Taille, croissance et tendances du marché du verre ultra-mince d'ici 2034

Taille et prévisions du marché du verre ultra-mince (2021-2034), parts de marché mondiales et régionales, tendances et analyse des opportunités de croissance : Couverture du rapport : Par procédé de fabrication (flottaison et fusion), application (substrats pour semi-conducteurs, écrans plats et dispositifs de commande tactile, vitrages automobiles et autres), secteur d’utilisation finale (électronique grand public, automobile, médical et santé et autres) et zone géographique

- Statut : Données publiées

- Code du rapport : TIPRE00009965

- Catégorie : Produits chimiques et matériaux

- Nombre de pages : 150

- Formats de rapport disponibles :

- Date de dernière mise à jour : June 11, 2026

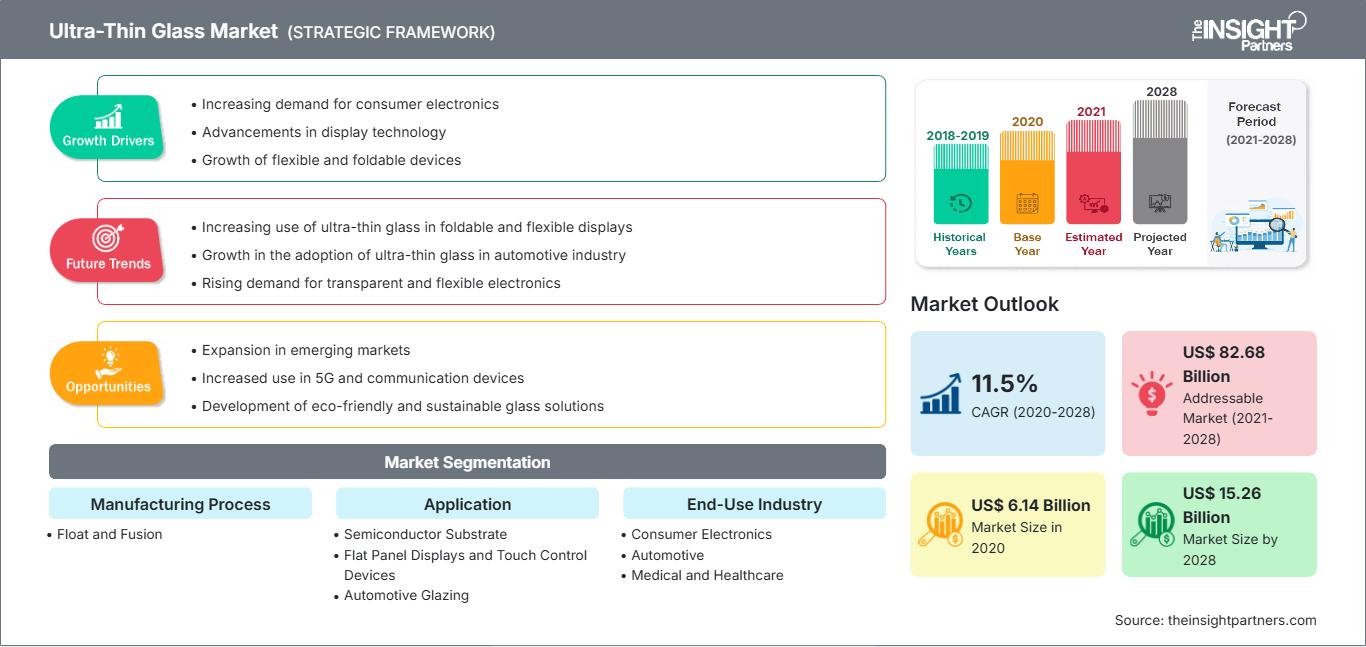

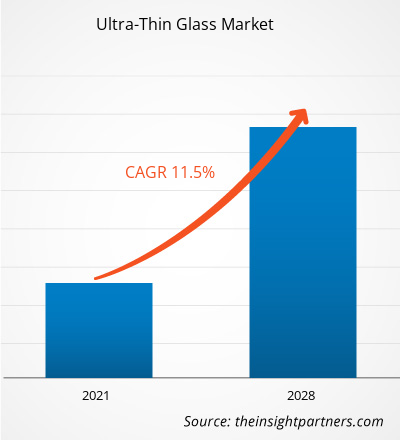

Le marché mondial du verre ultra-mince devrait atteindre 55,85 milliards de dollars américains d'ici 2034, contre 23,44 milliards de dollars américains en 2025. Ce marché devrait enregistrer un TCAC de 10,13 % au cours de la période de prévision 2026-2034.

Les principaux facteurs de croissance du marché incluent un intérêt mondial croissant pour les composants électroniques légers et performants, une prise de conscience accrue des consommateurs quant à la durabilité et la résistance aux rayures supérieures du verre par rapport aux polymères plastiques, et une évolution significative vers des architectures d'appareils pliables et flexibles. Par ailleurs, le marché devrait bénéficier de la popularité grandissante des véhicules électriques dotés de cockpits intelligents intégrés, de l'augmentation des besoins en matière de conditionnement des semi-conducteurs pour les technologies 5G et d'intelligence artificielle, ainsi que de l'intégration croissante du verre ultra-mince dans des segments médicaux à forte valeur ajoutée tels que les biocapteurs de diagnostic et les dispositifs de surveillance de la santé portables.

Analyse du marché du verre ultra-mince

L'analyse du marché du verre ultra-mince révèle une évolution vers des substrats fonctionnels à haute valeur ajoutée, les fabricants privilégiant la clarté optique et la flexibilité mécanique. Le marché se diversifie, s'étendant aux secteurs traditionnels de l'automobile et de l'affichage, dominés par le verre flotté, ainsi qu'aux marchés en forte croissance du verre étiré par fusion pour l'électronique pliable haut de gamme. Des opportunités stratégiques émergent dans les applications spécialisées des semi-conducteurs et des biotechnologies, où la stabilité thermique et la résistance chimique supérieures du verre ultra-mince par rapport aux alternatives organiques offrent un avantage concurrentiel indéniable. L'expansion du marché repose sur la maîtrise du rendement lors de la découpe de précision et sur l'intégrité des systèmes de manutention automatisés pour les feuilles ultra-fragiles. La différenciation concurrentielle repose désormais sur des techniques de renforcement exclusives, telles que le traitement chimique par échange d'ions, et sur la capacité à fournir des revêtements multifonctionnels antireflets et anti-traces de doigts. Cette approche permet aux fabricants de verre haut de gamme de pratiquer des prix plus élevés sur un marché exigeant une précision technique extrême.

Aperçu du marché du verre ultra-mince

Le verre ultra-mince, autrefois cantonné aux applications de laboratoire, est désormais omniprésent dans l'industrie de la haute technologie. Le marché comprend notamment le verre de protection ultra-flexible pour smartphones, les substrats haute fréquence pour l'encapsulation de puces et les vitrages légers pour les secteurs de l'aérospatiale et de l'automobile. Conglomérats verriers internationaux et entreprises spécialisées en science des matériaux se disputent ce marché, utilisant des techniques de fabrication avancées pour produire un verre plus fin qu'un cheveu. La demande croissante d'appareils électroniques plus fins et plus portables, émanant de consommateurs férus de technologie en Asie-Pacifique et en Amérique du Nord, a contribué à la popularité du verre ultra-mince comme solution de protection et d'interface de premier plan. L'Asie-Pacifique domine le marché en termes de chiffre d'affaires grâce à son pôle de production électronique bien établi, tandis que l'Amérique du Nord progresse dans les applications aérospatiales et l'innovation en matière de dispositifs médicaux. Le marché mondial est le plus développé dans les régions à forte concentration de production d'écrans, grâce à la large disponibilité des technologies OLED et Micro-LED. La concurrence entre les marques stimule l'innovation dans la composition du verre, conduisant à l'intégration de variantes spécialisées en aluminosilicate et en borosilicate. Le marché américain est un pôle majeur d'innovation en matière de matériaux, soutenu par un écosystème de semi-conducteurs robuste et une forte concentration de géants de l'électronique grand public. La demande intérieure se concentre de plus en plus sur les appareils pliables et les solutions d'encapsulation avancées pour les semi-conducteurs. Les investissements stratégiques dans les sites de production locaux favorisent l'adoption de substrats en verre de haute précision.

Personnalisez ce rapport selon vos besoins.

Bénéficiez d'une PERSONNALISATION GRATUITEMarché du verre ultra-mince : Perspectives stratégiques

-

Découvrez les principales tendances du marché présentées dans ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Facteurs de croissance et opportunités du marché du verre ultra-mince

Facteurs de marché :

- Performances optiques et mécaniques supérieures : le verre ultra-mince offre une meilleure transparence et un toucher plus agréable que les films plastiques. Sa résistance à la chaleur et aux produits chimiques le rend idéal pour les processus de fabrication rigoureux des écrans haute définition modernes.

- La démocratisation des appareils pliables : L’essor des smartphones et ordinateurs portables pliables a maintenu une forte demande en écrans en verre flexible. À mesure que les consommateurs adoptent ces appareils, le verre ultra-fin continue de gagner des parts de marché de manière stable par rapport aux polyimides plastiques.

- Expansion rapide de la 5G et des technologies des semi-conducteurs : la transmission de données à haute fréquence exige des substrats à faibles pertes diélectriques. Le verre ultra-mince est de plus en plus utilisé dans les boîtiers de semi-conducteurs avancés pour soutenir l’infrastructure de la 5G et le calcul haute vitesse.

Opportunités de marché :

- Expansion dans le vitrage automobile et les intérieurs intelligents : au-delà des appareils portables, le verre ultra-mince offre des opportunités importantes dans les vitres légères et les écrans de tableau de bord incurvés à grande échelle pour les véhicules électriques de nouvelle génération.

- Croissance dans les segments médicaux et biotechnologiques : la mise en place de partenariats stratégiques entre les fabricants de verre et les entreprises de dispositifs médicaux pourrait faciliter l’accès aux segments à forte marge des diagnostics au point de soins, où le verre ultra-mince sert de substrat stable pour les puces microfluidiques.

- Diversification vers les énergies durables : Les producteurs ont de plus en plus d’opportunités de cibler le secteur des énergies renouvelables grâce à un verre léger et flexible destiné aux systèmes photovoltaïques intégrés au bâtiment (BIPV) et aux chargeurs solaires portables.

Analyse de segmentation du rapport sur le marché du verre ultra-mince

Le marché du verre ultra-mince est analysé selon différents segments afin de mieux comprendre sa structure, son potentiel de croissance et les tendances émergentes. Voici l'approche de segmentation standard utilisée dans la plupart des rapports sectoriels :

Par procédé de fabrication :

- Flottant : Le principal moteur de volume, notamment dans les secteurs du vitrage automobile et des écrans grand format, grâce à des capacités de production à grand volume bien établies et à des économies d’échelle dans la production de verre d’une épaisseur minimale de 0,1 mm.

- Fusion : un segment technique en pleine expansion qui produit du verre d’une qualité de surface et d’une épaisseur exceptionnelles. Ce procédé est de plus en plus privilégié pour les applications électroniques haut de gamme exigeant des surfaces tactiles impeccables, sans polissage supplémentaire.

Sur demande :

- Écrans plats et dispositifs à commande tactile : Ils restent le principal canal d’utilisation du verre ultra-mince, bénéficiant de la demande mondiale de smartphones, de tablettes et de téléviseurs haut de gamme.

- Substrat semi-conducteur : le segment d’application qui connaît la croissance la plus rapide, notamment pour le conditionnement de puces haute densité et les interposeurs, permettant des composants électroniques plus compacts et plus efficaces.

- Vitrage automobile : Offre une gamme d’applications sélectionnées mais croissantes pour la réduction du poids et l’amélioration de l’esthétique intérieure dans la conception des véhicules modernes.

- Autres : Inclut des utilisations de niche dans les capteurs, les substrats biotechnologiques et les composants d'énergie solaire.

Par secteur d'utilisation finale :

- Électronique grand public : le secteur le plus important, porté par le cycle continu de miniaturisation des appareils et l’essor de la technologie des écrans pliables.

- Automobile : Un secteur en forte croissance, axé sur la réduction du poids à vide des véhicules et l'amélioration de la numérisation des habitacles.

- Secteur médical et de la santé : Utilise du verre ultra-mince pour des outils de diagnostic de haute précision, des lames de microscope et des capteurs médicaux portables.

- Autres : Englobe l'aérospatiale, la défense et la fabrication industrielle spécialisée.

Par géographie :

- Amérique du Nord

- Europe

- Asie-Pacifique

- Amérique du Sud et centrale

- Moyen-Orient et Afrique

Portée du rapport sur le marché du verre ultra-mince

| Attribut du rapport | Détails |

|---|---|

| Taille du marché en 2025 | 23,44 milliards de dollars américains |

| Taille du marché d'ici 2034 | 55,85 milliards de dollars américains |

| TCAC mondial (2026 - 2034) | 10,13% |

| Données historiques | 2021-2024 |

| Période de prévision | 2026-2034 |

| Segments couverts |

Par procédé de fabrication

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché du verre ultra-mince : comprendre son impact sur la dynamique commerciale

Le marché du verre ultra-mince connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux. Cette demande est alimentée par l'évolution des préférences des consommateurs, les progrès technologiques et une meilleure connaissance des avantages du produit. Face à cette demande grandissante, les entreprises diversifient leur offre, innovent pour répondre aux besoins des consommateurs et tirent parti des tendances émergentes, ce qui contribue à stimuler la croissance du marché.

Analyse des parts de marché du verre ultra-mince par zone géographique

La région Asie-Pacifique devrait connaître la croissance la plus rapide dans les années à venir. Les marchés émergents d'Amérique du Nord et d'Europe offrent également de nombreuses opportunités inexploitées pour les applications de verre haut de gamme dans les secteurs médical et automobile.

Le marché du verre ultra-mince connaît une transformation majeure, passant d'un composant électronique de niche à un matériau de haute technologie polyvalent. Cette croissance est alimentée par la forte demande en électronique flexible et l'expansion du secteur automobile haut de gamme. Vous trouverez ci-dessous un résumé des parts de marché et des tendances par région :

1. Amérique du Nord

- Part de marché : Un segment de niche en pleine expansion, porté par l’adoption précoce des appareils pliables et les applications aérospatiales haut de gamme.

-

Facteurs clés :

- Forte présence de pionniers technologiques mondiaux et marché établi des smartphones de luxe.

- Demande croissante d'interposeurs en verre dans le conditionnement des semi-conducteurs piloté par l'IA.

- Expansion des secteurs médical et diagnostique nécessitant des substrats en verre de haute pureté.

- Tendances : Investissements importants dans les applications biotechnologiques et généralisation du verre ultra-mince renforcé pour les dispositifs portables militaires et industriels.

2. Europe

- Part de marché : Détient une part substantielle, principalement grâce à l'industrie automobile de pointe et au secteur du verre architectural durable de la région.

-

Facteurs clés :

- Forte demande de vitrages légers et aérodynamiques de la part des géants de l'automobile en Allemagne et en France.

- Cadre de R&D établi pour les énergies renouvelables et les matériaux de construction économes en énergie.

- Des réglementations environnementales strictes incitent à réduire le poids des transports.

- Tendances : Une orientation stratégique vers les principes de l'économie circulaire, en privilégiant la recyclabilité du verre mince et son intégration dans les systèmes photovoltaïques intégrés au bâtiment (BIPV).

3. Asie-Pacifique

- Part de marché : Détient la plus grande part de marché au niveau mondial, grâce notamment aux pôles de fabrication électronique les plus importants au monde, situés en Chine, en Corée du Sud, à Taïwan et au Japon.

-

Facteurs clés :

- Concentration massive d'usines de production de panneaux OLED et Micro-LED.

- Initiatives gouvernementales pour l'autosuffisance en semi-conducteurs et l'infrastructure 5G.

- L'urbanisation rapide alimente la demande en technologies grand public haut de gamme et ultra-minces.

- Tendances : Un changement stratégique vers une production localisée de verre ultra-mince (UTG) pour réduire la dépendance à la chaîne d'approvisionnement, parallèlement à d'importants efforts de R&D dans la fabrication pour la découpe de verre à haut rendement.

4. Amérique du Sud et centrale

- Part de marché : Marché émergent avec une présence industrielle croissante au Brésil et au Chili.

-

Facteurs clés :

- Extension des chaînes de montage pour les marques régionales d'électronique grand public.

- Modernisation de la chaîne d'approvisionnement automobile pour inclure des interfaces intérieures numériques.

- Tendances : Augmentation des importations de feuilles de verre de haute technologie pour la finition locale des smartphones et hausse de la production de capteurs industriels spécialisés.

5. Moyen-Orient et Afrique

- Part de marché : Marché en développement en transition vers une production industrielle formalisée.

-

Facteurs clés :

- Investissements stratégiques dans les villes (par exemple, NEOM) nécessitant des solutions d'affichage et de vitrage avancées.

- Croissance du secteur de l'énergie solaire, notamment pour les panneaux légers et à haut rendement.

- Tendances : Mise en place de plateformes logistiques et de finition modernes pour combler le fossé entre la production asiatique et la demande de la zone EMEA.

Les principales entreprises opérant sur le marché du verre ultra-mince sont :

- Corning Incorporated

- AGC Inc.

- Nippon Electric Glass Co., Ltd.

- SCHOTT AG

- Central Glass Co., Ltd.

- CSG Holding Co., Ltd.

- Émerger le verre

- Nippon Sheet Glass Co., Ltd

- Xinyi Glass Holdings Limited

- Luoyang Glass Co., Ltd.

Avertissement : Les entreprises mentionnées ci-dessus ne sont classées dans aucun ordre particulier.

Actualités et développements récents du marché du verre ultra-mince

- En novembre 2025, Alpen High Performance Products (Alpen) a annoncé une collaboration avec Corning Incorporated, l'un des leaders mondiaux de l'innovation dans les domaines du verre, de la céramique et des matériaux. Dans le cadre de cette collaboration, Alpen utilisera le verre Corning® Enlighten™ comme vitrage central ultra-mince pour ses unités de triple et quadruple vitrage, contribuant ainsi à la commercialisation de fenêtres de nouvelle génération sur le marché américain.

- En septembre 2025, Nippon Electric Glass Co., Ltd. a annoncé que sa feuille de verre ultra-mince conçue exclusivement pour le renforcement chimique, Dinorex UTG™, avait été adoptée pour le revêtement de l'écran principal interne du dernier smartphone pliable de HONOR, le Magic V Flip2. HONOR est un fabricant d'appareils intelligents qui acquiert rapidement une reconnaissance mondiale.

Couverture et livrables du rapport sur le marché du verre ultra-mince

Le rapport « Taille et prévisions du marché du verre ultra-mince (2021-2034) » fournit une analyse détaillée du marché couvrant les domaines suivants :

- Taille et prévisions du marché du verre ultra-mince aux niveaux mondial, régional et national pour tous les segments de marché clés couverts par le périmètre de l'étude

- Tendances du marché du verre ultra-mince, ainsi que dynamique du marché, notamment les moteurs, les contraintes et les principales opportunités

- Analyse PEST et SWOT détaillée

- Analyse du marché du verre ultra-mince couvrant les principales tendances du marché, le cadre mondial et régional, les principaux acteurs, les réglementations et les développements récents du marché

- Analyse du paysage industriel et de la concurrence, incluant la concentration du marché, l'analyse par carte thermique, les principaux acteurs et les développements récents sur le marché du verre ultra-mince.

- Profils d'entreprise détaillés

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires