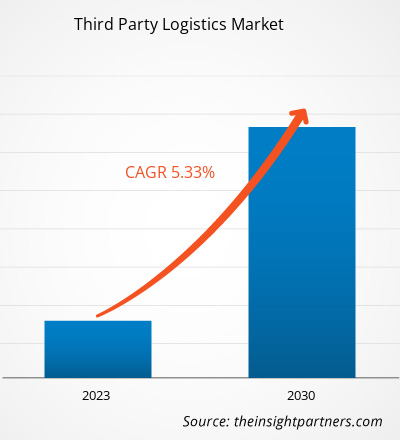

بلغت قيمة سوق الخدمات اللوجستية لطرف ثالث 1273.1 مليار دولار أمريكي في عام 2022، ومن المتوقع أن تصل إلى 1929.18 مليار دولار أمريكي بحلول عام 2030؛ ومن المتوقع أن تسجل معدل نمو سنوي مركب بنسبة 5.33٪ خلال الفترة 2022-2030.

ومن المرجح أن يظل الانتشار المتزايد للتجارة الإلكترونية يمثل اتجاها رئيسيا في السوق.

تحليل سوق الخدمات اللوجستية للطرف الثالث

إن صعود التجارة الإلكترونية والرغبة في التسليم في نفس اليوم أو اليوم التالي يدفعان الطلب على خدمات التوصيل في الميل الأخير. على سبيل المثال، وضعت خدمة Amazon Prime معايير جديدة للتسليم السريع، مما دفع شركات الخدمات اللوجستية الخارجية إلى تكييف خدماتها لتلبية هذه التوقعات. أدى الوعي المتزايد بالقضايا البيئية والاستدامة إلى زيادة الطلب على حلول الخدمات اللوجستية الصديقة للبيئة. يتبنى مزودو الخدمات اللوجستية الخارجية المركبات الكهربائية، ويحسنون الطرق لتقليل الانبعاثات، وينفذون ممارسات التعبئة والتغليف المستدامة بما يتماشى مع توقعات المستهلكين والجهات التنظيمية.

نظرة عامة على سوق الخدمات اللوجستية للطرف الثالث

يعد نقل السلع المصنعة من المصانع إلى المستودعات المرحلة الأولى في عملية الطرف الثالث للخدمات اللوجستية. تقوم شركة الطرف الثالث للخدمات اللوجستية بتخزين المنتج بمجرد وصوله إلى المستودع أو مركز التنفيذ. يتم تخزين المنتجات وفقًا لـ SKU الخاصة بها، حيث يكون لكل SKU مكان تخزين مخصص خاص به. يتم إدخال العناصر التي تدخل المستودع عادةً في نظام التتبع الخاص بالمزود في هذه المرحلة. يساعد تكامل البرامج في العمليات الفعّالة والناجعة.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق الخدمات اللوجستية للجهات الخارجية:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محركات وفرص سوق الخدمات اللوجستية للجهات الخارجية

فوائد إدارة التغيرات الموسمية للمنتجات لصالح السوق

لقد قامت شركات الخدمات اللوجستية الخارجية بتوسيع شبكات الموارد التي تدعم الشركات الرئيسية للتوسع بكفاءة وبطريقة فعالة من حيث التكلفة. بالإضافة إلى ذلك، يمكن لشركات الخدمات اللوجستية الخارجية تقديم موارد كافية ومرونة في الخدمات للمخزون الموسمي أو إصدارات المنتجات الجديدة. تشهد العديد من المؤسسات اختلافات موسمية في ميول العملاء، ويصبح من الضروري إدارة مثل هذه التقلبات للحفاظ على الفعالية وتلبية الطلب.

تطبيق حلول البرمجيات وتبني تحليلات البيانات الضخمة

ومن المتوقع أيضًا أن يؤدي تبني الأجهزة التي تدعم تقنية تحديد الهوية بموجات الراديو إلى تخزين البيانات لتسهيل النقل، الأمر الذي من شأنه أيضًا تبسيط تتبع المنتجات وتحديد هويتها. كما ستعمل البرامج المتعلقة بأنظمة إدارة النقل على الحد من عدم الكفاءة والتكاليف. وعلاوة على ذلك، فإن استخدام برامج التعرف على الكلام في اتصالات أنظمة إدارة المستودعات سيساعد في إنجاز الطلبات وتسجيل المخزون مع خفض احتياجات تدريب الموظفين. جنبًا إلى جنب مع هذا، فإن قبول التكنولوجيا المستندة إلى السحابة في منظمات الخدمات اللوجستية التابعة لجهات خارجية سيستجيب للمطالب من خلال الاعتراف بالحاجة إلى وصول العميل، مما يسمح لهم بمعالجة الاتجاهات الموسمية بشكل أفضل.

تقرير تحليل تجزئة سوق الخدمات اللوجستية للطرف الثالث

إن القطاعات الرئيسية التي ساهمت في استنتاج تحليل سوق الخدمات اللوجستية لطرف ثالث هي طريقة النقل والخدمات والمستخدمين النهائيين.

- بناءً على وسيلة النقل، ينقسم سوق الخدمات اللوجستية للطرف الثالث إلى الطرق والسكك الحديدية والممرات المائية والطرق الجوية. احتل قطاع الطرق حصة سوقية أكبر في عام 2023.

- بناءً على الخدمات، ينقسم سوق الخدمات اللوجستية للجهات الخارجية إلى النقل الدولي والتخزين والنقل المحلي وإدارة المخزون وغيرها. احتل قطاع النقل المحلي حصة سوقية أكبر في عام 2023.

- بناءً على المستخدمين النهائيين، يتم تقسيم سوق الخدمات اللوجستية للجهات الخارجية إلى السيارات والرعاية الصحية والتجزئة والسلع الاستهلاكية والآخرون. احتفظت شريحة الآخرين بحصة سوقية أكبر في عام 2023.

تحليل حصة سوق الخدمات اللوجستية للجهات الخارجية حسب المنطقة الجغرافية

ينقسم النطاق الجغرافي لتقرير سوق الخدمات اللوجستية لطرف ثالث بشكل أساسي إلى خمس مناطق: أمريكا الشمالية، ومنطقة آسيا والمحيط الهادئ، وأوروبا، والشرق الأوسط وأفريقيا، وأمريكا الجنوبية والوسطى.

يشمل نطاق تقرير سوق الخدمات اللوجستية لأطراف ثالثة أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك) وأوروبا (روسيا والمملكة المتحدة وفرنسا وألمانيا وإيطاليا وبقية أوروبا) ومنطقة آسيا والمحيط الهادئ (كوريا الجنوبية والهند وأستراليا واليابان والصين وبقية منطقة آسيا والمحيط الهادئ) والشرق الأوسط وأفريقيا (المملكة العربية السعودية وجنوب إفريقيا والإمارات العربية المتحدة وبقية منطقة الشرق الأوسط وأفريقيا) وأمريكا الجنوبية والوسطى (الأرجنتين والبرازيل وبقية أمريكا الجنوبية والوسطى). من حيث الإيرادات، سيطرت منطقة آسيا والمحيط الهادئ على حصة سوق الخدمات اللوجستية لأطراف ثالثة في عام 2023. تعد أوروبا ثاني أكبر مساهم في سوق الخدمات اللوجستية لأطراف ثالثة العالمية، تليها أمريكا الشمالية.

رؤى إقليمية حول سوق الخدمات اللوجستية لطرف ثالث

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق الخدمات اللوجستية للجهات الخارجية طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق الخدمات اللوجستية للجهات الخارجية والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق الخدمات اللوجستية للجهات الخارجية

نطاق تقرير سوق الخدمات اللوجستية للطرف الثالث

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 1273.1 مليار دولار أمريكي |

| حجم السوق بحلول عام 2030 | 1929.18 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2030) | 5.33% |

| البيانات التاريخية | 2020-2021 |

| فترة التنبؤ | 2023-2030 |

| القطاعات المغطاة | حسب وسيلة النقل

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

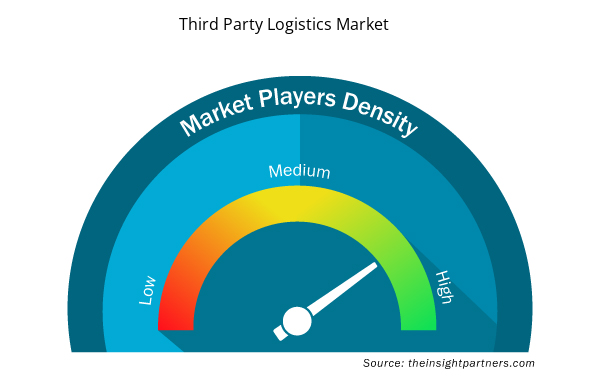

كثافة اللاعبين في السوق: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق الخدمات اللوجستية للجهات الخارجية نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق الخدمات اللوجستية لطرف ثالث هي:

- سيفا للخدمات اللوجستية

- فيديكس

- المُرسِلون

- لوجستيات سان فرانسيسكو

- ميرسك للخدمات اللوجستية

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق الخدمات اللوجستية للطرف الثالث

أخبار سوق الخدمات اللوجستية للجهات الخارجية والتطورات الأخيرة

يتم تقييم سوق الخدمات اللوجستية للطرف الثالث من خلال جمع البيانات النوعية والكمية بعد البحث الأولي والثانوي، والذي يتضمن منشورات الشركات المهمة وبيانات الجمعيات وقواعد البيانات. فيما يلي بعض التطورات في سوق الخدمات اللوجستية للطرف الثالث:

- أعلنت شركة دي بي شينكر، إحدى شركات تقديم الخدمات اللوجستية الرائدة في العالم، وشركة يو إس إيه تراك، وهي شركة رائدة في تقديم حلول السعة، عن اتفاق تستحوذ بموجبه شركة دي بي شينكر على جميع الأسهم المتداولة لشركة يو إس إيه تراك مقابل 31.72 دولارًا أمريكيًا للسهم نقدًا. وتكلف الصفقة شركة يو إس إيه تراك ما يقرب من 435 مليون دولار أمريكي، بما في ذلك النقد والديون المفترضة. (المصدر: دي بي شينكر، بيان صحفي، يوليو 2022)

- أعلنت مجموعة دويتشه بوست دي إتش إل، الشركة الرائدة في مجال الخدمات اللوجستية في العالم، اليوم عن تغيير اسم الشركة إلى "مجموعة دي إتش إل" اعتبارًا من 1 يوليو 2023. يعكس الاسم الجديد التحول الذي مرت به المجموعة في السنوات الماضية ويشيد بالتركيز على أنشطتها اللوجستية الوطنية والدولية كمحرك للنمو المستقبلي. (المصدر مجموعة دي إتش إل، بيان صحفي، يوليو 2023)

تقرير سوق الخدمات اللوجستية للجهات الخارجية وتغطية النتائج

يوفر تقرير "حجم سوق الخدمات اللوجستية لطرف ثالث والتوقعات (2020-2030)" تحليلاً مفصلاً للسوق يغطي المجالات التالية:

- حجم سوق الخدمات اللوجستية للطرف الثالث وتوقعاته على المستويات العالمية والإقليمية والوطنية لجميع قطاعات السوق الرئيسية التي يغطيها النطاق

- اتجاهات سوق الخدمات اللوجستية للجهات الخارجية بالإضافة إلى ديناميكيات السوق مثل المحركات والقيود والفرص الرئيسية

- تحليل مفصل لـ PEST و SWOT

- تحليل سوق الخدمات اللوجستية لطرف ثالث يغطي اتجاهات السوق الرئيسية والإطار العالمي والإقليمي والجهات الفاعلة الرئيسية واللوائح والتطورات الأخيرة في السوق

- تحليل المشهد الصناعي والمنافسة الذي يغطي تركيز السوق، وتحليل خريطة الحرارة، واللاعبين البارزين، والتطورات الأخيرة لسوق الخدمات اللوجستية للطرف الثالث

- ملفات تعريف الشركة التفصيلية

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

- Nurse Call Systems Market

- Vision Care Market

- Hummus Market

- Saudi Arabia Drywall Panels Market

- Authentication and Brand Protection Market

- Fertilizer Additives Market

- Single-Use Negative Pressure Wound Therapy Devices Market

- Animal Genetics Market

- Sandwich Panel Market

- Pressure Vessel Composite Materials Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

Asia Pacific dominated the third party logistics market in 2022.

The investment in research & development by manufacturers is the future trend of the third party logistics market.

US$ 1929.18 billion estimated value of the third party logistics market by 2030.

6.6% is the expected CAGR of the third party logistics market.

DHL Group, Kuehne + Nagel International AG, DB Schenker, C.H. Robinson Worldwide Inc., DSV AS, Sinotrans Ltd., Giodis SA, United Parcel Service Inc., XPO Inc., Torello Transpoti Srl are some of the leading players in the market.

The List of Additional Companies - Third party logistics market

- CEVA Logistics

- FedEx

- Expeditors

- SF Logistics

- Maersk Logistics

- Kintetsu World Express

- Yusen Logistics

- Toll Group

- Hellmann Worldwide Logistics

- Penske Logistics

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير