Marktwachstum, Größe, Anteil, Trends, Analyse der wichtigsten Akteure und Prognose für Radiologieinformationssysteme (RIS) bis 2031

Marktgröße und Prognose für Radiologie-Informationssysteme (RIS) (2021 – 2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalyse: Nach Produkt (Standalone-RIS und integriertes RIS), Bereitstellung (webbasiertes RIS, Cloud-basiertes RIS und niedergelassene Ärzte), Komponente (Dienste, Hardware und Software), Endbenutzer (niedergelassene Ärzte, Krankenhäuser und Anbieter von Notfallversorgungsdiensten) und Geografie (Nordamerika, Europa, Asien-Pazifik, Naher Osten und Afrika sowie Süd- und Mittelamerika)

- Status : Veröffentlichte Daten

- Berichtscode : TIPHC00002561

- Kategorie : Technologie, Medien und Telekommunikation

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : February 15, 2025

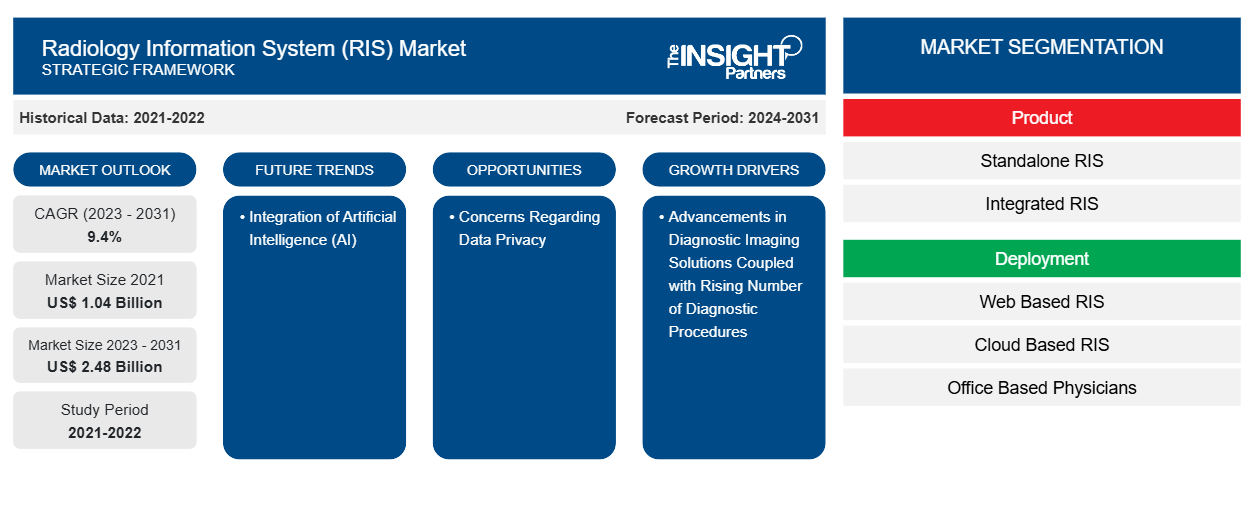

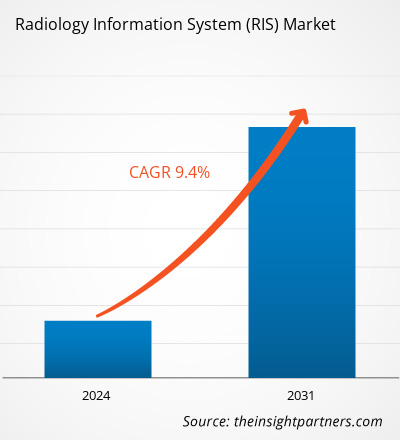

Der Markt für Radiologieinformationssysteme (RIS) hatte im Jahr 2021 ein Volumen von 1,04 Milliarden US-Dollar und soll von XX Milliarden US-Dollar im Jahr 2023 auf 2,48 Milliarden US-Dollar im Jahr 2031 anwachsen. Der Markt wird voraussichtlich zwischen 2023 und 2031 eine durchschnittliche jährliche Wachstumsrate von 9,4 % verzeichnen. Das wachsende Bewusstsein für Radiologieinformationssysteme (RIS) mit ihren geringeren Gesundheitsrisiken und die Akzeptanz in den Entwicklungsregionen werden wahrscheinlich weiterhin die wichtigsten Trends auf dem Markt für Radiologieinformationssysteme (RIS) bleiben.

Marktanalyse für Radiologieinformationssysteme (RIS)

Zu den wichtigsten Wachstumsfaktoren auf dem Markt zählen die steigenden Inzidenzraten chronischer Krankheiten, der Zugang zu Informationstechnologiesystemen im Gesundheitswesen und staatliche Mittel für die Krebsforschung. Darüber hinaus nimmt die Belastung durch chronische Krankheiten weltweit zu, verbunden mit einer zunehmenden Alterung der Bevölkerung, und lebensstilbedingte Erkrankungen wie Krebs, Arthritis, Herz-Kreislauf-Erkrankungen und Diabetes sind einige der Hauptfaktoren, die für das Wachstum dieses Marktes verantwortlich sind. Eine Zunahme der Krebsfälle wird voraussichtlich zu einer verstärkten Fokussierung auf Radiologiedienste für eine angemessene Diagnose führen, was die Nachfrage nach Radiologieinformationssystemen erhöhen dürfte. Die zunehmenden chronischen Krankheiten wie Krebs steigern die Nachfrage nach Radiologieinformationssystemen. Die hohen Installationskosten und der Mangel an Fachkräften werden das Marktwachstum während des Untersuchungszeitraums jedoch voraussichtlich hemmen.

Marktübersicht für Radiologieinformationssysteme (RIS)

RIS ist eine spezielle Gesundheitssoftware, die zur Verwaltung und Optimierung der Abläufe in Radiologie- und Bildgebungszentren entwickelt wurde. Das RIS speichert, verwaltet und verteilt radiologische Bilder , Patienteninformationen und zugehörige Daten. Kontinuierliche technologische Fortschritte, darunter maschinelles Lernen, Deep Learning und die Integration von KI in das Gesundheitswesen, werden die Genauigkeit und Effizienz von Radiologiesystemen verbessern. Darüber hinaus führt die wachsende Nachfrage nach integrierten Gesundheitslösungen zur Verbesserung der Patientenversorgung und Optimierung von Arbeitsabläufen zur Einführung von RIS. Staatliche Vorschriften und Initiativen fördern auch die Standardisierung medizinischer Daten und Aufzeichnungen. Sie bieten auch Anreize für die Einführung von IT-Diensten im Gesundheitswesen, was sich voraussichtlich positiv auf die Marktwachstumschancen auswirken wird.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Radiologieinformationssysteme (RIS): Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Markttreiber und Chancen für Radiologieinformationssysteme (RIS)

Fortschritte bei diagnostischen Bildgebungslösungen begünstigen den Markt

Die Einführung der digitalen Bildgebung hat das Fachgebiet der Radiologie verändert. Sie katalysierte den Übergang von der traditionellen filmbasierten Bildgebung zu digitalen Formaten, optimiertem Datenmanagement und verbesserter Zugänglichkeit. Die digitale Bildverarbeitung führte auch zu deutlichen Verbesserungen der Bildqualität. RIS ermöglicht es dem medizinischen Personal, Termine für Patienten sowohl auf ambulanter als auch auf stationärer Basis zu vereinbaren. Die Radiologie hat sich in Richtung computergestütztes Management im Gesundheitswesen weiterentwickelt und auf die Nachfrage nach kosteneffizienter und schneller Kommunikation zwischen Radiologieabteilungen und ihren Benutzern reagiert. In den letzten Jahren gab es im Gesundheitswesen verschiedene Entwicklungen bei Bildgebungsverfahren für diagnostische Zwecke. In den letzten Jahren wurden viele Fortschritte in der digitalen Radiographie gemacht , darunter KI-gestützte Röntgeninterpretation, Dual-Energy-Bildgebung, Tomosynthese, computergestützte Diagnose, automatische Bildzusammenstellung und digitale mobile Radiographie. Diese Fortschritte haben zu einer verbesserten Bildqualität geführt, was dazu beiträgt, die Patientenversorgung zu verbessern und bessere Patientenergebnisse zu erzielen. Darüber hinaus reduziert der Einsatz der digitalen Radiographie den Bedarf an wiederholten Bildgebungsverfahren, was den Vorteil einer geringeren Strahlenbelastung hat.

