Rapporto di mercato sulla gestione autunnale 2031 per segmenti, geografia, dinamiche, sviluppi recenti e approfondimenti strategici

Dati storici : 2021-2022 | Anno base : 2023 | Periodo di previsione : 2024-2031Dimensioni e previsioni del mercato della gestione delle cadute (2021-2031), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per prodotto (cuscinetti sensori, tappetini, protezioni per i fianchi, sistemi di allarme, dispositivi di comunicazione e altri prodotti), applicazione (sistemi di rilevamento delle cadute, attrezzature per la prevenzione delle cadute e sistemi di monitoraggio e risposta post-caduta), fascia d'età [popolazione anziana (65 anni e oltre) e adulti (18-64 anni)], utente finale (ospedali e cliniche, case di cura, strutture di assistenza domiciliare e altri utenti finali) e geografia

- Stato : Edito

- Codice del report : TIPRE00010475

- Categoria : Scienze della vita

- Numero di pagine : 205

- Formati di report disponibili :

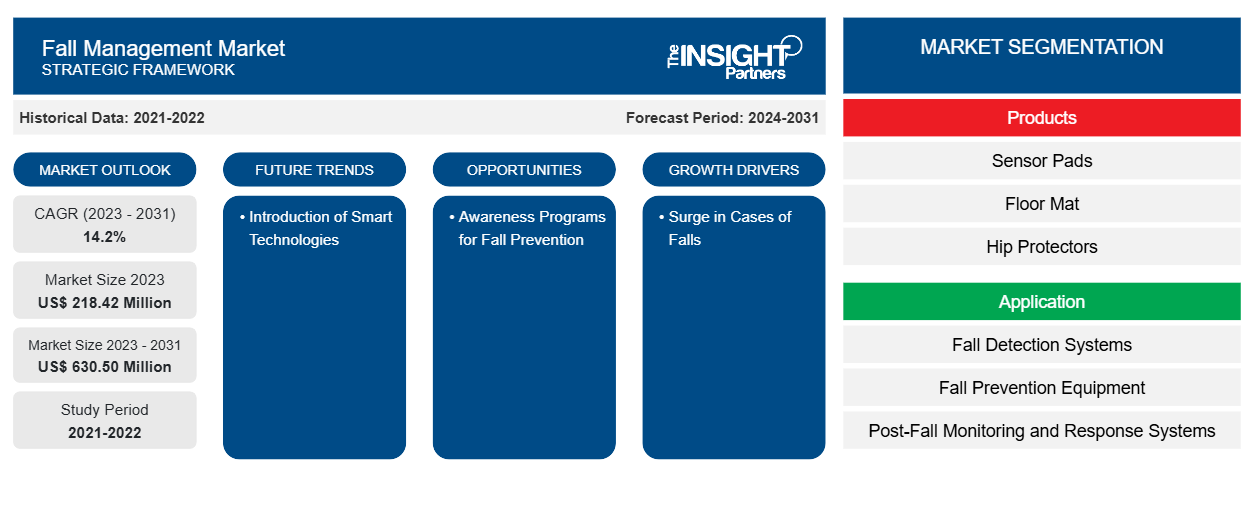

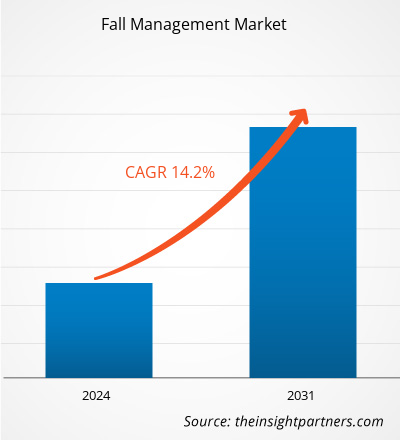

Si prevede che la dimensione del mercato della gestione delle cadute raggiungerà i 630,50 milioni di dollari entro il 2031, rispetto ai 218,42 milioni di dollari del 2023. Si stima che il mercato registrerà un CAGR del 14,2% nel periodo 2023-2031. È probabile che l'integrazione delle tecnologie intelligenti con la tecnologia delle camere bianche porti nuove tendenze sul mercato nei prossimi anni.

Analisi di mercato della gestione delle cadute

Una combinazione di pratiche basate sulle prove, progressi tecnologici e una crescente consapevolezza delle conseguenze delle cadute tra la popolazione anziana guida sempre di più la gestione delle cadute negli adulti. Con l'invecchiamento demografico, gli operatori sanitari riconoscono la necessità di strategie complete di prevenzione delle cadute che comprendano valutazione del rischio, modifiche ambientali ed educazione del paziente. L'implementazione di strumenti standardizzati di valutazione del rischio di caduta consente ai professionisti sanitari di identificare precocemente gli individui ad alto rischio, consentendo interventi personalizzati. Inoltre, l'integrazione della tecnologia, come sensori indossabili e dispositivi per la casa intelligente, offre notevoli opportunità per monitorare i modelli di movimento e fornire avvisi in tempo reale agli operatori sanitari, migliorando la sicurezza. I programmi educativi per pazienti e personale sanitario sono essenziali per promuovere una cultura di sicurezza e consapevolezza sui rischi di caduta. Le iniziative di coinvolgimento della comunità, come programmi di esercizi che migliorano l'equilibrio e la forza, rafforzano ulteriormente gli individui nell'adottare misure proattive. Poiché le politiche enfatizzano sempre di più l'assistenza incentrata sul paziente, esiste un'opportunità unica di collaborazione interdisciplinare per migliorare i protocolli di gestione delle cadute. Sfruttando questi driver e opportunità, i sistemi sanitari possono ridurre significativamente gli incidenti di caduta, migliorare i risultati per i pazienti e promuovere il benessere generale tra gli adulti, in particolare in contesti di assistenza a lungo termine e riabilitazione.

Panoramica del mercato della gestione delle cadute

Secondo l'Organizzazione Mondiale della Sanità (OMS), le cadute possono portare all'immobilità e al ricovero in case di cura, e sono anche la principale causa di mortalità in tutto il mondo. I Centers for Disease Control and Prevention (CDC) indicano le cadute come un fattore importante che colpisce le persone di età pari o superiore a 65 anni, causando gravi lesioni. Oltre 14 milioni, ovvero 1 anziano su 4, segnalano cadute di diversa intensità ogni anno. Secondo un rapporto pubblicato dalla Population Division delle Nazioni Unite, la popolazione geriatrica del mondo era di circa 600 milioni nel 2021, e si prevede che il numero raggiungerà ulteriormente i 2 miliardi entro il 2050. Inoltre, secondo le statistiche pubblicate dal CDC nel 2024, 1 caduta su 10 provoca lesioni negli anziani che comportano limitazioni nelle attività quotidiane da loro svolte per un giorno o più o li costringono a cercare assistenza medica. Ogni anno, gli anziani effettuano circa 3 milioni di visite al pronto soccorso per cercare cure per le cadute. Inoltre, in questa fascia demografica si verificano ogni anno circa 1 milione di ricoveri ospedalieri correlati a cadute. Le cadute sono anche la causa più comune di lesioni cerebrali traumatiche (TBI). Pertanto, l'incidenza crescente delle cadute insieme all'invecchiamento della popolazione richiede lo sviluppo di sistemi e soluzioni per la gestione delle cadute.

Le aziende stanno investendo in tecnologie avanzate per la prevenzione e il rilevamento delle cadute. A febbraio 2024, Dozee, una startup indiana, ha introdotto un'innovativa funzionalità Fall Prevention Alert (FPA) nel suo sistema di monitoraggio remoto dei pazienti (RPM) e di allerta precoce (EWS) senza contatto basato sull'intelligenza artificiale (AI). La funzionalità FPA è progettata per rivoluzionare la sicurezza dei pazienti negli ospedali. Securitas Healthcare è una delle aziende che offre soluzioni per monitorare e ridurre le cadute dei pazienti impiegando sistemi avanzati di allerta caduta. L'azienda collabora con partner fidati per migliorare la sicurezza dei pazienti negli ospedali aiutandoli a implementare protocolli efficaci di gestione delle cadute.

Secondo un articolo pubblicato nel Journal of Current Medical Research and Opinion nel 2021, scivolamenti, inciampi e cadute sono la seconda causa più comune di giornate lavorative perse nel settore sanitario degli Stati Uniti. Anche Hartford Financial Services Group annovera questi tre tra i tipi di reclami più comuni, rappresentando collettivamente il 66% di tutti i reclami nel settore sanitario . Pertanto, agiscono come una fonte significativa di perdite per molti settori. Gli operatori di mercato si stanno concentrando sulla fornitura di soluzioni di prevenzione delle cadute nelle strutture sanitarie. A marzo 2024, HD Nursing, leader nelle soluzioni per la sicurezza dei pazienti, ha stretto una partnership con WellnessMats, uno dei principali fornitori di soluzioni premium per la posizione eretta. Questa collaborazione mirava a migliorare il comfort e la sicurezza riducendo al contempo l'affaticamento e lo stress per gli operatori sanitari negli ospedali e nei sistemi sanitari. Tali collaborazioni e investimenti da parte delle aziende per gestire il crescente numero di incidenze di caduta alimenterebbero la crescita del mercato della gestione delle cadute durante il periodo di previsione.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato della gestione autunnale: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità di mercato per la gestione autunnale

La crescente preferenza per l'assistenza domiciliare rafforza la crescita del mercato

Poiché le popolazioni anziane preferiscono ricevere assistenza presso le proprie abitazioni, vi è una crescente attenzione alle soluzioni di gestione delle cadute adatte agli ambienti di assistenza domiciliare. Sistemi di allarme portatili e tappetini antiscivolo, specificamente progettati per uso residenziale, stanno diventando sempre più popolari tra gli operatori sanitari e le famiglie dei pazienti. I produttori si concentrano sulla facilità d'uso delle soluzioni di gestione delle cadute per gli ambienti di assistenza domiciliare, consentendo agli anziani di mantenere la propria indipendenza garantendo al contempo la propria sicurezza. Questa tendenza all'indipendenza riflette un movimento più ampio verso modelli di assistenza personalizzati che danno priorità al comfort e all'accessibilità nella gestione dei rischi per la salute a casa. A luglio 2024, Gamgee ha annunciato il lancio della protezione anticaduta Gamgee Wi-Fi per la sicurezza degli anziani. Questo innovativo sistema utilizza le reti Wi-Fi esistenti per fornire una soluzione completa per l'assistenza agli anziani. Risponde alla crescente domanda di sistemi efficaci di rilevamento delle cadute e di risposta alle emergenze, consentendo agli anziani di vivere in modo indipendente e sicuro nelle proprie case.

La personalizzazione dei programmi di prevenzione delle cadute sta diventando sempre più importante, poiché gli operatori sanitari riconoscono che le esigenze possono variare notevolmente tra i pazienti. Gli interventi personalizzati basati su specifici fattori di rischio, come limitazioni della mobilità o deficit cognitivi, stanno guadagnando terreno. È probabile che le strutture sanitarie implementino valutazioni complete che informino strategie di gestione delle cadute personalizzate per ciascun paziente. Questo approccio di personalizzazione delle soluzioni di gestione delle cadute per gli ambienti di assistenza domiciliare non solo migliora l'efficacia degli interventi, ma promuove anche un maggiore coinvolgimento del paziente nei propri piani di cura. Pertanto, la crescente preferenza per l'assistenza agli anziani a domicilio guida il progresso del mercato della gestione delle cadute.

Programmi di sensibilizzazione per la prevenzione delle cadute per creare opportunità di crescita

Si prevede che il mercato della gestione delle cadute crescerà con la crescente consapevolezza della necessità di prevenzione delle cadute tra operatori sanitari, pazienti e famiglie. Secondo un articolo pubblicato su PubMed Central a luglio 2021, il numero di beneficiari dei programmi di prevenzione delle cadute basati sulle prove (EBFPP) dell'Amministrazione per la vita comunitaria ha raggiunto oltre 85.000 anziani nel periodo 2014-2019. La partecipazione agli EBFPP ha portato a una maggiore sicurezza, a una minore paura di cadere e a una riduzione sia delle cadute che delle cadute con lesioni. Inoltre, le campagne educative che sottolineano il rischio di cadute e le significative ripercussioni hanno motivato le strutture sanitarie a enfatizzare i programmi di prevenzione delle cadute. Il CDC ha lanciato l'iniziativa STEADI (ovvero Stopping Elderly Accidents, Deaths, and Injuries) nel 2012 per aiutare gli operatori sanitari a prevenire le cadute negli anziani. Questo programma si concentra sulla fornitura di strumenti di valutazione del rischio di caduta, materiali didattici per i pazienti e strategie di intervento basate sulle prove agli operatori sanitari. Il CDC collabora con le strutture sanitarie per identificare i pazienti a rischio e promuovere misure quali programmi di esercizi e valutazioni della sicurezza domestica per ridurre gli incidenti di caduta attraverso il coinvolgimento della comunità e la formazione degli operatori.

Ad aprile 2024, Connect America, leader nelle soluzioni di assistenza virtuale, ha lanciato un programma di prevenzione delle cadute per aiutare gli anziani e tutti coloro che soffrono di patologie croniche a vivere in sicurezza nelle loro case. Questo programma completo si concentra sull'identificazione e sulla previsione dei rischi di caduta, fornendo al contempo istruzione e supporto per ridurre i casi di caduta tra le popolazioni anziane e a rischio. Pertanto, il cambiamento verso un'assistenza proattiva evidenzia l'importanza di sistemi efficienti di gestione delle cadute, creando in ultima analisi prospettive di mercato per le aziende che offrono nuovi prodotti progettati per soddisfare queste crescenti aspettative.

Analisi della segmentazione del rapporto di mercato sulla gestione delle cadute

I segmenti chiave che hanno contribuito alla derivazione dell'analisi di mercato della gestione delle cadute sono il prodotto, l'applicazione, la fascia d'età, l'utente finale e l'area geografica.

- Il mercato della gestione delle cadute, in base al prodotto, è segmentato in cuscinetti con sensori, tappetini, protezioni per i fianchi, sistemi di allarme, dispositivi di comunicazione e altri prodotti. Il segmento dei sistemi di allarme ha detenuto la quota maggiore del mercato della gestione delle cadute nel 2023 e si prevede che registrerà un CAGR significativo nel periodo 2023-2031.

- In base all'applicazione, il mercato è segmentato in sistemi di rilevamento delle cadute, apparecchiature di prevenzione delle cadute e sistemi di monitoraggio e risposta post-caduta. Il segmento dei sistemi di rilevamento delle cadute ha detenuto la quota maggiore del mercato della gestione delle cadute nel 2023.

- Il mercato della gestione delle cadute, in base alla fascia d'età, è segmentato in popolazione anziana (65 anni e oltre) e adulti (18-64 anni). Il segmento della popolazione anziana (65 anni e oltre) ha detenuto la quota maggiore del mercato della gestione delle cadute nel 2023 e si prevede che registrerà un CAGR significativo nel periodo 2023-2031.

- In base all'utente finale, il mercato è segmentato in ospedali e cliniche, case di cura, strutture di assistenza domiciliare e altri utenti finali. Il segmento ospedali e cliniche ha detenuto la quota maggiore del mercato della gestione delle cadute nel 2023.

Analisi della quota di mercato della gestione delle cadute per area geografica

L'ambito geografico del rapporto di mercato sulla gestione delle cadute è suddiviso principalmente in cinque regioni principali: Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud e Centro America. Il Nord America ha dominato il mercato nel 2023. La crescita del mercato nella regione può essere attribuita alla presenza di attori chiave del mercato, all'accettazione precoce di tecnologie avanzate e a un'infrastruttura sanitaria consolidata. Le cadute sono la causa principale di infortuni e morte tra gli anziani. Pertanto, la consapevolezza delle soluzioni e delle tecnologie per la gestione delle cadute sta crescendo negli Stati Uniti con l'aumento della popolazione geriatrica poiché il settore sanitario nel paese fa molto affidamento sui progressi tecnologici per fornire trattamenti efficaci e prolungare ulteriormente l'aspettativa di vita. I Centers for Disease Control and Prevention (CDC) segnalano che circa il 25% degli anziani subisce cadute ogni anno nel paese, evidenziando l'urgenza di strategie efficaci di prevenzione e gestione delle cadute. Di conseguenza, sia il settore sanitario pubblico che quello privato hanno intensificato gli sforzi per affrontare i rischi di caduta attraverso varie iniziative e strategie per aumentare la consapevolezza sulle cause e la prevenzione delle cadute, insieme all'importanza di sistemi di rilevamento e risposta precoci.

Gli operatori sanitari, le strutture di assistenza a lungo termine e i centri di riabilitazione adottano in modo proattivo programmi di gestione delle cadute, integrando valutazioni del rischio di caduta, esercizi di rafforzamento muscolare e allenamento dell'equilibrio nelle cure di routine per gli anziani. Ad esempio, nell'aprile 2024, Connect America, un innovatore riconosciuto a livello nazionale di soluzioni di assistenza virtuale che consentono agli anziani e a coloro che vivono con patologie croniche di vivere in sicurezza e bene a casa, ha annunciato il lancio del suo innovativo programma di prevenzione delle cadute. Il programma di prevenzione delle cadute Connect America mira ad affrontare questo problema con l'implementazione di innovative tecnologie sanitarie connesse, come l'impegno virtuale AI, l'analisi predittiva e i servizi di supporto, per aiutare a identificare e prevedere i soggetti a rischio e fornire interventi di assistenza preventiva per ridurre al minimo il potenziale di una caduta o mitigare l'intensità di una lesione da caduta.

Le aziende negli Stati Uniti si stanno impegnando per migliorare l'accessibilità e la convenienza attraverso partnership con programmi governativi come Medicare e Medicaid, che hanno iniziato a coprire soluzioni di gestione specifiche come i dispositivi di rilevamento delle cadute. Inoltre, gli operatori sanitari e le compagnie assicurative riconoscono sempre di più i vantaggi finanziari dell'investimento nella prevenzione delle cadute, in quanto possono ridurre i costi associati alle lesioni causate dalle cadute, che sono costose da curare e gestire. Con l'aumento della consapevolezza, le soluzioni di gestione delle cadute stanno diventando sempre più integrate nel più ampio sistema sanitario. Pertanto, il mercato statunitense della gestione delle cadute si sta espandendo rapidamente con sforzi sostenuti per aumentare la consapevolezza, migliorare l'accessibilità e migliorare la convenienza per garantire l'adozione su larga scala di soluzioni di prevenzione e gestione delle cadute.

Approfondimenti regionali sul mercato della gestione autunnale

Le tendenze regionali e i fattori che influenzano il Fall Management Market durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del Fall Management Market in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud e Centro America.

- Ottieni i dati specifici regionali per il mercato della gestione autunnale

Ambito del rapporto di mercato sulla gestione delle cadute

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 218,42 milioni di dollari USA |

| Dimensioni del mercato entro il 2031 | 630,50 milioni di dollari USA |

| CAGR globale (2023-2031) | 14,2% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

Per prodotti

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato della gestione autunnale: comprendere il suo impatto sulle dinamiche aziendali

Il mercato del Fall Management Market sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato della gestione delle cadute sono:

- Alimed Inc

- Curbell, Inc

- Società DeRoyal Industries Inc.

- Emfit Ltd

- Società Rondish Limited

- Società di assistenza intelligente

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato Fall Management

Notizie di mercato e sviluppi recenti sulla gestione delle cadute

Il mercato della gestione delle cadute viene valutato raccogliendo dati qualitativi e quantitativi dopo la ricerca primaria e secondaria, che include importanti pubblicazioni aziendali, dati associativi e database. Di seguito sono elencati alcuni degli sviluppi chiave nel mercato della gestione delle cadute:

- Bay Alarm Medical, azienda leader nei sistemi di allerta medica, ha rilasciato il suo nuovo sistema di allerta mobile SOS Micro. Il sistema è un aggiornamento delle popolari offerte di allerta medica dell'azienda, ma presenta hardware più nuovo e più piccolo. (Fonte: Bay Alarm Medical, sito Web aziendale, ottobre 2024)

- Tunstall Healthcare, un fornitore di soluzioni per la salute e l'assistenza connesse, ha lanciato un prodotto nuovo e innovativo, Tunstall GO, che offre voce bidirezionale, rilevamento delle cadute e localizzabilità. Sviluppato da Chiptech, integra i pacchetti di teleassistenza offrendo agli utenti i mezzi per accedere facilmente all'assistenza quando sono lontani da casa. (Fonte: Tunstall Healthcare, sito Web aziendale, marzo 2021).

Copertura e risultati del rapporto di mercato sulla gestione delle cadute

Il rapporto "Dimensioni e previsioni del mercato della gestione delle cadute (2021-2031)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato della gestione delle cadute a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Tendenze del mercato della gestione delle cadute, nonché dinamiche di mercato quali conducenti, sistemi di ritenuta e opportunità chiave

- Analisi PEST e SWOT dettagliate

- Analisi di mercato sulla gestione delle cadute che copre le principali tendenze di mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti per il mercato della gestione autunnale

- Profili aziendali dettagliati

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi storica (2 anni), anno base, previsione (7 anni) con CAGR

- Analisi PEST e SWOT

- Valore/volume delle dimensioni del mercato - Globale, Regionale, Nazionale

- Industria e panorama competitivo

- Set di dati Excel

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative

Sblocca sconti esclusivi sui report

Richiedi ora

Ottieni un campione gratuito per - Mercato della gestione autunnale

Ottieni un campione gratuito per - Mercato della gestione autunnale