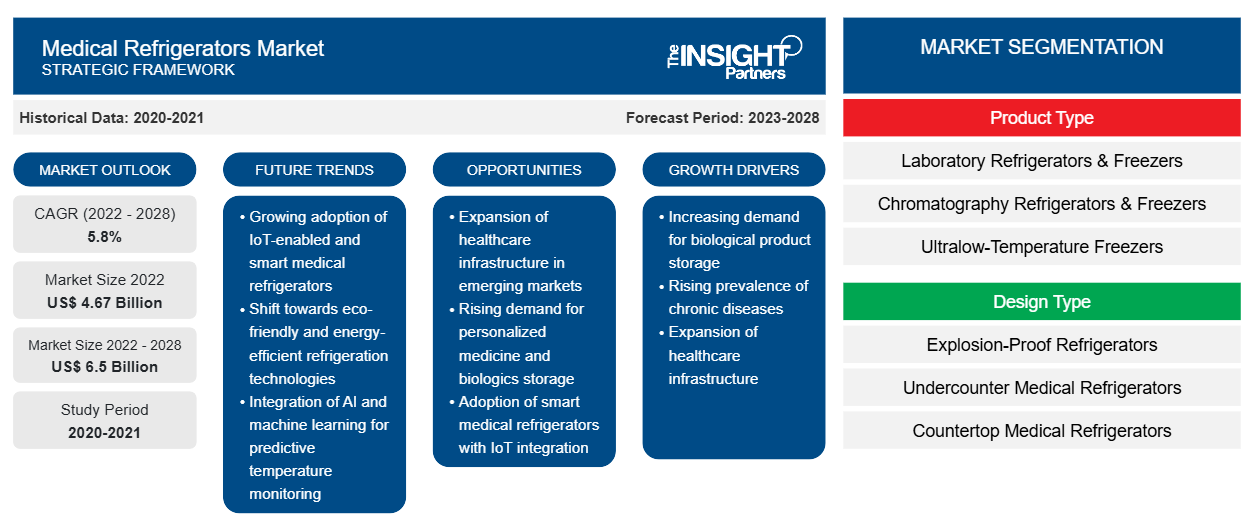

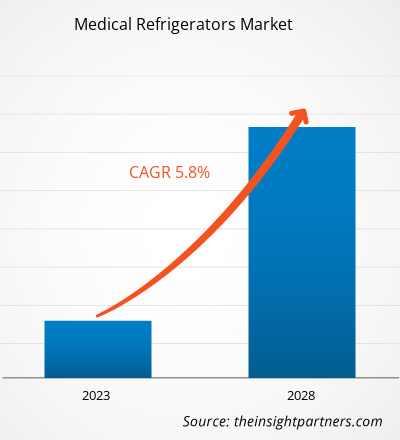

[تقرير بحثي] من المتوقع أن ينمو سوق الثلاجات الطبية من 4،665.97 مليون دولار أمريكي في عام 2022 إلى 6،499.18 مليون دولار أمريكي بحلول عام 2028؛ ومن المتوقع أن يسجل معدل نمو سنوي مركب بنسبة 5.8٪ من عام 2023 إلى عام 2028.

وجهة نظر المحلل:

تخزن الثلاجات الطبية مكونات بيولوجية مختلفة مثل الدم ومشتقات الدم والكواشف البيولوجية واللقاحات والأدوية والمواد الكيميائية القابلة للاشتعال. يؤدي العدد المتزايد من الإجراءات الطبية، إلى جانب الانتشار المتزايد لمشاكل مثل فقر الدم والسرطان، إلى توسع طرق نقل الدم. تقدر منظمة الصليب الأحمر الأمريكية أن ما يقرب من 13.6 مليون دم كامل وخلايا دم حمراء يتم جمعها سنويًا في الولايات المتحدة. سيؤدي الطلب المتزايد على عمليات نقل الدم إلى دفع نمو السوق. كما أدى الاستخدام المتزايد لهذه العوامل لعلاج نقص السكر في الدم الشديد إلى زيادة الطلب في السوق. تسعى البلدان النامية إلى إدخال تقنيات تبريد سلسلة التبريد الطبية الجديدة لضمان التخزين الآمن للأدوية. بالإضافة إلى ذلك، تُستخدم الثلاجات الطبية أيضًا في قسم المناعة الدموية لتخزين الدم الكامل ومكونات الدم والكواشف بأمان وراحة.

نظرة عامة على السوق

تُستخدم الثلاجات الطبية بشكل أساسي في الرعاية الصحية، حيث تُستخدم لتخزين العديد من المنتجات الحساسة للحرارة مثل اللقاحات والدم وما إلى ذلك. ومع تقدم التكنولوجيا، قطعت تكنولوجيا التبريد خطوات كبيرة في تلبية احتياجات الصناعات الطبية والرعاية الصحية. وقد أدت التطورات التكنولوجية إلى تحسين كفاءة الطاقة وتحسين الخصائص الصوتية وتنظيم درجة الحرارة بشكل أفضل. تحتوي هذه الأجهزة على تقنيات تبريد دقيقة وبرامج مراقبة درجة الحرارة الحديثة ووظائف التحذير عن بعد. يدمج العديد من الشركات المصنعة واجهات تعتمد على الويب وتقدم شاشات رسومية. كما أنها تنفذ إعدادات درجات الحرارة المنخفضة والمنخفضة للغاية وأنظمة جمع البيانات وإدارتها لزيادة الوظائف. إن الحاجة المتزايدة إلى الثلاجات الطبية بسبب زيادة حالات الأمراض المزمنة وتطورات السوق والتقدم التكنولوجي، من بين أمور أخرى، تدفع نمو سوق الثلاجات الطبية العالمية.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق الثلاجات الطبية:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محركات النمو والتحديات:

يؤدي الدم ومكوناته العديد من الوظائف الحيوية في الجسم. وبالتالي، فإن فقدان الدم الشديد يمكن أن يؤدي إلى حالات تهدد الحياة مثل صدمة نقص حجم الدم / النزف، والتي تتطلب نقل الدم الفوري لمنع فشل الأعضاء والوفاة. يعد نقل الدم أحد الخطوات المهمة في العديد من الإجراءات الجراحية، وكذلك في العلاج الكيميائي، وعلاج الخلايا الجذعية، وإجراءات زراعة الأعضاء؛ كما يتم استخدامه في علاج الأمراض الحادة والمزمنة الناجمة عن نقص أو عيوب في بروتينات البلازما أو مكونات الدم الخلوية، لتجنب المضاعفات مثل النزيف الذي يهدد الحياة أو لتحسين نوعية الحياة. على سبيل المثال، وفقًا للبيانات المقدمة من منظمة الصحة العالمية، يؤثر فقر الدم على حوالي 25٪ من السكان، أي حوالي 1.6 مليار شخص، في جميع أنحاء العالم؛ انتشار الحالة هو الأعلى، أي 47.4٪، بين الأطفال الصغار والأطفال في سن ما قبل المدرسة. تقدر مؤسسة الهيموفيليا الوطنية أن أكثر من 400000 شخص في جميع أنحاء العالم مصابون بالهيموفيليا. وفقًا لنتائج بيانات الصليب الأحمر الوطني الأمريكي لعام 2023، يتم جمع 13.6 مليون وحدة من خلايا الدم الكاملة والحمراء سنويًا في الولايات المتحدة. في الولايات المتحدة، هناك حاجة إلى حوالي 29000 وحدة من خلايا الدم الحمراء و6500 وحدة من البلازما وحوالي 5000 وحدة من الصفائح الدموية يوميًا. وبالتالي، شجع الطلب المتزايد على الدم الآمن ومكونات الدم لنقل الدم تصنيع أو تطوير أنواع مختلفة من مجمدات بنوك الدم ؛ كما أدى ذلك إلى اعتماد مجمدات ULT للتخزين الآمن بسبب الإرشادات الصارمة التي فرضتها منظمة الصحة العالمية لتخزين عينات الدم، مما يساهم في نمو سوق الثلاجات الطبية.

ويشهد قطاع الرعاية الصحية تطورات تكنولوجية تعمل على تسريع تبني وقبول الثلاجات الطبية. ونتيجة لذلك، تركز الشركات على تصنيع المبردات الطبيعية الموفرة للطاقة وضواغط العاكس لتقليل استهلاك الطاقة بشكل فعال من خلال التحكم في الدوران البطيء السرعة. يجب تخزين عينات البحث البيولوجي تحت -80 درجة مئوية، أي عند قيم درجات الحرارة المنخفضة للغاية (ULT). توفر ميزة ULT بديلاً لتقنية التبريد القياسية القائمة على الضاغط والتي تستمر في التحسن مع نمو فهمها. علاوة على ذلك، تتميز المنتجات المبتكرة من شركة هاير بيوميديكال، مثل تقنية تحويل التردد الذكي، باستهلاك طاقة لا مثيل له يبلغ 8.2 كيلو وات في الساعة / يوم بسعة وحدة تبلغ 829 لتر / 29.2 قدم مكعب. وبالمثل، تحظى تقنيات أخرى، مثل كلمات المرور الافتراضية الفريدة للمجمدات الذكية، والتبريد بالحالة الصلبة، وأنظمة الباركود ثنائية الأبعاد، والمجمدات المشتركة، ومجمدات المختبرات المتنقلة، باهتمام كبير.

علاوة على ذلك، تطبق العديد من المستشفيات الجديدة استراتيجيات مختلفة للحد من الاستثمارات الرأسمالية. يعد شراء المعدات المجددة أو المجددة الموجودة إحدى الطرق لتلبية الطلب المرتفع على المنتجات المعقولة التكلفة والموثوقة. لا تطلب المستشفيات الصغيرة ذات الميزانيات المحدودة فقط معدات التصوير الطبي المجددة، بل وأيضًا بعض المعاهد الطبية الرائدة. علاوة على ذلك، تعد الأجهزة الطبية المجددة فعالة من حيث التكلفة، والقيود الميزانية على العديد من المستويات، وخاصة في قطاعات الرعاية الصحية في البلدان الحساسة للتكلفة، تجبر المعاهد الطبية على اختيار هذه الأجهزة. أنشأ العديد من الشركات المصنعة الأصلية والمجددة المستقلة سوقًا منفصلة للأجهزة المستعملة المزدهرة في الهند. ومع ذلك، أثار المصنعون المحليون العديد من القضايا، مطالبين بحظر تام لمثل هذه الأجهزة. لا تقدم الشركات المصنعة الكبرى في سوق الثلاجات الطبية مجمدات مجددة، مما يعيق أداءها في السوق. وبالتالي، فإن تفضيل المستهلك المتزايد للمعدات المجددة يعيق انتشار السوق إلى حد ما.

تقسيم التقرير ونطاقه:

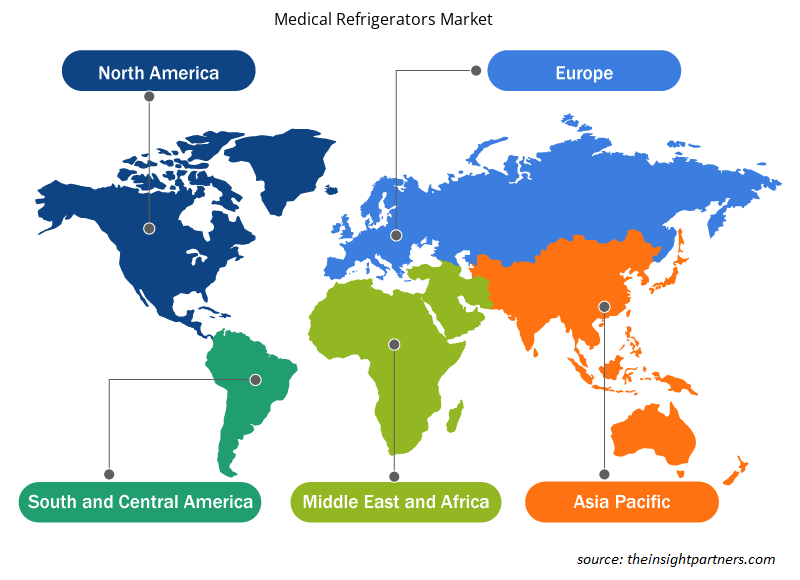

يتم تقسيم "سوق الثلاجات الطبية العالمية" بناءً على نوع المنتج ونوع التصميم ونوع الباب ونطاق التحكم في درجة الحرارة والحجم والمستخدم النهائي. بناءً على نوع المنتج، يتم تقسيم سوق الثلاجات الطبية إلى ثلاجات ومجمدات للمختبرات، وثلاجات ومجمدات الكروماتوغرافيا، ومجمدات ذات درجات حرارة منخفضة للغاية ، وثلاجات بنوك الدم ومجمدات البلازما، وأنظمة التخزين المبردة، وثلاجات ومجمدات الصيدلة، وثلاجات ومجمدات الإنزيمات، وثلاجات ومجمدات المستشفيات، ومجمدات الصدمات، وغيرها. بناءً على نوع التصميم، يتم تقسيم سوق الثلاجات الطبية إلى ثلاجات مقاومة للانفجار، وثلاجات طبية تحت المنضدة، وثلاجات طبية فوق المنضدة، وثلاجات تخزين المواد القابلة للاشتعال. بناءً على نطاق التحكم في درجة الحرارة، يتم تقسيم سوق الثلاجات الطبية إلى ما بين -1 و-50 درجة مئوية، وما بين 2 درجة مئوية و8 درجات مئوية، وما بين -51 و-150 درجة مئوية، وأقل من -151 درجة مئوية. بناءً على المستخدمين النهائيين، يتم تقسيم سوق الثلاجات الطبية إلى المستشفيات والصيدليات والمختبرات الطبية وبنوك الدم وشركات الأدوية ومعاهد البحوث ومراكز التشخيص. بناءً على الجغرافيا يتم تقسيمها إلى أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك) وأوروبا (ألمانيا وفرنسا وإيطاليا والمملكة المتحدة وإسبانيا وبقية أوروبا) وآسيا والمحيط الهادئ (أستراليا والصين واليابان والهند وكوريا الجنوبية وبقية آسيا والمحيط الهادئ) والشرق الأوسط وأفريقيا (جنوب أفريقيا والمملكة العربية السعودية والإمارات العربية المتحدة وبقية الشرق الأوسط وأفريقيا) وأمريكا الجنوبية والوسطى (البرازيل والأرجنتين وبقية أمريكا الجنوبية والوسطى).

التحليل القطاعي:

بناءً على نوع المنتج، يتم تقسيم سوق الثلاجات الطبية إلى ثلاجات ومجمدات للمختبرات، وثلاجات ومجمدات الكروماتوغرافيا، ومجمدات ذات درجات حرارة منخفضة للغاية، وثلاجات بنوك الدم ومجمدات البلازما، وأنظمة التخزين المبردة، وثلاجات ومجمدات الصيدليات، وثلاجات ومجمدات الإنزيمات، وثلاجات ومجمدات المستشفيات، ومجمدات الصدمة، وغيرها. احتلت ثلاجات بنوك الدم ومجمدات البلازما الحصة الأكبر من السوق. إن الانتشار المتزايد للأمراض المختلفة وارتفاع حوادث الطرق، مما يؤكد على الحاجة إلى الحفاظ على مخزون كافٍ في بنوك الدم وتنظيم معسكرات التبرع بالدم، يعزز نمو سوق القطاع. علاوة على ذلك، من المتوقع أن ينمو نفس القطاع بأعلى معدل نمو سنوي مركب خلال الفترة 2022-2030.

بناءً على نوع التصميم، يتم تقسيم سوق الثلاجات الطبية إلى ثلاجات مقاومة للانفجار، وثلاجات طبية تحت المنضدة، وثلاجات طبية فوق المنضدة، وثلاجات تخزين المواد القابلة للاشتعال. احتل قطاع الثلاجات الطبية فوق المنضدة الحصة الأكبر من السوق. ومع ذلك، من المتوقع أن يسجل قطاع الثلاجات الطبية تحت المنضدة أعلى معدل نمو سنوي مركب في السوق خلال الفترة 2022-2030. يرجع نمو سوق قطاع الثلاجات الطبية فوق المنضدة إلى حجمها الصغير وقدرتها على التكيف مع المساحات الأصغر مثل مختبرات الأبحاث الصغيرة والعيادات ومرافق الرعاية الصحية الواقعة في أماكن نائية.

بناءً على نطاق التحكم في درجة الحرارة، ينقسم سوق الثلاجات الطبية إلى ما بين -1 و-50 درجة مئوية، وما بين 2 درجة مئوية و8 درجات مئوية، وما بين -51 و-150 درجة مئوية، وأقل من -151 درجة مئوية. قادت شريحة ما بين -1 درجة مئوية و-50 درجة مئوية السوق في عام 2022 بأعلى حصة سوقية ومن المتوقع أن تحتفظ بهيمنتها خلال الفترة 2022-2030.

بناءً على المستخدمين النهائيين، يتم تقسيم سوق الثلاجات الطبية إلى المستشفيات والصيدليات والمختبرات الطبية وبنوك الدم وشركات الأدوية ومعاهد الأبحاث ومراكز التشخيص وغيرها. احتل قطاع بنوك الدم الحصة الأكبر من السوق في عام 2022، ومن المتوقع أيضًا أن يسجل أعلى معدل نمو سنوي مركب. إن الانتشار المتزايد لأمراض الدم وارتفاع حالات الحوادث يدفعان نمو السوق لقطاع بنوك الدم.

التحليل الإقليمي:

بناءً على الجغرافيا، ينقسم سوق الثلاجات الطبية العالمية إلى خمس مناطق رئيسية: أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ وأمريكا الجنوبية والوسطى والشرق الأوسط وأفريقيا. في عام 2022، احتلت أمريكا الشمالية أكبر حصة سوقية عالمية للثلاجات الطبية. كان سوق الثلاجات الطبية في الولايات المتحدة هو الرائد في منطقة أمريكا الشمالية. يُعزى نمو السوق إلى زيادة الإنفاق على البحث والتطوير، ويُعزى النمو السريع للمنطقة إلى التطورات في قطاعي الأدوية والتكنولوجيا الحيوية. بالإضافة إلى ذلك، فإن ارتفاع معدلات الإصابة بالسرطان في الولايات المتحدة وزيادة اعتماد الثلاجات والمجمدات الطبية الحيوية من شأنه أن يدفع السوق. بالإضافة إلى ذلك، ينمو عدد بنوك الدم والصيدليات والمختبرات التشخيصية بسرعة في جميع أنحاء البلاد بسبب اللاعبين الرئيسيين في السوق في الولايات المتحدة.

من المتوقع أن تشهد منطقة آسيا والمحيط الهادئ معدل نمو سنوي مركب مرتفع في سوق الثلاجات الطبية العالمية بسبب التطور التكنولوجي المتزايد والوعي بصحة الناس ونظافتهم. نظرًا للعمالة الرخيصة والماهرة في منطقة آسيا والمحيط الهادئ، فهي أسرع القطاعات نموًا، وتنقل العديد من الشركات مرافق التصنيع الخاصة بها إلى هناك. نظرًا للاستخدام المتزايد للثلاجات الطبية، من المتوقع أن ينمو السوق بسرعة في الهند والصين. علاوة على ذلك، تتزايد أيضًا المبادرات الحكومية لزيادة عدد عينات الدم التي يتم جمعها. في الهند، تساعد المنظمة الوطنية لمكافحة الإيدز (NACO) والمجلس الوطني لنقل الدم (NBTC) في الترويج للتبرع الطوعي بالدم. ومن المتوقع أن ينمو الطلب على الثلاجات الطبية مع زيادة عدد وحدات الدم التي يتم جمعها. ومن المتوقع أن ينمو السوق مع زيادة الاستثمارات والتمويل لتحسين مرافق الرعاية الصحية والبنية التحتية.

نظرة إقليمية على سوق الثلاجات الطبية

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق الثلاجات الطبية طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق الثلاجات الطبية والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق الثلاجات الطبية

نطاق تقرير سوق الثلاجات الطبية

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 4.67 مليار دولار أمريكي |

| حجم السوق بحلول عام 2028 | 6.5 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2028) | 5.8% |

| البيانات التاريخية | 2020-2021 |

| فترة التنبؤ | 2023-2028 |

| القطاعات المغطاة | حسب نوع المنتج

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

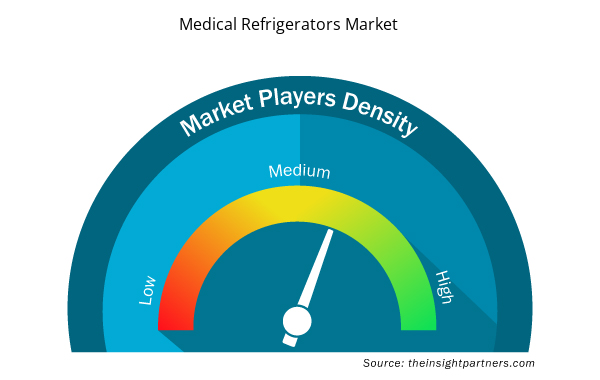

كثافة اللاعبين في السوق: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق الثلاجات الطبية نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلك المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق الثلاجات الطبية هي:

- شركة ثيرمو فيشر العلمية

- شركة فيليب كيرش المحدودة

- شركة جودريج وبويس للتصنيع المحدودة

- مجموعة شركات هاير

- شركة بلو ستار المحدودة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق الثلاجات الطبية

تطورات الصناعة والفرص المستقبلية:

فيما يلي قائمة بالمبادرات المختلفة التي اتخذتها شركات الثلاجات الطبية الرائدة العاملة في سوق الثلاجات الطبية العالمية:

- في مارس 2022، أعلنت شركة B Medical Systems أن منتجها Ultra-Low Freezer U201 قد حصل على موافقة WHO PQS المسبقة.

- في يناير 2022، أعلنت شركة B Medical Systems عن خطتها لافتتاح منشأة تصنيع جديدة في الهند لتلبية الطلب المتزايد على منتجات سلسلة التبريد الطبية، بما في ذلك ثلاجات اللقاحات، في البلاد.

- في ديسمبر 2020، تعاونت شركة Tobin Scientific وPHCbi على حل توزيع لقاح COVID-19 الإقليمي لتلبية الحاجة إلى متطلبات درجات الحرارة المنخفضة للغاية.

- في يونيو 2020، استحوذت دولاس على شركة بوليستار، وهي شركة مقرها المملكة المتحدة كانت رائدة في الاستخدام المبتكر للطاقة الشمسية والطاقة الكهرومائية وطاقة الرياح وثلاجات الرعاية الصحية الحديثة لتخزين اللقاحات. بوليستار هي شركة مقرها المملكة المتحدة تنتج معدات التبريد الصناعية والطبية.

- في أبريل 2020، وقعت شركة Thermo Fisher Scientific اتفاقية شراكة مع شركة DKSH لتوزيع ثلاجات Revco RDE Series Ultra Low Temperature (ULT). ركزت هذه الاتفاقية بشكل أساسي على القطاع السريري.

- في ديسمبر 2020، أعلنت شركة Follett LLC عن توسيع مرافق التصنيع التابعة لها في Forks Township. بإضافة 12 مليون دولار أمريكي و90 ألف قدم مربع، سيرتفع إجمالي مساحة التصنيع والمكاتب تحت السقف إلى حوالي 250 ألف قدم مربع. تم الانتهاء من التوسع والاستثمارات المرتبطة به بحلول منتصف عام 2021.

المنافسة والشركات الرئيسية:

تشمل بعض شركات الثلاجات الطبية البارزة العاملة في السوق شركة Thermo Fisher Scientific Inc.؛ وPhilipp Kirsch GmbH، وGodrej & Boyce Manufacturing Company Limited، وHaier Group Corporation، وBlue Star Limited، وHelmer Scientific Inc.؛ وVestfrost Solutions، وPHC Holdings Corporation، وFOLLETT LLC، وLec Medical، وغيرها. تركز الشركة على إطلاق منتجات جديدة والتوسع الجغرافي لتلبية الطلب العالمي المتزايد وزيادة نطاق منتجاتها في محافظ المنتجات المتخصصة. يسمح لها وجودها العالمي الواسع بخدمة العديد من العملاء وزيادة حصتها في السوق.

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

- 3D Mapping and Modelling Market

- Skin Tightening Market

- High Speed Cable Market

- Blood Collection Devices Market

- Fixed-Base Operator Market

- Arterial Blood Gas Kits Market

- USB Device Market

- Water Pipeline Leak Detection System Market

- Hair Extensions Market

- Pharmacovigilance and Drug Safety Software Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

Thermo Fisher Scientific Inc. and PHC Holdings Corporation are the top two companies that hold huge market shares in the medical refrigerators market.

The laboratory refrigerators and freezers segment held the largest share of the market in the global medical refrigerators market and held the largest market share of 41.00% in 2022.

The medical refrigerators market majorly consists of the players such Thermo Fisher Scientific Inc., Philipp Kirsch GmbH, Godrej & Boyce Manufacturing Company Limited, Haier Group Corporation, Blue Star Limited, Helmer Scientific Inc., Vestfrost Solutions, PHC Holdings Corporation, FOLLETT LLC, and Lec Medical among others.

The CAGR value of the medical refrigerators market during the forecasted period of 2023-2028 is 5.8%.

Key factors that are driving the growth of this market are increasing demand for blood and blood components, technological advancements in medical refrigerators, and growing R&D activities to introduce new drug compounds are expected to boost the market growth for the medical refrigerators over the years.

The countertop medical refrigerators segment dominated the global medical refrigerators market and accounted for the largest market share of 47.31% in 2022.

Medical refrigerators are used to store vaccines, pharmaceuticals, chemotherapeutics, blood, plasma, and other samples that require tight temperature control. These are more reliable products for the storage of medicinal products as they emit less heat and less sound into the room. Rising occurrence of hematological disorders and an increment in the number of accidents have increased the requirement for plasma for employment in plasma fractionation operations. In return, this requirement has led to an increase in requirements for plasma freezers and refrigerators at the blood bank. These features are boosting demand for blood bank development worldwide. Thus, driving demand for medical refrigerators for pharmaceutical and laboratory use.

The between -1 to -50°C segment dominated the global medical refrigerators market and held the largest market share of 38.91% in 2022.

The hospitals and pharmacies segment dominated the global medical refrigerators market and held the largest market share of 41.16% in 2022.

Global medical refrigerators market is segmented by region into North America, Europe, Asia Pacific, Middle East & Africa and South & Central America. In North America, the U.S. is the largest market for medical refrigerators. The region is expected to witness a consistent growth owing to factors such as rising research activities for the treatment of diseases, increasing occurrence of chronic and infectious diseases, and the replacement of older medical refrigerators with newer and more advanced energy-efficient cold storage device. The Asia Pacific region is expected to account for the fastest growth in the medical refrigerators market. In India and China, the market is expected to grow rapidly owing to factors such as the research activities & pharmaceutical manufacturing and increasing investments by leading players and respective government agencies in emerging APAC countries.

The List of Companies - Medical Refrigerators

- THERMO FISHER SCIENTIFIC INC.

- Philipp Kirsch GmbH

- Godrej & Boyce Manufacturing Company Limited

- Haier Group Corporation

- Blue Star Limited

- Helmer Scientific Inc.

- Vestfrost Solutions

- PHC Holdings Corporation

- FOLLETT LLC

- Lec Medical

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير