Educational Furniture Market Share, Growth & Demand by 2034

Coverage: By Material (Wood, Plastic, Metal, and Others), Product Type (Benches and Chairs, Desks and Tables, Storage Units, and Others), and End Use (Institutional [Elementary School, Secondary School, and Higher Education] and Residential)

- Status : Data Released

- Report Code : TIPRE00028349

- Category : Consumer Goods

- No. of Pages : 150

- Available Report Formats :

- Last update date : March 18, 2026

2025 Market Size

US$ 8.98 Bn

Base year value

2034 Forecast

US$ 14.27 Bn

Projected by 2034

CAGR 2026-2034

5.3 %

Growth rate

Addressable Market

US$ 105.56 Bn

(2026-2034)

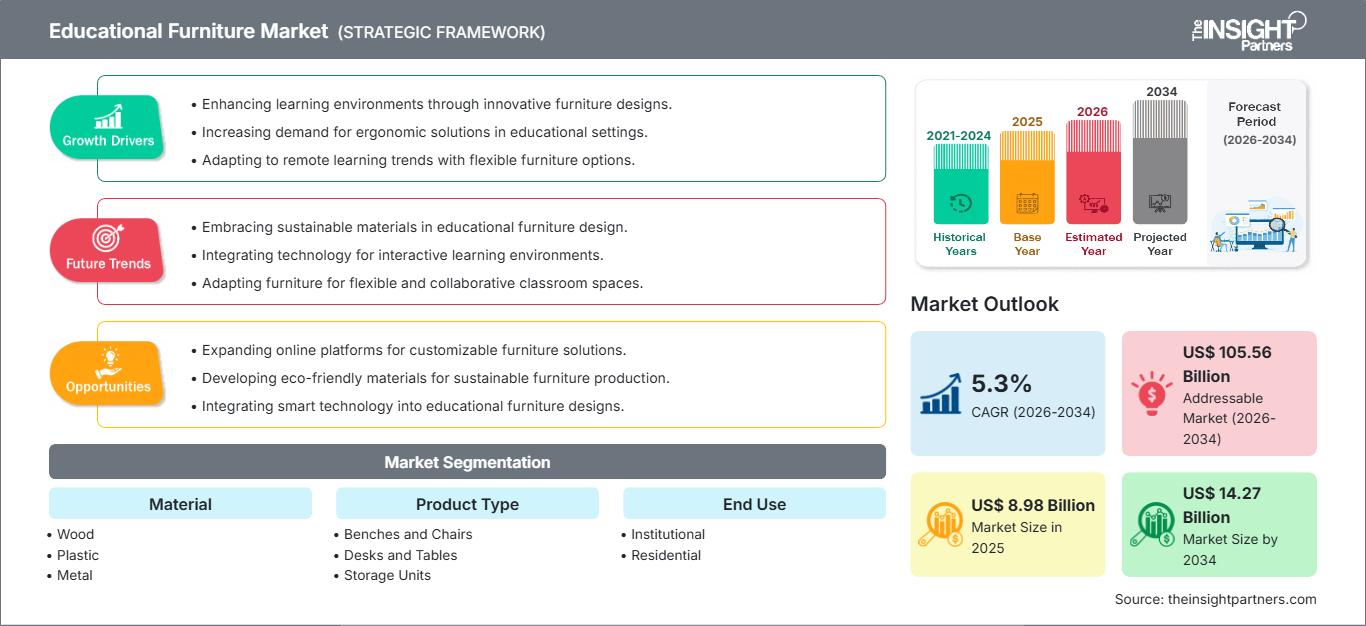

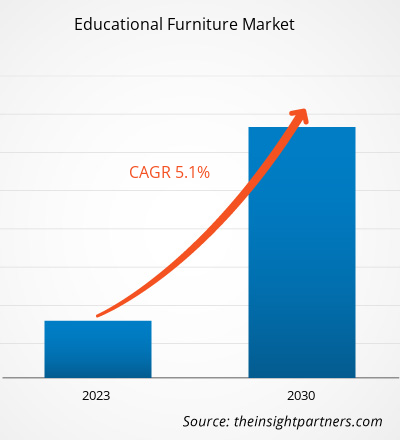

The global Educational Furniture Market size is projected to reach US$ 14.27 billion by 2034 from US$ 8.98 billion in 2025. The market is anticipated to register a CAGR of 5.30% during the forecast period 2026–2034

Key market dynamics include a heightening global focus on inclusive and sensory-friendly learning environments, rising demand for technology-integrated modular assets, and a significant shift toward biophilic design principles. Additionally, the market is expected to benefit from the growing adoption of hybrid learning infrastructures, the expansion of STEM-focused laboratory facilities in emerging economies, and the increasing inclusion of mobile, lightweight furniture that facilitates rapid classroom reconfiguration.

Educational Furniture Market Analysis

The educational furniture market analysis reveals a decisive move toward agile infrastructure as institutions transition from passive to active pedagogy. It indicates the market is in a durability-first sector for public K-12 schooling and a high-tech sector for private universities and research hubs. Strategic opportunities are emerging in the neuroarchitecture segment, where furniture is designed to reduce cognitive load and sensory overstimulation, offering a clear competitive advantage in student mental health support. The analysis also notes that market expansion is increasingly tied to the circular economy, with a growing emphasis on refurbish-ready designs and closed-loop material sourcing. Competitive differentiation now stands out depending on branding that highlights indoor air quality certifications, integrated power delivery for 1-to-1 device programs, and tool-free assembly features. This approach helps top-tier vendors secure long-term contracts with large-scale educational districts looking for future-proofed assets.

Educational Furniture Market Overview

Educational furniture has transformed from a static utility into a vital component of the modern learning ecosystem. The market encompasses acoustic decompression shelters, height-adjustable collaborative tables, and mobile caddies for digital tools. Both multinational conglomerates and specialized design boutiques compete in this market, utilizing advanced polymers, sustainably harvested timber, and lightweight alloys. Growing demand for ubiquitous learning, where hallways and cafeterias are converted into productive breakout zones, has increased the popularity of flexible seating as a versatile institutional solution. Asia-Pacific leads in growth due to widespread educational reforms and new campus construction, while North America remains the leader in value due to its early adoption of ergonomic standards and smart classroom technologies. The US market is particularly focused on ADA compliance and inclusive design, ensuring furniture accommodates students of all physical abilities. Competition among brands is fueling the development of AI-driven storage systems and furniture with embedded IoT sensors to track space utilization and student engagement.

Market Assessment and Insights

- Global market for Educational Furniture was valued at US$ 8.98 Billion in 2025

- Annual market size is expected to reach US$ 14.27 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 105.56 Billion

- Market is anticipated to register a CAGR of 5.3% during the forecast period

- The United States represents a key market, supported by Enhancing learning environments through innovative furniture designs., Increasing demand for ergonomic solutions in educational settings., Adapting to remote learning trends with flexible furniture options., as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Expanding online platforms for customizable furniture solutions., Developing eco-friendly materials for sustainable furniture production., Integrating smart technology into educational furniture designs. are expected to influence market dynamics and addressable market

- Report profiles industry participants, including AFC Furniture Solutions Pvt Ltd, Fleetwood Group Inc, Scholar Craft Products Inc, Smith Systems Manufacturing Co, Knoll Inc, Haworth Inc, Vitra International AG, Virco Manufacturing Corp, Office Line Srl, Creaciones Falcon SLU, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Educational Furniture Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Educational Furniture Market Drivers and Opportunities

Market Drivers:

- Proliferation of Hybrid and Blended Learning Models: The rise of digital-first instruction requires furniture that can accommodate video conferencing and collaborative software use, driving demand for tech-enabled desks.

- Global Push for Inclusive and Accessible Classrooms: Legislative mandates for accessibility are forcing schools to replace legacy units with height-adjustable and wheelchair-accessible furniture.

- Rapid Urbanization and Education Reform in Emerging Markets: Massive investments in public education in India and Southeast Asia are creating high-volume demand for durable, cost-effective furniture solutions.

Market Opportunities:

- Expansion into Vocational and Corporate Training: The global reskilling movement offers significant opportunities for specialized workshop furniture and high-durability laboratory benches.

- Growth in Biophilic and Nature-Integrated Design: There is a significant opening for furniture that incorporates organic shapes and natural textures to reduce student stress and improve concentration.

- Focus on Circularity and Product Life-Extension: Offering furniture-as-a-service (FaaS) or buy-back programs for used institutional furniture presents a sustainable path for revenue growth in eco-conscious regions.

Educational Furniture Market Report Segmentation Analysis

The educational furniture market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Material:

- Wood: The leading segment by revenue, favored for its long-lasting properties and inviting aesthetics, particularly in high-end primary and secondary schools.

- Plastic: A fast-growing category driven by the rising adoption of recycled and antimicrobial polymers that are lightweight and easy to sanitize.

- Metal: Critical for specialized environments like chemistry labs and industrial workshops where chemical resistance and structural integrity are paramount.

By Product Type:

- Benches and Chairs: The largest segment, currently undergoing a shift toward active seating and motion-friendly designs that support student focus.

- Desks and Tables: A high-growth segment focusing on nestable and foldable designs that allow classrooms to be cleared for different activities in minutes.

- Storage Units: Evolving from simple lockers to smart storage solutions with integrated charging and AI-managed organization features.

By End Use:

- Institutional: Comprises the majority of the market, driven by bulk procurement for K-12 schools, higher education, and specialized training centers.

- Residential: A rapidly expanding segment fueled by the normalization of remote learning and the need for dedicated, ergonomic study spaces at home.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Educational Furniture Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 8.98 Billion |

| Market Size by 2034 | US$ 14.27 Billion |

| Global CAGR (2026 - 2034) | 5.3% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Material

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Educational Furniture Market Players Density: Understanding Its Impact on Business Dynamics

The Educational Furniture Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Educational Furniture Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for infrastructure providers and modular furniture manufacturers to expand.

The educational furniture market is undergoing a significant transformation, moving from a rigid institutional necessity to a human-centric tool for engagement. Growth is driven by the modernization of teaching methods, a surge in smart campus investments, and the global trend toward sustainable institutional procurement.

1. North America

- Market Share: Holds a dominant position, driven by a shift toward project-based learning and high institutional budgets.

- Key Drivers:

- Integration of charging ports and digital tool support in classroom furniture

- High replacement rates of legacy furniture to meet new ergonomic and safety standards

- Growth in higher education is seeking specialized research lab furniture

- Trends: Adoption of residential comfort in commercial designs, making school spaces feel more inviting and less institutional.

2. Europe

- Market Share: A stable and highly regulated market with a strong focus on circular economy principles and indoor air quality.

- Key Drivers:

- Stringent environmental regulations favoring zero-formaldehyde boards and recycled materials

- Government funding for retrofitting classrooms with energy-efficient and flexible layouts

- Strong cultural preference for high-quality, long-lasting wooden furniture

- Trends: Use of acoustic furniture and dividers to create micro-learning spaces within open-plan school designs.

3. Asia-Pacific

- Market Share: The fastest-growing region, with India and China investing heavily in New Education Policies and infrastructure upgrades.

- Key Drivers:

- Rapid rise in private and international school enrollments

- Government-led initiatives to improve literacy and basic school facilities in rural areas

- Shift toward modern, colorful, and ergonomic designs in urban educational hubs

- Trends: Large-scale B2B contracts for standardized furniture sets, with a growing interest in low-maintenance plastic and metal hybrids.

4. South and Central America

- Market Share: An emerging market focusing on durability and cost-efficiency to serve growing student populations.

- Key Drivers:

- Modernization of public schools to reduce dropout rates and improve learning outcomes

- Rising middle-class investment in high-quality home-study furniture

- Growth of the regional manufacturing base in countries like Brazil

- Trends: Adoption of stackable and multi-purpose furniture to maximize utility in high-density urban school districts.

5. Middle East and Africa

- Market Share: A developing market with a high demand for premium, high-tech campus solutions in the GCC region.

- Key Drivers:

- Strategic investments in world-class education cities and specialized technical universities

- High standards for institutional branding and aesthetic appeal in private education

- Need for durable materials that can withstand local environmental conditions

- Trends: Deployment of smart lockers and technology-embedded lecture hall seating to support digital-first university curricula.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as HNI Corporation, Steelcase Inc., and MillerKnoll. Regional artisanal experts and niche players like Inspace School Furniture, OK Play India, and VS America also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Inclusivity and Accessibility: Position educational furniture as an equalizer by offering height-adjustable and sensory-friendly options that cater to neurodiverse learners.

- Technological Connectivity: Furniture is no longer just a surface; it acts as a hub for charging, cable management, and seamless integration with student laptops and tablets.

- Supply Chain Resilience: Top players manage the entire value chain, from sourcing responsibly harvested wood to using advanced metal fabrication techniques for long-lasting performance.

- Multi-Disciplinary Cooperation: Designers are increasingly working with educators and psychologists to create pieces that support cognitive development and physical wellness.

Opportunities and Strategic Moves

- Target the rising demand for sensory-friendly furniture (e.g., acoustic pods and weighted seating) to support inclusive education initiatives globally.

- Invest in augmented reality (AR) tools that allow educational administrators to virtually stage classrooms with modular furniture before committing to large-scale procurement.

Major Companies operating in the Educational Furniture Market are:

- AFC Furniture Solutions Pvt Ltd

- Fleetwood Group Inc

- Scholar Craft Products Inc

- Smith Systems Manufacturing Co

- Knoll Inc

- Haworth Inc

- Vitra International AG

- Virco Manufacturing Corp

- Office Line Srl

- Creaciones Falcon SLU

Disclaimer: The companies listed above are not ranked in any particular order.

Educational Furniture Market News and Recent Developments

- In February 2026, School Specialty® announced the official launch of its new Childcraft Out2Grow Outdoor Furniture line. Designed to extend learning beyond the traditional classroom, the innovative collection offers a durable, sustainable, and economical way for schools to create engaging, learning environments rooted in exploration, movement, and real-world discovery.

- In March 2024, Smith System announced its collaboration with Landscape Forms to launch 'OpenSpaces', highly durable outdoor school furniture for enhanced learning experiences. OpenSpaces will include nine products, all sourced from Landscape Forms. The Michigan-based manufacturer is known for high-design outdoor furniture and accessories for commercial and public spaces.

Educational Furniture Market Report Coverage and Deliverables

The Educational Furniture Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Educational Furniture Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Educational Furniture Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Educational Furniture Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Educational Furniture Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends