Crescita, dimensioni, quota, tendenze, analisi dei principali attori e previsioni del mercato dei componenti di rigenerazione mineraria fino al 2030

Dimensioni e previsioni del mercato dei componenti di rigenerazione per l'industria mineraria (2020-2030), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per componente (motore, assale, trasmissione, cilindro idraulico e altri), attrezzatura (escavatori, pale gommate, bulldozer gommati, bulldozer cingolati, autocarri da trasporto e altri) e settore (carbone, metallo e altri) e area geografica.

- Stato : Edito

- Codice del report : TIPRE00007379

- Categoria : Produzione e costruzione

- Numero di pagine : 210

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : July 26, 2024

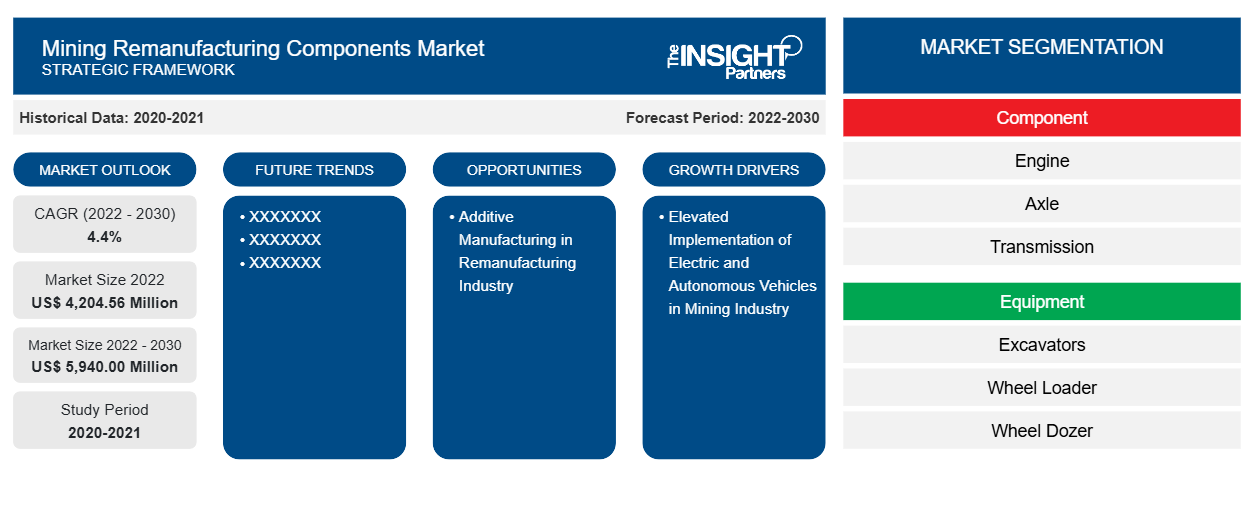

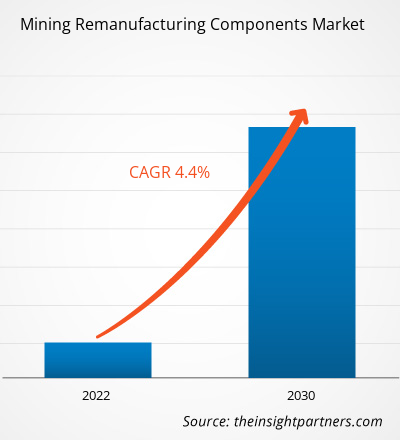

Il mercato dei componenti di rigenerazione mineraria è stato valutato a 4.204,56 milioni di dollari USA nel 2022 e si prevede che raggiungerà i 5.940,00 milioni di dollari USA entro il 2030; si prevede che registrerà un CAGR del 4,40% dal 2022 al 2030. È probabile che il crescente sviluppo nel settore minerario rimanga una tendenza chiave nel mercato.remanufacturing components market was valued at US$ 4,204.56 million in 2022 and is projected to reach US$ 5,940.00 million by 2030; it is expected to register a CAGR of 4.40% from 2022 to 2030. The growing development in the mining sector is likely to remain a key trend in the market.

Analisi di mercato dei componenti di rigenerazione minerariaRemanufacturing Components Market Analysis

Si prevede che il crescente sviluppo nel settore minerario e la crescente attenzione alla riduzione della spesa complessiva del ciclo di vita delle attrezzature minerarie alimenteranno la crescita del mercato dei componenti di rigenerazione mineraria a livello globale. Le crescenti scoperte di nuovi siti minerari stanno inoltre rafforzando la domanda di componenti di rigenerazione mineraria in tutto il mondo. I problemi di qualità relativi alle parti dei rigeneratori o ai componenti minerari potrebbero ostacolare la crescita del mercato dei componenti di rigenerazione mineraria. Tuttavia, si prevede che l'implementazione di tecnologie di produzione additiva nel settore minerario guiderà la crescita del mercato nel periodo di previsione.

Panoramica del mercato dei componenti di rigenerazione mineraria

L'attività mineraria è un settore ad alta intensità di capitale. Attrezzature, componenti e dispositivi costosi sono principalmente integrati nel processo complessivo. Le aziende minerarie sono fortemente focalizzate sull'aumento del ciclo di vita dei componenti con processi di manutenzione e rigenerazione periodici per ridurre le possibilità di arresto del sistema e guasti del processo. La crescente attenzione al progresso tecnologico e la crescente enfasi sulla praticità del progetto stanno guidando la domanda di componenti di rigenerazione per l'attività mineraria. Sia i rivenditori che gli specialisti dedicati alla rigenerazione eseguono ispezioni dei componenti principali recuperati per valutare se sono idonei per la rigenerazione. Questa fase elimina la necessità di tempi di attesa che altrimenti sarebbero necessari se le ispezioni fossero eseguite solo presso la struttura di ricezione del nucleo. La fase di progettazione e ingegneria di alto valore del processo di rigenerazione comporta l'uso di tecnologie di produzione additiva avanzate per ripristinare i componenti alle specifiche originali e alle condizioni di nuovo. La sezione dedicata alla rigenerazione sviluppa molte delle tecnologie utilizzate durante questa fase. Il riassemblaggio comprende sia parti rigenerate che nuove, nonché miglioramenti ingegneristici.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato dei componenti di rigenerazione mineraria: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità di mercato per i componenti di rigenerazione per l'industria minerariaRemanufacturing Components Market Drivers and Opportunities

La crescita dell'industria mineraria nei paesi sviluppati favorirà il mercato

L'industria mineraria negli Stati Uniti consiste nell'esplorazione, estrazione, arricchimento e lavorazione di minerali solidi naturali presenti sulla terra. Carbone, metalli (come ferro e rame) e minerali industriali sono esempi di minerali estratti. Gli Stati Uniti sono un importante produttore e utilizzatore di minerali e metalli in tutto il mondo. I materiali estratti sono fondamentali per la tecnologia di consumo e industriale e definiscono l'espansione industriale generale degli Stati Uniti. Oltre agli Stati Uniti, la Cina è un altro paese in cui l'industria mineraria è cresciuta a dismisura negli ultimi anni. Pertanto, la crescita continua dell'industria mineraria nelle nazioni sviluppate come gli Stati Uniti e la Cina. Questa crescita nell'attività mineraria ha influenzato direttamente la domanda di attrezzature nel settore, come pale gommate e bulldozer gommati, guidando in ultima analisi la domanda di componenti di rigenerazione mineraria nelle nazioni sviluppate.beneficiation, and processing of naturally existing solid minerals from the earth. Coal, metals (such as iron and copper), and industrial minerals are examples of mined minerals. The US is a major producer and user of minerals and metals worldwide. Mined materials are crucial to consumer and industrial technology and define the general industrial expansion of the US. Apart from the US, China is another country where the mining industry has grown multifold in the past few years. Thus, continuous growth in the mining industry in developed nations such as the US and China. This growth in mining has directly affected the demand for equipment in the industry, such as wheel loaders and wheel dozers, ultimately driving the demand for mining remanufacturing components in developed nations.

Elevata implementazione di veicoli elettrici e autonomi nell'industria mineraria

Il settore minerario si sta concentrando sullo sfruttamento di veicoli minerari "senza conducente" a basse emissioni, che rappresentano una mossa avanzata per la decarbonizzazione. I veicoli elettrici vengono combinati con altre flotte per sfruttare sia le operazioni sotterranee che quelle a cielo aperto, acquistando o rinnovando le flotte di veicoli con motore diesel esistenti. La società Caterpillar ha esposto il suo primo prototipo di veicolo alimentato a batteria presso la sede aziendale di Tuscon, in Arizona, nel 2022. Inoltre, Caterpillar ha lanciato il suo camion minerario EV con una capacità di 240 tonnellate nel 2023. Si prevede che le aziende manifatturiere minerarie aumenteranno l'adozione di camion elettrici per comodità operativa. Si prevede che la domanda aumentata di veicoli elettrici nel settore minerario creerà grandi opportunità per il mercato dei componenti di rigenerazione mineraria durante il periodo di previsione.driverless" mine vehicles which is a advancned move for decarbonization. Electric vehicles are combined with other fleets for leveraging both in the underground and open pit operations by procuring or revamping existing diesel engine vehicle fleets. Caterpillar company had displayed its first battery-powered vehicle prototype at the company's Tuscon, Arizona, in 2022. Furthermore, Caterpillar launched its EV mining truck with a 240-ton capacity in 2023. The mining manufacturing companies are projected to increase the adoption of electric trucks for operational convenience. The augmented demand for electric vehicles in the mining sector is expected to create high opportunities for the mining remanufacturing component market during the forecast period.

Analisi della segmentazione del rapporto di mercato dei componenti di rigenerazione mineraria

I segmenti chiave che hanno contribuito alla derivazione dell'analisi di mercato dei componenti di rigenerazione mineraria sono componenti, attrezzature e industria.

- In base al componente, il mercato dei componenti di rigenerazione mineraria è suddiviso in motore, assale, trasmissione, cilindro idraulico e altri. Il segmento motore ha detenuto la quota maggiore del mercato nel 2022.

- In base all'attrezzatura, il mercato è segmentato in escavatori, pale gommate, dozer gommati, dozer cingolati, autocarri da trasporto e altri. Il segmento dei dozer cingolati ha detenuto la quota maggiore del mercato nel 2022.

- In termini di settore, il mercato è diviso in carbone, metallo e altri. Il segmento del metallo ha detenuto una quota significativa del mercato nel 2022.

Analisi della quota di mercato dei componenti di rigenerazione mineraria per area geografica

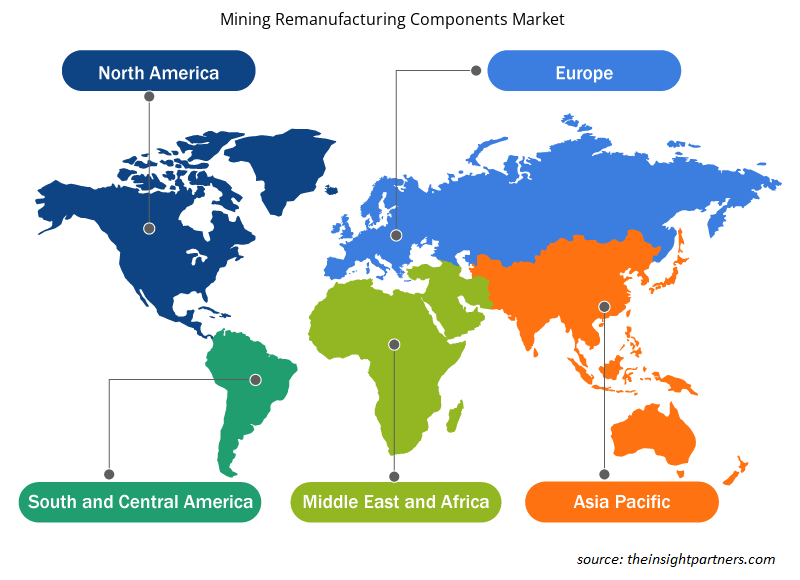

L'ambito geografico del rapporto sul mercato dei componenti di rigenerazione per l'industria mineraria è suddiviso principalmente in cinque regioni: Nord America, Asia Pacifico, Europa, Medio Oriente e Africa, e Sud e Centro America.

L'Asia Pacifica è leader del mercato. La Cina è uno dei paesi più importanti nel mercato dei componenti di rigenerazione mineraria nell'Asia Pacifica. I significativi finanziamenti del governo cinese per lo sviluppo del settore minerario e l'attenzione all'innovazione di prodotto creano opportunità per il mercato dei componenti di rigenerazione mineraria. L'industrializzazione e un numero crescente di progetti minerari stanno agendo come un importante motore per il mercato.

Approfondimenti regionali sul mercato dei componenti di rigenerazione mineraria

Le tendenze regionali e i fattori che influenzano il Mining Remanufacturing Components Market durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti di Mining Remanufacturing Components Market e la geografia in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud e Centro America.

- Ottieni i dati specifici regionali per il mercato dei componenti di rigenerazione mineraria

Ambito del rapporto di mercato sui componenti di rigenerazione mineraria

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2022 | 4.204,56 milioni di dollari USA |

| Dimensioni del mercato entro il 2030 | 5.940,00 milioni di dollari USA |

| CAGR globale (2022-2030) | 4,4% |

| Dati storici | 2020-2021 |

| Periodo di previsione | 2022-2030 |

| Segmenti coperti |

Per componente

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato: comprendere il suo impatto sulle dinamiche aziendali

Il mercato dei componenti di rigenerazione mineraria sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato dei componenti di rigenerazione per l'industria mineraria sono:

- AB Volvo

- Atlante Copco

- Caterpillar Inc.

- Epiroc AB

- Macchine edili Hitachi

- Azienda JC Komatsu Ltd.

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato dei componenti di rigenerazione mineraria

Notizie e sviluppi recenti sul mercato dei componenti di rigenerazione mineraria

Il mercato dei componenti di rigenerazione mineraria viene valutato raccogliendo dati qualitativi e quantitativi dopo la ricerca primaria e secondaria, che include importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito sono elencati alcuni degli sviluppi nel mercato dei componenti di rigenerazione mineraria:

- SRC Holdings ha completato il suo nuovo magazzino, occupato da SRC Logistics (SRCL), su North Mulroy Road a Springfield. La struttura di 413.000 piedi quadrati, completata dopo 13 mesi di costruzione, fa parte del piano di SRCL di crescere con gli attuali partner OEM e soddisfare nuove opportunità commerciali. La terza fase di espansione su North Mulroy Road segue la prima nel 2021. (Fonte: SRC Holdings, comunicato stampa, maggio 2023)

- Komatsu Ltd. e Toyota stanno collaborando a un progetto congiunto per sviluppare un veicolo leggero autonomo (ALV) utilizzando l'Autonomous Haulage System (AHS) di Komatsu. L'obiettivo è migliorare la sicurezza e la produttività nelle miniere tramite l'utilizzo di autocarri da trasporto autonomi e ALV automatizzati. (Fonte: Komatsu Ltd, comunicato stampa, maggio 2023)

Copertura e risultati del rapporto di mercato sui componenti di rigenerazione mineraria

Il rapporto "Dimensioni e previsioni del mercato dei componenti di rigenerazione mineraria (2020-2030)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato dei componenti di rigenerazione mineraria a livello globale, regionale e nazionale per tutti i principali segmenti di mercato coperti dall'ambito

- Tendenze del mercato dei componenti di rigenerazione mineraria e dinamiche di mercato come fattori trainanti, vincoli e opportunità chiave

- Analisi PEST e SWOT dettagliate

- Analisi di mercato dei componenti di rigenerazione mineraria che copre le principali tendenze di mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti per il mercato dei componenti di rigenerazione mineraria

- Profili aziendali dettagliati

Nivedita è una ricercatrice affermata con oltre 9 anni di esperienza in ricerche di mercato e consulenza aziendale. Attualmente Project Manager nel settore ICT presso The Insight Partners, vanta una profonda esperienza nella gestione e nell'esecuzione di incarichi di ricerca sindacati, personalizzati, in abbonamento e di consulenza in diversi settori tecnologici.

Con una comprovata esperienza nell'analisi basata sui dati e nella fornitura di insight fruibili, Nivedita ha contribuito in modo determinante a diversi progetti critici. Il suo lavoro include l'esecuzione end-to-end dei progetti, dalla comprensione degli obiettivi del cliente all'analisi delle tendenze di mercato, fino alla formulazione di raccomandazioni strategiche. Ha collaborato ampiamente con aziende leader nel settore ICT, aiutandole a identificare opportunità di mercato e a gestire i cambiamenti del settore.

Nivedita ha conseguito un MBA in Management presso IMS, Dehradun. Prima di entrare in The Insight Partners, ha maturato una preziosa esperienza presso MarketsandMarkets e Future Market Insights a Pune, dove ha ricoperto diversi ruoli di ricerca e ha costruito solide basi nell'analisi di settore e nel coinvolgimento dei clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative