Análisis y pronóstico del mercado de semillas forrajeras por tamaño, participación, crecimiento y tendencias para 2030

Datos históricos : | Año base : | Período de pronóstico :Análisis y pronósticos del mercado de semillas forrajeras por tamaño, participación, crecimiento y tendencias para 2030

- Estado : Publicada

- Código de informe : TIPRE00005662

- Categoría : Alimentos y bebidas

- Número de páginas : 200

- Formatos de informe disponibles :

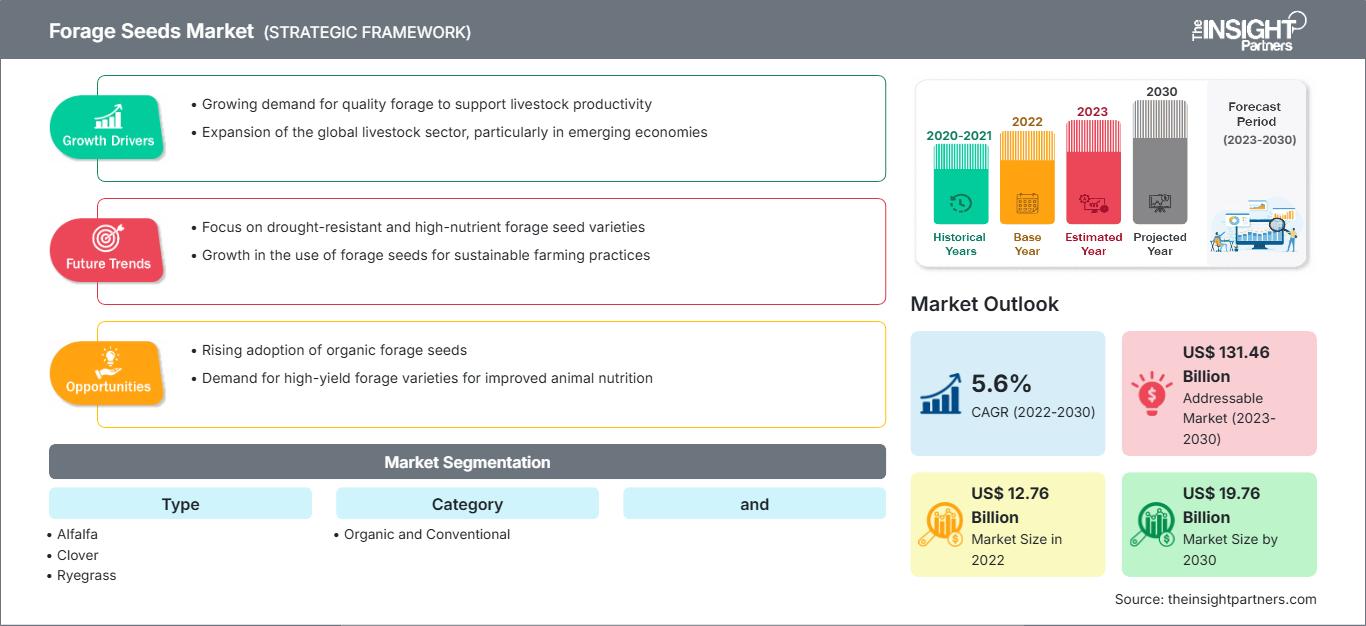

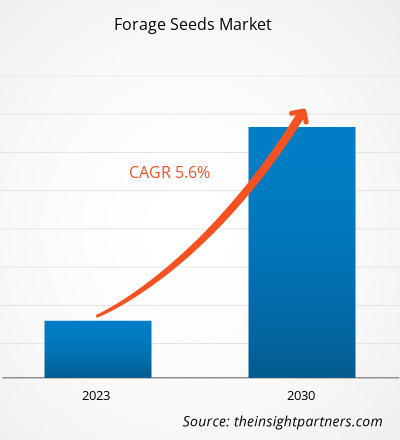

[Informe de investigación] Se espera que el mercado crezca de US$ 12.757,00 millones en 2022 a US$ 19.755,46 millones en 2030; se espera que registre una CAGR del 5,6% de 2022 a 2030.

Perspectivas del mercado y opinión de los analistas:

Los piensos convencionales suelen contener altas cantidades de sustancias químicas que perjudican la calidad de la carne al ser consumida por los animales. A largo plazo, el consumo de este tipo de carne provoca diversos trastornos de salud. Para solucionar este problema, los fabricantes están desarrollando piensos orgánicos sin aditivos químicos. Los animales que se alimentan de estos piensos ofrecen carne de alto valor nutricional. Por ello, los consumidores suelen considerar los productos orgánicos y naturales como alternativas más saludables a los productos convencionales. Los consumidores se inclinan principalmente por los productos orgánicos, lo que ha impulsado a los fabricantes a invertir considerablemente en productos elaborados con componentes orgánicos. Además, el acceso más accesible a información ilimitada a través de internet ha aumentado la concienciación de los consumidores sobre sus necesidades de salud, lo que ha impulsado la creciente demanda de piensos orgánicos. Por lo tanto, se espera que la creciente preferencia por los piensos orgánicos se convierta en una tendencia significativa en el mercado de semillas forrajeras durante el período de pronóstico.

Factores impulsores del crecimiento y desafíos:

Las mejoras tecnológicas en la genética de semillas ofrecen una oportunidad para el crecimiento del mercado mundial de semillas forrajeras. Los fabricantes de semillas han desarrollado diferentes variedades o características de semillas, como semillas híbridas, transgénicas, no transgénicas y orgánicas, gracias a los avances tecnológicos. La preferencia de los agricultores por estas variedades transgénicas está aumentando paulatinamente en diversas regiones forrajeras para minimizar las pérdidas de cultivos causadas por malezas y enfermedades, y mejorar la calidad de las semillas. Las semillas híbridas se desarrollan mediante la polinización cruzada, cuidadosamente controlada, de dos plantas progenitoras diferentes de la misma especie para producir nuevas características que no se pueden crear mediante la endogamia de dos plantas iguales. Generalmente, la polinización cruzada de las semillas híbridas se realiza manualmente.

Las semillas transgénicas se producen mediante ingeniería genética, alterando el material genético de un organismo. Se cultivan en laboratorios mediante técnicas biotecnológicas modernas. Por otro lado, las semillas no transgénicas se cultivan mediante polinización. Las semillas orgánicas se consideran semillas no transgénicas. Las semillas orgánicas se producen de forma natural sin pesticidas, fertilizantes ni ninguna otra sustancia química. Estas semillas son resistentes a las enfermedades y tienen una mayor capacidad para prosperar en condiciones adversas.

Estas técnicas de mejoramiento permiten el desarrollo de nuevas variedades de semillas con las características deseadas mediante la modificación del ADN de las semillas y las células vegetales. Estas mejoras tecnológicas ayudan a abordar los desafíos que enfrentan los agricultores durante el cultivo de semillas forrajeras. Por lo tanto, se espera que las constantes mejoras tecnológicas generen oportunidades lucrativas en el mercado de semillas forrajeras en los próximos años.

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de semillas forrajeras: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Segmentación y alcance del informe:

El mercado global de semillas forrajeras se segmenta según tipo, categoría, ganado y geografía. Según el tipo, el mercado de semillas forrajeras se segmenta en [alfalfa, trébol (blanco, rojo, híbrido y otros), raigrás (raigrás anual, raigrás perenne, raigrás italiano e híbrido), fleo, sorgo, bromo, trébol de patas de pájaro, caupí, festuca de los prados y otros]. Según la categoría, el mercado se segmenta en orgánico y convencional. Según el ganado, el mercado de semillas forrajeras se segmenta en rumiantes, aves de corral, cerdos y otros. El mercado de semillas forrajeras, según la geografía, está segmentado en América del Norte (EE. UU., Canadá y México), Europa (Alemania, Francia, Italia, Reino Unido, Rusia y el resto de Europa), Asia Pacífico (Australia, China, Japón, India, Corea del Sur y el resto de Asia Pacífico), Medio Oriente y África (Sudáfrica, Arabia Saudita, Emiratos Árabes Unidos y el resto de Medio Oriente y África) y América del Sur y Central (Brasil, Chile y el resto de América del Sur y Central).

