Informe de mercado de herramientas de carburo 2028 por segmentos, geografía, dinámica, desarrollos recientes e ideas estratégicas

Pronóstico del mercado de herramientas de carburo hasta 2028: impacto de la COVID-19 y análisis global por tipo de herramienta (fresas de extremo, brocas con punta, fresas, taladros, cortadores y otras herramientas), configuración (manual y mecánica) y usuario final (automoción y transporte, fabricación de metales, construcción, petróleo y gas, maquinaria pesada y otros usuarios finales).

- Estado : Publicada

- Código de informe : TIPRE00007001

- Categoría : Fabricación y construcción

- Número de páginas : 165

- Formatos de informe disponibles :

- Fecha de última actualización : June 17, 2024

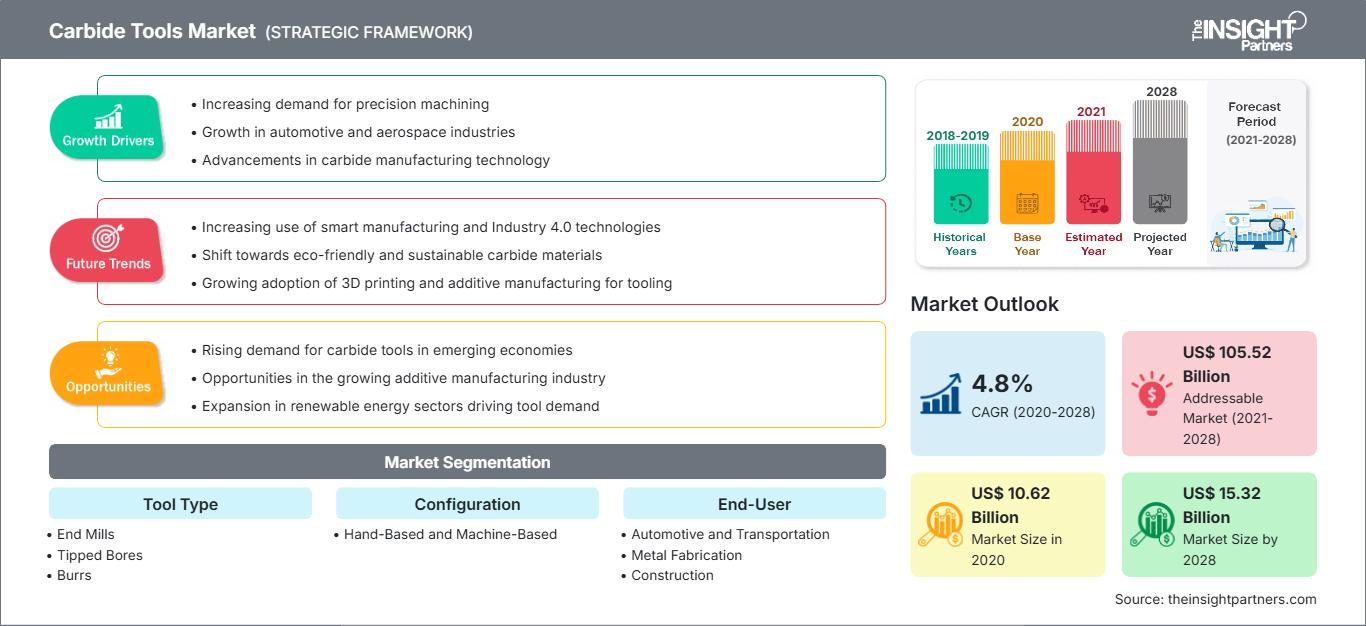

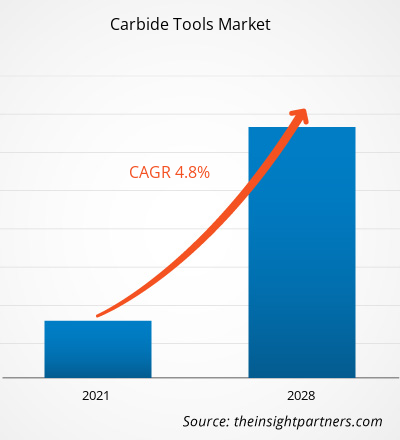

[Informe de investigación] El mercado de herramientas de carburo se valoró en 10.623,97 millones de dólares estadounidenses en 2020 y se prevé que alcance los 15.320,99 millones de dólares estadounidenses en 2028; se espera que crezca a una tasa de crecimiento anual compuesta (TCAC) del 4,8% entre 2021 y 2028.

