Crecimiento del mercado de dispositivos de acceso vascular y tendencias recientes hasta 2031

Datos históricos : 2021-2023 | Año base : 2024 | Período de pronóstico : 2025-2031Tamaño y pronóstico del mercado de dispositivos de acceso vascular (2021-2031), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tipo de producto (catéteres intravenosos periféricos cortos, catéteres de línea media, catéteres centrales de inserción periférica (PICC), catéteres centrales, puertos implantables y accesorios), aplicación (administración de fármacos, administración de líquidos y nutrición, transfusión de hemoderivados y otros), vía de inserción (subcutánea e intravenosa), usuario final (hospitales y clínicas, centros de cirugía ambulatoria y otros) y geografía.

- Estado : Datos publicados

- Código de informe : TIPHE100000983

- Categoría : Ciencias de la vida

- Número de páginas : 150

- Formatos de informe disponibles :

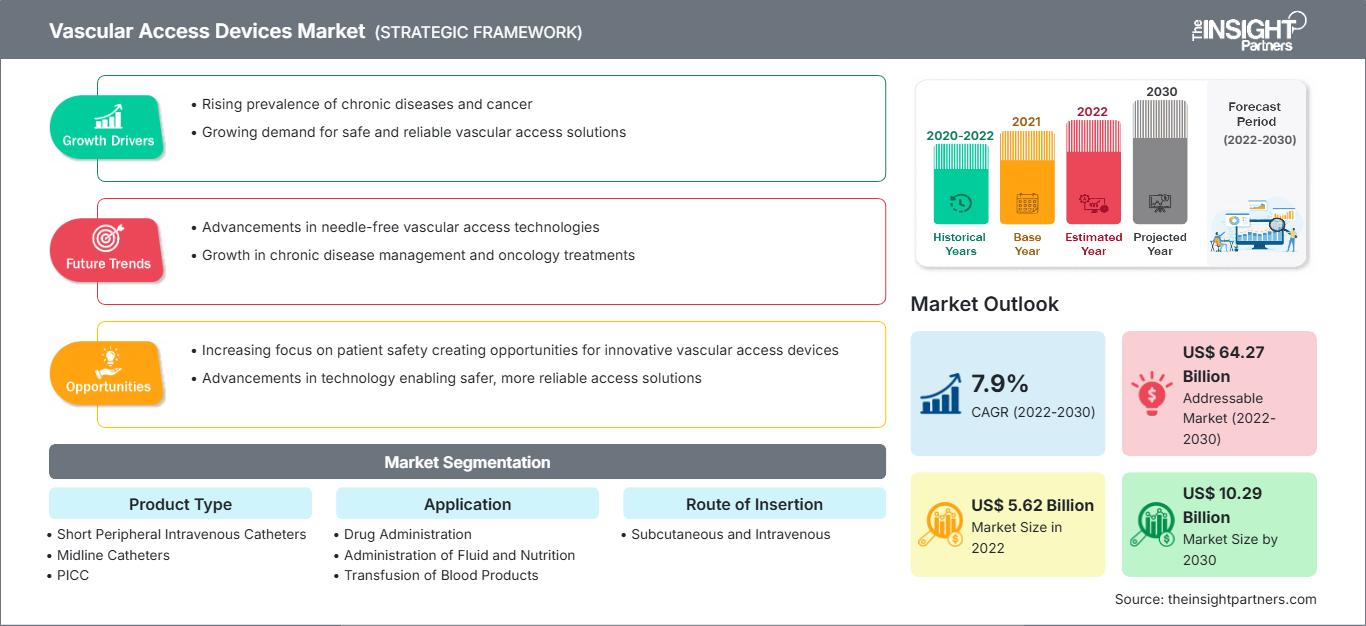

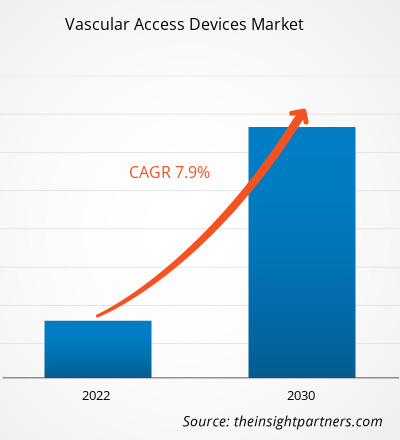

Se espera que el tamaño del mercado de dispositivos de acceso vascular alcance los US$ 7.33 mil millones para 2031. Se anticipa que el mercado registre una CAGR del 6,1% durante 2025-2031.

Perspectivas del mercado y opinión de los analistas:

Los dispositivos de acceso vascular se colocan en diversos puntos anatómicos para acceder a la vena cava superior o inferior: vena yugular interna, vena subclavia, vena yugular externa y vena femoral. El creciente tamaño del mercado de dispositivos de acceso vascular se debe a la creciente prevalencia de enfermedades crónicas y a la creciente necesidad de tratamientos de quimioterapia. Además, las iniciativas estratégicas de las empresas para mantenerse competitivas en el mercado impulsan el crecimiento del mercado. Es probable que un aumento significativo en el uso de dispositivos de acceso venoso robóticos basados en IA impulse nuevas tendencias en el mercado de dispositivos de acceso vascular durante el período de pronóstico.

Factores impulsores del crecimiento y desafíos:

La quimioterapia es un tratamiento primario o adyuvante que se utiliza para reducir o eliminar tumores mediante la administración de fármacos potentes. Por lo tanto, el aumento de casos de cáncer impulsa la demanda de procedimientos de quimioterapia. Según estimaciones de la Agencia Internacional para la Investigación del Cáncer (IARC), en 2020 se notificaron 19,3 millones de nuevos casos de cáncer a nivel mundial y se produjeron aproximadamente 10 millones de muertes debido a la enfermedad. Según el Registro Nacional del Cáncer (NCR), en Sudáfrica se diagnosticaron alrededor de 110.000 nuevos casos de cáncer, con más de 56.000 muertes relacionadas con el cáncer en 2020. Además, se proyecta que la carga de morbilidad aumentará en las próximas décadas, con un aumento estimado de 138.000 y 175.000 nuevos casos de cáncer para 2030 y 2040, respectivamente, mientras que la mortalidad relacionada con el cáncer aumentará a 73.000 y 94.000 en dichos años. Por lo tanto, la creciente prevalencia del cáncer impulsa el crecimiento del mercado de dispositivos de acceso vascular.

Personalice este informe según sus necesidades

Obtenga PERSONALIZACIÓN GRATUITAMercado de dispositivos de acceso vascular: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Segmentación y alcance del informe:

El análisis del mercado de dispositivos de acceso vascular se ha llevado a cabo considerando los siguientes segmentos: tipo de producto, aplicación, vía de inserción, usuario final y geografía. El mercado, por tipo de producto, está segmentado en catéteres intravenosos periféricos cortos, catéteres de línea media, PICC (catéteres centrales de inserción periférica), catéteres centrales, puertos implantables y accesorios. El mercado para el segmento de catéter central está segmentado a su vez en CICC (catéter central de inserción central), FICC (catéter central de inserción femoral) y otros. Según la aplicación, el mercado de dispositivos de acceso vascular está segmentado en administración de fármacos, administración de líquidos y nutrición, transfusión de productos sanguíneos y otros. Según la vía de inserción, el mercado se bifurca en subcutáneo e intravenoso. Según los usuarios finales, el mercado está segmentado en hospitales y clínicas, centros de cirugía ambulatoria y otros. El alcance del informe del mercado de dispositivos de acceso vascular abarca América del Norte (EE. UU., Canadá y México), Europa (España, Reino Unido, Alemania, Francia, Italia y el resto de Europa), Asia Pacífico (Corea del Sur, China, Japón, India, Australia y el resto de Asia Pacífico), Medio Oriente y África (Sudáfrica, Arabia Saudita, Emiratos Árabes Unidos y el resto de Medio Oriente y África) y América del Sur y Central (Brasil, Argentina y el resto de América del Sur y Central).

Análisis segmentario:

El mercado de dispositivos de acceso vascular, por tipo de producto, se segmenta en catéteres intravenosos periféricos cortos, catéteres de línea media, catéteres centrales de inserción periférica (PICC), catéteres centrales, puertos implantables y accesorios. El mercado del segmento de catéteres centrales se subdivide en catéteres centrales de inserción central (CICC), catéteres centrales de inserción femoral (FICC) y otros. En 2022, el segmento de catéteres intravenosos periféricos cortos representó la mayor cuota de mercado de dispositivos de acceso vascular, y se espera que este segmento registre la mayor tasa de crecimiento anual compuesta (TCAC) entre 2022 y 2030.

Según la aplicación, el mercado de dispositivos de acceso vascular se segmenta en administración de fármacos, administración de fluidos y nutrición, transfusión de hemoderivados, entre otros. En 2022, el segmento de administración de fármacos tuvo la mayor participación y se proyecta que registre la mayor tasa de crecimiento anual compuesta (TCAC) entre 2022 y 2030.

Según la vía de inserción, el mercado de dispositivos de acceso vascular se divide en subcutáneo e intravenoso. El segmento intravenoso tuvo una mayor cuota de mercado en 2022 y se prevé que registre una tasa de crecimiento anual compuesta (TCAC) más alta entre 2022 y 2030.

Por usuario final, el mercado se segmenta en hospitales y clínicas, centros de cirugía ambulatoria y otros. Se prevé que el mercado de dispositivos de acceso vascular para hospitales y clínicas crezca entre 2022 y 2030.

Análisis regional:

Norteamérica es el mayor contribuyente al crecimiento del mercado global de dispositivos de acceso vascular. Se prevé que Asia Pacífico registre la tasa de crecimiento anual compuesta (TCAC) más alta del mercado durante el período 2022-2030. Norteamérica tuvo la mayor participación en el mercado global en 2022 debido a la creciente prevalencia de enfermedades crónicas, el aumento de la población geriátrica, la presencia de actores clave del mercado involucrados en el desarrollo de productos nuevos y existentes, y el auge de los avances tecnológicos. En Norteamérica, Estados Unidos tuvo la mayor participación de mercado en 2022.

Perspectivas regionales del mercado de dispositivos de acceso vascular

Los analistas de The Insight Partners han explicado detalladamente las tendencias regionales y los factores que influyen en el mercado de dispositivos de acceso vascular durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de dispositivos de acceso vascular en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

Alcance del informe de mercado de dispositivos de acceso vascular

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2024 | XX mil millones de dólares estadounidenses |

| Tamaño del mercado en 2031 | US$ 7.33 mil millones |

| CAGR global (2025-2031) | 6,1% |

| Datos históricos | 2021-2023 |

| Período de pronóstico | 2025-2031 |

| Segmentos cubiertos |

Por tipo de producto

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de dispositivos de acceso vascular: comprensión de su impacto en la dinámica empresarial

El mercado de dispositivos de acceso vascular está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y un mayor conocimiento de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

- Obtenga una descripción general de los principales actores clave del mercado de dispositivos de acceso vascular

Desarrollos de la industria y oportunidades futuras:

El pronóstico del mercado de dispositivos de acceso vascular se estima a partir de diversos hallazgos de investigación, tanto secundarios como primarios, como publicaciones de empresas clave, datos de asociaciones y bases de datos. Según los comunicados de prensa publicados por los principales actores del mercado, se enumeran algunas estrategias:

- En noviembre de 2023, BD (Becton, Dickinson, and Company) lanzó una nueva tecnología de extracción de sangre sin aguja, compatible con catéteres integrados, lo que contribuyó a hacer realidad la visión de la compañía de una hospitalización con una sola punción. El dispositivo de extracción de sangre sin aguja PIVO Pro presenta mejoras de diseño para lograr la compatibilidad con catéteres intravenosos periféricos integrados y largos, incluyendo el nuevo sistema de catéter intravenoso cerrado Nexiva con acceso intravenoso NearPort.

- En mayo de 2023, Teleflex Inc. lanzó dos nuevos dispositivos: el Arrow VPS Rhythm DLX y el estilete NaviCurve, diseñados para optimizar los procedimientos de inserción de catéteres PICC y reducir la probabilidad de complicaciones. El dispositivo VPS Rhythm DLX proporciona información en tiempo real sobre la ubicación de la punta del catéter mediante la actividad eléctrica cardíaca del paciente. El estilete NaviCurve presenta una curva anatómica y una punta flexible, diseñadas para autoorientarse a la anatomía del paciente, lo que facilita el avance del catéter PICC en la vena cava superior (VCS) y permite una inserción exitosa.

Panorama competitivo y empresas clave:

Teleflex Inc., BD, B. Braun SE, Terumo Medical Corporation, Medtronic, Fresenius Kabi, Baxter, Vygon SAS, Kimal y Access Vascular Inc. se encuentran entre las empresas destacadas que se describen en el informe de mercado de dispositivos de acceso vascular. Además, se han estudiado y analizado otras empresas para obtener una visión integral del mercado y su ecosistema. Estas empresas se centran en la expansión geográfica y el lanzamiento de nuevos productos para satisfacer la creciente demanda de los consumidores de todo el mundo y ampliar su gama de productos especializados. Su presencia global les permite atender a una amplia base de clientes, lo que facilita la expansión del mercado.

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis histórico (2 años), año base, pronóstico (7 años) con CAGR

- Análisis PEST y FODA

- Tamaño del mercado, valor/volumen: global, regional y nacional

- Industria y panorama competitivo

- Conjunto de datos de Excel

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias

Desbloquea descuentos exclusivos en informes

Consultar ahora

Obtenga una muestra gratuita para - Mercado de dispositivos de acceso vascular

Obtenga una muestra gratuita para - Mercado de dispositivos de acceso vascular