Zunehmende Nutzung von IT-Diensten im Gesundheitswesen in Schwellenländern – eine Chance für das Wachstum des Marktes für Radiologieinformationssysteme (RIS)

Weltweit besteht ein wachsender Bedarf an Technologieeinführung in Radiologiediensten, um die Nachfrage zu decken. Die Zukunft von RIS liegt in der Nutzung künstlicher Intelligenz (KI) und maschinellem Lernen (ML). KI-Algorithmen können Radiologen helfen, Bilder zu analysieren, Anomalien zu erkennen und Entscheidungen zu unterstützen. ML-Algorithmen können kontinuierlich aus riesigen Datenmengen lernen und Diagnosen und Behandlungspläne verfeinern. Verbesserte Konnektivität durch Internet und Mobiltechnologie, Teleradiologie, künstliche Intelligenz, Entwicklungen in der medizinischen Bildgebungsinformatik und tragbare oder mobile medizinische Bildgebungsgeräte können abgelegenen Standorten in jedem Land Zugang zu besserer Gesundheitsversorgung und Diagnostik ermöglichen. Darüber hinaus werden Gesundheitssysteme in Entwicklungsländern technologiefreundlicher, da die Länder eine Internationalisierung der Gesundheitsversorgung als etablierte Marken erleben. So erweiterte beispielsweise die in den USA ansässige Cleveland Clinic ihre Märkte in den Vereinigten Arabischen Emiraten, und das in England ansässige Start-up Babylon, eine auf maschinellem Lernen und KI basierende Diagnose-App für die Primärversorgung, trat in China und Ruanda ein.

Segmentierungsanalyse des Marktberichts zum Radiologieinformationssystem (RIS)

Wichtige Segmente, die zur Ableitung der Marktanalyse für Radiologieinformationssysteme (RIS) beigetragen haben, sind Produkt, Bereitstellung, Komponente und Endbenutzer.

- Basierend auf dem Produkt ist der Markt für Radiologieinformationssysteme (RIS) in eigenständige RIS und integrierte RIS unterteilt. Im Jahr 2023 hielt das Segment der integrierten RIS den größten Marktanteil, und es wird erwartet, dass dasselbe Segment im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate verzeichnet.

- Nach Bereitstellung ist der Markt in webbasierte RIS, cloudbasierte RIS und lokale RIS segmentiert. Im Jahr 2023 hielt das webbasierte RIS-Segment den größten Marktanteil. Es wird jedoch erwartet, dass das cloudbasierte RIS-Segment zwischen 2023 und 2031 die höchste durchschnittliche jährliche Wachstumsrate verzeichnet.

- Basierend auf den Komponenten wird der Markt für Radiologieinformationssysteme (RIS) in Hardware, Software und Dienstleistungen unterteilt. Im Jahr 2023 hielt das Dienstleistungssegment den größten Marktanteil, und das Softwaresegment dürfte im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate verzeichnen.

- In Bezug auf den Endverbraucher ist der Markt in niedergelassene Ärzte, Krankenhäuser und Notfallgesundheitsdienstleister segmentiert. Im Jahr 2023 hielt das Krankenhaussegment den größten Marktanteil, und es wird geschätzt, dass dasselbe Segment im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate verzeichnet.