Los avances en el diseño de procesos de fabricación y la creciente necesidad de aumentar la eficacia de la producción están sentando las bases para que los fabricantes investiguen productos de máquinas herramienta superiores, lo que impulsa la demanda de herramientas de carburo. Las máquinas herramienta utilizadas en diversas industrias se emplean principalmente para mecanizar o dar forma a metales u otros materiales rígidos, otorgándoles una forma única mediante procesos de mandrinado, rectificado, cizallado y corte. Actualmente, existen dos tipos principales de máquinas herramienta que se utilizan ampliamente en diferentes industrias: las de acero rápido (HSS) y las de carburo. Estas herramientas se utilizan extensamente en aplicaciones de mecanizado debido a sus características significativas, como alta velocidad, menor tiempo de ciclo, larga vida útil, retención del filo a altas temperaturas de mecanizado y excepcional resistencia al desgaste. La creciente popularidad de las herramientas de carburo, especialmente en aplicaciones de fabricación, es uno de los factores clave que se espera impulsen el mercado durante el período de pronóstico. Además, estas herramientas de carburo se utilizan en plantas de fabricación de las industrias automotriz, aeroespacial, ferroviaria, de muebles y carpintería, energética y de equipos médicos. En estos sectores, se utilizan herramientas de corte especiales para diseñar y fabricar productos, lo que impulsa la demanda de herramientas de carburo. El uso de estas herramientas en diversas industrias, tanto para su operación manual como automática, está impulsando aún más el crecimiento del mercado global de herramientas de carburo.

Obtendrá personalización gratuita de cualquier informe, incluyendo partes de este informe, análisis a nivel de país y paquetes de datos de Excel. Además, podrá aprovechar excelentes ofertas y descuentos para empresas emergentes y universidades.

Mercado de herramientas de carburo: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado que se describen en este informe.Esta muestra GRATUITA incluirá análisis de datos, que abarcarán desde tendencias de mercado hasta estimaciones y pronósticos.

Impacto de la pandemia de COVID-19 en el mercado de herramientas de carburo

La pandemia de COVID-19 ha sacudido diversos sectores. El tremendo crecimiento en la propagación del virus ha impulsado a los gobiernos de todo el mundo a imponer estrictas restricciones a la circulación de vehículos y personas. Debido a las prohibiciones de viaje, los confinamientos masivos y el cierre de negocios, la pandemia ha afectado negativamente a las economías e innumerables industrias en varios países. La imposición de confinamientos ha resultado en una menor producción de materias primas, bienes y servicios. Por lo tanto, las industrias manufactureras, automotrices, de semiconductores y electrónica, de petróleo y gas, mineras, de aviación y otras han experimentado una disminución en sus operaciones debido al cese temporal de actividades.

El confinamiento mundial para minimizar la transmisión del virus ha interrumpido significativamente las actividades de la cadena de suministro y el volumen de producción de numerosos fabricantes, especialmente de las pequeñas y medianas empresas. Además, la producción en múltiples industrias se contrajo considerablemente durante 2020, lo que provocó una caída en el mercado de herramientas de carburo. Sin embargo, ante la creciente necesidad de productos sanitarios, la demanda de herramientas de carburo está aumentando considerablemente en el sector médico.

Perspectivas del mercado de herramientas de carburo

El aumento de la producción en el sector automotriz impulsa el crecimiento del mercado de herramientas de carburo

La producción automotriz está en constante aumento en todo el mundo, especialmente en los países asiáticos y europeos, lo que impulsa la demanda de herramientas de carburo. El sector utiliza ampliamente estas herramientas en el mecanizado de metales de cigüeñales, el fresado frontal y la perforación, entre otras operaciones de mecanizado involucradas en la fabricación de autopartes. La industria automotriz está obteniendo excelentes resultados con el uso de carburo de tungsteno en rótulas, frenos, cigüeñales de vehículos de alto rendimiento y otras piezas mecánicas que soportan un uso intensivo y temperaturas extremas. Gigantes automotrices como Audi, BMW, Ford Motor Company y Range Rover contribuyen significativamente al crecimiento del mercado de herramientas de carburo. Los vehículos híbridos eléctricos están ganando terreno en Norteamérica, impulsando así el crecimiento de este mercado en la región. Países como Estados Unidos y Canadá son fabricantes de automóviles destacados en la región. Según el Consejo de Política Automotriz Estadounidense, los fabricantes de automóviles y sus proveedores contribuyen con aproximadamente el 3% al PIB de Estados Unidos. General Motors Company, Ford Motor Company, Fiat Chrysler Automobiles y Daimler se encuentran entre los principales fabricantes de automóviles en Norteamérica. Según datos de la Organización Internacional de Fabricantes de Vehículos Automotores, en 2019, Estados Unidos y Canadá fabricaron aproximadamente 2.512.780 y 461.370 automóviles, respectivamente. Además, las herramientas de carburo también se utilizan ampliamente en las industrias ferroviaria, aeroespacial y de defensa, y naval.

Información de mercado basada en el tipo de herramienta

Según el tipo de herramienta, el mercado de herramientas de carburo se segmenta en fresas de extremo, mandriles con punta, fresas de desbaste, brocas, cortadores y otras herramientas. En 2020, el segmento de fresas de extremo representó la mayor cuota de mercado.

Información de mercado basada en la configuración

Según su configuración, el mercado de herramientas de carburo se divide en manuales y mecanizadas. En 2020, el segmento de herramientas mecanizadas representó la mayor cuota de mercado.

Información de mercado basada en el usuario final

Por usuario final, el mercado de herramientas de carburo se segmenta en automoción y transporte, fabricación de metales, construcción, petróleo y gas, maquinaria pesada y otros usuarios finales. En 2020, el segmento de automoción y transporte representó la mayor cuota de mercado.

Las empresas que operan en el mercado de herramientas de carburo adoptan estrategias como fusiones, adquisiciones e iniciativas de mercado para mantener su posición. A continuación, se enumeran algunos avances de los principales actores:

- En noviembre de 2020, GARR TOOL se asoció con Mastercam para ofrecer a sus clientes una biblioteca completa de herramientas integrada en la plataforma Mastercam. Esta alianza será de gran valor para los clientes actuales y futuros, ya que el proceso de fabricación depende cada vez más del acceso instantáneo y sencillo a los datos.

- En febrero de 2019, el Grupo CERATIZIT adquirió el 50% de las acciones de Stadler Metalle GmbH & Co. KG. La empresa declaró que la inversión en Stadler les permitió asegurar toda la cadena de suministro de materias primas y centrarse aún más en el reciclaje de herramientas de carburo en el suministro de materias primas.

Perspectivas regionales del mercado de herramientas de carburo

Los analistas de The Insight Partners han explicado en detalle las tendencias regionales y los factores que influyen en el mercado de herramientas de carburo durante el período de previsión. Esta sección también analiza los segmentos y la geografía del mercado de herramientas de carburo en Norteamérica, Europa, Asia Pacífico, Oriente Medio y África, y Sudamérica y Centroamérica.

Alcance del informe de mercado de herramientas de carburo

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2020 | 10.620 millones de dólares estadounidenses |

| Tamaño del mercado para 2028 | 15.320 millones de dólares estadounidenses |

| Tasa de crecimiento anual compuesto global (2020 - 2028) | 4,8% |

| Datos históricos | 2018-2019 |

| período de previsión | 2021-2028 |

| Segmentos cubiertos |

Por tipo de herramienta

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de los participantes en el mercado de herramientas de carburo: comprensión de su impacto en la dinámica empresarial.

El mercado de herramientas de carburo está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las nuevas tendencias, lo que impulsa aún más el crecimiento del mercado.

- Obtenga una visión general de los principales actores del mercado de herramientas de carburo.

El mercado mundial de herramientas de carburo se ha segmentado como se indica a continuación:

Por tipo de herramienta

- Fresas de extremo

- Cañones con punta

- Burrs

- Taladros

- Cortadores

- Otras herramientas

Por configuración

- Hecho a mano

- Basado en máquinas

Por el usuario final

- Automoción y transporte

- Fabricación de metales

- Construcción

- Petróleo y gas

- Maquinaria pesada

- Otros usuarios finales

Por geografía

-

América del norte

- A NOSOTROS

- Canadá

- México

-

Europa

- Francia

- Alemania

- Italia

- Reino Unido

- Rusia

- El resto de Europa

-

Asia Pacífico (APAC)

- Porcelana

- India

- Corea del Sur

- Japón

- Australia

- Resto de Asia Pacífico

-

Oriente Medio y África (MEA)

- Sudáfrica

- Arabia Saudita

- Emiratos Árabes Unidos

- Resto de Oriente Medio y África

-

Sudamérica (SAM)

- Brasil

- Argentina

- El resto de SAM

Perfiles de empresas

- Xinrui Industry Co., Ltd.

- CERATIZIT SA

- HERRACIÓN GARR

- Compañía de herramientas de corte Ingersoll

- Herramientas de precisión KYOCERA

- GRUPO DIMAR

- Corporación MITSUBISHI MATERIALS

- Coromant de Sandvik

- Compañía YG-1, Ltd.

- Corporación Makita

Nivedita es una investigadora con más de 9 años de experiencia en Investigación de Mercados y Consultoría de Negocios. Actualmente se desempeña como Gerente de Proyectos en el área de TIC en The Insight Partners, y aporta una amplia experiencia en la gestión y ejecución de proyectos de investigación sindicados, personalizados, por suscripción y de consultoría en diversos sectores tecnológicos.

Con una trayectoria comprobada en la entrega de análisis basados en datos e información práctica, Nivedita ha sido una colaboradora clave en varios proyectos cruciales. Su trabajo abarca la ejecución integral de proyectos, desde la comprensión de los objetivos del cliente y el análisis de las tendencias del mercado hasta la formulación de recomendaciones estratégicas. Ha colaborado extensamente con empresas líderes en TIC, ayudándolas a identificar oportunidades de mercado y a adaptarse a los cambios del sector.

Nivedita posee un MBA en Administración de Empresas por IMS, Dehradun. Antes de unirse a The Insight Partners, adquirió una valiosa experiencia en MarketsandMarkets y Future Market Insights en Pune, donde ocupó diversos puestos de investigación y desarrolló una sólida base en análisis del sector y la interacción con el cliente.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias