اتجاهات سوق ألياف الكربون وفرص النمو الاستراتيجي المتوقعة حتى عام 2031

البيانات التاريخية : 2021-2022 | سنة الأساس : 2023 | فترة التنبؤ : 2023-2031حجم سوق ألياف الكربون وتوقعاته (2021-2031)، والحصة العالمية والإقليمية، والاتجاهات، وفرص النمو. يغطي التقرير: المواد الخام (القائمة على البولي أكريلونيتريل والقائمة على الملعب)، والتطبيق (المواد المركبة، والأقطاب الكهربائية الدقيقة، وغيرها)، والصناعات النهائية (السيارات، والفضاء والدفاع، والبناء والتشييد، والسلع الرياضية، وطاقة الرياح، والمنسوجات، والصناعات البحرية، وغيرها)، والموقع الجغرافي.

- تاريخ التقرير : Feb 2026

- رمز التقرير : TIPRE00002830

- الفئة : المواد الكيميائية والمواد

- الحالة : البيانات الصادرة

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 150

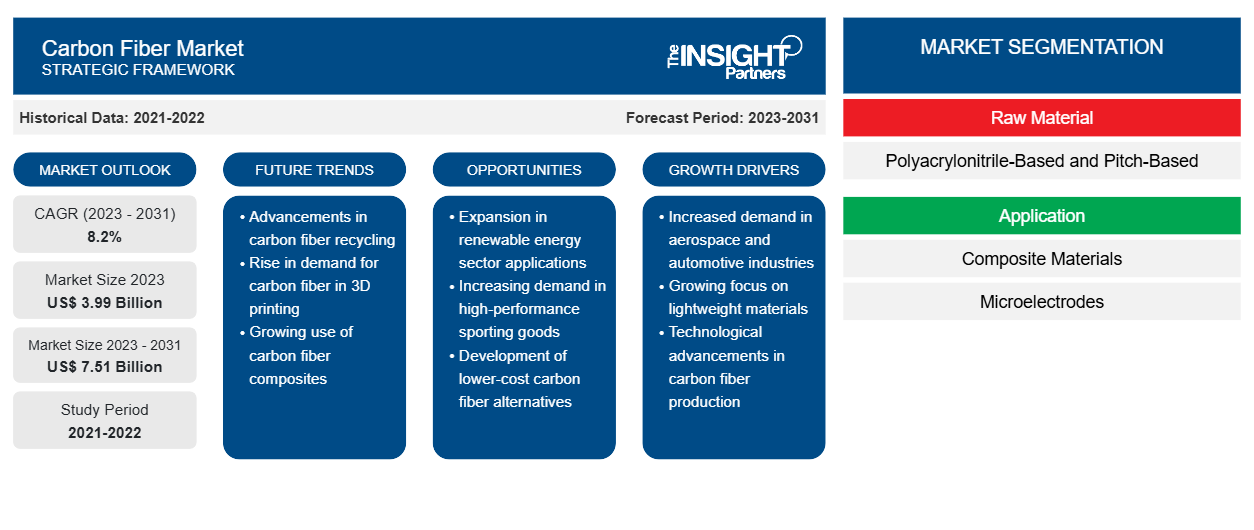

من المتوقع أن يصل حجم سوق ألياف الكربون إلى 7.51 مليار دولار أمريكي بحلول عام 2031 من 3.99 مليار دولار أمريكي في عام 2023. ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب بنسبة 8.2٪ خلال الفترة 2023-2031. ومن المرجح أن يؤدي الطلب المتزايد من قطاعات الطيران والسيارات والمعدات الرياضية والصناعة إلى ظهور اتجاهات جديدة لسوق ألياف الكربون في المستقبل.

تحليل سوق ألياف الكربون

تتمتع ألياف الكربون بقوة ميكانيكية وصلابة ومقاومة للحرارة والمواد الكيميائية بشكل ملحوظ. وهي أخف وزناً بشكل ملحوظ من الفولاذ أو الألومنيوم ولكنها تتمتع بقوة نسبية أو أعلى. وهذا يجعل ألياف الكربون مادة مطلوبة في التطبيقات حيث يكون تقليل الوزن أمرًا بالغ الأهمية مثل الطيران والسيارات والمعدات الرياضية والقطاعات الصناعية. ومن المتوقع أن يستمر سوق ألياف الكربون في النمو مع اعتماد الصناعات في مختلف القطاعات بشكل متزايد على مركبات ألياف الكربون لتلبية احتياجاتها من المواد خفيفة الوزن والمتينة والموفرة للطاقة. ومن المرجح أيضًا أن تساهم التطورات التكنولوجية في عمليات تصنيع ألياف الكربون وتطوير تقنيات الإنتاج الفعالة من حيث التكلفة في توسيع السوق في السنوات القادمة.

نظرة عامة على سوق ألياف الكربون

يسعى مصنعو السيارات إلى الحصول على مواد مبتكرة وعالية الجودة لإنتاج مكونات السيارات خفيفة الوزن ذات القوة الميكانيكية العالية والقوة الشد. تعتبر ألياف الكربون واحدة من أكثر المواد ملاءمة لإنتاج أجزاء السيارات خفيفة الوزن. علاوة على ذلك، تُستخدم المركبات المقواة بألياف الكربون كمادة أساسية لتحل محل أجزاء الفولاذ والألمنيوم الأثقل وزنًا والتي تؤدي إلى انخفاض كفاءة الوقود. أدى استخدام ألياف الكربون في صناعة السيارات إلى تحسين كفاءة الوقود، مما أدى إلى الحفاظ على الطاقة وتقليل انبعاثات ثاني أكسيد الكربون. تستخدم شركات تصنيع السيارات الرائدة ألياف الكربون لتصنيع المكونات. على سبيل المثال، تتكون وحدة إيرباص A350 من 52٪ بوليمر مقوى بألياف الكربون (CFRP)، في حين أن وحدة BMW i3 بها هيكل من البوليمر المقوى بألياف الكربون في الغالب.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق ألياف الكربون: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محركات وفرص سوق ألياف الكربون

اعتماد شفرات توربينات خفيفة الوزن في صناعة طاقة الرياح يعزز نمو سوق ألياف الكربون

لقد شهدنا زيادة ملحوظة في تركيب مزارع الرياح مع تفضيل متزايد لاستخدام الموارد المتجددة. يتم تخصيص مساحات كبيرة من الأراضي والمناطق الساحلية في بلدان مختلفة لعمليات توربينات الرياح. تلعب ألياف الكربون دورًا مهمًا في صناعة طاقة الرياح . ينتج مصنعو توربينات الرياح في الوقت الحاضر شفرات أطول وأخف وزنًا وأكثر كفاءة باستخدام مواد مركبة متقدمة مثل ألياف الكربون. يتيح تمديد طول شفرات التوربينات توليد طاقة أكبر. عادة ما يتم تصميم الشفرات الكبيرة مع التركيز بشكل أساسي على الصلابة وانحراف الطرف. ومع ذلك، تساهم صلابة ألياف الكربون العالية في تقليل انحراف الشفرات. وبالتالي، تسمح شفرات التوربينات الكبيرة المصنوعة من ألياف الكربون المركبة بقطر برج أكبر لخلوص معين بين الشفرة والبرج. تُستخدم ألياف الكربون أيضًا في غطاء السارية، وهو العمود الفقري للشفرة.

أثبتت ألياف الكربون أنها بديل فعال للألياف الزجاجية في تصميمات توربينات الرياح نظرًا لصلابتها العالية وكثافتها المنخفضة مقارنة بألياف الزجاج، مما يسمح بشفرات أرق وأكثر صلابة وأخف وزنًا. ومع ذلك، فإن الشفرات المصنوعة من ألياف الكربون تظهر قدرة منخفضة نسبيًا على تحمل التلف وقوة الضغط والإجهاد النهائي. لذلك، تُستخدم ألياف الكربون بشكل شائع في تصنيع شفرات توربينات الرياح. تستخدم شركات مثل Vestas Wind Systems A/S وGamesa Technology Corp ألياف الكربون في أجزاء هيكلية انتقائية من الشفرات وتستفيد من الشفرات الأخف وزنًا في جميع أنحاء نظام التوربين. تتطلب الشفرات الخفيفة مكونات توربينية وبرجية أقل قوة، مما يؤدي في النهاية إلى تقليل التكاليف الإجمالية. وبالتالي، فإن الزيادة في استخدام شفرات التوربينتوربينتوربينات خفيفة الوزن في صناعة طاقة الرياح تعزز الطلب على ألياف الكربون، وبالتالي تعزز نمو السوق.

ارتفاع الطلب على ألياف الكربون في الطباعة ثلاثية الأبعاد من شأنه أن يوفر فرصًا للنمو

في السنوات الأخيرة، اكتسبت الطابعات ثلاثية الأبعاد اهتمامًا باعتبارها تقنية إنتاج صغيرة الحجم ومتعددة المنتجات. تعد طباعة ألياف الكربون ثلاثية الأبعاد أكثر تقنيات التصنيع الإضافي شيوعًا. تتم إضافة البلاستيك المقوى بألياف الكربون إلى خيوط الطباعة ثلاثية الأبعاد لتحسين مرونة وقوة الأجزاء المطبوعة. تتمتع هذه المواد المركبة بقوة أعلى بكثير من المعادن، بغض النظر عن وزنها الأقل من المعادن. بالإضافة إلى ذلك، يمكن خلط ألياف الكربون مع راتنجات بلاستيكية لتعزيز الخصائص الميكانيكية للأجزاء المطبوعة ثلاثية الأبعاد. تعد الطباعة ثلاثية الأبعاد باستخدام المركبات المقواة بألياف الكربون من بين أكثر تقنيات التصنيع الإضافي رواجًا. تكتسب تقنية التصنيع الإضافي قوة جذب هائلة بسبب مزاياها مثل خفض التكاليف المحتمل وتعقيد الأجزاء الأعلى والتكامل الوظيفي. تُستخدم ألياف الكربون لتطوير مواد الطباعة ثلاثية الأبعاد لسيارات السباق ومواد البناء والمعدات الرياضية والطائرات بدون طيار والمنتجات المستخدمة يوميًا وما إلى ذلك. تركز بعض الشركات الكبرى على إطلاق مركبات مطبوعة ثلاثية الأبعاد تعتمد على ألياف الكربون.

تقرير تحليل تجزئة سوق ألياف الكربون

تعتبر القطاعات الرئيسية التي تم أخذها في الاعتبار لتقديم تحليل سوق ألياف الكربون هي المنتج والاستخدام النهائي.

- بناءً على المواد الخام، يتم تقسيم سوق ألياف الكربون إلى ألياف تعتمد على البولي أكريلونيتريل وألياف تعتمد على القار. احتلت شريحة ألياف الكربون المعتمدة على البولي أكريلونيتريل حصة سوقية أكبر في عام 2023.

- من حيث التطبيق، يتم تقسيم سوق ألياف الكربون إلى مواد مركبة وأقطاب كهربائية دقيقة وغيرها. احتل قطاع المواد المركبة الحصة الأكبر في السوق في عام 2023.

- بحسب صناعة الاستخدام النهائي، يتم تصنيف سوق ألياف الكربون إلى السيارات، والفضاء والدفاع، والبناء والتشييد ، والسلع الرياضية، وطاقة الرياح، والمنسوجات، والبحرية، وغيرها. احتل قطاع السيارات الحصة الأكبر من السوق في عام 2023.

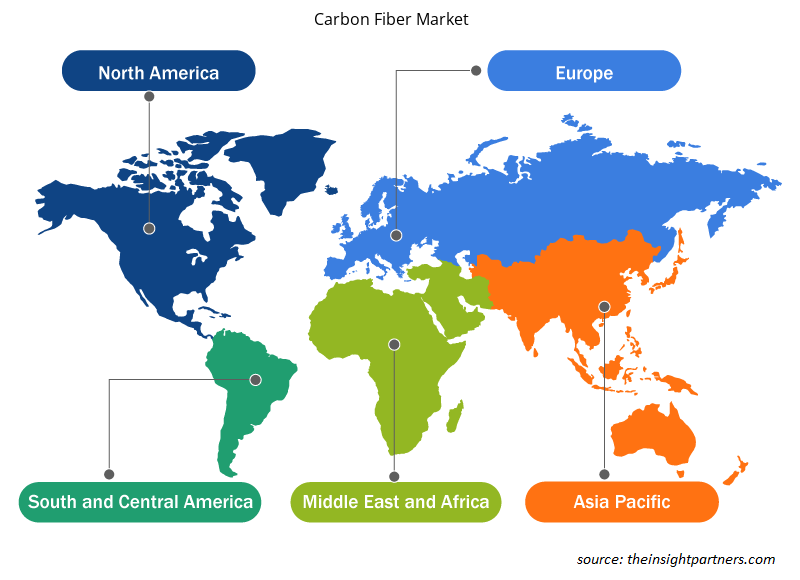

تحليل حصة سوق ألياف الكربون حسب المنطقة الجغرافية

ينقسم النطاق الجغرافي لتقرير سوق ألياف الكربون بشكل أساسي إلى خمس مناطق: أمريكا الشمالية، ومنطقة آسيا والمحيط الهادئ، وأوروبا، والشرق الأوسط وأفريقيا، وأمريكا الجنوبية والوسطى.

لقد هيمنت منطقة آسيا والمحيط الهادئ على سوق ألياف الكربون. إن الدخل المتاح المرتفع للأشخاص في منطقة آسيا والمحيط الهادئ يزيد من مبيعات المركبات التجارية ومركبات الركاب، مما يعزز الحاجة إلى المركبات. بالإضافة إلى ذلك، فإن زيادة الاستثمارات من قبل شركات تصنيع السيارات الرائدة وقدرات تصنيع المركبات الكهربائية المتزايدة في منطقة آسيا والمحيط الهادئ تدفع الطلب على المركبات التقليدية والكهربائية في المنطقة. ويعزى نمو صناعة تصنيع مكونات المركبات في منطقة آسيا والمحيط الهادئ إلى صناعة السيارات المتنامية في المنطقة. تُستخدم ألياف الكربون على نطاق واسع في تصنيع المركبات المركبة. وبالتالي، مع نمو صناعة السيارات، يتزايد الطلب على ألياف الكربون أيضًا في جميع أنحاء المنطقة.

رؤى إقليمية حول سوق ألياف الكربون

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق ألياف الكربون طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق ألياف الكربون والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق ألياف الكربون

نطاق تقرير سوق ألياف الكربون

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2023 | 3.99 مليار دولار أمريكي |

| حجم السوق بحلول عام 2031 | 7.51 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2023 - 2031) | 8.2% |

| البيانات التاريخية | 2021-2022 |

| فترة التنبؤ | 2023-2031 |

| القطاعات المغطاة |

حسب المواد الخام

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق ألياف الكربون: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق ألياف الكربون نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلك المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق ألياف الكربون هي:

- إس جي إل كربون إس إي

- شركة دواكسا للصناعات المتقدمة للمواد المركبة المحدودة

- شركة فورموزا للبلاستيك

- شركة هيكسل

- شركة هايوسونج للمواد المتقدمة

- شركة كوريها

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق ألياف الكربون

أخبار سوق ألياف الكربون والتطورات الأخيرة

يتم تقييم سوق ألياف الكربون من خلال جمع البيانات النوعية والكمية بعد البحث الأولي والثانوي، والتي تتضمن منشورات الشركات المهمة وبيانات الجمعيات وقواعد البيانات. فيما يلي قائمة بالتطورات في سوق ألياف الكربون:

- أعلنت شركة Toray Industries, Inc. اليوم أنها طورت ألياف الكربون TORAYCA T1200، وهي أعلى قوة في العالم عند 1160 كيلو رطل لكل بوصة مربعة (Ksi). سيدفعنا هذا العرض الجديد إلى الأمام لتقليل البصمة البيئية من خلال تخفيف المواد البلاستيكية المقواة بألياف الكربون. تفتح هذه الألياف أيضًا حدود أداء جديدة للتطبيقات التي تعتمد على القوة. تتراوح تطبيقاتها المحتملة من الهياكل الجوية والدفاع إلى الطاقة البديلة والمنتجات الاستهلاكية. (المصدر: Toray Advanced Composites، بيان صحفي، 2023)

- ستقدم شركة SGL Carbon ألياف كربون جديدة بوزن 50 كيلوجرامًا في معرض JEC World 2023. ستتوافق ألياف الكربون الجديدة SIGRAFIL C T50-4.9/235 مع متطلبات القوة العالية لتصميمات الأوعية المضغوطة الشائعة وتتميز بقدرة استطالة عالية. كما أنها تمكن من تطبيقات أخرى في قطاعات السوق التي تتطلب قوة واستطالة عالية. (المصدر: SGL Carbon، بيان صحفي، 2023)

تغطية تقرير سوق ألياف الكربون والمنتجات النهائية

يوفر تقرير "حجم سوق ألياف الكربون والتوقعات (2021-2031)" تحليلاً مفصلاً للسوق يغطي المجالات التالية:

- حجم السوق والتوقعات على المستويات العالمية والإقليمية والوطنية لجميع قطاعات السوق الرئيسية التي يغطيها النطاق

- ديناميكيات السوق مثل المحركات والقيود والفرص الرئيسية

- الاتجاهات المستقبلية الرئيسية

- تحليل مفصل لقوى بورتر الخمس ونقاط القوة والضعف والفرص والتهديدات

- تحليل السوق العالمي والإقليمي الذي يغطي اتجاهات السوق الرئيسية واللاعبين الرئيسيين واللوائح والتطورات الأخيرة في السوق

- تحليل المشهد الصناعي والمنافسة الذي يغطي تركيز السوق، وتحليل خريطة الحرارة، واللاعبين البارزين، والتطورات الأخيرة

- ملفات تعريف الشركة التفصيلية

حابي محلل أبحاث سوق متمرس، يتمتع بخبرة 8 سنوات في قطاع الكيماويات والمواد، بالإضافة إلى خبرته في قطاعي الأغذية والمشروبات والسلع الاستهلاكية. وهو مهندس كيميائي من معهد فيشواكارما للتكنولوجيا (VIT)، وقد اكتسب معرفةً عميقةً في مجالات الكيماويات الصناعية والتخصصية، والدهانات والطلاءات، والورق والتغليف، ومواد التشحيم، والمنتجات الاستهلاكية.

تشمل كفاءات حابي الأساسية تقدير حجم السوق والتنبؤ به، ووضع معايير تنافسية، وتحليل الاتجاهات، والتفاعل مع العملاء، وكتابة التقارير، وتنسيق الفريق، مما يجعله بارعًا في تقديم رؤى عملية ودعم اتخاذ القرارات الاستراتيجية.

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

تقارير ذات صلة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق ألياف الكربون

احصل على عينة مجانية ل - سوق ألياف الكربون