تحليل وتوقعات سوق خدمات ركوب الخيل حسب الحجم والمشاركة والنمو والاتجاهات 2031

البيانات التاريخية : 2021-2022 | سنة الأساس : 2023 | فترة التنبؤ : 2023-2031حجم سوق خدمات نقل الركاب وتوقعاته (2021-2031)، والحصة العالمية والإقليمية، والاتجاهات، وفرص النمو. يغطي التقرير: حسب نوع الخدمة (النقل الإلكتروني، ومشاركة السيارات، وتأجير السيارات، والتنقل داخل المحطة)، ونوع المركبة (ذات عجلتين، وثلاث عجلات، وأربع عجلات، وغيرها)، والموقع (حضري وريفي)، والمستخدم النهائي (مؤسسي وشخصي)، والموقع الجغرافي.

- تاريخ التقرير : Mar 2026

- رمز التقرير : TIPRE00004789

- الفئة : السيارات والنقل

- الحالة : البيانات الصادرة

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 150

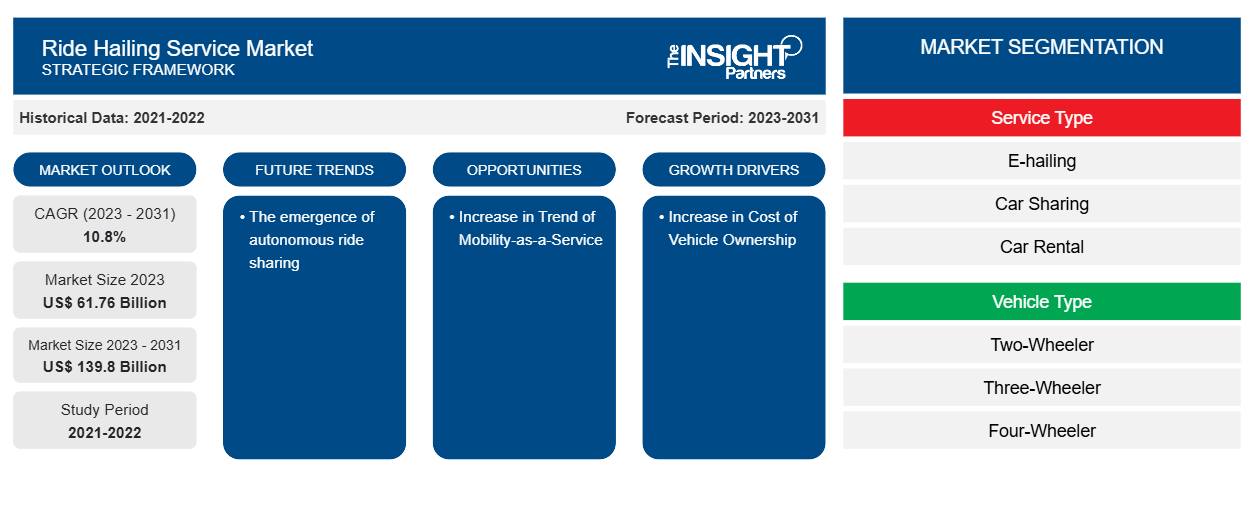

من المتوقع أن يصل حجم سوق خدمات النقل بالسيارات إلى 139.8 مليار دولار أمريكي بحلول عام 2031 من 61.76 مليار دولار أمريكي في عام 2023. ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب بنسبة 10.8٪ خلال الفترة 2023-2031. ومن المرجح أن يظل ظهور خدمة مشاركة الرحلات ذاتية القيادة اتجاهًا رئيسيًا في السوق.

تحليل سوق خدمات النقل التشاركي

من المتوقع أن يؤدي ارتفاع اتجاه خدمات النقل حسب الطلب في جميع أنحاء العالم إلى دفع نمو السوق في السنوات القادمة. بالإضافة إلى ذلك، من المتوقع أن يؤدي ارتفاع تكلفة امتلاك المركبات إلى زيادة الطلب على خدمات نقل الركاب خلال فترة التوقعات. علاوة على ذلك، من المتوقع أن يؤدي ارتفاع اتجاه التنقل كخدمة في جميع أنحاء العالم إلى دفع نمو سوق خدمات نقل الركاب من عام 2023 إلى عام 2031.

نظرة عامة على سوق خدمات النقل التشاركي

تشمل الجهات المعنية الرئيسية في منظومة سوق خدمات النقل بالسيارات مقدمي حلول التكنولوجيا ومقدمي خدمات النقل بالسيارات والمستخدمين النهائيين. يشمل مقدمو حلول التكنولوجيا الأجهزة المتصلة أو غيرها من الشركات المصنعة للأجهزة ومطوري البرامج. إن الزيادة في عدد مقدمي حلول التكنولوجيا تدفع بشكل حاسم إلى التحول الرقمي في خدمات النقل بالسيارات. ومن المتوقع أن تزيد خدمات النقل بالسيارات بعد كوفيد بسبب الاتجاه المتزايد لخدمات النقل عند الطلب، وخلق فرص العمل، وانخفاض معدل ملكية السيارات بين جيل الألفية. بالإضافة إلى ذلك، فإن التقدم التكنولوجي في المركبات المتصلة والأوتوماتيكية للحد من انبعاثات ثاني أكسيد الكربون والزيادات الكبيرة في مبيعات هذه المركبات الذكية والفعالة لاستخدام خدمات النقل بالسيارات تدفع نمو السوق العالمية. يأخذ مقدمو خدمات النقل بالسيارات الخدمات من مقدمي حلول التكنولوجيا. مع التطورات التكنولوجية المتزايدة في خدمات النقل بالسيارات، يتزايد الطلب على سوق خدمات النقل بالسيارات.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق خدمات النقل التشاركي: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محركات وفرص سوق خدمات النقل التشاركي

ارتفاع تكلفة امتلاك المركبات لصالح السوق

تساهم التمويل والوقود والصيانة والتسجيل/الضرائب والصيانة، فضلاً عن الاستهلاك، في تكلفة امتلاك السيارة. تزداد تكلفة امتلاك السيارة عامًا بعد عام. ويمثل الاستهلاك أكثر من 43٪ من إجمالي تكلفة الملكية، وفقًا لجمعية السيارات الأمريكية (AAA). ومع ذلك، فإن التكاليف الأخرى، مثل الصيانة والبنزين ، تمثل 25٪. زادت أسعار الوقود وتكاليف الصيانة بشكل كبير في السنوات العشر الماضية ومن المتوقع أن تزيد في السنوات القادمة. وعلى الرغم من زيادة ملكية السيارات أثناء الوباء، فمن المتوقع أن تنخفض بعد عام 2021 وتعود إلى مستويات ما قبل الوباء. وهذا يسمح لمقدمي خدمات نقل الركاب بالاستفادة من هذا التطور الديموغرافي، حيث يعد الجيل الجديد المتمرس في التكنولوجيا من بين المستخدمين الأكثر نشاطًا لهذه الخدمات.pre-pandemic levels. This allows ride-hailing providers to benefit from this demographic development, as the new technology-savvy generation is among the most active users of these services.

زيادة في اتجاه التنقل كخدمة

يمكن للعملاء غير القادرين على شراء السيارة تجربة سفر سلس من خلال خدمات التنقل. تعمل خدمة التنقل كخدمة على تقليل تكلفة التملك والتشغيل من خلال تعظيم تكلفة مشاركة السيارات وطلب الركوب. بالإضافة إلى ذلك، فإن الوتيرة السريعة للتحضر تؤدي بالفعل إلى ازدحام مروري. قد يكون مفهوم خدمة التنقل (MaaS) خيارًا أفضل لتقليل الازدحام المروري من خلال الاستخدام الأكبر لشبكة النقل العام والخاص الحالية. الطلب العاجل والمتزايد على حلول فعالة للتعامل مع حركة المرور في المدن الذكية والذي بدوره من المتوقع أن يغذي نمو سوق خدمة طلب الركوب حتى عام 2031. لذلك، من المتوقع أن يؤدي الاتجاه المتزايد للتنقل كخدمة (MaaS) إلى تغذية نمو سوق خدمة طلب الركوب العالمية.MaaS) concept may be a better choice for minimizing traffic congestion by greater use of existing public and private transportation network. The urgent and increased demand for effective solutions to handle traffic in smart cities which in turn is expected to fuel ride hailing service market growth through 2031. Therefore, the increasing trend of mobility as a Service (MaaS) is expected to fuel the growth of the global ride-hailing service market.

تقرير تحليلي لتجزئة سوق خدمات النقل التشاركي

القطاعات الرئيسية التي ساهمت في استنباط تحليل سوق خدمات النقل التشاركي هي نوع الخدمة، ونوع السيارة، والموقع، والمستخدم النهائي

- بناءً على نوع الخدمة، ينقسم سوق خدمات النقل بالسيارات إلى خدمات النقل الإلكتروني ومشاركة السيارات وتأجير السيارات والتنقل عبر المحطات. وقد احتل قطاع النقل بالسيارات الإلكتروني أكبر حصة سوقية في عام 2023.

- بحسب نوع المركبة، يتم تقسيم السوق إلى مركبات ذات عجلتين، ومركبات ذات ثلاث عجلات، ومركبات ذات أربع عجلات، وغيرها. وقد استحوذت فئة المركبات ذات الأربع عجلات على أكبر حصة من السوق في عام 2023.

- على أساس الموقع، ينقسم السوق إلى حضري وريفي. وقد استحوذ القطاع الحضري على حصة كبيرة من السوق في عام 2023.

- بحسب المستخدم النهائي، يتم تقسيم السوق إلى مؤسسي وشخصي. احتل القطاع المؤسسي الحصة الأكبر من السوق في عام 2023.

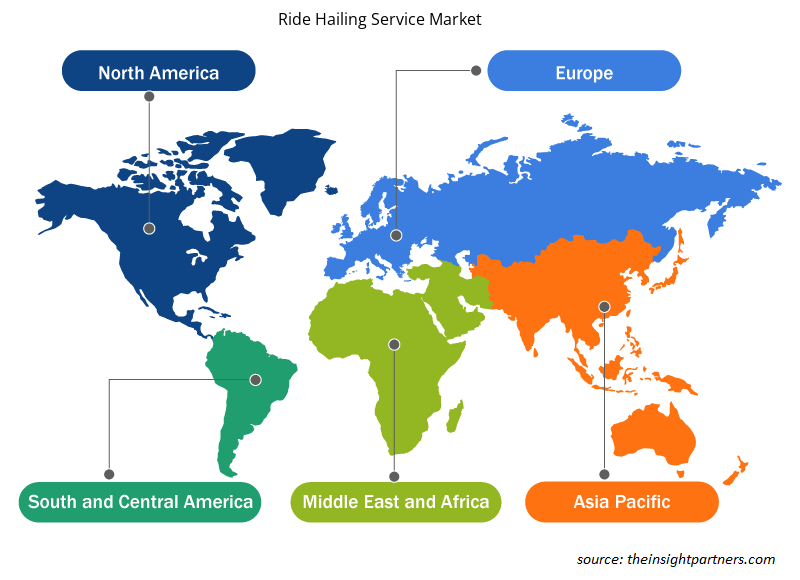

تحليل حصة سوق خدمات النقل التشاركي حسب المنطقة الجغرافية

ينقسم النطاق الجغرافي لتقرير سوق خدمات نقل الركاب بشكل أساسي إلى خمس مناطق: أمريكا الشمالية، وآسيا والمحيط الهادئ، وأوروبا، والشرق الأوسط وأفريقيا، وأمريكا الجنوبية.

يشمل نطاق تقرير سوق خدمات نقل الركاب أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك) وأوروبا (ألمانيا وفرنسا وإيطاليا وإسبانيا والمملكة المتحدة وبقية أوروبا) وآسيا والمحيط الهادئ (الصين والهند وأستراليا واليابان وكوريا الجنوبية وبقية آسيا والمحيط الهادئ) والشرق الأوسط وأفريقيا (جنوب أفريقيا والمملكة العربية السعودية والإمارات العربية المتحدة وبقية الشرق الأوسط وأفريقيا) وأمريكا الجنوبية (البرازيل والأرجنتين وبقية أمريكا الجنوبية). من حيث الإيرادات، سيطرت منطقة آسيا والمحيط الهادئ على حصة سوق خدمات نقل الركاب في عام 2023. كانت أمريكا الشمالية ثاني أكبر مساهم في الإيرادات في سوق خدمات نقل الركاب العالمية، تليها أوروبا.

نظرة إقليمية على سوق خدمات النقل التشاركي

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق خدمات النقل عبر الإنترنت طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق خدمات النقل عبر الإنترنت والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق خدمات النقل التشاركي

نطاق تقرير سوق خدمات النقل التشاركي

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2023 | 61.76 مليار دولار أمريكي |

| حجم السوق بحلول عام 2031 | 139.8 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2023 - 2031) | 10.8% |

| البيانات التاريخية | 2021-2022 |

| فترة التنبؤ | 2023-2031 |

| القطاعات المغطاة |

حسب نوع الخدمة

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق خدمات النقل التشاركي: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق خدمات النقل الجماعي نموًا سريعًا، مدفوعًا بالطلب المتزايد من جانب المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق خدمات النقل التشاركي هي:

- شركة أني تكنولوجيز الخاصة المحدودة

- شركة دايملر ايه جي

- شركة دلفي للتكنولوجيا

- شركة ديدي العالمية

- جيت

- شركة جراب القابضة المحدودة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق خدمات النقل

أخبار سوق خدمات النقل التشاركي والتطورات الأخيرة

يتم تقييم سوق خدمات النقل بالسيارات من خلال جمع البيانات النوعية والكمية بعد البحث الأولي والثانوي، والتي تتضمن منشورات الشركات المهمة وبيانات الجمعيات وقواعد البيانات. فيما يلي بعض التطورات في سوق خدمات النقل بالسيارات:

- قامت شركة Kakao Mobility، وهي شركة تقدم خدمات النقل التشاركي، بتوسيع حضورها من خلال إطلاق خدمات النقل التشاركي في آسيا والشرق الأوسط. (المصدر: Kakao Mobility، بيان صحفي، نوفمبر 2023)

- بدأت شركة DiDi Global Inc. عملية تسجيل السائقين في مدينة كيب تاون بجنوب أفريقيا، وبدأت في تقديم خدمات النقل التشاركي للمستهلكين في ثاني أكبر مدينة في البلاد. (المصدر: DiDi Global Inc.، بيان صحفي، مارس 2021)

تقرير سوق خدمات النقل التشاركي: التغطية والنتائج المتوقعة

يوفر تقرير "حجم سوق خدمات النقل التشاركي والتوقعات (2021-2031)" تحليلاً مفصلاً للسوق يغطي المجالات التالية:

- حجم سوق خدمات النقل التشاركي وتوقعاته على المستويات العالمية والإقليمية والوطنية لجميع قطاعات السوق الرئيسية التي يغطيها النطاق

- اتجاهات سوق خدمات النقل التشاركي بالإضافة إلى ديناميكيات السوق مثل السائقين والقيود والفرص الرئيسية

- تحليل مفصل لـ PEST و SWOT

- تحليل سوق خدمات النقل التشاركي الذي يغطي اتجاهات السوق الرئيسية والإطار العالمي والإقليمي والجهات الفاعلة الرئيسية واللوائح والتطورات الأخيرة في السوق

- تحليل المشهد الصناعي والمنافسة الذي يغطي تركيز السوق، وتحليل خريطة الحرارة، واللاعبين البارزين، والتطورات الأخيرة لسوق خدمة نقل الركاب

- ملفات تعريف الشركة التفصيلية

نافين خبيرٌ متمرسٌ في أبحاث السوق والاستشارات، يتمتع بخبرةٍ تزيد عن 9 سنوات في مشاريع مُخصصة ومُشتركة واستشارية. يشغل حاليًا منصب نائب الرئيس المساعد، وقد نجح في إدارة أصحاب المصلحة عبر سلسلة قيمة المشاريع، وألّف أكثر من 100 تقرير بحثي وأكثر من 30 مهمة استشارية. يمتد نطاق عمله ليشمل مشاريع صناعية وحكومية، مساهمًا بشكل كبير في نجاح العملاء واتخاذ القرارات القائمة على البيانات.

نافين حاصلٌ على شهادة في هندسة الإلكترونيات والاتصالات من جامعة فرجينيا التقنية، كارناتاكا، وشهادة ماجستير في إدارة الأعمال في التسويق والعمليات من جامعة مانيبال. وهو عضوٌ نشطٌ في معهد مهندسي الكهرباء والإلكترونيات (IEEE) لمدة 9 سنوات، حيث شارك في مؤتمراتٍ وندواتٍ تقنية، وتطوّع على مستوى الأقسام والمناطق. قبل منصبه الحالي، عمل مستشارًا استراتيجيًا مساعدًا في IndustryARC، ومستشارًا للخوادم الصناعية في شركة هيوليت باكارد (HP Global).

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق خدمات نقل الركاب

احصل على عينة مجانية ل - سوق خدمات نقل الركاب