Análisis segmentario:

En cuanto a la ganadería, el mercado de semillas forrajeras se segmenta en rumiantes, aves de corral, cerdos y otros. El segmento de rumiantes representó la mayor participación en el mercado de semillas forrajeras en 2022 y se espera que registre una tasa de crecimiento significativa durante el período de pronóstico. Los rumiantes incluyen ganado vacuno, ovino, caprino y búfalo. El forraje es la principal fuente de proteína, fibra y energía para los rumiantes. Las leguminosas forrajeras, como la alfalfa y el trébol, aportan el 75 % de la proteína cruda a los rumiantes. Las gramíneas forrajeras aportan grandes cantidades de fibra. El forraje también reduce el costo total de la alimentación ruminal. Por lo tanto, los ganaderos suelen utilizar forraje junto con los alimentos para animales. La creciente concienciación sobre la nutrición específica para rumiantes, especialmente vacas lecheras, cabras y ovejas, y ganado vacuno de carne, está impulsando la demanda de forraje, impulsando así el crecimiento del mercado de semillas forrajeras.

Análisis regional:

Según la geografía, el mercado de semillas forrajeras se segmenta en cinco regiones clave: Norteamérica, Europa, Asia Pacífico, Sudamérica y Centroamérica, y Oriente Medio y África. El mercado mundial de semillas forrajeras estuvo dominado por Norteamérica y se estimó en unos 5.000 millones de dólares estadounidenses en 2022. Norteamérica es uno de los mercados más importantes para las semillas forrajeras debido a la creciente demanda de forraje como alimento, el consumo de carne y las condiciones climáticas, así como al creciente consumo de productos pecuarios a pesar del aumento de los precios, la sólida consolidación de la industria de alimentos para animales y la agricultura. El creciente número de personas que optan por productos ricos en proteínas y más saludables, el aumento de la renta disponible, los cambios en el estilo de vida y los hábitos alimentarios contribuyen al aumento de la demanda de carne rica en proteínas en Estados Unidos, Canadá y México. Por lo tanto, con el aumento del consumo de productos cárnicos, la demanda de alimentos para animales aumenta, impulsando aún más el mercado de semillas forrajeras. La región es una de las mayores productoras de alimentos para animales de la región. Según un informe de Alltech Global, en 2020, la región produjo más de 254 millones de toneladas métricas de alimentos para animales. La producción masiva de alimentos para animales en Norteamérica y la creciente preocupación por la seguridad alimentaria, especialmente en lo que respecta a la carne y los productos lácteos, han impulsado un mayor consumo de alimentos nutritivos para animales, como los forrajes, en la región.

Se espera que el aumento significativo de la ganadería en Norteamérica impulse la demanda de alimentos para animales, como forrajes, durante el período de pronóstico. Por ejemplo, según la Asociación de Forrajes y Pastoreo de Foothills, el inventario de ganado canadiense se situó en 12,29 millones de cabezas el 1 de julio de 2021, un 0,2 % más que el 1 de julio de 2020. Este aumento se atribuye a la creciente demanda de productos cárnicos frescos, que ha disparado la importación de ganado. Además, según el informe del Departamento de Agricultura de los Estados Unidos (UDSA), en 2021, Norteamérica registró más de 114 millones de cabezas de ganado vacuno y más de 109 millones de cabezas de cerdo en la región. Por lo tanto, el aumento del ganado vacuno y la creciente demanda de alimentos saludables impulsan la demanda de semillas de forraje en toda la región.

Desarrollos de la industria y oportunidades futuras:

A continuación se enumeran diversas iniciativas adoptadas por los actores clave que operan en el mercado de semillas forrajeras:

- En noviembre de 2022, UPL Ltd., proveedor global de soluciones agrícolas sostenibles, anunció que su empresa, Advanta Seeds UK, y Bunge firmaron un acuerdo para adquirir una participación del 20 % cada una en SEEDCORP|HO. Esta inversión se enmarca en el objetivo OpenAg del Grupo UPL de impulsar la colaboración para ofrecer un paquete completo de soluciones a los agricultores.

- En octubre de 2022, KKR, una firma de inversión global, y UPL Limited, un proveedor global de soluciones agrícolas, anunciaron la firma de acuerdos definitivos bajo los cuales KKR invertirá US$ 300 millones por una participación del 13,33% en Advanta Enterprises Limited, una subsidiaria de Ltd.

Impacto del COVID-19:

La pandemia de COVID-19 afectó las economías e industrias en varios países. Las prohibiciones de viaje, los confinamientos y los cierres de negocios en los principales países de América del Norte, Europa, Asia Pacífico (APAC), América del Sur y Central (SAM) y Oriente Medio y África (MEA) afectaron negativamente el crecimiento de varias industrias, incluyendo la industria agrícola y de alimentos para animales. El cierre de las unidades de fabricación perturbó las cadenas de suministro globales, los cronogramas de entrega, las actividades de fabricación y las ventas de diversos productos esenciales y no esenciales. Varias empresas anunciaron posibles retrasos en las entregas de productos y una caída en las ventas futuras de sus productos en 2020. Además, las prohibiciones impuestas por varios gobiernos en Europa, Asia y América del Norte a los viajes internacionales obligaron a las empresas a suspender temporalmente sus planes de colaboración y asociación. Todos estos factores obstaculizaron la industria de alimentos para animales en 2020 y principios de 2021, restringiendo así el crecimiento del mercado de semillas forrajeras.

Perspectivas regionales del mercado de semillas forrajeras

Los analistas de The Insight Partners han explicado detalladamente las tendencias regionales y los factores que influyen en el mercado de semillas forrajeras durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de semillas forrajeras en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

Alcance del informe de mercado de semillas forrajeras

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2022 | US$ 12.76 mil millones |

| Tamaño del mercado en 2030 | US$ 19.76 mil millones |

| CAGR global (2022-2030) | 5,6% |

| Datos históricos | 2020-2021 |

| Período de pronóstico | 2023-2030 |

| Segmentos cubiertos |

Por tipo

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de semillas forrajeras: comprensión de su impacto en la dinámica empresarial

El mercado de semillas forrajeras está creciendo rápidamente, impulsado por la creciente demanda del consumidor final debido a factores como la evolución de las preferencias del consumidor, los avances tecnológicos y un mayor conocimiento de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades del consumidor y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

- Obtenga una descripción general de los principales actores clave del mercado de semillas forrajeras

Panorama competitivo y empresas clave:

UPL Ltd, DLF Seeds AS, Corteva Inc, Limagrain UK Ltd, S&W Seed Co, Deutsche Saatveredelung AG, Cerience, Allied Seed LLC, MAS Seeds SA y Syngenta AG se encuentran entre los principales actores del mercado global de semillas forrajeras. Estos fabricantes ofrecen soluciones de semillas de vanguardia con características innovadoras para brindar una experiencia superior a los agricultores y su ganado.

- Análisis histórico (2 años), año base, pronóstico (7 años) con CAGR

- Análisis PEST y FODA

- Tamaño del mercado, valor/volumen: global, regional y nacional

- Industria y panorama competitivo

- Conjunto de datos de Excel

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias

Desbloquea descuentos exclusivos en informes

Consultar ahora

Obtenga una muestra gratuita para - Mercado de semillas forrajeras

Obtenga una muestra gratuita para - Mercado de semillas forrajeras