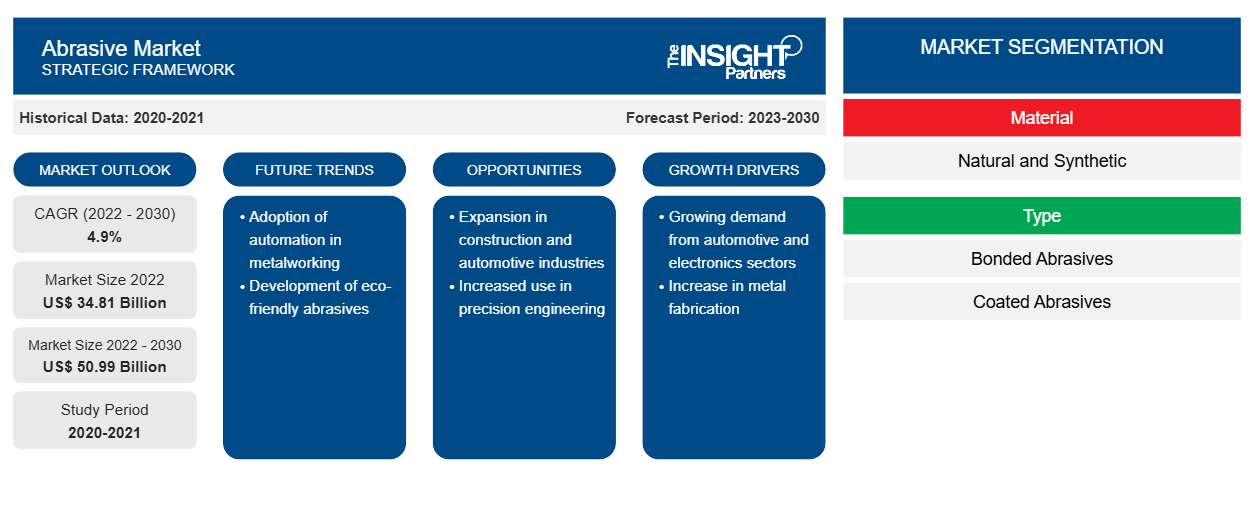

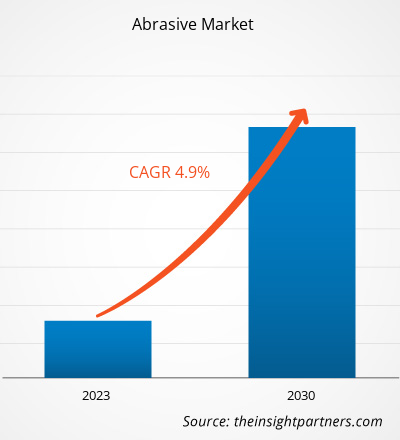

[تقرير بحثي] تم تقييم حجم سوق المواد الكاشطة بـ 34.81 مليار دولار أمريكي في عام 2022 ومن المتوقع أن يصل إلى 50.99 مليار دولار أمريكي بحلول عام 2030؛ ومن المتوقع أن يسجل معدل نمو سنوي مركب بنسبة 4.9٪ من عام 2022 إلى عام 2030.

رؤى السوق ووجهة نظر المحلل:

تُستخدم المواد الكاشطة في تطبيقات مختلفة مثل تلميع الأرضيات والتصنيع والطحن والطحن الدقيق. تُستخدم هذه المواد أيضًا في تطبيقات التلميع الخفيفة في صناعات السيارات والأثاث والتصنيع والبناء. العوامل الرئيسية التي تدفع نمو سوق المواد الكاشطة هي الطلب المتزايد على المواد الكاشطة من صناعات السيارات وتصنيع المعادن والكهرباء والإلكترونيات. تُستخدم المواد الكاشطة في مجموعة واسعة من تطبيقات السيارات مثل طحن الأسطح وإزالة النتوءات والتلميع والصب لتصنيع العجلات؛ قطع وطحن مكونات الجسم؛ إزالة اللحام وشطب الحواف؛ الطلاء والسطح في معالجة وتشكيل رفوف السيارات. أدى النمو في استخدام صفائح الألومنيوم في صناعات النقل والطلب المتزايد على المواد خفيفة الوزن إلى خلق طلب على أدوات فعالة لتطبيقات الطحن والتلميع والقطع. علاوة على ذلك، من المتوقع أن يوفر اعتماد المواد الكاشطة في تطبيقات الأتمتة والروبوتات فرصًا مربحة لنمو سوق المواد الكاشطة .

محركات النمو والتحديات:

تعد صناعة تصنيع السيارات والمعادن المتنامية والطلب المتزايد على المواد الكاشطة من صناعة الكهرباء والإلكترونيات من بين العوامل الرئيسية التي تدفع السوق. تُستخدم المواد الكاشطة في مجموعة متنوعة من تطبيقات الإلكترونيات والفوتونيات مثل التركيب والطحن الدقيق والتلميع وتلميع الرقاقة. في صناعة الإلكترونيات، تتطلب أجهزة التركيب دقة عالية لضمان استقرارها أثناء الاختبار والتحليل. يستخدم أكسيد الألومنيوم وكربيد السيليكون عمومًا في عمليات التركيب نظرًا لصلابتهما العالية واستقرارهما البعدي. يستخدم كربيد البورون أيضًا لتركيب المكونات الحساسة مثل السيراميك ومواد أشباه الموصلات نظرًا لكثافته المنخفضة وصلابته العالية ومقاومته الكيميائية. أدت المبيعات المتزايدة للمكونات الكهربائية والإلكترونية بسبب التحول نحو المركبات الكهربائية والطلب المتزايد على السلع الاستهلاكية الإلكترونية إلى زيادة الطلب على المواد عالية الكفاءة لإنتاج المكونات. وفقًا لتقرير شركة Parker Hannifin Corporation، من المتوقع أن يصل السوق العالمي لأدوات الآلات التي يتم التحكم فيها رقميًا بواسطة الكمبيوتر (CNC) إلى 129 مليار دولار أمريكي بحلول عام 2026. تعد الصين أكبر مركز تصنيع للإلكترونيات في العالم. تعمل عوامل مثل انخفاض تكاليف العمالة وتوافر العمالة الماهرة وسلاسل التوريد السائدة على دفع نمو صناعة الإلكترونيات. كما تُظهر حكومة الهند نهجًا عدوانيًا للترويج للبلاد كسوق بديلة للصين. إن النمو في صناعة الكهرباء والإلكترونيات يحرك سوق المواد الكاشطة.

يمكن أن تعمل التقلبات في أسعار المواد الخام كرادع للسوق. تخضع المواد الكاشطة مثل أكسيد الألومنيوم وكربيد السيليكون لتقلبات الأسعار بسبب عوامل مثل اضطرابات سلسلة التوريد والتوترات الجيوسياسية وتقلبات الطلب. غالبًا ما يتم تداول المواد الخام المستخدمة في المواد الكاشطة كسلع أساسية في الأسواق العالمية، مما يعرضها لديناميكيات سوق السلع الأساسية. يمكن أن تؤثر تكاليف الطاقة، وخاصة لعمليات التصنيع كثيفة الطاقة، بشكل كبير على أسعار المواد الخام. يمكن أن تؤثر التقلبات في أسعار النفط ومصادر الطاقة الأخرى على تكاليف إنتاج المواد الكاشطة وتساهم في تقلب الأسعار. في يونيو 2021، أعلنت شركة Ningxia Anteli Carbon Material Co Ltd عن زيادة في سعر كربيد السيليكون في الصين. يمكن أن تؤدي زيادات الأسعار في المنتجات البترولية والمواد الخام الأخرى إلى تقييد هوامش الربح على المنتجات، مما يشكل تحديًا لنمو سوق المواد الكاشطة.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق المواد الكاشطة:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تقسيم التقرير ونطاقه:

"تحليل وتوقعات سوق المواد الكاشطة العالمية حتى عام 2030" هي دراسة متخصصة ومتعمقة مع التركيز بشكل كبير على اتجاهات السوق العالمية وفرص النمو. يهدف التقرير إلى تقديم نظرة عامة على السوق مع تقسيم السوق التفصيلي حسب المادة والنوع والتطبيق وقناة المبيعات. شهد السوق نموًا كبيرًا في الماضي القريب ومن المتوقع أن يستمر هذا الاتجاه خلال فترة التنبؤ. يقدم التقرير إحصائيات رئيسية حول استهلاك المواد الكاشطة على مستوى العالم. بالإضافة إلى ذلك، يوفر تقرير سوق المواد الكاشطة العالمية تقييمًا نوعيًا للعوامل المختلفة التي تؤثر على أداء السوق على مستوى العالم. يتضمن التقرير أيضًا تحليلًا شاملاً للاعبين الرائدين في السوق وتطوراتهم الاستراتيجية الرئيسية. تم إجراء العديد من التحليلات لتحديد العوامل الدافعة الرئيسية واتجاهات سوق المواد الكاشطة والفرص المربحة التي من شأنها بدورها أن تساعد في تحديد جيوب الإيرادات الرئيسية.

يتم تقدير توقعات سوق المواد الكاشطة على أساس نتائج بحثية ثانوية وأولية مختلفة، مثل منشورات الشركات الرئيسية وبيانات الجمعيات وقواعد البيانات. علاوة على ذلك، يوفر تحليل النظام البيئي وتحليل القوى الخمس لبورتر رؤية شاملة للسوق، مما يساعد على فهم سلسلة التوريد بأكملها والعوامل المختلفة التي تؤثر على أداء السوق.

التحليل القطاعي:

يتم تقسيم سوق المواد الكاشطة العالمية على أساس المادة والنوع والتطبيق وقناة المبيعات. بناءً على النوع، يتم تقسيم السوق إلى مواد كاشطة ملتصقة (أقراص وعجلات وغيرها) ومواد كاشطة مطلية (أقراص رفرف وأقراص ألياف وأقراص خطاف وحلقة وأحزمة ولفائف وغيرها). شكلت شريحة المواد الكاشطة الملتصقة حصة كبيرة في سوق المواد الكاشطة في عام 2022. يتم تصنيع المواد الكاشطة الملتصقة عن طريق الجمع بين الحبوب مع عوامل الترابط وتشكيل الخليط ثم إطلاق أو خبز المنتج الناتج. يتم ربط المواد الكاشطة الملتصقة بمادة رابطة؛ المواد الرابطة المستخدمة بشكل شائع في المواد الكاشطة هي من المطاط أو الزجاج أو الراتينج أو الطين. تُستخدم المواد الكاشطة الملتصقة مع مثقاب أو أداة دوارة. يتم نحت المواد الكاشطة الملتصقة في عجلات طحن وعجلات قطع وشرائح ومخاريط وأشكال أخرى. تُستخدم هذه الأنواع من المواد الكاشطة في تطبيقات متنوعة، مثل تلميع الأرضيات، والتصنيع، والتلميع، وطحن الأدوات اليدوية، وطحن المنتجات بدقة، مثل أعمدة الكرنك والكرات وشفرات الحلاقة. تُستخدم هذه المواد الكاشطة الملتصقة في صناعات متنوعة، بما في ذلك صناعة السيارات والبناء والتصنيع والنجارة.

بناءً على التطبيق، يتم تقسيم السوق إلى السيارات والفضاء والبحرية وتصنيع المعادن والنجارة والكهرباء والإلكترونيات وغيرها. احتل قطاع السيارات حصة كبيرة في سوق المواد الكاشطة في عام 2022. تُستخدم المواد الكاشطة على نطاق واسع في كل جانب من جوانب صناعة السيارات من قبل الشركات المصنعة وورش الإصلاح/الميكانيكا وموردي قطع غيار السيارات. في صناعة السيارات، تُستخدم المواد الكاشطة للسيارات بشكل أساسي لتنظيف وطحن وتلميع الأسطح أو الأجزاء المعدنية. يُعد ورق الصنفرة وعجلات الطحن ومركبات التلميع وأقراص الصنفرة من بين المواد الكاشطة المستخدمة في صناعة السيارات لإزالة الطلاء والصدأ وتلميع الأسطح. في تصنيع العجلات، تُستخدم المواد الكاشطة لطحن الأسطح والتشطيب والصب والتشكيل والتلميع.

التحليل الإقليمي:

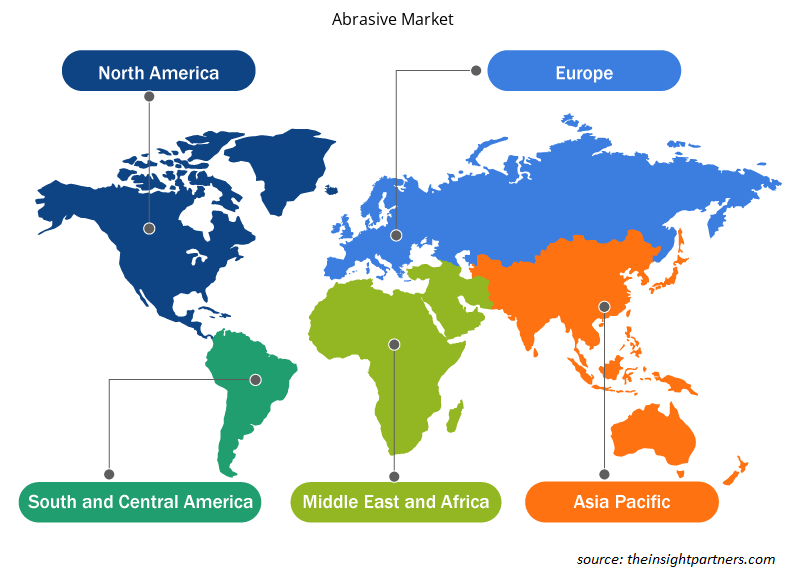

يقدم التقرير نظرة عامة مفصلة على السوق فيما يتعلق بخمس مناطق رئيسية - أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ (APAC) والشرق الأوسط وأفريقيا (MEA) وأمريكا الجنوبية والوسطى. من حيث الإيرادات، سيطرت منطقة آسيا والمحيط الهادئ على سوق المواد الكاشطة وقُدرت قيمتها بأكثر من 20 مليار دولار أمريكي في عام 2022. مع مشاريع تطوير البنية التحتية والتحضر الجارية، هناك حاجة متزايدة للمواد الكاشطة في تطبيقات البناء في المنطقة. من تشكيل وتنعيم الأسطح الخرسانية إلى قطع وتشطيب الهياكل المعدنية، تلعب المواد الكاشطة دورًا حيويًا في تحسين جودة ودقة مشاريع البناء. بالإضافة إلى ذلك، مع توسع قطاعي التجارة والنقل البحري، هناك حاجة متزايدة لبناء السفن وصيانتها، مما يحفز الطلب على المواد الكاشطة في تطبيقات مختلفة. تعد الصين واليابان وكوريا الجنوبية من الدول الرائدة في قطاع بناء السفن. تتطلب الطبيعة المعقدة وواسعة النطاق لبناء السفن مواد كاشطة يمكنها التعامل مع مواد متنوعة تستخدم في بناء السفن، بما في ذلك الفولاذ والسبائك المختلفة. ومن المتوقع أن تعمل كل هذه العوامل على تعزيز سوق المواد الكاشطة خلال فترة التنبؤ.

من المتوقع أن يصل سوق المواد الكاشطة في أوروبا إلى حوالي 7 مليارات دولار أمريكي بحلول عام 2030. تعد صناعة السيارات من بين أهم الصناعات وأسرعها نموًا في أوروبا. تساهم صناعة السيارات بشكل ملحوظ في الناتج المحلي الإجمالي للعديد من الدول الأوروبية، بما في ذلك ألمانيا والمملكة المتحدة وإيطاليا. وفقًا للمفوضية الأوروبية، تعد أوروبا أكبر مصنع للسيارات في جميع أنحاء العالم. في عام 2022، حافظت صناعة الطيران والدفاع الأوروبية على انتعاشها الاقتصادي بعد الوباء. في صناعة الطيران، تعتبر المواد الكاشطة ضرورية لتشكيل وتشطيب وتكرير مواد مختلفة مثل المعادن والمركبات. من قطع عوارض الفولاذ إلى تشكيل التفاصيل المعقدة في العناصر المعمارية، تعد الأدوات الكاشطة لا غنى عنها لتحقيق الدقة وتلبية مواصفات التصميم في مشاريع البناء.

رؤى إقليمية حول سوق المواد الكاشطة

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق المواد الكاشطة طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق المواد الكاشطة والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق المواد الكاشطة

نطاق تقرير سوق المواد الكاشطة

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 34.81 مليار دولار أمريكي |

| حجم السوق بحلول عام 2030 | 50.99 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2030) | 4.9% |

| البيانات التاريخية | 2020-2021 |

| فترة التنبؤ | 2023-2030 |

| القطاعات المغطاة | حسب المادة

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

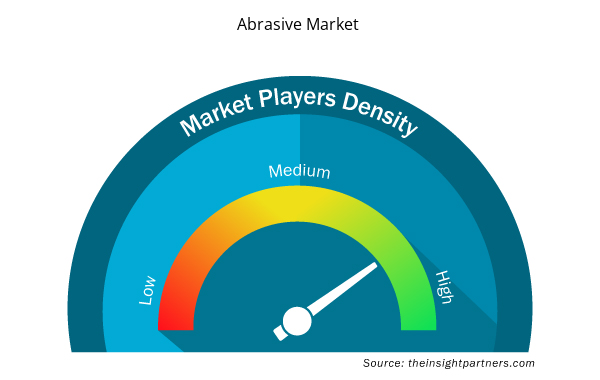

كثافة اللاعبين في السوق الكاشطة: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق المواد الكاشطة نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق المواد الكاشطة هي:

- شركة ديرفوس المحدودة

- شركة CUMI AWUKO Abrasives GmbH

- شركة روبرت بوش المحدودة

- Tyrolit Schleifmittelwerke Swarovski AG & Co KG

- شركة صن ابراسيفز المحدودة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق المواد الكاشطة

تطورات الصناعة والفرص المستقبلية:

فيما يلي بعض المبادرات التي اتخذها اللاعبون الرئيسيون العاملون في سوق المواد الكاشطة:

- في يناير 2024، استحوذت شركة Tyrolit على حصة الأغلبية في شركة Abrasive Tools Specialists، وهي شركة استيراد وبيع بالجملة وتحويل الأدوات الكاشطة، وذلك بهدف تعزيز حضورها في السوق الأسترالية وتنويع عروض منتجاتها وتلبية احتياجات العملاء المتنوعة.

- في ديسمبر 2023، أعلنت شركة ميركا عن خطة لبناء مصنع مبتكر لتصنيع الحبوب الدائرية في جيبو، فنلندا. ومن المتوقع أن يؤدي الاستثمار إلى تقليل بصمة ميركا من ثاني أكسيد الكربون بنحو 5000 طن متري. وعلاوة على ذلك، سيتم إطلاق أول منتجات الكاشطة الدائرية في عام 2026.

المنافسة والشركات الرئيسية:

تعد شركة 3M Co، وSaint-Gobain، وSia Abrasives Industries AG، وDeerfos، وTyrolit، وINDASA، وMirka Ltd، وCumi Awuko Abrasives Gmbh، وBosch Limited، وHermes Schleifmittel Gmbh، وVSM AG، وSAIT Abrasivi SpA من بين اللاعبين الرئيسيين الذين تم عرضهم في تقرير سوق المواد الكاشطة. يركز اللاعبون في السوق العالمية على توفير منتجات عالية الجودة لتلبية طلب العملاء.

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

Based on application, metal fabrication is the fastest-growing segment. Fabricated metals are an integral part of many end-use industries such as automotive, aerospace, electrical & electronics, and marine. The growth in end-use industries is driving the demand for abrasives.

Asia Pacific abrasive market is expected to surge due to government investments in end-use industries such as aerospace and automotive. Asia Pacific is the manufacturing hub for many companies operating in the automotive, aerospace, consumer goods, metal fabrication and woodworking industries. Further, industrialization and developments in several economies such as China, India, Taiwan, South Korea and Japan is fueling the demand for abrasives.

The major players operating in the global abrasive market are Compagnie de Saint Gobain SA, 3M Co, Sia Abrasives Industries AG, Robert Bosch GmbH, and Sun Abrasives Co Ltd, amongst others.

Based on the material, the synthetic segment accounted for the largest revenue share. One of the primary reasons for preference for synthetic abrasives over natural abrasives is their cost-effectiveness. Synthetic abrasives such as silicon carbide and aluminum oxide are significantly cheaper than diamonds used as abrasives. Therefore, growing demand for synthetic abrasives across the globe drives the abrasive market.

Growing automotive and metal fabrication industry, and rising demand for abrasives from electrical and electronics industry, are some of the key driving factors for the abrasive market.

The adoption of abrasives in automation and robotic applications offer lucrative growth opportunities to the global abrasive market during the forecast period.

The List of Companies - Abrasive Market

- Deerfos Co Ltd

- CUMI AWUKO Abrasives GmbH

- Robert Bosch GmbH

- Tyrolit Schleifmittelwerke Swarovski AG & Co KG

- Sun Abrasives Co Ltd

- Compagnie de Saint Gobain SA

- sia Abrasives Industries AG

- RHODIUS Abrasives GmbH

- 3M Co

- Ekamant AB

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير