Rapporto sul mercato Strumenti in metallo duro 2028 per segmenti, geografia, dinamiche, sviluppi recenti e approfondimenti strategici

Previsioni di mercato degli utensili in metallo duro fino al 2028 - Impatto del COVID-19 e analisi globale per tipo di utensile (frese a candela, fori con punta, sbavature, trapani, frese e altri utensili), configurazione (manuale e meccanica) e utente finale (settore automobilistico e dei trasporti, lavorazione dei metalli, edilizia, petrolio e gas, macchinari pesanti e altri utenti finali)

- Stato : Edito

- Codice del report : TIPRE00007001

- Categoria : Produzione e costruzione

- Numero di pagine : 165

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 17, 2024

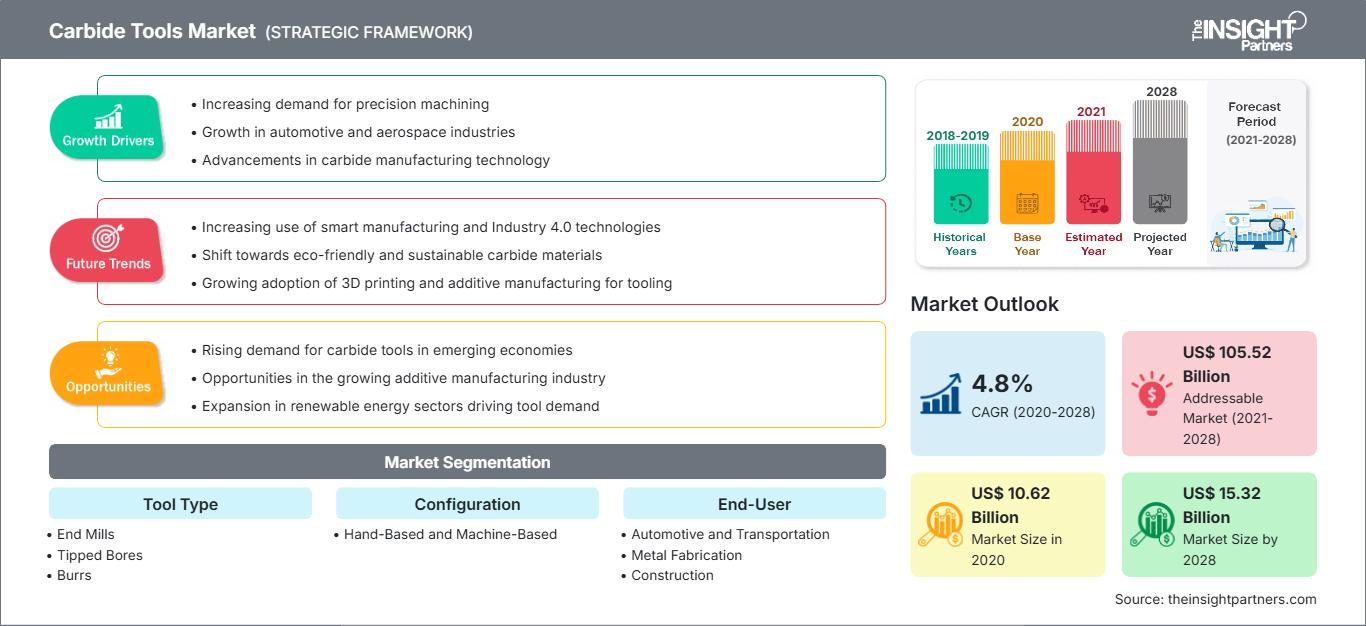

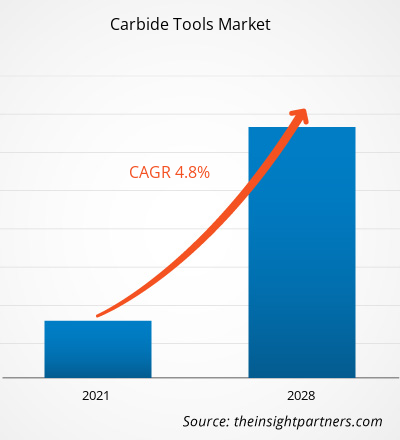

[Rapporto di ricerca]Il mercato degli utensili in metallo duro è stato valutato a 10.623,97 milioni di dollari nel 2020 e si prevede che raggiungerà i 15.320,99 milioni di dollari entro il 2028; si prevede una crescita a un CAGR del 4,8% dal 2021 al 2028.

I crescenti sviluppi nella progettazione della produzione e le crescenti esigenze di aumento dell'efficienza produttiva stanno gettando le basi per la ricerca da parte dei produttori di prodotti per macchine utensili di qualità superiore, incrementando così la domanda di utensili in metallo duro. Le macchine utensili utilizzate in tutti i settori sono principalmente impiegate per la lavorazione o la sagomatura di metalli o altri materiali rigidi per offrire una forma unica mediante alesatura, rettifica, cesoiatura e taglio. Attualmente, esistono due tipi principali di macchine utensili utilizzate in modo significativo in diversi settori: acciaio rapido (HSS) e utensili in metallo duro. Questi utensili sono ampiamente utilizzati in diverse applicazioni di lavorazione meccanica grazie alle loro caratteristiche significative, come l'alta velocità, i tempi di ciclo ridotti, la lunga durata, il mantenimento del tagliente ad alte temperature di lavorazione e l'eccezionale resistenza all'usura del tagliente. La crescente popolarità degli utensili in metallo duro, in particolare nelle applicazioni manifatturiere, è uno dei fattori significativi che si prevede stimolerà il mercato durante il periodo di previsione. Inoltre, questi utensili in metallo duro vengono utilizzati in unità produttive nei settori automobilistico, aerospaziale, ferroviario, dell'arredamento e della carpenteria, dell'energia e delle apparecchiature sanitarie. In questi settori, vengono utilizzati utensili da taglio speciali per progettare e realizzare un prodotto, il che sta incrementando la domanda di utensili in metallo duro. L'impiego di utensili in metallo duro in diversi settori, per l'azionamento manuale o automatico, sta ulteriormente stimolando la crescita del mercato degli utensili in metallo duro a livello globale.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato degli utensili in metallo duro: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

La pandemia di COVID-19 ha scosso diversi settori. L'enorme crescita della diffusione del virus ha spinto i governi di tutto il mondo a imporre severe restrizioni alla circolazione di veicoli e persone. A causa di divieti di viaggio, lockdown di massa e chiusure aziendali, la pandemia ha avuto un impatto negativo sulle economie e su innumerevoli settori in diversi paesi. L'imposizione del lockdown ha comportato una minore produzione di materie prime, beni e servizi. Pertanto, i settori manifatturiero, automobilistico, dei semiconduttori e dell'elettronica, petrolifero e del gas, minerario, aeronautico e altri hanno assistito a un calo delle loro attività a causa della temporanea chiusura delle attività.

Il lockdown mondiale per ridurre al minimo la trasmissione del virus ha interrotto significativamente le attività della catena di approvvigionamento e i volumi di produzione di diversi produttori, in particolare delle piccole e medie imprese. Inoltre, le attività produttive in diversi settori si sono contratte significativamente nel corso del 2020, con conseguente calo del mercato degli utensili in metallo duro. Tuttavia, con la crescente domanda di prodotti sanitari, la domanda di utensili in metallo duro sta aumentando vertiginosamente nel settore medico.

Approfondimenti sul mercato degli utensili in metallo duro: l'aumento della produzione nel settore automobilistico alimenta la crescita del mercato degli utensili in metallo duro

La produzione automobilistica è in costante crescita in tutto il mondo, in particolare nei paesi asiatici ed europei, il che sta alimentando la domanda di utensili in metallo duro. Il settore utilizza ampiamente utensili in metallo duro nella lavorazione dei metalli degli alberi motore, nella fresatura frontale e nella foratura, tra le altre lavorazioni meccaniche coinvolte nella produzione di componenti per auto. L'industria automobilistica sta ottenendo ottimi risultati con l'uso del carburo di tungsteno in giunti sferici, freni, alberi motore di veicoli ad alte prestazioni e altre parti meccaniche di veicoli sottoposti a un uso intenso e a temperature estreme. Giganti dell'automotive come Audi, BMW, Ford Motor Company e Range Rover stanno contribuendo in modo significativo alla crescita del mercato degli utensili in metallo duro. I veicoli elettrici ibridi stanno guadagnando terreno in Nord America, stimolando così la crescita del mercato degli utensili in metallo duro nella regione. Paesi come gli Stati Uniti e il Canada sono importanti produttori automobilistici nella regione. Secondo l'American Automotive Policy Council, le case automobilistiche e i loro fornitori contribuiscono per circa il 3% al PIL degli Stati Uniti. General Motors Company, Ford Motor Company, Fiat Chrysler Automobiles e Daimler sono tra i principali produttori automobilistici del Nord America. Secondo i dati dell'Organizzazione Internazionale dei Costruttori di Veicoli a Motore, nel 2019, Stati Uniti e Canada hanno prodotto rispettivamente circa 2.512.780 e circa 461.370 automobili. Inoltre, gli utensili in metallo duro sono ampiamente utilizzati anche nei settori ferroviario, aerospaziale e della difesa e marittimo.

Approfondimenti di mercato basati sulla tipologia di utensile

In base alla tipologia di utensile, il mercato degli utensili in metallo duro è segmentato in frese a candela, alesatori con punta, frese a disco, punte, frese e altri utensili. Nel 2020, il segmento delle frese ha rappresentato la quota maggiore del mercato.

Approfondimenti di mercato basati sulla configurazione

In base alla configurazione, il mercato degli utensili in metallo duro si divide in utensili manuali e utensili meccanici. Nel 2020, il segmento degli utensili meccanici ha rappresentato una quota di mercato maggiore.

Approfondimenti di mercato basati sull'utente finale

In base all'utente finale, il mercato degli utensili in metallo duro è segmentato in automotive e trasporti, lavorazione dei metalli, edilizia, petrolio e gas, macchinari pesanti e altri utenti finali. Nel 2020, il segmento automotive e trasporti ha rappresentato la quota maggiore del mercato.

Gli operatori che operano nel mercato degli utensili in metallo duro adottano strategie come fusioni, acquisizioni e iniziative di mercato per mantenere le proprie posizioni sul mercato. Di seguito sono elencati alcuni sviluppi dei principali attori:

- A novembre 2020, GARR TOOL ha stretto una partnership con Mastercam per offrire ai clienti una libreria completa di utensili, integrata nella piattaforma Mastercam. La partnership avrà un valore enorme per i clienti attuali e futuri, poiché il processo di produzione dipende sempre più dall'accesso immediato e semplice ai dati.

- A febbraio 2019, il Gruppo CERATIZIT ha acquisito il 50% delle azioni di Stadler Metalle GmbH & Co. KG. L'azienda ha dichiarato che l'investimento in Stadler ha consentito di garantire l'intera catena di fornitura delle materie prime e di concentrarsi ancora di più sul riciclo degli utensili in metallo duro nella fornitura di materie prime.

Le tendenze regionali e i fattori che influenzano il mercato degli utensili in metallo duro durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la geografia del mercato degli utensili in metallo duro in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America Meridionale e Centrale.

Ambito del rapporto di mercato degli utensili in metallo duro

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2020 | US$ 10.62 Billion |

| Dimensioni del mercato per 2028 | US$ 15.32 Billion |

| CAGR globale (2020 - 2028) | 4.8% |

| Dati storici | 2018-2019 |

| Periodo di previsione | 2021-2028 |

| Segmenti coperti |

By Tipo di utensile

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato degli utensili in metallo duro: comprendere il suo impatto sulle dinamiche aziendali

Il mercato degli utensili in metallo duro è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Mercato degli utensili in metallo duro Panoramica dei principali attori chiave

- Frese

- Fori con punta

- Base

- Trapani

- Frese

- Altri utensili

Per configurazione

- Manuali

- Macchine

Per utente finale

- Automotive e trasporti

- Fabbricazione di metalli

- Edilizia

- Petrolio e gas

- Macchinari pesanti

- Altri utenti finali

Per area geografica

- Nord America

- Stati Uniti

- Canada

- Messico

- Europa

- Francia

- Germania

- Italia

- Regno Unito

- Russia

- Resto d'Europa

- Asia Pacifico (APAC)

- Cina

- India

- Sud Corea

- Giappone

- Australia

- Resto dell'APAC

- Medio Oriente e Asia Africa (MEA)

- Sudafrica

- Arabia Saudita

- Emirati Arabi Uniti

- Resto del MEA

- Sud America (SAM)

- Brasile

- Argentina

- Resto del SAM

Profili aziendali

- Xinrui Industry Co., Ltd.

- CERATIZIT SA

- GARR TOOL

- Ingersoll Cutting Tool Company

- KYOCERA Precision Tools

- DIMAR GROUP

- MITSUBISHI MATERIALS Corporation

- Sandvik Coromant

- YG-1 Co., Ltd.

- Makita Corporation

Nivedita è una ricercatrice affermata con oltre 9 anni di esperienza in ricerche di mercato e consulenza aziendale. Attualmente Project Manager nel settore ICT presso The Insight Partners, vanta una profonda esperienza nella gestione e nell'esecuzione di incarichi di ricerca sindacati, personalizzati, in abbonamento e di consulenza in diversi settori tecnologici.

Con una comprovata esperienza nell'analisi basata sui dati e nella fornitura di insight fruibili, Nivedita ha contribuito in modo determinante a diversi progetti critici. Il suo lavoro include l'esecuzione end-to-end dei progetti, dalla comprensione degli obiettivi del cliente all'analisi delle tendenze di mercato, fino alla formulazione di raccomandazioni strategiche. Ha collaborato ampiamente con aziende leader nel settore ICT, aiutandole a identificare opportunità di mercato e a gestire i cambiamenti del settore.

Nivedita ha conseguito un MBA in Management presso IMS, Dehradun. Prima di entrare in The Insight Partners, ha maturato una preziosa esperienza presso MarketsandMarkets e Future Market Insights a Pune, dove ha ricoperto diversi ruoli di ricerca e ha costruito solide basi nell'analisi di settore e nel coinvolgimento dei clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative