Marktwachstum und aktuelle Trends für Gefäßzugangsgeräte bis 2031

Marktgröße und Prognose für Gefäßzugangssysteme (2021–2031), globaler und regionaler Marktanteil, Trends und Wachstumspotenzialanalyse. Berichtsabdeckung: Nach Produkttyp (kurze periphere Venenkatheter, Midline-Katheter, PICC, zentrale Venenkatheter, implantierbare Portsysteme und Zubehör), Anwendung (Medikamentenverabreichung, Flüssigkeits- und Nährstoffzufuhr, Transfusion von Blutprodukten und Sonstiges), Einführungsweg (subkutan und intravenös), Endnutzer (Krankenhäuser und Kliniken, ambulante Operationszentren und Sonstiges) und Geografie.

- Status : Veröffentlichte Daten

- Berichtscode : TIPHE100000983

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : May 30, 2024

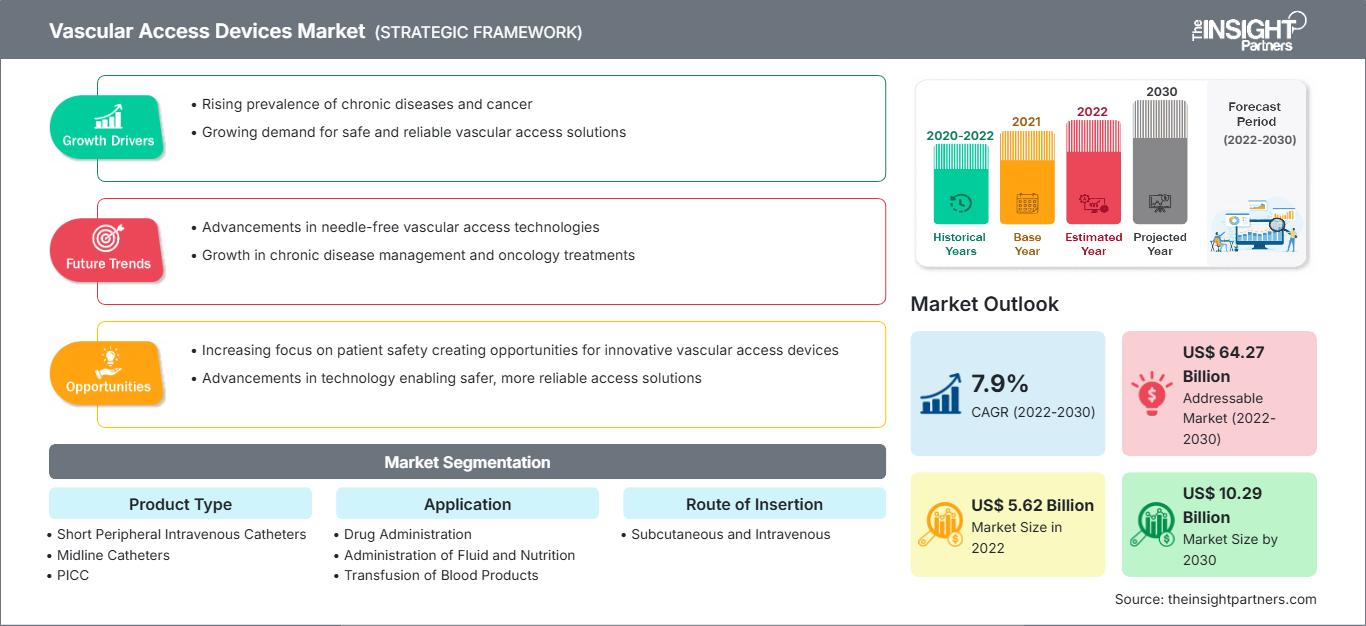

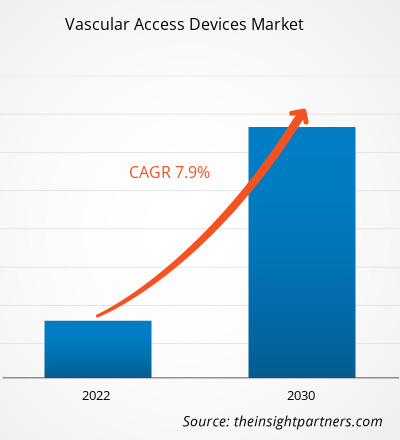

Es wird erwartet, dass der Markt für Gefäßzugangsgeräte bis 2031 ein Volumen von 7,33 Milliarden US-Dollar erreichen wird. Für den Zeitraum 2025–2031 wird ein durchschnittliches jährliches Wachstum von 6,1 % prognostiziert.

Markteinblicke und Analystenmeinung:

Gefäßzugangssysteme werden über verschiedene anatomische Stellen platziert, um die obere oder untere Hohlvene zu erreichen – die Vena jugularis interna, die Vena subclavia, die Vena jugularis externa und die Vena femoralis. Das Wachstum des Marktes für Gefäßzugangssysteme wird durch die zunehmende Verbreitung chronischer Erkrankungen und den steigenden Bedarf an Chemotherapien angetrieben. Darüber hinaus fördern strategische Initiativen von Unternehmen zur Sicherung ihrer Wettbewerbsfähigkeit das Marktwachstum. Ein deutlicher Anstieg des Einsatzes KI-gestützter robotergestützter Venenzugangssysteme dürfte im Prognosezeitraum neue Markttrends für Gefäßzugangssysteme mit sich bringen.

Wachstumstreiber und Herausforderungen:

Chemotherapie ist eine primäre oder adjuvante Behandlungsmethode, die Tumore durch die Verabreichung starker Medikamente verkleinert oder beseitigt. Die steigende Zahl von Krebserkrankungen treibt daher die Nachfrage nach Chemotherapien an. Laut Schätzungen der Internationalen Agentur für Krebsforschung (IARC) wurden im Jahr 2020 weltweit 19,3 Millionen neue Krebsfälle und etwa 10 Millionen Todesfälle durch Krebs gemeldet. Dem Nationalen Krebsregister (NCR) zufolge wurden in Südafrika im Jahr 2020 rund 110.000 neue Krebsfälle diagnostiziert, und es gab über 56.000 krebsbedingte Todesfälle. Darüber hinaus wird erwartet, dass die Krankheitslast in den kommenden Jahrzehnten zunimmt. Schätzungen zufolge werden die neuen Krebsfälle bis 2030 auf 138.000 und bis 2040 auf 175.000 steigen, während die krebsbedingte Sterblichkeit in den genannten Jahren auf 73.000 bzw. 94.000 ansteigen wird. Die zunehmende Verbreitung von Krebs treibt somit das Wachstum des Marktes für Gefäßzugangssysteme an.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Gefäßzugangsgeräte: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Berichtssegmentierung und -umfang:

Die Marktanalyse für Gefäßzugangssysteme wurde unter Berücksichtigung der folgenden Segmente durchgeführt: Produkttyp, Anwendung, Einführungsweg, Endnutzer und geografische Lage. Nach Produkttyp ist der Markt in kurze periphere Venenkatheter, Midline-Katheter, PICC (peripher eingeführte zentrale Katheter), zentrale Katheter, implantierbare Portsysteme und Zubehör unterteilt. Der Markt für zentrale Katheter ist weiter unterteilt in CICC (zentral eingeführte zentrale Katheter), FICC (femoral eingeführte zentrale Katheter) und Sonstige. Basierend auf der Anwendung ist der Markt für Gefäßzugangssysteme in Medikamentenverabreichung, Flüssigkeits- und Nährstoffzufuhr, Transfusion von Blutprodukten und Sonstige unterteilt. Nach Einführungsweg ist der Markt in subkutan und intravenös unterteilt. Basierend auf den Endnutzern ist der Markt in Krankenhäuser und Kliniken, ambulante Operationszentren und Sonstige unterteilt. Der Bericht über den Markt für Gefäßzugangsgeräte umfasst Nordamerika (USA, Kanada und Mexiko), Europa (Spanien, Großbritannien, Deutschland, Frankreich, Italien und das übrige Europa), den asiatisch-pazifischen Raum (Südkorea, China, Japan, Indien, Australien und das übrige Asien-Pazifik), den Nahen Osten und Afrika (Südafrika, Saudi-Arabien, die VAE und der übrige Nahe Osten und Afrika) sowie Süd- und Mittelamerika (Brasilien, Argentinien und das übrige Süd- und Mittelamerika).

Segmentanalyse:

Der Markt für Gefäßzugangssysteme ist nach Produkttyp in kurze periphere Venenkatheter, Midline-Katheter, PICC (peripher eingeführte zentrale Katheter), zentrale Katheter, implantierbare Portsysteme und Zubehör unterteilt. Der Markt für zentrale Katheter gliedert sich weiter in CICC (zentral eingeführte zentrale Katheter), FICC (femoral eingeführte zentrale Katheter) und Sonstige. Im Jahr 2022 entfiel der größte Marktanteil auf kurze periphere Venenkatheter, und für dieses Segment wird im Zeitraum 2022–2030 die höchste durchschnittliche jährliche Wachstumsrate (CAGR) erwartet.

Basierend auf der Anwendung ist der Markt für Gefäßzugangssysteme in die Segmente Medikamentenverabreichung, Verabreichung von Flüssigkeiten und Nährstoffen, Transfusion von Blutprodukten und Sonstiges unterteilt. Im Jahr 2022 hatte das Segment Medikamentenverabreichung den größten Marktanteil und wird voraussichtlich im Zeitraum 2022–2030 die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen.

Basierend auf dem Applikationsweg wird der Markt für Gefäßzugangssysteme in subkutane und intravenöse Systeme unterteilt. Das intravenöse Segment hatte 2022 einen größeren Marktanteil und wird voraussichtlich im Zeitraum 2022–2030 eine höhere durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen.

Nach Endnutzer ist der Markt in Krankenhäuser und Kliniken, ambulante Operationszentren und Sonstige unterteilt. Der Markt für Gefäßzugangsgeräte im Segment Krankenhäuser und Kliniken dürfte im Zeitraum 2022–2030 wachsen.

Regionalanalyse:

Nordamerika trägt am meisten zum Wachstum des globalen Marktes für Gefäßzugangssysteme bei. Für den asiatisch-pazifischen Raum wird im Zeitraum 2022–2030 die höchste durchschnittliche jährliche Wachstumsrate (CAGR) prognostiziert. Nordamerika hielt 2022 den größten Anteil am Weltmarkt, was auf die zunehmende Verbreitung chronischer Erkrankungen, die wachsende Zahl älterer Menschen, die Präsenz wichtiger Marktteilnehmer bei der Entwicklung neuer und bestehender Produkte sowie auf den technologischen Fortschritt zurückzuführen ist. Innerhalb Nordamerikas hatten die USA 2022 den größten Marktanteil.

Markt für Gefäßzugangsgeräte: Regionale Einblicke

Die regionalen Trends und Einflussfaktoren auf den Markt für Gefäßzugangssysteme im gesamten Prognosezeitraum wurden von den Analysten von The Insight Partners eingehend erläutert. Dieser Abschnitt behandelt außerdem die Marktsegmente und die geografische Verteilung des Marktes für Gefäßzugangssysteme in Nordamerika, Europa, Asien-Pazifik, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika.

Marktbericht über Gefäßzugangsgeräte – Umfang

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2024 | US$ XX Milliarden |

| Marktgröße bis 2031 | 7,33 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2025 - 2031) | 6,1 % |

| Historische Daten | 2021-2023 |

| Prognosezeitraum | 2025–2031 |

| Abgedeckte Segmente |

Nach Produkttyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Bereich vaskulärer Zugangsgeräte: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Gefäßzugangsgeräte wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile der Produkte. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen für die Bedürfnisse der Verbraucher und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

- Verschaffen Sie sich einen Überblick über die wichtigsten Akteure im Markt für Gefäßzugangsgeräte

Branchenentwicklungen und Zukunftschancen:

Die Marktprognose für Gefäßzugangsgeräte basiert auf verschiedenen Sekundär- und Primärforschungsergebnissen, darunter wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken. Laut Pressemitteilungen der wichtigsten Marktteilnehmer verfolgen diese unter anderem folgende Strategien:

- Im November 2023 brachte BD (Becton, Dickinson and Company) eine neue nadelfreie Blutentnahmetechnologie auf den Markt, die mit integrierten Kathetern kompatibel ist und so die Vision des Unternehmens von einem Krankenhausaufenthalt mit nur einem Stich ermöglicht. Das nadelfreie Blutentnahmegerät PIVO Pro zeichnet sich durch Designverbesserungen aus, die die Kompatibilität mit integrierten und langen peripheren Venenkathetern gewährleisten, einschließlich des neuen geschlossenen Venenkathetersystems Nexiva mit NearPort IV-Zugang.

- Im Mai 2023 brachte Teleflex Inc. zwei neue Medizinprodukte auf den Markt – das Arrow VPS Rhythm DLX-Gerät und den NaviCurve-Stylet –, die die PICC-Einlage optimieren und das Komplikationsrisiko verringern sollen. Das VPS Rhythm DLX-Gerät liefert in Echtzeit Informationen zur Katheterspitzenposition anhand der elektrischen Herzaktivität des Patienten. Der NaviCurve-Stylet verfügt über eine anatomische Krümmung und eine flexible Spitze, die sich selbstständig an die Patientenanatomie anpassen und so das Vorschieben des PICC in die obere Hohlvene (Vena cava superior, V. cava sup.) für eine erfolgreiche Insertion erleichtern.

Wettbewerbsumfeld und Schlüsselunternehmen:

Teleflex Inc., BD, B. Braun SE, Terumo Medical Corporation, Medtronic, Fresenius Kabi, Baxter, Vygon SAS, Kimal und Access Vascular Inc. gehören zu den führenden Anbietern von Gefäßzugangsgeräten, die im Marktbericht analysiert werden. Darüber hinaus wurden weitere Unternehmen untersucht und analysiert, um ein umfassendes Bild des Marktes und seines Ökosystems zu erhalten. Diese Unternehmen konzentrieren sich auf geografische Expansion und die Einführung neuer Produkte, um die weltweit steigende Nachfrage zu decken und ihr Produktportfolio im Spezialbereich zu erweitern. Ihre globale Präsenz ermöglicht es ihnen, einen großen Kundenstamm zu bedienen und so die Marktexpansion zu fördern.

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends