Tamaño del mercado, cuota de mercado y demanda de terminales automatizadas de entrega de paquetes para 2034

Datos históricos : 2021-2024 | Año base : 2025 | Período de pronóstico : 2026-2034Tamaño y pronóstico del mercado de terminales automatizadas de entrega de paquetes (2021-2034), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por implementación (interior y exterior), proveedores de servicios (minoristas/comercio electrónico, envío/logística, almacenes, gobierno, otros) y geografía.

- Estado : Datos publicados

- Código de informe : TIPTE100000497

- Categoría : Electrónica y semiconductores

- Número de páginas : 150

- Formatos de informe disponibles :

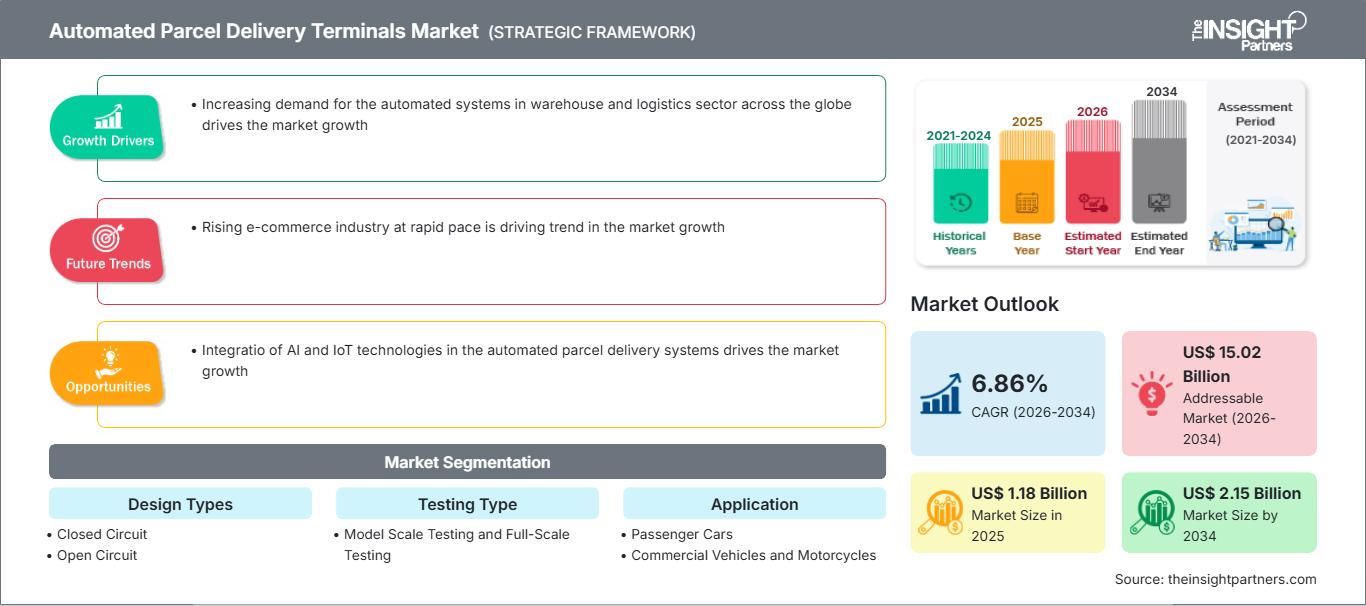

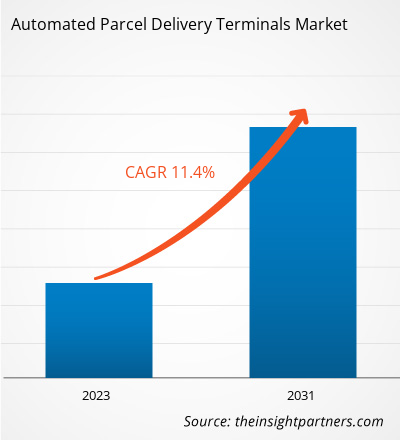

Se prevé que el mercado de terminales automatizadas de entrega de paquetes alcance los 2150 millones de dólares estadounidenses en 2034, frente a los 1180 millones de dólares estadounidenses de 2025. Se espera que el mercado registre una tasa de crecimiento anual compuesta (CAGR) del 6,86 % durante el período de previsión 2026-2034.

Los terminales de entrega de paquetes automatizados son taquillas automáticas con unidades de autoservicio diseñadas para agilizar la entrega de paquetes. Estos terminales se instalan en lugares de alto tránsito como centros comerciales, tiendas minoristas, supermercados, estaciones de autobuses, aeropuertos, estaciones de tren y otras áreas públicas. El objetivo principal de estos terminales es proporcionar una forma segura y conveniente para que las personas dejen y recojan paquetes en cualquier momento. Los terminales de entrega de paquetes automatizados, combinados con tecnologías avanzadas, están diseñados para satisfacer la creciente demanda del sector logístico y de almacenamiento.

Análisis del mercado de terminales automatizadas de entrega de paquetería

El mercado de terminales automatizadas de entrega de paquetes está experimentando un rápido crecimiento debido a la creciente demanda de los consumidores por opciones de entrega sin contacto y convenientes. Los avances tecnológicos para mejorar la productividad y reducir los tiempos de entrega han impulsado significativamente el crecimiento del mercado de terminales automatizadas de entrega de paquetes. Las tecnologías avanzadas incluyen la integración de IA e IoT para automatizar las opciones de entrega de paquetes. Los principales actores del mercado se centran en innovaciones tecnológicas para resolver los problemas relacionados con la entrega de última milla. Además, el rápido crecimiento del sector del comercio electrónico, junto con el aumento de las tendencias de compra en línea, ha generado una enorme demanda para el mercado de terminales automatizadas de entrega de paquetes durante el período previsto.

Descripción general del mercado de terminales automatizadas de entrega de paquetería

El creciente auge del comercio electrónico, impulsado por el aumento de las compras en línea a nivel mundial, ha generado una enorme demanda de terminales automatizadas de entrega de paquetes durante el período previsto. Según la Organización para la Administración del Comercio Internacional (OACT), se espera que las ventas globales de comercio electrónico B2B alcancen los 36 billones de dólares estadounidenses para 2026. Este crecimiento se debe principalmente a sectores como la manufactura, la salud, la energía y los servicios profesionales. Asimismo, la creciente demanda de sistemas automatizados en el sector de almacenes y logística a nivel global impulsa el crecimiento del mercado.

Personaliza este informe para adaptarlo a tus necesidades.

Obtén PERSONALIZACIÓN GRATUITAMercado de terminales automatizadas de entrega de paquetería: Perspectivas estratégicas

-

Descubra las principales tendencias del mercado que se recogen en este informe.Esta muestra GRATUITA incluirá análisis de datos, que abarcan desde tendencias de mercado hasta estimaciones y pronósticos.

Factores impulsores y oportunidades del mercado de terminales automatizadas de entrega de paquetes

La creciente demanda de sistemas automatizados en el sector de almacenes y logística a nivel mundial impulsa el crecimiento del mercado.

El mercado se ve impulsado por el rápido crecimiento del sector del comercio electrónico, lo que ha generado una enorme demanda de sistemas automatizados de entrega de paquetes. Esto ha impulsado el crecimiento del mercado de terminales automatizadas de entrega de paquetes.

Además, factores como las entregas en zonas remotas y los intentos de entrega fallidos generan costes adicionales para las empresas. Por ello, las soluciones de recogida en tienda, como los terminales de entrega de paquetes automatizados, están ganando popularidad entre los minoristas de comercio electrónico.

La adopción generalizada de teléfonos móviles y acceso a internet ha permitido a los consumidores comprar productos de otros países. Se prevé que, como consecuencia, el número de envíos de paquetes aumente significativamente. Los minoristas también están promoviendo el uso de opciones de entrega alternativas para evitar retrasos y fallos en las entregas.

Los gobiernos de todo el mundo están haciendo gran hincapié en la digitalización y fomentando los pagos sin efectivo, especialmente en países en desarrollo como China e India. Pueden impulsar sus objetivos políticos de una economía digitalizada, sin efectivo y más transparente mediante el uso de la opción de pago contra entrega (COD, por sus siglas en inglés) disponible en las terminales inteligentes de entrega de paquetes, lo que facilita transacciones exitosas y fluidas entre clientes y consumidores.

La creciente adopción de tecnologías avanzadas como el aprendizaje automático, la inteligencia artificial, el internet de las cosas y la cadena de bloques está impulsando el crecimiento del mercado.

La creciente integración de tecnologías avanzadas como el aprendizaje automático, la inteligencia artificial y el Internet de las cosas para el lanzamiento de terminales de paquetería automatizadas está generando importantes oportunidades en el mercado. Varios actores clave del mercado están desarrollando y lanzando tecnologías avanzadas basadas en terminales de entrega de paquetería automatizadas. Por ejemplo, en noviembre de 2023, Oman Post, filial del Grupo Asyad, lanzó una innovadora terminal de paquetería automatizada. Esta tecnología de vanguardia contribuyó a una mejora del 43 % en la eficiencia operativa, lo que a su vez mejora la satisfacción del cliente. El sistema, implementado con tecnología de IA, mejora la productividad y aumenta la eficiencia en la entrega de paquetes a los clientes. Esta terminal basada en IA procesa hasta 6000 paquetes por hora y clasifica más de 12 líneas por ciclo.

Análisis de segmentación del informe de mercado de terminales automatizadas de entrega de paquetes

Los segmentos clave que contribuyeron a la elaboración del análisis de mercado de terminales automatizadas de entrega de paquetes son los proveedores de servicios y de implementación.

- En función de su uso, el mercado se divide en interior y exterior.

- En función de los usuarios finales, el mercado se divide en minoristas/comercio electrónico, transporte/logística, almacenes, gobierno y otros.

Análisis de la cuota de mercado de terminales automatizadas de entrega de paquetes por región geográfica

El alcance geográfico del informe de mercado de terminales automatizadas de entrega de paquetes se divide principalmente en cinco regiones: América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur.

Se prevé que Norteamérica lidere el crecimiento del mercado debido a la rápida adopción de tecnologías avanzadas basadas en terminales automatizadas de entrega de paquetes. Estados Unidos y Canadá poseen una participación significativa en el mercado global, con una creciente inversión en automatización de almacenes por parte de las principales empresas de logística estadounidenses.

Sin embargo, existe una importante oportunidad en los países en desarrollo de la región de Asia-Pacífico para adoptar terminales automatizadas de entrega de paquetes, debido al creciente auge del comercio electrónico a nivel mundial. India y China son los países que más rápidamente están adoptando estas terminales. Varios proveedores líderes de servicios logísticos están invirtiendo considerablemente en la adquisición de terminales automatizadas para satisfacer la creciente demanda del sector.

Alcance del informe de mercado sobre terminales automatizadas de entrega de paquetes

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2025 | 1.180 millones de dólares estadounidenses |

| Tamaño del mercado para 2034 | 2.150 millones de dólares estadounidenses |

| Tasa de crecimiento anual compuesta global (2026 - 2034) | 6,86% |

| Datos históricos | 2021-2024 |

| Período de pronóstico | 2026-2034 |

| Segmentos cubiertos |

Por tipos de diseño

|

| Regiones y países incluidos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de los actores del mercado de terminales automatizadas de entrega de paquetes: comprender su impacto en la dinámica empresarial.

El mercado de terminales automatizadas de entrega de paquetes está experimentando un rápido crecimiento, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor concienciación sobre los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

Noticias y novedades del mercado de terminales automatizadas de entrega de paquetería

El mercado de terminales automatizadas de entrega de paquetes se evalúa mediante la recopilación de datos cualitativos y cuantitativos tras una investigación primaria y secundaria, que incluye publicaciones corporativas importantes, datos de asociaciones y bases de datos. A continuación, se presenta una lista de los avances y estrategias en el mercado de terminales automatizadas de entrega de paquetes:

- En abril de 2021, Cleveron, empresa de robótica para la entrega de paquetes, lanzó el Cleveron 701, un vehículo semiautónomo para la entrega de última milla. Está diseñado para mejorar la productividad y la eficiencia de las empresas de logística y comercio minorista, impulsando así la entrega de paquetes en la última milla. (Fuente: Flyability, comunicado de prensa/sitio web de la empresa/boletín informativo)

Cobertura y entregables del informe de mercado de terminales automatizadas de entrega de paquetes.

El informe “Tamaño y pronóstico del mercado de terminales automatizadas de entrega de paquetes (2021–2031)” proporciona un análisis detallado del mercado que abarca las siguientes áreas:

- Tamaño del mercado y pronóstico a nivel global, regional y nacional para todos los segmentos clave del mercado cubiertos en el alcance.

- Dinámica del mercado, como factores impulsores, limitaciones y oportunidades clave.

- Tendencias clave de futuro

- Análisis detallado de las cinco fuerzas de Porter

- Análisis de mercado global y regional que abarca las principales tendencias del mercado, los actores más importantes, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama industrial y de la competencia, que abarca la concentración del mercado, el análisis mediante mapas de calor, los principales actores y los desarrollos recientes.

- Perfiles detallados de empresas con análisis FODA

Naveen es un experimentado profesional en investigación de mercados y consultoría con más de 9 años de experiencia en proyectos personalizados, sindicados y de consultoría. Actualmente se desempeña como Vicepresidente Asociado, donde ha gestionado con éxito a las partes interesadas en toda la cadena de valor del proyecto y ha redactado más de 100 informes de investigación y más de 30 proyectos de consultoría. Su trabajo abarca proyectos industriales y gubernamentales, contribuyendo significativamente al éxito de los clientes y a la toma de decisiones basada en datos.

Naveen es licenciado en Ingeniería Electrónica y Comunicaciones por la VTU (Karnataka) y tiene un MBA en Marketing y Operaciones por la Universidad de Manipal. Ha sido miembro activo del IEEE durante 9 años, participando en conferencias, simposios técnicos y realizando voluntariado tanto a nivel de sección como regional. Antes de su puesto actual, trabajó como Consultor Estratégico Asociado en IndustryARC y como Consultor de Servidores Industriales en Hewlett Packard (HP Global).

- Análisis histórico (2 años), año base, pronóstico (7 años) con CAGR

- Análisis PEST y FODA

- Tamaño del mercado, valor/volumen: global, regional y nacional

- Industria y panorama competitivo

- Conjunto de datos de Excel

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias

Desbloquea descuentos exclusivos en informes

Consultar ahora

Obtenga una muestra gratuita para - Mercado de terminales automatizadas de entrega de paquetes

Obtenga una muestra gratuita para - Mercado de terminales automatizadas de entrega de paquetes