Additive Manufacturing Material Market Share, Growth & Forecast by 2034

Additive Manufacturing Material Market Size and Forecasts (2021–2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage : By Technology (Stereolithography, Fused Deposition Modeling, Laser Sintering, and Other Technologies), End User (Aerospace and Defense, Automotive, Healthcare, Industrial and Other End Users), Material (Plastic, Metals, and Ceramics)

- Status : Data Released

- Report Code : TIPRE00039700

- Category : Manufacturing and Construction

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 10, 2026

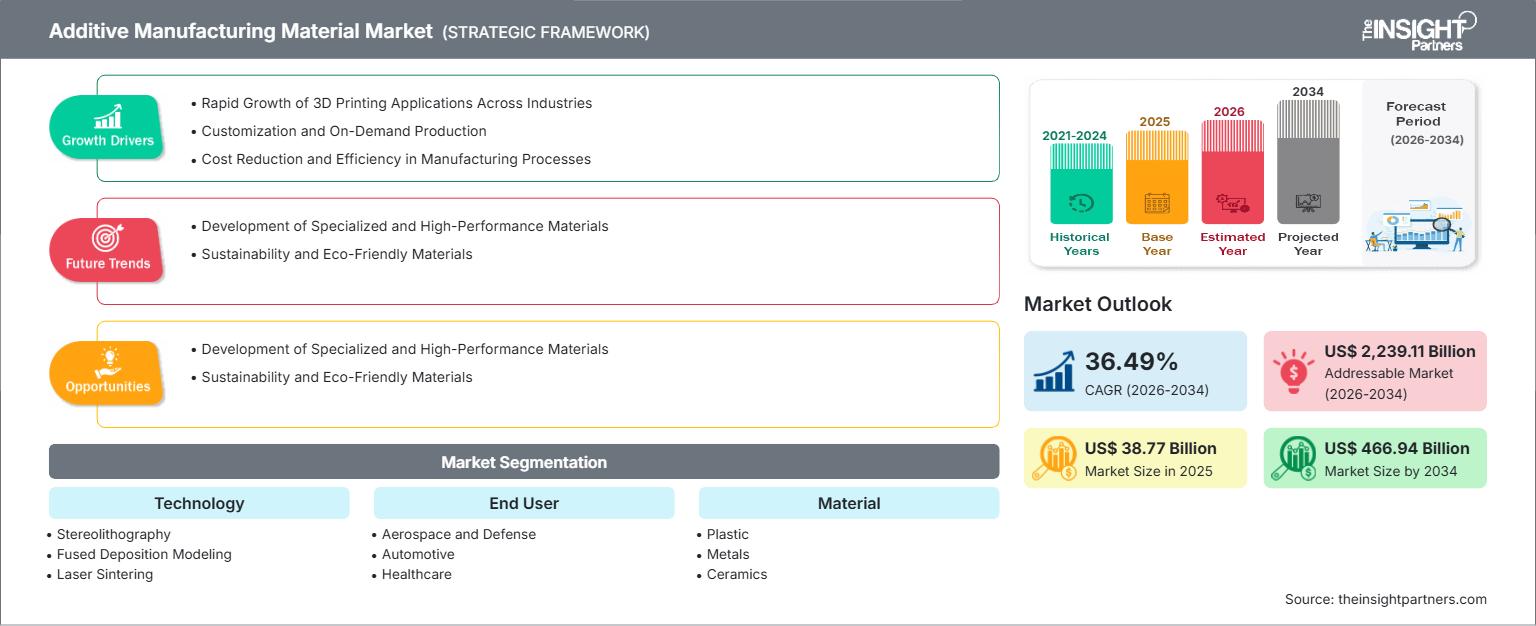

2025 Market Size

US$ 38.77 Bn

Base year value

2034 Forecast

US$ 466.94 Bn

Projected by 2034

CAGR 2026-2034

36.49 %

Growth rate

Addressable Market

US$ 2,239.11 Bn

(2026-2034)

The additive manufacturing material market size was valued at US$ 38.77 billion in 2025 and is forecast to reach US$ 466.94 billion by 2034. In the period between 2026 and 2034, it is anticipated to witness a CAGR of 36.49%. Market growth can be attributed to increased use of qualified polymers, metal powders, photopolymers, ceramics, and composite feedstocks.

According to the additive manufacturing material market report, the North American region will grow at a CAGR of 33–35% during 2026–2034, owing to the aerospace qualification program, medical device manufacturing, and supply chain localization driven by the defense sector. The United States continues to be the leading market because feedstock manufacturers and original equipment manufacturers have been aligning with repeatable production processes and digitization.

Additive Manufacturing Material Market Assessment and Insights

- North America accounted for 34–36% additive manufacturing material market share in 2025 and is expected to grow at a 33–35% CAGR during 2026–2034, driven by aerospace, medical, and defense production programs.

- The US represented 78–82% of North America in 2025 and is expected to grow at a 34–36% CAGR as qualified materials move into regulated applications.

- Europe held 24–26% share in 2025 and is projected to grow at a 32–34% CAGR, led by Germany, the UK, France, Italy, and Spain.

- Asia Pacific held 27–29% share in 2025 and is forecast to grow at a 38–40% CAGR, led by China, Japan, South Korea, and India.

- Largest Segment: Plastic held 52–56% market share in 2025 and is expected to register a 34–36% CAGR through 2034 due to broad industrial and healthcare use.

- High Growth Segment: Metals held 31–35% market share in 2025 and is expected to register a 39–41% CAGR through 2034 as aerospace and orthopedic demand rises.

- Key companies analyzed in detail: 3D Systems Corporation, GE Additive, Desktop Metal, Inc., EnvisionTEC GmbH, EOS GmbH, The ExOne Company, MakerBot Industries, LLC, Materialise NV, Optomec Inc., Stratasys Ltd., Arkema S.A., and BASF SE.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The Additive Manufacturing Material Market has evolved from prototyping material supply to certified production material supply, in which material traceability is as important as printer output. Polymers by extrusion and resins in photopolymer processes continue to be popular for fixtures, dental molds, and design confirmation applications, whereas laser sintering and metal powder bed fusion applications are increasing in use for regulatory parts. The supplier competition is increasingly centered on material repeatability, powder structure, recycling processes, and material qualification for applications.

In the additive manufacturing material market outlook, it is predicted that by 2034, new industrial centers in the Asia-Pacific and Middle Eastern regions will drive higher consumption of localized materials as governments establish advanced manufacturing centers and hospitals adopt personalized devices. The regulatory windfall in the form of medical equipment certification, aviation material standards, and circular manufacturing policies would help suppliers who have evidence of consistency, recyclability, and mechanics.

Additive Manufacturing Material Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 38.77 Billion |

| Market Size by 2034 | US$ 466.94 Billion |

| Global CAGR (2026 - 2034) | 36.49% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Additive Manufacturing Material Market Analysis

Demand is greatest where additive manufacturing results in weight savings, shortened lead times, or minimized tooling. Aerospace applications employ nickel, titanium, and high-performance polymers in certified components; healthcare employs biocompatible resins and metals in dental, orthopedic, and surgical planning applications; automotive employs polymers in jigs, fixtures, and limited-series components. The additive manufacturing material market is expanding in scope as end users move beyond pilot cells into serial production.

The value chain includes powder atomizers, polymer compounding facilities, resin formulators, printer OEMs, service bureaus, software suppliers, and certifying agencies. Tightening supply dynamics center on the development of qualified feedstock programs in response to production customers' needs for consistent particle-size distributions, moisture levels, thermal properties, and post-processability. As a consequence, growth in the additive manufacturing material market will depend more on application qualification than on individual equipment purchases.

Competition is concentrating on integrated material-printer-software systems. 3D Systems Corporation, Stratasys Ltd., EOS GmbH, Materialise NV, and GE Additive focus on regulated workflows, whereas Arkema S.A. and BASF SE bolster their specialty polymers. Desktop Metal, Inc., The ExOne Company, and Optomec Inc. back their metal and binder-jetting solutions; therefore, the analysis of the additive manufacturing material market is increasingly focused on end-use efficiency.

Investment activity focuses on materials that have proven mechanical properties, comply with healthcare regulations, and are traceable for aerospace applications. Suppliers are aligning on proprietary resin systems, recyclable thermoplastic materials, metal powders, and factory software to reduce waste. The share of suppliers with closed-loop quality data in the additive manufacturing material Market will increase due to customer priorities.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Additive Manufacturing Material Market: Strategic Insights

Regional Insights

North America additive manufacturing material

The North American region accounted for 34-36% of the market share in 2025 and is expected to grow at a CAGR of 33-35% between 2026 and 2034. Demand from aerospace & defense, medical devices, and industrial tooling customers is supported by the integration of material qualification and lot traceability, along with manufacturing repeatability, into procurement processes.

US defense applications, the aerospace supply chain in Canada, and the automotive manufacturing sector in Mexico provide a balanced demand profile in this region. While plastics continue to be used for tooling and fixtures, metals will benefit from titanium, aluminum, and nickel alloys. Thus, the Additive Manufacturing Material market trends in North America center on certifiable materials, larger builds, and post-processing capabilities.

U.S. additive manufacturing material Market

The US accounted for 78–82% of North America in 2025 and is projected to grow at a 34–36% CAGR during 2026–2034. Demand is supported by aerospace primes, medical device clusters, automotive engineering centers, and defense modernization programs. Domestic reshoring initiatives increase demand for certified metal powders, engineering thermoplastics, and high-temperature resins.

3D Systems Corporation, Stratasys Ltd., GE Additive, Desktop Metal, Inc., The ExOne Company, and Optomec Inc. maintain strong US activity through printer platforms, materials programs, or industrial service networks. Application trends include dental devices, surgical planning, aviation interiors, tooling, casting patterns, and spare-part production, reinforcing domestic additive manufacturing material Market demand.

Europe additive manufacturing material Market

Europe represented 24–26% share in 2025 and is expected to record a 32–34% CAGR through 2034, with Germany as the leading country. The UK market is supported by aerospace, defense, motorsport, and medical design services, where engineering polymers and metals enable low-volume certified parts and rapid tooling.

German leadership in regional acceptance is evident in machine construction, automotive engineering, industrial automation, and powder bed fusion technology. EOS GmbH, BASF SE, and specialist material providers improve the availability of metal powders, photopolymers, and engineering thermoplastics. More and more often, demand is driven by qualified production cells and not just prototyping laboratories.

Countries like France, Italy, and Spain support additive manufacturing regionally in aerospace supply chains, dental laboratories, industrial equipment, and energy components. While the French industry focuses on aviation and medicine, Italy focuses on tools and design-driven manufacturing. Spain profits from its automotive industry and renewable energy components, which require lightweight materials.

APAC additive manufacturing material Market

Asia Pacific held 27–29% share in 2025 and is projected to grow at a 38–40% CAGR during 2026–2034. China is the leading country, supported by electronics, automotive, aerospace, dental, and industrial policy programs that favor local production of polymers and metal powders.

Japan and South Korea emphasize precision manufacturing, robotics, semiconductor tooling, and medical devices, creating demand for stable resins and engineering plastics. India is scaling additive manufacturing centers for defense, healthcare, and education, while Australia uses metal printing in mining, medical, and aerospace maintenance applications.

Middle East & Africa additive manufacturing material Market

Middle East & Africa is expected to grow at a 35–37% CAGR during 2026–2034. Saudi Arabia is the leading country, supported by industrial diversification, energy infrastructure, and localization strategies. The UAE uses additive manufacturing in construction components, aviation maintenance, and healthcare applications.

South Africa contributes through mining equipment, medical devices, and university-led metal printing research, while the rest of MEA remains early-stage. Regional demand is strongest where spare parts, energy assets, and infrastructure maintenance benefit from shorter lead times and reduced dependence on imported components.

Segmentation Analysis

Technology

The technology segment is expected to grow at a 35–37% CAGR during 2026–2034 as users select processes based on geometry, throughput, surface finish, and material compatibility. Stereolithography supports precision resin applications, fused deposition modeling scales polymer tooling, and laser sintering enables powder-based industrial parts. Process choice increasingly determines material qualification costs and production economics.

- Stereolithography maintains strong demand in dental, medical modeling, jewelry, and high-detail prototyping because photopolymer resins deliver smooth surfaces, dimensional accuracy, and repeatable small-batch production.

- Fused Deposition Modeling leads practical factory adoption for jigs, fixtures, thermoplastic prototypes, and low-volume parts because machines are accessible, materials are diverse, and workflows are familiar.

- Laser Sintering supports functional polymer and metal powder applications where complex geometries, consolidated assemblies, and mechanical strength justify higher material qualification and post-processing requirements.

End User

The end user segment is projected to grow at a 36–38% CAGR from 2026 to 2034 as adoption broadens from prototyping to validated production. Aerospace and defense require lightweight certified materials, automotive users prioritize tooling and customization, healthcare emphasizes patient-specific solutions, and industrial users focus on spare parts, fixtures, and process efficiency.

- Aerospace and Defense generates high-value demand for titanium, nickel alloys, and flame-retardant polymers where lightweighting, part consolidation, and certified repeatability outweigh material cost sensitivity.

- Automotive adoption is concentrated in prototyping, tooling, motorsport, electric vehicle components, and low-volume customization, with polymers dominating today and metals expanding in performance applications.

- Healthcare remains strategically important because dental, orthopedic, surgical planning, and prosthetic workflows require biocompatible materials, traceable batches, and repeatable patient-specific production.

- Industrial end users adopt materials for fixtures, spare parts, molds, and maintenance tooling, especially where downtime reduction and local production justify qualification investments.

Material

The material segment is expected to grow at a 36–38% CAGR during 2026–2034. Plastic holds the largest 52–56% share because thermoplastics and photopolymers suit broad workflows. Metals are the high-growth group with 31–35% share and 39–41% CAGR, driven by aerospace, medical, and energy applications. Ceramics remain specialized but valuable for thermal and biomedical use.

- Plastic materials dominate installed workflows because filaments, powders, and resins support prototypes, tooling, dental models, fixtures, and functional parts at manageable qualification cost.

- Metals are expanding in high-value applications requiring strength, heat resistance, or lightweighting, especially titanium, aluminum, stainless steel, nickel alloys, and cobalt-chrome powders.

- Ceramics serve demanding niches in dental, biomedical, electronics, chemical processing, and high-temperature applications where wear resistance, insulation, or biocompatibility creates strategic value.

Opportunity Snapshot

| End User | Revenue Contribution | Trend Tag | Adoption Stage |

| Aerospace and Defense | High | Certified Parts | Scaling |

| Automotive | Medium | EV Tooling | Scaling |

| Healthcare | High | Patient Specific | Mature |

| Industrial and Other End Users | Medium | Spare Parts | Scaling |

Additive Manufacturing Material Market Growth Drivers and Impact Analysis

Shift from Prototyping to Certified Production

Industrial customers are adopting additive manufacturing processes in serial production, where the qualification of materials, their traceability, and repeatability influence material purchase decisions. The aerospace and healthcare industries need proven mechanical performance, sterilization resistance, and consistent batches, hence increased demand for qualified materials rather than general materials. This will lead to higher revenue per customer since qualified materials are used consistently in the production process.

Lightweighting Across Aerospace and Mobility

There is increased reliance on additive manufacturing in aircraft, spacecraft, electric vehicles, and performance cars to reduce weight, integrate assemblies, and accelerate development processes. Lightweight components minimize fuel and energy consumption, while lattice designs and topological optimizations enable forms that are not possible with conventional machining processes. This leads to higher demand for aluminum, titanium, nickel, carbon-reinforced polymers, and flame-retardant plastics. The impact on the market will be greatest where the cost of materials is justified.

Healthcare Personalization and Dental Digitization

Demand for healthcare is growing due to the capability to manufacture patient-specific implants, surgical guides, dental prosthesis, anatomical models, and orthotics using additive manufacturing technology. Resin materials are used by dental laboratories for their speed and consistency, whereas titanium and cobalt-chrome materials are used in the orthopedics and cranio-maxillofacial sectors. The consequence of this trend is that there will be continuous consumption of materials based on clinical workflows rather than on prototyping.

Additive Manufacturing Material Market Future Trends

Closed-Loop Material Qualification Platforms

Future adoption depends on the development of platforms that connect material certificates, printer settings, build supervision, post-processing, and part inspection into a single quality document. Such an approach will speed up the qualification process and help manufacturers duplicate validated builds at different sites. Material producers with digital passports, reused powder records, and data analysis capabilities will be better able to retain their customers. It is also beneficial for auditing in medical, aviation, and military applications that require documentation.

Sustainable and Recycled Feedstock Adoption

The additive manufacturing material market forecast indicates that polymer recycling, powder recovery processes, and sustainable manufacturing methods will gain prominence as producers align additive manufacturing with sustainability goals. The subsequent step will focus on maintaining mechanical characteristics while minimizing virgin material use and packaging waste. Companies that can demonstrate the performance, moisture resistance, and processability of their recycled materials will have an edge in procurement. Sustainability will thus evolve from being just a marketing message into becoming a material qualification process.

Additive Manufacturing Material Market Opportunities

Localized Production Networks for Critical Spare Parts

Downtime can be minimized through material qualification for distributed spare-part manufacturing. This possibility is particularly prominent for spare parts with low annual volume, high inventory costs, long lead times, or obsolete tooling. Material providers will be able to leverage the value created by providing application kits and qualified process parameters, as well as by supplying security on a regional basis.

Medical-Grade Materials for Regulated Point-of-Care Manufacturing

Hospitals, dental clinics, and orthopedic centers are considering point-of-care manufacturing for surgical guides, models, splints, dentures, and patient-specific implants. There is an opportunity for materials manufacturers to develop biocompatible resins, sterilizable polymers, and metal powders that meet regulatory standards and documentation requirements. This goes beyond merely selling materials, as training and validation are also needed. Manufacturers who make this easy will be in demand.

Recent Developments

- June 2026: Stratasys Ltd. — the company announced certified flame-retardant FDM material for rail-ready additive manufacturing, strengthening its transportation materials portfolio and supporting applications that require safety, compliance, and repeatable thermoplastic performance. The launch aligns with demand for regulated polymer parts in mobility and industrial systems.

- April 2026: EOS GmbH — EOS announced the acquisition of Metalpine, expanding its industrial metal additive manufacturing capabilities and strengthening access to advanced metal powder expertise. The move supports customer demand for qualified metal materials, tighter supply control, and production-grade powder bed fusion workflows.

- November 2025: 3D Systems Corporation — the company introduced next-generation stereolithography solutions at Formnext 2025, reinforcing its focus on productivity, precision, and resin-based production workflows. The announcement supports demand for high-throughput photopolymer materials across dental, industrial, and healthcare applications.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends