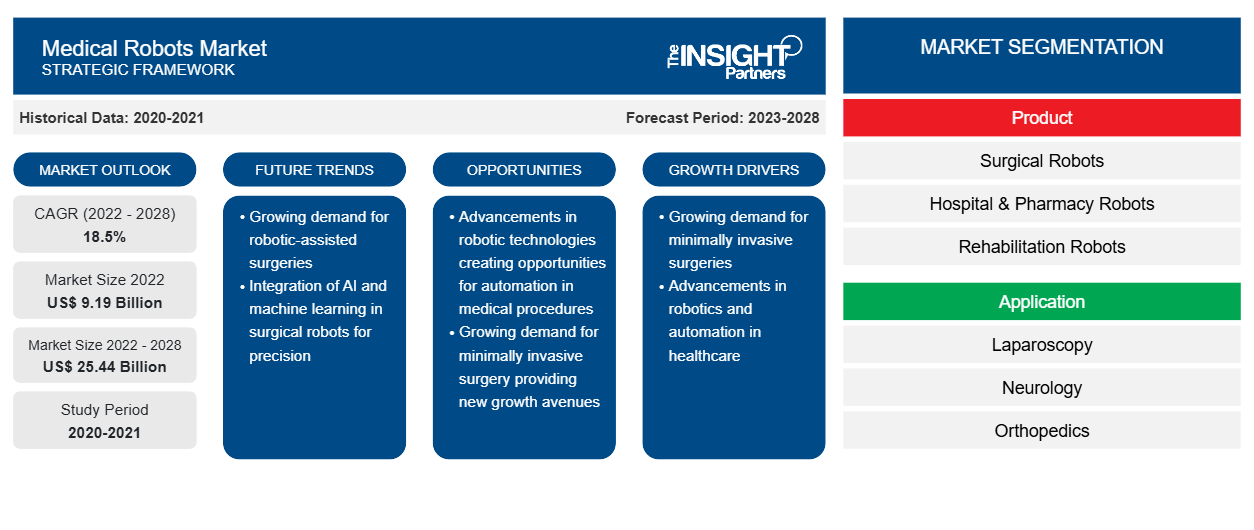

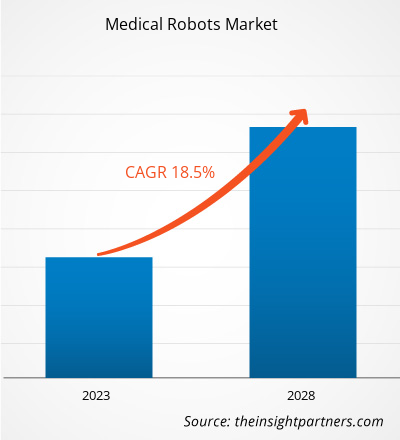

من المتوقع أن يصل سوق الروبوتات الطبية إلى 25،443.36 مليون دولار أمريكي بحلول عام 2028 من قيمة تقديرية قدرها 9،189.70 مليون دولار أمريكي في عام 2022؛ ومن المتوقع أن ينمو بمعدل نمو سنوي مركب قدره 18.5٪ من عام 2022 إلى عام 2028.

من المتوقع أن يؤدي العدد المتزايد من العمليات الجراحية وارتفاع عدد عمليات إطلاق المنتجات والموافقات عليها إلى دفع سوق الروبوتات الطبية . ومع ذلك، فإن التكلفة العالية للإجراءات الجراحية والتركيب تعيق نمو السوق.

تم تصميم الروبوتات الطبية لتطبيقات طبية متخصصة. يمكن لهذه الروبوتات إجراء مجموعة متنوعة من المهام الطبية مثل الجراحة والاختبارات الطبية ومراقبة المريض. يمكنها إجراء الجراحة بناءً على التخطيط الجراحي المسبق فقط. تمكن الروبوتات الطبية من الدقة العالية في الجراحات المفتوحة والجراحات قليلة التوغل. كما أنها تقلل بشكل كبير من الوقت المطلوب للجراحة. علاوة على ذلك، يمكن استخدام الروبوتات الطبية لنقل المرضى من مكان إلى آخر في المستشفى. الروبوتات للرعاية عن بعد، وروبوتات التطهير لتقليل العدوى المكتسبة من المستشفى، والهياكل الخارجية الروبوتية لتدريب إعادة التأهيل التي توفر الدعم الخارجي وتدريب العضلات كلها أمثلة على تطبيقات الروبوتات الطبية. تم استخدام تقنية الروبوتات في الرعاية الصحية لأول مرة في عام 1985، على الرغم من أنه في عام 2000 فقط حصل روبوت دافنشي على موافقة إدارة الغذاء والدواء الأمريكية لإجراء العمليات الجراحية. يُعرف روبوت دافنشي على نطاق واسع بتطبيقاته في جراحة القلب وجراحة الرأس والرقبة وجراحة المسالك البولية.

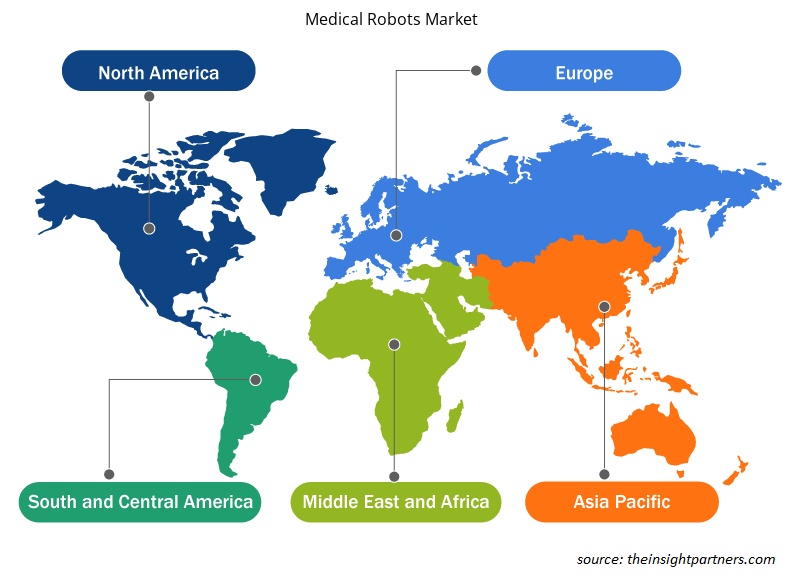

من المرجح أن تهيمن أمريكا الشمالية على سوق الروبوتات الطبية خلال فترة التنبؤ. استحوذت الولايات المتحدة على أكبر حصة من سوق أمريكا الشمالية في عام 2022 ومن المتوقع أن تستمر في هذا الاتجاه خلال فترة التنبؤ. وفقًا لدراسة نشرتها الجمعية الأمريكية لجراحة التمثيل الغذائي والسمنة في عام 2022، شهدت الولايات المتحدة نموًا بنسبة 62.0٪ تقريبًا في جراحات السمنة خلال العقد الماضي. بالإضافة إلى ذلك، وفقًا للدراسة التي نشرتها وكالة أبحاث الرعاية الصحية والجودة في عام 2017، تم إجراء حوالي 0.7 مليون عملية جراحية لاستبدال الركبة بالكامل في الولايات المتحدة سنويًا. ومن المقدر أن يوفر هذا العدد الكبير من الإجراءات الجراحية بيئة مواتية لتبني مرافق الرعاية الصحية المتقدمة التي ستقود سوق الروبوتات الطبية في الولايات المتحدة خلال فترة التنبؤ.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق الروبوتات الطبية:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

يتم تقسيم سوق الروبوتات الطبية بناءً على المنتج والتطبيق والمستخدم النهائي والجغرافيا. من حيث الجغرافيا، يتم تقسيم السوق على نطاق واسع إلى أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى. يقدم تقرير الروبوتات الطبية رؤى وتحليلات متعمقة للسوق، مع التركيز على معايير مثل اتجاهات السوق والتقدم التكنولوجي وديناميكيات السوق والتحليل التنافسي للاعبين الرائدين في السوق عالميًا.

رؤى السوق

عدد كبير من العمليات الجراحية

هناك ارتفاع في عدد العمليات الجراحية التي يتم إجراؤها على مستوى العالم. وقد حدثت زيادة في حالات الإصابة بأمراض القلب والأوعية الدموية في الدول الأوروبية خلال السنوات الخمس والعشرين الماضية. وفي المنطقة، أدى ارتفاع حالات الإصابة بمرض السكري وتغييرات نمط الحياة إلى زيادة عدد جراحات القلب والأوعية الدموية والجراحات العامة.

يعد السرطان والسكري من الأسباب الرئيسية للوفاة على مستوى العالم. ووفقًا لدراسة أجرتها الجمعية الأمريكية للسرطان (ACS)، في عام 2021، تم تشخيص حوالي 1.9 مليون حالة إصابة بالسرطان جديدة في الولايات المتحدة. وفي عام 2021، وفقًا لسجل السرطان الهولندي، تم تسجيل حوالي 123672 حالة إصابة جديدة بالسرطان في هولندا. وعلاوة على ذلك، وفقًا للاتحاد الدولي للسكري (IDF)، في عام 2021، كان ما يقدر بنحو 537 مليون شخص في جميع أنحاء العالم مصابين بالسكري. ومن المتوقع أن يصل العدد إلى 783 مليون بحلول عام 2045.

وفقًا للدراسة التي نشرتها الجمعية الأمريكية لجراحة الأيض والسمنة، تم إجراء حوالي 252000 عملية جراحية لفقدان الوزن في الولايات المتحدة في عام 2019. يخلق العدد المتزايد من العمليات الجراحية الحاجة إلى أدوات الجراحة الروبوتية. لذلك، فإن الانتشار المذهل للأمراض المزمنة والعدد المتزايد من العمليات الجراحية يولد الطلب على أدوات الجراحة الروبوتية.

رؤى المنتج

بناءً على المنتج، يتم تقسيم سوق الروبوتات الطبية العالمية إلى روبوتات جراحية وروبوتات إعادة التأهيل وروبوتات جراحة الراديو غير الجراحية وروبوتات المستشفيات والصيدليات وغيرها. يتم تقسيم الروبوتات الجراحية إلى أنظمة روبوتية لجراحة الأعصاب وأنظمة روبوتية لجراحة القلب وأنظمة روبوتية جراحية بالمنظار وأنظمة روبوتية جراحية للعظام. في عام 2022، احتل قطاع الروبوتات الجراحية الحصة الأكبر من السوق. الجراحات الروبوتية هي إجراءات جراحية يتم إجراؤها باستخدام أنظمة جراحية آلية. الروبوتات الجراحية هي أجهزة طبية ذاتية التشغيل ويتم التحكم فيها بواسطة الكمبيوتر ومبرمجة للمساعدة في وضع الأدوات الجراحية والتلاعب بها، تساعد هذه الروبوتات الجراحية الجراحين على إجراء العمليات الجراحية المعقدة. تتمتع هذه الروبوتات بالقدرة على تعزيز قدرات الجراحين الذين يقومون بإجراء الجراحة المفتوحة. لذلك، يُسمح للروبوتات الجراحية بإجراء العمليات الجراحية المعقدة والمتقدمة بدقة متزايدة من خلال طرق طفيفة التوغل. ومع ذلك، من المتوقع أن يسجل قطاع روبوتات إعادة التأهيل أعلى معدل نمو سنوي مركب خلال فترة التنبؤ.

رؤى التطبيق

بناءً على التطبيق، يتم تقسيم سوق الروبوتات الطبية العالمية إلى تنظير البطن، وطب الأعصاب، وجراحة العظام، وأمراض النساء، وأمراض المسالك البولية، وأمراض القلب، وغيرها. في عام 2022، احتل قطاع تنظير البطن الحصة الأكبر من السوق. ومع ذلك، من المتوقع أن يسجل قطاع طب الأعصاب أعلى معدل نمو سنوي مركب خلال فترة التنبؤ. تنظير البطن هو إجراء تشخيصي جراحي يستخدم لفحص الأعضاء داخل البطن. الجراحة الروبوتية هي إجراء طفيف التوغل يتطلب شقوقًا صغيرة فقط وينطوي على مخاطر منخفضة. في عام 2000، أصبح نظام جراحة دافنشي أول نظام جراحة روبوتية معتمد من قبل إدارة الغذاء والدواء للجراحة التنظيرية العامة. وأحدث طراز متطور هو دافنشي Xi. أدى نشر الروبوتات الطبية إلى تحسين الكفاءة في الإجراءات الجراحية بالمنظار. في يناير 2022، أجرى روبوت جراحة بالمنظار على الأنسجة الرخوة للخنزير دون يد توجيهية للإنسان. مع تحرك المجال الطبي نحو المزيد من الأساليب الجراحية التي تعتمد على التنظير البطني، سيكون من المهم أن يكون لدينا نظام آلي مصمم لمثل هذه الإجراءات للمساعدة. أحد الأسباب الرئيسية وراء التفضيل المتزايد للإجراءات التنظيرية في السنوات الأخيرة هو التحول التدريجي لقطاع الرعاية الصحية بعيدًا عن الجراحات المفتوحة. من المرجح أن ينمو سوق التنظير البطني في السنوات القادمة بسبب جميع العوامل المذكورة أعلاه.

رؤى المستخدم النهائي

بناءً على المستخدم النهائي، يتم تقسيم سوق الروبوتات الطبية العالمية إلى مستشفيات ومراكز جراحية متنقلة وغيرها. في عام 2022، احتل قطاع المستشفيات الحصة الأكبر من السوق. علاوة على ذلك، من المتوقع أن يسجل نفس القطاع أعلى معدل نمو سنوي مركب في السوق خلال فترة التنبؤ، وذلك بسبب المزايا الطبية واستخدام الروبوتات الطبية في الإجراءات الجراحية بمعدل متزايد والأداء المحسن للروبوتات أثناء الإجراءات الجراحية.

تعد عمليات إطلاق المنتجات والتعاون من الاستراتيجيات المعتمدة على نطاق واسع من قبل اللاعبين في سوق الروبوتات الطبية العالمية لتوسيع بصماتهم العالمية ومحافظ منتجاتهم. يركز اللاعبون أيضًا على استراتيجية الشراكة لتوسيع قاعدة عملائهم، مما يسمح لهم بدوره بالحفاظ على اسم علامتهم التجارية عالميًا. إنهم يهدفون إلى ازدهار حصصهم في السوق من خلال تطوير المنتجات المبتكرة. فيما يلي بعض التطورات الرئيسية الأخيرة في السوق:

- في فبراير 2022، استحوذت شركة Capsa Healthcare، وهي شركة رائدة في مجال ابتكار حلول تقديم الرعاية الصحية للمستشفيات ومقدمي الرعاية طويلة الأجل والصيدليات بالتجزئة، على شركة Humanscale Healthcare، وهي شركة مصممة ومصنعة لحلول التكنولوجيا المرنة ومحطات العمل الحاسوبية ومقرها مدينة نيويورك، نيويورك.

- في يناير 2022، أطلقت شركة Omnicell, Inc. محطة Reimaging IV، وهي روبوت تحضير المحاليل الوريدية الآلي بالكامل والذي يعالج مشكلات الصناعة بشكل مباشر مع توفير سلامة المرضى والدقة وتوفير التكاليف والتحكم في سلسلة التوريد وفوائد الامتثال.

- في أكتوبر 2021، أطلقت Accuray نظام Precision Treatment Planning System، الذي يتيح للمستخدمين التخطيط بسهولة وتحسين الجودة وتقديم العلاجات بكفاءة. VOLO Ultra هو أحدث تطور لحل التخطيط، وهو نظام Accuray Precision Treatment Planning System. يساعد في تسريع علاجات Radixact وTomoTherapy حتى يتمكن الأطباء من علاج المزيد من المرضى كل يوم. وهو يتضمن مُحسِّنًا متطورًا مع خوارزمية حديثة وسريعة تعتمد على التدرج توفر جودة خطة مثالية لكل علاج.

- في يونيو 2021، أطلقت شركة ARxium الروبوت "RIVA" في مستشفى جامعة ليل لإعداد العلاجات الكيميائية القابلة للحقن.

رؤى إقليمية حول سوق الروبوتات الطبية

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق الروبوتات الطبية طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق الروبوتات الطبية والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق الروبوتات الطبية

نطاق تقرير سوق الروبوتات الطبية

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 9.19 مليار دولار أمريكي |

| حجم السوق بحلول عام 2028 | 25.44 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2028) | 18.5% |

| البيانات التاريخية | 2020-2021 |

| فترة التنبؤ | 2023-2028 |

| القطاعات المغطاة | حسب المنتج

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق الروبوتات الطبية: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق الروبوتات الطبية نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق الروبوتات الطبية هي:

- أبوت

- شركة ف. هوفمان-لاروش المحدودة

- شركة إيمونيكسبريس

- بنغلاديش

- داناهر

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق الروبوتات الطبية

الروبوتات الطبية – تقسيم السوق

يتم تقسيم سوق الروبوتات الطبية العالمية على أساس المنتج والتطبيق والمستخدم النهائي. من حيث المنتج، يتم تقسيم سوق الروبوتات الطبية العالمية إلى روبوتات جراحية وروبوتات إعادة تأهيل وروبوتات جراحة إشعاعية غير جراحية وروبوتات مستشفيات وصيدليات وغيرها. بناءً على التطبيق، يتم تقسيم سوق الروبوتات الطبية العالمية إلى تنظير البطن وطب الأعصاب وجراحة العظام وأمراض النساء وأمراض المسالك البولية وأمراض القلب وغيرها. من حيث المستخدم النهائي، يتم تقسيم سوق الروبوتات الطبية إلى مستشفيات ومراكز جراحية متنقلة وغيرها.

نبذة عن الشركة

- شركة الجراحة البديهية

- شركة سترايكر

- شركة هوكوما ايه جي

- ميدترونيك

- شركة أوريس هيلث

- شركة أكوراي المحدودة

- شركة أومنيسيل

- أركسيوم

- شركة إكسو بيونيكس القابضة المحدودة

- كيربي ليستر ذ.م.م.

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

- Virtual Event Software Market

- Artificial Intelligence in Defense Market

- Redistribution Layer Material Market

- Europe Surety Market

- Smart Mining Market

- Embolization Devices Market

- Adaptive Traffic Control System Market

- Non-Emergency Medical Transportation Market

- Procedure Trays Market

- Rare Neurological Disease Treatment Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

The pandemic of coronavirus disease 2019 (COVID-19) has increased hospital resource us. As a result, health care systems are overburdened, and the delivery of medical care to all patients has become a challenge in the region. In addition, medical device industry is also facing negative impact of this pandemic. As the COVID-19 pandemic continues to unfold, medical device companies are finding difficulties in managing their operations. Many companies offering medical robots have their business operations in the United states and business are adversely being affected by the effects of a widespread outbreak of COVID-19. This has disrupted and restricted company’s ability to distribute products, as well as temporary closures of company’s facilities. However, gradually hospitals have started resuming elective procedures as the COVID-19 recovery rate is increasing the demand for medical equipment like medical robots is expected to increase.

In 2022, North America is likely to account for the largest share in the global medical robots market. However, Asia Pacific is projected to grow at a faster pace over the forecast period. The growth of the medical robots market in this region is primarily due to increasing number of minimally invasive surgeries in Japan and China, due to the rise in the medical tourism in India, and the growth in the initiatives taken by government to enhance the usage of medical robots.

The medical robots market majorly consists of players such as Intuitive Surgical, Inc., Stryker Corporation, Hocoma AG, Medtronic, Auris Health, Inc., Accuray Incorporated, Omnicell Inc., Arxium, Ekso Bionics Holdings, Inc., ad Kirby Lester LLC among others.

Intuitive Surgical, Inc., and Stryker Corporation are the top two companies that hold huge market shares in the medical robots market.

The surgical robots segment is likely to for the largest share in the global medical robots market by product owing to key factors like rise of technological innovations in robotic systems to increase their efficiency and utility, rapid advancements in surgical robots, rising demand for minimal invasive surgical procedures, advantages of robotic assisted surgeries, the post-surgery benefits, and rising per capita healthcare spending in emerging countries.

The CAGR value of the medical robots market during the forecasted period of 2022-2028 is 18.5%.

Medical robots are designed to assist surgeons during the surgical procedures. Medical robots are professional service robots that are used inside and outside of the hospital settings to progress the overall level of patient care. They reduce the workload of healthcare staff, enabling them to spend more time caring directly to patients while creating substantial operational procedure which provides efficacy and reduced cost investments for healthcare amenities. The medical robots are majorly used for surgical producers, there are different types of medical robots. The types of the medical robots include surgical robots, rehabilitation robots, hospital & pharmacy robots, and more.

The use of the medical robots is more in countries of US as the technological advancement is matured and is highly involved in the research and developments for the healthcare and medical industries. The Canada is also a matured market for the medical robotics as the rise in the support by the government for the developments of the medical equipment is rising with the help of financial support. However, the Mexico is the late adopter of the medical robots still the market is likely to propel significantly in the forecasted period due to the advantages provided by the medical robots.

The List of Companies - Medical Robots Market

- Abbott

- F. Hoffmann-La Roche Ltd.

- Immunexpress Inc.

- BD

- Danaher

- Luminex Corporation

- Thermo Fisher Scientific Inc.

- bioMerieux SA.

- T2 Biosystems, Inc.

- Axis-Shield Diagnostics Ltd.

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير