نمو سوق إعادة تبطين الأنابيب، حجمه، حصته السوقية، اتجاهاته، تحليلات اللاعبين الرئيسيين، والتوقعات حتى عام 2031

البيانات التاريخية : 2021-2023 | سنة الأساس : 2024 | فترة التنبؤ : 2025-2031حجم سوق إعادة تبطين الأنابيب وتوقعاته (2025-2031)، والحصة العالمية والإقليمية، والاتجاهات، وفرص النمو. يغطي التقرير: حسب الحل (المنتج (معدات CIPP، البطانة، نفاثات الماء عالية الضغط، أسطوانة الانعكاس، آلة السحب، وغيرها) والخدمة (الأنابيب المعالجة في الموقع (إصلاح البقعة أو الرقعة والبطانة أو الإصلاح الأطول)، السحب في الموقع، تفجير الأنابيب والطلاء الداخلي للأنابيب))، طريقة المعالجة (المعالجة في البيئة المحيطة، المعالجة بالماء الساخن، المعالجة بالبخار، والمعالجة بالأشعة فوق البنفسجية)، المستخدم النهائي (النفط والغاز، الكيماويات، البلديات، وغيرها)، والجغرافيا.

- تاريخ التقرير : May 2025

- رمز التقرير : TIPMC00002032

- الفئة : التصنيع والبناء

- الحالة : نُشرت

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 183

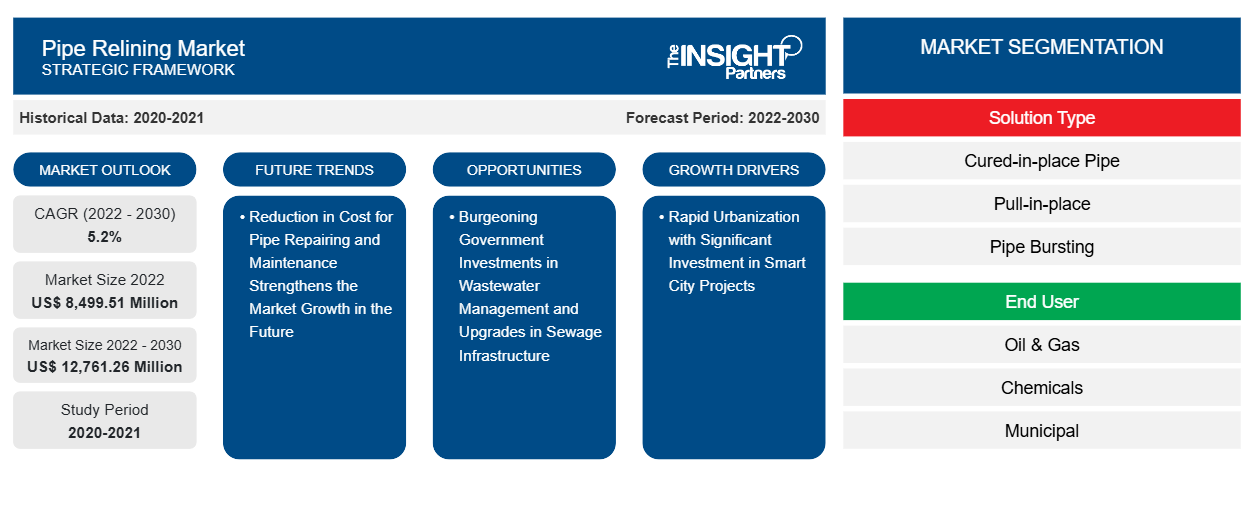

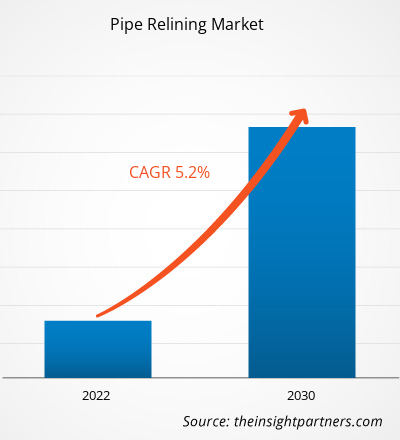

من المتوقع أن يصل حجم سوق إعادة تبطين الأنابيب إلى 13,093.73 مليون دولار أمريكي بحلول عام 2031، مقارنةً بـ 9,267.61 مليون دولار أمريكي في عام 2024. ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب قدره 5.3% خلال الفترة 2025-2031. ومن المرجح أن يُسهم انخفاض تكلفة إصلاح وصيانة الأنابيب في ظهور اتجاهات جديدة في السوق خلال السنوات القادمة.

تحليل سوق إعادة تبطين الأنابيب

يتألف سوق إعادة تبطين الأنابيب بشكل عام من ثلاثة أطراف رئيسية: موردو المعدات أو المواد، ومقدمو خدمات إعادة تبطين الأنابيب، والمستخدمون النهائيون. يقدم موردو المواد الخام والمعدات معدات ومواد إعادة تبطين الأنابيب لمقدمي الخدمات العاملين في هذا السوق. كما يقدم مقدمو الخدمات مجموعة واسعة من خدمات إعادة تبطين الأنابيب القياسية والمتخصصة لمستخدميهم النهائيين. ويشمل المستخدمون النهائيون لمعدات وخدمات إعادة تبطين الأنابيب بشكل رئيسي محطات معالجة المياه الحكومية، وشركات النفط والغاز، والبلديات، والمستخدمين السكنيين. وتقدم الجهات الحكومية تمويلًا لتجديد خطوط الأنابيب الحالية المتعلقة بالمياه، ومعالجة المياه، وخطوط الصرف الصحي، والنفط والغاز. ومن المتوقع أن يؤدي تزايد توافر التمويل إلى دفع عجلة سوق إعادة تبطين الأنابيب خلال فترة التوقعات. كما أن التركيز المتزايد على الحلول الفعالة من حيث التكلفة، والأقل تدخلاً، والصديقة للبيئة لتكنولوجيا إصلاح الأنابيب له تأثير إيجابي على سوق إعادة تبطين الأنابيب. ومن المتوقع أن يوفر التعاون المتزايد بين المصنّعين، ومقدمي الخدمات، والهيئات التنظيمية، والمستخدمين النهائيين فرصًا كبيرة لسوق إعادة تبطين الأنابيب في جميع أنحاء العالم.

نظرة عامة على سوق إعادة تبطين الأنابيب

تلعب إعادة تبطين الأنابيب دورًا محوريًا في قطاع تكنولوجيا الحفر بدون حفر، حيث تُقدم حلولًا مبتكرة لإعادة تأهيل وإصلاح خطوط الأنابيب القديمة أو التالفة دون الحاجة إلى حفر مكثف. وقد اكتسب سوق إعادة تبطين الأنابيب زخمًا على مر السنين، ويدعمه الطلب المتزايد على حلول إصلاح خطوط الأنابيب الفعالة من حيث التكلفة والمستدامة والأقل تدخلاً. ويشمل نطاق إعادة تبطين الأنابيب إصلاح أنابيب الصرف الصحي، وأنابيب المياه الرئيسية، وأنظمة الصرف الصحي، والأنابيب الصناعية في القطاعات البلدية والسكنية والتجارية.

عوامل مثل تزايد عدد البنى التحتية القديمة لأنابيب الأنابيب، واللوائح الصارمة المتعلقة بتسرب الأنابيب والأضرار التي تفرضها العديد من الجهات الحكومية، وهيئات تنظيم معايير السلامة، لها تأثير عميق على نمو السوق. علاوة على ذلك، فإن الطلب المتزايد من مختلف المستخدمين النهائيين، مثل النفط والغاز، والمواد الكيميائية، والقطاعات البلدية والصناعية، ومعالجة المياه، لا يزال يوفر فرصًا ثابتة، مما يدفع نمو سوق تجديد الأنابيب.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق إعادة تبطين الأنابيب: رؤى استراتيجية

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليل البيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محركات وفرص سوق إعادة تبطين الأنابيب

لوائح صارمة لمنع التسرب وصيانة شبكات الأنابيب

شهد سوق إعادة تبطين الأنابيب نموًا ملحوظًا في السنوات الأخيرة، مدفوعًا بالطلب المتزايد على حلول فعّالة من حيث التكلفة لإصلاح الأنابيب وتجديدها. وتُعد إعادة تبطين الأنابيب تقنيةً لا تتطلب حفر خنادق، وتتضمن تركيب بطانة أنبوب جديدة داخل أنبوب قائم دون الحاجة إلى حفر مكثف أو تعطيل البنية التحتية المحيطة. ومن العوامل الرئيسية المؤثرة على نمو سوق إعادة تبطين الأنابيب الطلب المتزايد على تجديد البنية التحتية للنفط والغاز. ومع استمرار نمو الطلب العالمي على الطاقة، يواجه قطاع النفط والغاز ضغوطًا متزايدة لصيانة وتطوير شبكته الواسعة من خطوط الأنابيب وغيرها من البنى التحتية الحيوية. وقد أدى ذلك إلى زيادة كبيرة في مشاريع إعادة التأهيل والتجديد، مما حفّز الطلب على حلول إعادة تبطين الأنابيب.

تستحوذ مشاريع بناء النفط والغاز في الشرق الأوسط وأفريقيا على الحصة الأكبر، تليها الولايات المتحدة. في عام 2024، بدأت شركة قطر للطاقة، وهي شركة الطاقة المملوكة للدولة في قطر، أنشطة تقييم شاملة في حقل الغاز الطبيعي التابع لها. تهدف هذه الجهود إلى زيادة احتياطيات البلاد من الغاز وتمهيد الطريق لتوسيع طاقتها الإنتاجية من الغاز الطبيعي المسال إلى 142 مليون طن سنويًا بحلول نهاية عام 2030. في عام 2024، مُنحت قطر للطاقة عقودًا بقيمة 6 مليارات دولار أمريكي لعمليات المرحلة التالية من تطوير حقل النفط البارز في الدولة الخليجية. يهدف مشروع "رؤية"، وهو مشروع التطوير الثالث لحقل الشاهين، وهو مشروع مشترك بين قطر للطاقة وتوتال للطاقة، إلى جلب أكثر من 550 مليون برميل من النفط. من المتوقع أن يبدأ المشروع الإنتاج في عام ٢٠٢٧، بهدف إنتاج ١٠٠ ألف برميل يوميًا من الحقل البحري. في يناير ٢٠٢٣، أعلنت شركة مصيرة للنفط، التابعة لشركة ريكس إنترناشونال المستقلة ومقرها سنغافورة، عن إتمامها حملة حفر بحرية في المربع ٥٠ بسلطنة عُمان. وفي أكتوبر ٢٠٢٣، أعلنت شركة كيه سي إيه دويتاغ، الشريك الرائد في مجال الحفر والهندسة والتكنولوجيا، عن أول منصة حفر محلية الصنع لها في عُمان خلال حفل أقيم لشركة تنمية نفط عُمان.

في عام 2024، أعلنت إدارة سلامة خطوط الأنابيب والمواد الخطرة التابعة لوزارة النقل أن الحكومة الأمريكية تخطط لمنح منح يبلغ مجموعها 196 مليون دولار أمريكي لإصلاح واستبدال خطوط أنابيب الغاز الطبيعي القديمة في 20 ولاية. في أبريل 2023، وافق مسؤولو ولاية ميشيغان الأمريكية على استثمار بقيمة 500 مليون دولار أمريكي لتجديد النفق الوقائي لخط أنابيب نفط قديم. يمتد خط أنابيب النفط تحت ولاية ميشيغان، ويربط بين بحيرتين عظيمتين. علاوة على ذلك، في أبريل 2023، حصلت شركة NV5 Global, Inc.، وهي شركة تقدم حلول تقييم المطابقة والاستشارات، على عقد بقيمة 16 مليون دولار أمريكي لتصميم ودعم خط أنابيب الغاز للمرافق العامة لمرافق الغاز في كاليفورنيا. تقدم شركة NV5 Global, Inc. تصميمًا هندسيًا لإدارة سلامة الأصول وتحسينات خطوط أنابيب الغاز لدعم توصيل الغاز الطبيعي بشكل موثوق وآمن. في مايو 2023، أعلنت السلطات الفيدرالية الأمريكية عن تمويل بقيمة 196 مليون دولار أمريكي ضمن برنامج بقيمة مليار دولار أمريكي لإصلاح واستبدال خطوط أنابيب الغاز الطبيعي القديمة والمتسربة في جميع أنحاء البلاد.

وفقًا لوزارة البترول والغاز الطبيعي، ارتفع طول خط أنابيب الغاز الطبيعي العامل في الهند من 15,340 كيلومترًا عام 2014 إلى 24,945 كيلومترًا عام 2024، بمعدل نمو قدره 62.6%. وبالتالي، يُسهم التركيز المتزايد على توسيع خطوط أنابيب وشبكات النفط والغاز في نمو سوق تجديد الأنابيب.

التركيز الحكومي المتزايد على إدارة مياه الصرف الصحي والتحديثات في البنية التحتية للصرف الصحي

نظراً لمخاوف السلامة العامة وندرة المياه النظيفة في مختلف البلدان، تُوظّف حكومات هذه الدول استثماراتٍ ضخمةً في تطوير بنيةٍ تحتيةٍ سليمةٍ للصرف الصحي ومرافقٍ لإدارة مياه الصرف الصحي. ولأنظمة الصرف الصحي السليمة فوائدٌ عديدة، منها تحسين جودة الحياة وظروف النظافة، والحفاظ على البيئة الطبيعية، وتوفير المياه ومعالجتها، والتنمية الاقتصادية، والحد من مخاطر الأضرار الناجمة عن الفيضانات، وتحسين مستوى المعيشة. ولتحقيق ذلك، تُوظّف حكومات مختلف الاقتصادات استثماراتٍ ضخمةً في تطوير بنيةٍ تحتيةٍ جديدةٍ للصرف الصحي وتحديث البنية التحتية القديمة.

على سبيل المثال، في يناير 2024، تلقت ولاية ماساتشوستس الأمريكية أكثر من 260 مليون دولار أمريكي لتطوير البنية التحتية للمياه والصرف الصحي. وفي عام 2023، تلقت مدينة هافرهيل الأمريكية أكثر من 12.8 مليون دولار أمريكي لتطوير أنظمة المياه والصرف الصحي. وفي عام 2023، أطلقت هيئة مياه ولاية كيرالا ومؤسسة المدينة مشروعًا للاستفادة من محطات معالجة مياه الصرف الصحي اللامركزية اليابانية المعروفة باسم "جوكاسو" في المدينة. وفي سبتمبر 2021، وافقت لجنة النقل والبنية التحتية في مجلس النواب على استثمار قدره 50 مليار دولار أمريكي يُخصص حتى عام 2026 لإدارة مياه الصرف الصحي ومكافحة الفيضانات وغيرها من البنى التحتية المتعلقة بالمياه. وفي عام 2023، تعاونت اللجنة الشعبية لمدينة بون هو مع الوكالة الكورية للتعاون الدولي (KOICA) للتخطيط لتنفيذ نظام الصرف الصحي الحضري ومعالجة مياه الصرف الصحي في مدينة بون هو. في عام ٢٠٢٤، وقّعت حكومتا جنوب أفريقيا وزيمبابوي اتفاقيةً ركّزت على نجاح نقل المياه المُنقّاة من محطة بيتبريدج لمعالجة المياه إلى موسينا. وفي عام ٢٠٢٣، أعلنت حكومة المملكة العربية السعودية عن خطة لاستثمار ١٤.٥٨ مليار دولار أمريكي في مشاريع جارية ومخطط لها لنقل المياه، وتحلية المياه، والخزانات الاستراتيجية، ومعالجة مياه الصرف الصحي، بالإضافة إلى استثمار عدد من المشاريع. ومن المتوقع أن تُؤثّر هذه المبادرات الحكومية إيجابًا على سوق إعادة تبطين الأنابيب.

تقرير تحليل تجزئة سوق إعادة تبطين الأنابيب

القطاعات الرئيسية التي ساهمت في استنتاج تحليل سوق إعادة تبطين الأنابيب هي الحل (المنتج والخدمة) والمستخدم النهائي

- من حيث الحلول، يُصنّف السوق إلى منتج وخدمة. وسيُهيمن قطاع الخدمات على السوق بحلول عام ٢٠٢٤.

- يُصنف السوق حسب المنتجات إلى معدات CIPP، والبطانة، ونفاثات المياه عالية الضغط، وأسطوانة الانعكاس، وآلة السحب، وغيرها. وقد هيمن قطاع معدات CIPP على السوق في عام 2024.

- بناءً على الخدمات، يُقسّم السوق إلى أنابيب مُعالجة في الموقع، وأنابيب سحب في الموقع، وأنابيب تفجير، وطلاء داخلي للأنابيب. هيمن قطاع الأنابيب المُعالجة في الموقع على السوق في عام ٢٠٢٤. ويُصنّف السوق، بحسب نوع الأنابيب المُعالجة في الموقع، إلى إصلاحات رقعة أو بقعية، وإصلاحات بطانة أو إصلاحات أطول. هيمن قطاع الأنابيب المُعالجة في الموقع على السوق في عام ٢٠٢٤.

- من حيث طرق المعالجة، يُصنف السوق إلى: المعالجة في البيئة المحيطة، والمعالجة بالماء الساخن، والمعالجة بالبخار، والمعالجة بالأشعة فوق البنفسجية. وقد هيمن قطاع المعالجة بالماء الساخن على السوق في عام ٢٠٢٤.

- بناءً على المستخدم النهائي، يُقسّم السوق إلى قطاعات النفط والغاز، والمواد الكيميائية، والقطاعات البلدية، وغيرها. وسيُهيمن قطاع النفط والغاز على السوق بحلول عام ٢٠٢٤.

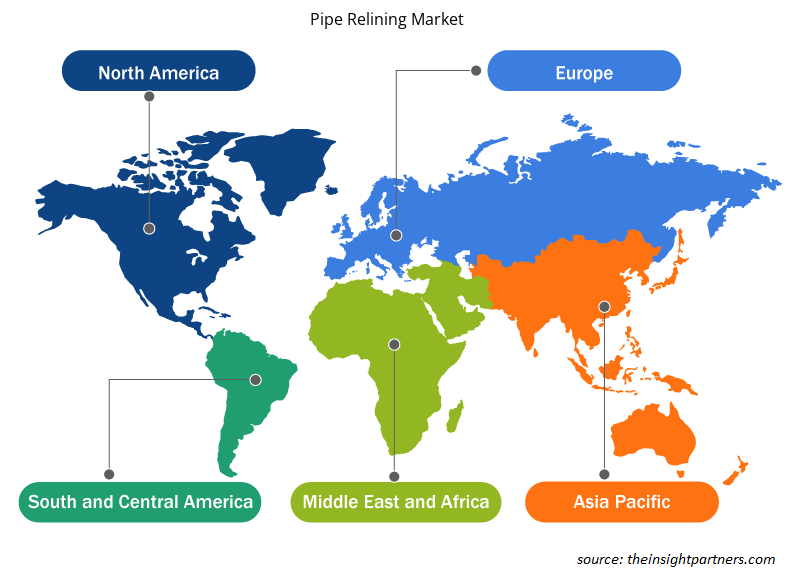

تحليل حصة سوق إعادة تبطين الأنابيب حسب المنطقة الجغرافية

يُقسّم سوق إعادة تبطين الأنابيب إلى خمس مناطق رئيسية: أمريكا الشمالية، وأوروبا، وآسيا والمحيط الهادئ، والشرق الأوسط وأفريقيا، وأمريكا الجنوبية والوسطى. وقد هيمنت أمريكا الشمالية على السوق في عام 2024، تلتها آسيا والمحيط الهادئ وأوروبا.

ينقسم سوق إعادة تبطين الأنابيب في أمريكا الشمالية إلى الولايات المتحدة الأمريكية وكندا والمكسيك. وتتمتع الولايات المتحدة بمكانة واعدة في السوق بفضل التطورات المستمرة في قطاعات النفط والغاز وإدارة المياه والصرف الصحي. ويؤدي تركيب أنابيب الصرف الصحي ومرافق معالجة مياه الصرف الصحي إلى زيادة الطلب على أعمال الصيانة. ويُعد ضمان إمدادات المياه الكافية والصرف الصحي السليم عنصرين أساسيين في البنية التحتية المتطورة لشبكات الصرف الصحي. ويتطلب تطوير البنى التحتية الجديدة، بما في ذلك الجامعات والمدارس والمكاتب التجارية والمساكن، مستوى عاليًا من أعمال إعادة تبطين الأنابيب لضمان تصريف فعال. في مارس 2024، أعلنت وزارة الزراعة الأمريكية للتنمية الريفية عن تخصيص 16.9 مليون دولار أمريكي لمشاريع تطوير المياه والصرف الصحي في ريف ميشيغان. وفي أبريل 2024، أعلنت الحكومة الأمريكية عن تخصيص 320 مليون دولار أمريكي لتطوير البنية التحتية للمياه المنزلية القبلية. وتعمل مبادرات التمويل الفيدرالية المختلفة على تعزيز البنية التحتية لمعالجة مياه الصرف الصحي في الولايات المتحدة. وقد صرف قانون تمويل وابتكار البنية التحتية للمياه بالفعل 8 مليارات دولار أمريكي كقروض لـ 42 مشروعًا للبنية التحتية لمياه الصرف الصحي.

خصص قانون البنية التحتية المشترك بين الحزبين 11.71 مليار دولار أمريكي من خلال صندوق المياه النظيفة الحكومي الدوار في عام 2023. علاوة على ذلك، تُعد توسعة محطة معالجة مياه الصرف الصحي في والنات كريك إلى 100 مليون جالون يوميًا، ومحطة وايتس كريك لمعالجة مياه الصرف الصحي، وتوسعة منشأة استصلاح المياه الجنوبية الغربية إلى 18 مليون جالون يوميًا، وتوسعة منشأة استصلاح المياه، وتوسعة منشأة استصلاح المياه - المرحلة الثانية، من بين مشاريع معالجة مياه الصرف الصحي المستقبلية في الولايات المتحدة. ومن المتوقع أن يؤدي العدد المتزايد من مرافق معالجة المياه ومياه الصرف الصحي ومشاريع البنية التحتية للصرف الصحي إلى زيادة الطلب على أنشطة إعادة تبطين الأنابيب خلال فترة التوقعات.

رؤى إقليمية حول سوق إعادة تبطين الأنابيب

قام محللو إنسايت بارتنرز بشرح شامل للاتجاهات والعوامل الإقليمية المؤثرة في سوق إعادة تبطين الأنابيب خلال فترة التوقعات. ويناقش هذا القسم أيضًا قطاعات سوق إعادة تبطين الأنابيب ونطاقه الجغرافي في أمريكا الشمالية، وأوروبا، وآسيا والمحيط الهادئ، والشرق الأوسط وأفريقيا، وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق إعادة تبطين الأنابيب

نطاق تقرير سوق إعادة تبطين الأنابيب

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2024 | 9,267.61 مليون دولار أمريكي |

| حجم السوق بحلول عام 2031 | 13,093.73 مليون دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2025 - 2031) | 5.3% |

| البيانات التاريخية | 2021-2023 |

| فترة التنبؤ | 2025-2031 |

| القطاعات المغطاة | حسب الحل

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق إعادة تبطين الأنابيب: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق إعادة تبطين الأنابيب نموًا سريعًا، مدفوعًا بتزايد طلب المستخدمين النهائيين نتيجةً لعوامل مثل تطور تفضيلات المستهلكين، والتقدم التكنولوجي، وزيادة الوعي بمزايا المنتج. ومع تزايد الطلب، تعمل الشركات على توسيع عروضها، والابتكار لتلبية احتياجات المستهلكين، والاستفادة من الاتجاهات الناشئة، مما يُعزز نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات العاملة في سوق أو قطاع معين. وتشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في سوق معين نسبةً إلى حجمه أو قيمته السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق إعادة تبطين الأنابيب هي:

- شركة تقنيات تجديد خطوط المياه

- مجموعة روتو روتر المحدودة

- شركة الحلول المتقدمة للحفر الخندق ذ.م.م

- شركة سيكيسوي الكيميائية المحدودة

- شركة إيجيون

- شركة سيلفرلاينينج القابضة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق إعادة تبطين الأنابيب

أخبار سوق إعادة تبطين الأنابيب والتطورات الأخيرة

يُقيّم سوق إعادة تبطين الأنابيب بجمع بيانات نوعية وكمية بعد البحث الأولي والثانوي، والتي تشمل منشورات الشركات المهمة، وبيانات الجمعيات، وقواعد البيانات. فيما يلي بعض التطورات الرئيسية في سوق إعادة تبطين الأنابيب:

- وقّعت مجموعة تريليبورغ، من خلال قسم حلول تريليبورغ الصناعية التابع لها، اتفاقية للاستحواذ على شركة NuFlow Technologies، المتخصصة في إصلاح الأنابيب ومقرها الولايات المتحدة. (المصدر: مجموعة تريليبورغ، بيان صحفي، فبراير 2025)

- قدمت شركة فورتكس مجموعتها الجديدة والشاملة من حلول أنظمة معالجة CIPP بالأشعة فوق البنفسجية. تُمكّن أنظمة معدات معالجة CIPP بالأشعة فوق البنفسجية من فورتكس، والبطانات، وشاحنات البناء المُخصصة، المدعومة بتدريب ودعم من خبراء، الشركة من أن تكون شريكًا قيّمًا في إعادة تأهيل البنية التحتية القديمة. (المصدر: فورتكس، بيان صحفي، فبراير 2023)

تغطية تقرير سوق إعادة تبطين الأنابيب والنتائج المتوقعة

يوفر تقرير "حجم سوق إعادة تبطين الأنابيب والتوقعات (2021-2031)" تحليلاً مفصلاً للسوق يغطي المجالات المذكورة أدناه:

- حجم سوق إعادة تبطين الأنابيب وتوقعاته على المستويات العالمية والإقليمية والوطنية لجميع قطاعات السوق الرئيسية التي يغطيها النطاق

- اتجاهات سوق إعادة تبطين الأنابيب، بالإضافة إلى ديناميكيات السوق مثل العوامل المحركة والقيود والفرص الرئيسية

- تحليل مفصل لـ PEST و SWOT

- تحليل سوق إعادة تبطين الأنابيب يغطي اتجاهات السوق الرئيسية والإطار العالمي والإقليمي والجهات الفاعلة الرئيسية واللوائح والتطورات الأخيرة في السوق

- تحليل المشهد الصناعي والمنافسة الذي يغطي تركيز السوق، وتحليل خريطة الحرارة، واللاعبين البارزين، والتطورات الأخيرة لسوق إعادة تبطين الأنابيب

- ملفات تعريف الشركة التفصيلية

نيفيديتا خبيرة أبحاث مُتميزة، تتمتع بخبرة تزيد عن 9 سنوات في أبحاث السوق واستشارات الأعمال. تشغل حاليًا منصب مديرة مشاريع في مجال تكنولوجيا المعلومات والاتصالات لدى شركة "ذا إنسايت بارتنرز"، وتتمتع بخبرة واسعة في إدارة وتنفيذ مهام الأبحاث المُجمعة والمُخصصة والقائمة على الاشتراكات والاستشارات في مختلف قطاعات التكنولوجيا.

بفضل سجلها الحافل في تقديم تحليلات قائمة على البيانات ورؤى عملية، ساهمت نيفيديتا بشكل رئيسي في العديد من المشاريع الحيوية. يشمل عملها تنفيذ المشاريع من البداية إلى النهاية، بدءًا من فهم أهداف العملاء، وتحليل اتجاهات السوق، وصولًا إلى استخلاص التوصيات الاستراتيجية. وقد تعاونت على نطاق واسع مع شركات رائدة في مجال تكنولوجيا المعلومات والاتصالات، مما ساعدها على تحديد فرص السوق ومواكبة تحولات القطاع.

تحمل نيفيديتا ماجستير إدارة أعمال في الإدارة من شركة "آي إم إس" في دهرادون. قبل انضمامها إلى "ذا إنسايت بارتنرز"، اكتسبت خبرة قيّمة في شركتي "ماركتس آند ماركتس" و"فيوتشر ماركت إنسايتس" في بونا، حيث شغلت مناصب بحثية مُختلفة وبنت أساسًا قويًا في تحليل القطاع والتفاعل مع العملاء.

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق إعادة تبطين الأنابيب

احصل على عينة مجانية ل - سوق إعادة تبطين الأنابيب