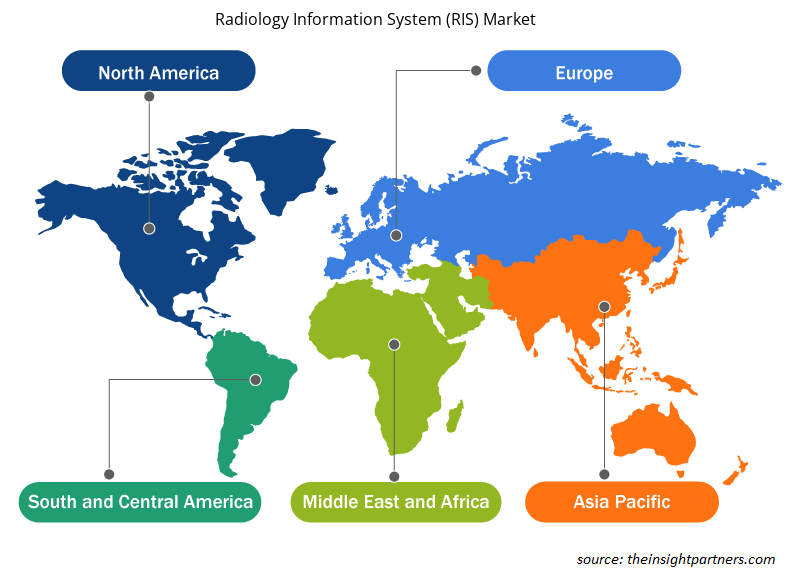

Marktanteilsanalyse für Radiologieinformationssysteme (RIS) nach Geografie

Der geografische Umfang des Marktberichts zum Radiologieinformationssystem (RIS) ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Südamerika/Süd- und Mittelamerika.

Nordamerika dominiert den Markt für Radiologieinformationssysteme (RIS). Die Nachfrage in der Region dürfte aufgrund mehrerer Faktoren wie staatlicher Investitionen in die Gesundheitsinfrastruktur, zunehmender Bekanntheit der medizinischen Bildgebung sowie der Vorteile, die mit der Implementierung von RIS verbunden sind, stark wachsen. In den USA sind Faktoren wie die große Anzahl von Bildgebungszentren in dieser Region, das schnelle Tempo des technologischen Fortschritts, die wachsende geriatrische Bevölkerung und die steigende Nachfrage nach computergestützter Diagnose einige der wichtigsten Wachstumstreiber dieses Marktes. Auch die Präsenz verschiedener Unternehmen, die sich mit der Entwicklung fortschrittlicher RIS-Systeme für die diagnostische Bildgebung in den Bereichen Herz-Kreislauf, Orthopädie, Zahnmedizin und Onkologie beschäftigen, dürfte Wachstumschancen für das Marktwachstum bieten. Der asiatisch-pazifische Raum dürfte jedoch in den kommenden Jahren aufgrund von Faktoren wie dem Wachstum der Gesundheitsinformationstechnologiebranche in dieser Region aufgrund der Verbesserung der Gesundheitsinfrastruktur und der steigenden Akzeptanz fortschrittlicher Gesundheitstechniken durch die Verbraucher die höchste durchschnittliche jährliche Wachstumsrate aufweisen.

Regionale Einblicke in den Markt für Radiologieinformationssysteme (RIS)

Die regionalen Trends und Faktoren, die den Markt für Radiologieinformationssysteme (RIS) während des gesamten Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie von Radiologieinformationssystemen (RIS) in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für Radiologieinformationssysteme (RIS).

Umfang des Marktberichts zum Radiologieinformationssystem (RIS)

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2021 | 1,04 Milliarden US-Dollar |

| Marktgröße bis 2031 | 2,48 Milliarden US-Dollar |

| Globale CAGR (2023 - 2031) | 9,4 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2024–2031 |

| Abgedeckte Segmente |

Nach Produkt

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte für Radiologieinformationssysteme (RIS): Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Radiologieinformationssysteme (RIS) wächst rasant, angetrieben durch die steigende Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten auf dem Markt für Radiologieinformationssysteme (RIS) tätigen Unternehmen sind:

- Koninklijke Philips NV,

- Siemens Healthineers AG,

- Bayer AG,

- Cerner Corporation,

- Allgemeine Elektrizit?tsgesellschaft,

- McKESSON CORPORATION,

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für Radiologieinformationssysteme (RIS)

Marktnachrichten und aktuelle Entwicklungen zum Radiologieinformationssystem (RIS)

Der Markt für Radiologieinformationssysteme (RIS) wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Im Folgenden finden Sie eine Liste der Entwicklungen auf dem Markt für Radiologieinformationssysteme (RIS):

- Royal Solutions Group, ein führender Anbieter von Gesundheitssoftware, freut sich, die Ausweitung seiner Partnerschaft mit Concord Technologies bekannt zu geben. Die Integration zusätzlicher Technologie aus Concords Practical AI-Suite hochmoderner Datenverarbeitungslösungen ermöglicht das einfache Scannen sowohl getippter als auch handschriftlicher Notizen und das anschließende Extrahieren und Integrieren der Daten in Arbeitsabläufe. Dies verspricht eine Veränderung der Art und Weise, wie Arztpraxen mit Auftragseingabe, Indizierung und Vorabgenehmigung umgehen. Durch die Automatisierung dieser kritischen Prozesse können sich medizinische Fachkräfte auf die Patientenversorgung statt auf den Papierkram konzentrieren. (Royal Solutions Group, LLC, Pressemitteilung, 2024)

- Manipal Hospitals, einer der führenden Gesundheitsdienstleister Indiens, hat eine Vereinbarung mit FUJIFILM India geschlossen. Im Rahmen der langfristigen Vereinbarung wird Manipal Hospitals mit einem umfangreichen Bildarchivierungs- und Kommunikationssystem (PACS) ausgestattet, das von FUJIFILM India betrieben wird. Das PACS macht das manuelle Speichern, Abrufen und Versenden vertraulicher Informationen, Filme und Berichte überflüssig. (FUJIFILM India Private Limited, News, 2023)

- PARATUS erwirbt Mehrheitsanteil an IMAGE Information Systems. IMAGE ist ein führender Anbieter von PACS, der Bildgebungszentren und Krankenhäuser auf der ganzen Welt bedient. Diese Investition von PARATUS ist ein strategischer Baustein beim Aufbau eines weltweit führenden Anbieters von Gesundheitssoftware und IT-Diensten. (RADiQ IMAGE Information Systems, News, 2023)

- Philips stellt neue KI-gestützte Informatiklösungen vor, um die Diagnosesicherheit durch Intelligenz in jedem Schritt des Radiologie-Workflows bei RSNA zu erhöhen. (Koninklijke Philips NV, News, 2022)

Marktbericht zum Radiologieinformationssystem (RIS): Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für Radiologieinformationssysteme (RIS) (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Projekts abgedeckt sind

- Marktdynamik wie Treiber, Beschränkungen und wichtige Chancen

- Wichtige Zukunftstrends

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Globale und regionale Marktanalyse mit wichtigen Markttrends, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen

- Detaillierte Firmenprofile

Ankita ist eine dynamische Marktforschungs- und Beratungsexpertin mit über 8 Jahren Erfahrung in den Bereichen Technologie, Medien, IKT sowie Elektronik und Halbleiter. Sie hat über 100 Beratungs- und Forschungsaufträge für globale Kunden wie Microsoft, Oracle, NEC Corporation, SAP, KPMG und Expeditors International erfolgreich geleitet und durchgeführt. Zu ihren Kernkompetenzen gehören Marktbewertung, Datenanalyse, Prognose, Strategieformulierung, Wettbewerbsbeobachtung und das Verfassen von Berichten. Ankita ist versiert in der Abwicklung kompletter Projektzyklen – von der Angebotserstellung vor dem Verkauf und Kundengesprächen bis hin zur Bereitstellung umsetzbarer Erkenntnisse nach dem Verkauf. Sie ist versiert in der Leitung funktionsübergreifender Teams, der Strukturierung komplexer Forschungsmodule und der Ausrichtung von Lösungen an kundenspezifischen Geschäftszielen. Ihre ausgezeichneten Kommunikationsfähigkeiten, Führungsqualitäten und Präsentationsfähigkeiten haben es ihr ermöglicht, in einem schnelllebigen und sich entwickelnden Marktumfeld stets wertorientierte Ergebnisse zu liefern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends