تقرير سوق خدمات تصنيع العلاج بالخلايا والجينات 2030 حسب القطاعات والجغرافيا والديناميكيات والتطورات الأخيرة والرؤى الاستراتيجية

البيانات التاريخية : 2020-2021 | سنة الأساس : 2022 | فترة التنبؤ : 2022-2030حجم سوق خدمات تصنيع العلاج الخلوي والجيني وتوقعاته (2020-2030)، والحصة العالمية والإقليمية، والاتجاهات، وفرص النمو. يغطي التقرير: حسب النوع [العلاج الخلوي (ذاتي، متماثل) والعلاج الجيني (فيروسي، ناقل غير فيروسي)]، والمؤشر (السرطان، جراحة العظام، وغيرها)، والتطبيق (التصنيع السريري، التصنيع التجاري)، والمستخدم النهائي [شركات الأدوية، والتكنولوجيا الحيوية، ومنظمات أبحاث العقود (CROs)، والموقع الجغرافي].

- تاريخ التقرير : Sep 2023

- رمز التقرير : TIPRE00024304

- الفئة : علوم الحياة

- الحالة : نُشرت

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 216

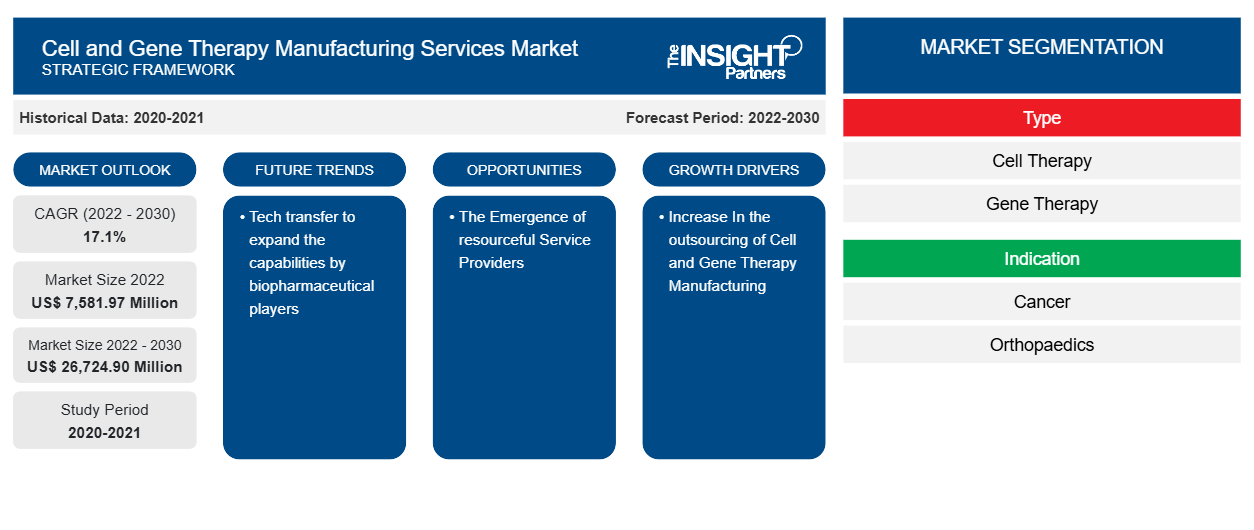

من المتوقع أن يصل حجم سوق خدمات تصنيع العلاج بالخلايا والجينات إلى 26,724.90 مليون دولار أمريكي بحلول عام 2030 من 7,581.97 مليون دولار أمريكي في عام 2022. ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب بنسبة 17.1٪ خلال الفترة 2022-2030. ومن المرجح أن يظل أتمتة خدمات التصنيع للعلاج بالخلايا والجينات اتجاهًا رئيسيًا في السوق.

تحليل سوق خدمات تصنيع العلاج بالخلايا والجينات

في السنوات الأخيرة، شهد قطاع تصنيع الخلايا والجينات المستعان بها من الخارج توسعًا وتغييرًا كبيرًا. ومع تقدم علاجات الخلايا والجينات، تعتمد شركات ابتكار الأدوية بشكل متزايد على مقدمي الخدمات لتلبية متطلبات التصنيع الخاصة بها. يتيح الاستعانة بمصادر خارجية للمبتكرين الاستفادة من الخبرة المتخصصة وقدرات منظمات تطوير وتصنيع العقود (CDMOs) لتقليل التكاليف وتسريع الوقت اللازم لطرح المنتجات في السوق. لقد تطور مشهد تصنيع علاجات الخلايا والجينات على مدار السنوات الخمس الماضية، مع التحول نحو منصات أكثر تطورًا تسمح بالتوسع وزيادة الأتمتة وأنظمة الجودة المحسنة، مما يشكل صناعة تصنيع العقود. مع العدد المتزايد من منتجات علاجات الخلايا والجينات المعتمدة في السوق كل عام، أصبحت الحاجة إلى تحسين العمليات أكثر أهمية على نحو متزايد.

نظرة عامة على سوق خدمات تصنيع العلاج بالخلايا والجينات

لقد زادت عمليات تصنيع الأدوية الحيوية بتمويل عام وخاص نتيجة للزيادة الكبيرة في المنتجات الصيدلانية الحيوية الجديدة التي تتنافس على الموافقة. ونتيجة لهذا، في حين تحاول الجهات الفاعلة الراسخة في الصناعة التمسك بمواقعها والريادة، تشارك منظمات جديدة في تقديم خدمات التصنيع للعلاجات الخلوية والجينية . وتعطي سياسات الرعاية الصحية في العديد من المناطق الآن الأولوية للقدرة على تصنيع المنتجات الصيدلانية (الجزيئات الصغيرة) من جميع الأنواع. بالإضافة إلى ذلك، حدث تحول نحو التصنيع الحيوي للجزيئات الأكبر، والعلاجات المؤتلفة، والبيولوجيات المعقدة بشكل متزايد في العديد من المناطق.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق خدمات تصنيع العلاج بالخلايا والجينات: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محركات وفرص سوق خدمات تصنيع العلاج بالخلايا والجينات

زيادة الطلب على تصنيع العلاج بالخلايا والجينات يعزز نمو السوق

وقد نتج عن أنشطة البحث المتنامية في مجال العلاج بالخلايا تقدم علاجي كبير في خدمات تصنيع العلاج بالخلايا والجينات. وتسعى الصناعة جاهدة إلى توسيع نطاق تصنيعها وإمكانية الوصول الشامل إلى عدد أكبر من السكان مع التأكيد على مزايا المنتجات الطبية العلاجية المتقدمة. وتتطلب التعقيدات المتزايدة للطب الشخصي تطوير قدرات التصنيع لمواكبة الطلب وضمان وصول المرضى إلى هذه العلاجات المبتكرة. والآن أصبح التصنيع التعاقدي يتمتع بخيارات أكثر بسبب ارتفاع الإنتاج العالمي. وقد زاد التمويل للمنتجات الصيدلانية الحيوية المعتمدة حديثًا، فضلاً عن التصنيع التعاقدي للأدوية الحيوية، من المصادر العامة والخاصة. وتقدم المنظمات العالمية خدمات التصنيع للعلاج بالخلايا والجينات، ويسعى المشاركون الراسخون في الصناعة إلى دعم عملياتهم. وبالتالي، من المرجح أن يؤدي التركيز الناشئ على تطوير تصنيع العلاج بالخلايا إلى دفع نمو السوق.

المبادرات الاستراتيجية من قبل اللاعبين الرئيسيين

وبسبب ارتفاع الموافقات والاستثمارات، هناك حاجة متزايدة لتصنيع العلاجات في المراحل السريرية والتجارية وما قبل السريرية. ويقوم اللاعبون الرئيسيون باستثمارات تطوير استراتيجية، مما يفتح الكثير من الفرص السوقية. وكمثال على الحاجة المتزايدة لخدمات تصنيع العلاج الخلوي والجينات، وقعت شركة بريستول مايرز سكويب والشركة الناشئة سيلاريس صفقة بقيمة 380 مليون دولار في مايو 2024. وفي أغسطس 2023، أكملت سيلاريس جولة تمويل من السلسلة C بقيمة 255 مليون دولار، وكانت بي إم إس من بين المستثمرين. وستقوم سيلاريس بتصنيع علاجات الخلايا التائية لمستقبلات المستضدات الكيمرية (CAR) لشركة بي إم إس. وستحجز بي إم إس مساحات في آلات تصنيع العلاج الخلوي الآلية لشركة سيلاريس، أو آلات Cell Shuttle، وفقًا لشروط الاتفاقية. وباستخدام الأموال من بيع بي إم إس، تعتزم سيلاريس فتح المزيد من المواقع في الولايات المتحدة وأوروبا واليابان بالإضافة إلى إدارة المواقع في سان فرانسيسكو ونيوجيرسي.

تقرير تحليلي لتجزئة سوق خدمات تصنيع العلاج بالخلايا والجينات

إن القطاعات الرئيسية التي ساهمت في اشتقاق تحليل سوق خدمات تصنيع العلاج بالخلايا والجينات هي النوع والمؤشر والتطبيق والمستخدم النهائي.

- بناءً على النوع، ينقسم سوق خدمات تصنيع العلاج الخلوي والعلاج الجيني إلى العلاج الخلوي والعلاج الجيني. وينقسم العلاج الخلوي إلى علاج ذاتي وعلاج متماثل. وينقسم العلاج الجيني إلى نواقل فيروسية وغير فيروسية.

- بحسب المؤشرات، يتم تصنيف السوق إلى السرطان، وجراحة العظام، وغيرها. احتل قطاع السرطان الحصة الأكبر من السوق في عام 2022.

- من حيث التطبيق، يتم تصنيف السوق إلى التصنيع السريري والتصنيع التجاري. احتل قطاع التصنيع التجاري الحصة الأكبر من السوق في عام 2022.

- بحسب المستخدم النهائي، يتم تقسيم السوق إلى شركات الأدوية والتكنولوجيا الحيوية ومنظمات الأبحاث التعاقدية (CROs). احتلت شريحة شركات الأدوية والتكنولوجيا الحيوية الحصة الأكبر من السوق في عام 2022.

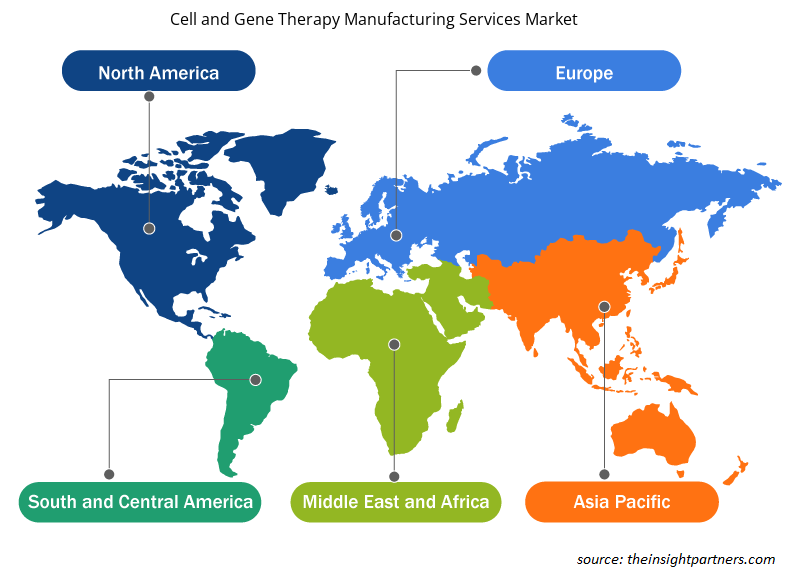

تحليل حصة سوق خدمات تصنيع العلاج بالخلايا والجينات حسب المنطقة الجغرافية

ينقسم النطاق الجغرافي لتقرير سوق خدمات تصنيع العلاج بالخلايا والجينات بشكل أساسي إلى خمس مناطق: أمريكا الشمالية، ومنطقة آسيا والمحيط الهادئ، وأوروبا، والشرق الأوسط وأفريقيا، وأمريكا الجنوبية والوسطى.

ومن المتوقع أن يتوسع سوق خدمات التصنيع المتعلقة بالعلاج بالخلايا والجينات نتيجة للطلب المتزايد على هذه المنتجات. ويرتبط هذا النمو بزيادة في عدد الشركات الناشئة، وزيادة في أنشطة البحث والتطوير، وزيادة الاستثمارات في بناء مرافق تصنيع العلاج بالخلايا والجينات في الولايات المتحدة وكندا.

بالإضافة إلى ذلك، خلال فترة التوقعات، نما سوق منطقة آسيا والمحيط الهادئ بشكل كبير بمعدل نمو سنوي مركب قوي. ويمكن أن يُعزى هذا النمو إلى عدد من العوامل، بما في ذلك الحاجة المتزايدة إلى حلول علاجية متقدمة، وسيناريوهات تنظيمية مواتية، والتركيز المتزايد على أنشطة البحث والتطوير. بالإضافة إلى ذلك، خلال فترة التوقعات، من المتوقع أن يكون سوق منطقة آسيا والمحيط الهادئ مدفوعًا بتوسع البنية التحتية للرعاية الصحية والاستثمارات المتزايدة التي تهدف إلى تحفيز أنشطة البحث.

رؤى إقليمية حول سوق خدمات تصنيع العلاج بالخلايا والجينات

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق خدمات تصنيع العلاج بالخلايا والجينات طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق خدمات تصنيع العلاج بالخلايا والجينات والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق خدمات تصنيع العلاج بالخلايا والجينات

نطاق تقرير سوق خدمات تصنيع العلاج بالخلايا والجينات

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 7,581.97 مليون دولار أمريكي |

| حجم السوق بحلول عام 2030 | 26,724.90 مليون دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2030) | 17.1% |

| البيانات التاريخية | 2020-2021 |

| فترة التنبؤ | 2022-2030 |

| القطاعات المغطاة |

حسب النوع

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق خدمات تصنيع العلاج بالخلايا والجينات: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق خدمات تصنيع العلاج بالخلايا والجينات نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلك المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق خدمات تصنيع العلاج الخلوي والجينات هي:

- شركة ثيرمو فيشر العلمية

- ميرك كي جي ايه ايه

- مختبرات تشارلز ريفر الدولية

- مجموعة لونزا ايه جي

- شركة ووشي أبتيك المحدودة

- شركة كاتالنت

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق خدمات تصنيع العلاج بالخلايا والجينات

أخبار السوق والتطورات الأخيرة في خدمات تصنيع العلاج بالخلايا والجينات

يتم تقييم سوق خدمات تصنيع العلاج بالخلايا والجينات من خلال جمع البيانات النوعية والكمية بعد البحث الأولي والثانوي، والتي تتضمن منشورات الشركات المهمة وبيانات الجمعيات وقواعد البيانات. فيما يلي بعض التطورات في سوق خدمات تصنيع العلاج بالخلايا والجينات:

- أعلنت شركتا RoslinCT وLykan Bioscience، وهما شركتان رائدتان في مجال تطوير وتصنيع العقود في صناعة العلاج الخلوي والجينات، عن اندماجهما، مما أدى إلى إنشاء شركة موحدة تعمل تحت العلامة التجارية RoslinCT. ويهدف هذا الاندماج، الذي تيسره شركة GHO Capital، وهي شركة استثمارية عالمية، إلى تأسيس لاعب مهيمن في سوق تطوير وتصنيع العقود في مجال العلاج الخلوي والجينات المتقدم. (المصدر: RoslinCT، بيان صحفي، يونيو 2023)

- اتفق مركز سينسيناتي للأطفال الطبي ومقدم خدمات البحث CTI Clinical Trial & Consulting Services على تشكيل شركة تركز على تقديم خدمات تصنيع الخلايا والعلاجات الجينية لصناعات التكنولوجيا الحيوية والأدوية. (المصدر: مركز سينسيناتي للأطفال الطبي، بيان صحفي، ديسمبر 2021)

تقرير سوق خدمات تصنيع العلاج بالخلايا والجينات والتغطية والنتائج المتوقعة

يوفر تقرير "حجم سوق خدمات تصنيع العلاج الخلوي والجينات وتوقعاته (2020-2030)" تحليلاً مفصلاً للسوق يغطي المجالات التالية:

- حجم سوق خدمات تصنيع العلاج بالخلايا والجينات وتوقعاته على المستويات العالمية والإقليمية والوطنية لجميع قطاعات السوق الرئيسية التي يغطيها النطاق

- اتجاهات سوق خدمات تصنيع العلاج بالخلايا والجينات بالإضافة إلى ديناميكيات السوق مثل المحركات والقيود والفرص الرئيسية

- تحليل مفصل لقوى PEST/Porter الخمس وSWOT

- تحليل سوق خدمات تصنيع العلاج بالخلايا والجينات يغطي اتجاهات السوق الرئيسية والإطار العالمي والإقليمي واللاعبين الرئيسيين واللوائح والتطورات الأخيرة في السوق.

- تحليل المشهد الصناعي والمنافسة الذي يغطي تركيز السوق، وتحليل خريطة الحرارة، واللاعبين البارزين، والتطورات الأخيرة لسوق خدمات تصنيع العلاج بالخلايا والجينات

- ملفات تعريف الشركة التفصيلية

مرينال محللة أبحاث مخضرمة، تتمتع بخبرة تزيد عن 8 سنوات في مجال استخبارات واستشارات سوق علوم الحياة. بفضل عقليتها الاستراتيجية والتزامها الراسخ بالتميز، اكتسبت خبرة واسعة في التنبؤ بالصناعات الدوائية، وتقييم فرص السوق، وتطوير معايير الصناعة. يرتكز عملها على تقديم رؤى عملية تُمكّن العملاء من اتخاذ قرارات استراتيجية مدروسة.

تكمن قوة مرينال الأساسية في ترجمة مجموعات البيانات الكمية المعقدة إلى معلومات استخباراتية قيّمة. وتُعدّ براعتها التحليلية ركيزةً أساسيةً في صياغة استراتيجيات دخول السوق (GTM) واكتشاف فرص النمو في قطاعي الأدوية والأجهزة الطبية. وبصفتها مستشارةً موثوقةً، تُركز مرينال باستمرار على تبسيط إجراءات سير العمل وترسيخ أفضل الممارسات، مما يُعزز الابتكار والكفاءة التشغيلية لعملائها.

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

تقارير ذات صلة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق خدمات تصنيع العلاج الخلوي والجيني

احصل على عينة مجانية ل - سوق خدمات تصنيع العلاج الخلوي والجيني