants, knee implants, dental implants, craniomaxillofacial implants, and others. In 2022, the hip implants segment held the largest share of the market. The knee implants segment is expected to record the fastest CAGR during 2022–2030. Hip implants relieve pain and restore mobility associated with hip diseases and arthritis. Inflammation, hip fracture, and natural wear-and-tear are common reasons for hip replacement surgery. Orthopedic hip implants are commonly used in pediatric patients to treat traumatic injuries and developmental hip dysplasia. Total hip replacement in the pediatric population requires a broad array of additional considerations because of the age and functional demands of these patients. Hip implants are commonly used during the treatment of patients diagnosed with hip dysplasia. In the US, 1 in 1,000 babies is born with hip dysplasia annually. Thus, the increasing incidence of hip dysplasia is anticipated to drive the pediatric orthopedic implants market for the hip implants segment. However, total hip arthroscopy is rarely recommended in children, which limits the use of hip implant products and hinders the pediatric orthopedic implants market growth to some extent.

Region Analysis – Pediatric Orthopedic Implants Market

Pediatric Orthopedic Implants Market Size and Forecast (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Hip Implants, Spine Implants, Knee Implants, Dental Implants, Craniomaxillofacial Implants, and Others); Application (Trauma & Deformity, Broken Bones, Bone and Joint Infection, Spinal Deformities, and Others); End User (Hospitals, Pediatric Clinics, and Others), and Geography

Pediatric Orthopedic Implants Market SWOT Analysis by 2030

Download Free Sample

Juvenile idiopathic arthritis (JIA) that causes swelling and stiffness in joints is a form of arthritis that is common in children. Durable knee implants play an important role in the management and treatment of JIA. Joint replacement offers dramatic benefits for the treatment of JIA. For instance, the incidence rate estimates for JIA range from 4 to 14 cases per 100,000 children annually in the US. Increasing participation in youth sports may increase the risk of knee injuries in children. According to the American Academy of Pediatrics (AAP), anterior cruciate ligament (ACL) tears in kids aged 6–18 have increased by about 2.3% each year over the past 20 years.

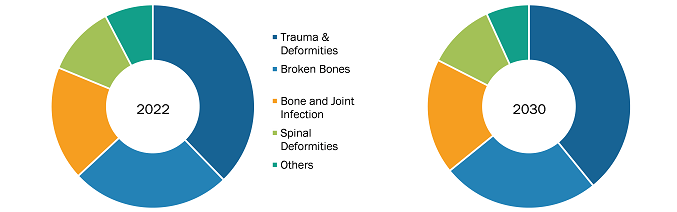

Based on application, the pediatric orthopedic implants market is classified into trauma and deformities, broken bones, bone and joint infection, spinal deformities, and others. In 2022, the trauma and deformities segment held the largest share of the market. It is further expected to register the highest CAGR during 2022–2030. The line of treatment of pediatric orthopedic trauma and deformities is evolving worldwide due to congenital diseases, developmental disorders, or acquired problems. Nonprofit organizations are taking initiatives to improve clinical outcomes and improve the management of orthopedic trauma in children. For instance, Children’s Hospital Colorado works closely with a multidisciplinary team appointed at the Orthopedics Institute, including orthopedic surgeons, rehabilitation providers, plastic surgery providers, and infectious disease specialists, to provide comprehensive care and ensure the best possible outcome for children. Moreover, congenital deformities involving the skeleton represent a major healthcare burden in Europe and other countries. According to the European Platform on Rare Disease Registration, the prevalence of skeletal dysplasia was 2 cases per 10,000 births in 2021 in Europe.

Based on end user, the pediatric orthopedic implants market is classified into hospitals, pediatric clinics, and others. In 2022, the hospitals segment accounted for the largest share of the market. The market for this segment is estimated to grow at a significant CAGR during 2022-2030. An orthopedic hospital is a medical facility focusing on diagnosing, treating, and managing musculoskeletal diseases and injuries. Due to the availability of advanced technologies and facilities, orthopedic hospitals are usually preferred for hip replacement, spine surgery, fractures, etc. Moreover, public and private hospitals are taking initiatives to improve and expand clinical services through partnerships and collaborations. In November 2022, NCH Healthcare System partnered with the Hospital for Special Surgery based in New York. In March 2021, CarePoint Health (a continuous provider of health care) collaborated with Rothman Orthopaedic Institute (a world leader in the field of orthopedics serving communities in Pennsylvania) to establish a comprehensive orthopedic services institute at Hoboken University Medical Center and Christ Hospital in Jersey City. This collaboration helps develop and enhance a broad array of high-quality orthopedic programs for medical, surgical, and related issues. Moreover, this collaboration expanded the availability of these clinical services in Hudson County and ensured access to convenient, patient-centered orthopedic care.

Based on geography, the pediatric orthopedic implants market is segmented into North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America. North America is the largest contributor to the growth of the pediatric orthopedic implants market, and Asia Pacific is expected to be the fastest-growing market in the coming years. The market growth in North America is attributed to the increasing cases of birth deformities and the rising implementation of growth strategies by key market players operating in this region. In addition, the growing health expenditures in major countries would drive market growth in the region during the forecast period. The US has a large number of clinics providing advanced surgical services, wherein the number of orthopedic surgeries performed is increasing notably. The World Health Organization (WHO) states road traffic injuries as the 8th leading cause of death among pediatric individuals. According to the Centers for Disease Control and Prevention (CDC), ~9.2 million children in the US are admitted to the emergency department for the treatment of accidental injuries such as falls and road traffic. The increasing number of traumatic injuries and road accidents, and the rising prevalence of congenital or acquired face deformities, coupled with technological advancements in plastic surgery procedures, contribute to the pediatric orthopedic implants market in the US. The Federal and state governments in the country offer various funds and support for orthopedic procedures. For instance, the Orthopaedic Research Program (US) supports clinical, epidemiological, and research outcomes in orthopedics and musculoskeletal rehabilitation. The funded studies focus on the preclinical testing and development of orthopedic devices/implants, human subject implant wear, and osteolysis.

Various types of implants are used in the treatment of pediatric orthopedic patients for the reduction of fractures or correction of other indications such as congenital anomalies of the musculoskeletal system. In the US, falls are the leading reason for emergency department visits paid to seek treatments for child injuries. According to a study titled "The Burst of Musculoskeletal Cancer in the US," traumatic injuries are the leading cause of death among children and adolescents in the US, causing 20,000 deaths annually. Trauma leads to injuries to the musculoskeletal system. In January 2023, Arthrex received US Food and Drug Administration (FDA) approval for its TightRope implant, which became the first and only device approved for pediatric ACL surgery. ACL injuries occur primarily in the young and active population and are typically caused by noncontact twisting or hyperextension injuries; they can also result from contact injuries.

Johnson & Johnson, Arthrex Inc., Stryker Corp, OrthoPediatrics Corp, WishBone Medical Inc., Samay Surgical Pvt Ltd., Vast Ortho Pvt Ltd., Merete GmbH, and Suhradam Ortho are among the leading companies operating in the pediatric orthopedic implants market.

Contact Us

Phone: +1-646-491-9876

Email Id: [email protected]