Rapporto di mercato delle celle di saldatura robotizzate 2031 per segmenti, geografia, dinamiche, sviluppi recenti e approfondimenti strategici

Dimensioni e previsioni del mercato delle celle di saldatura robotizzata (2021-2031), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per offerta (soluzioni e servizi), tipo di cella (celle pre-ingegnerizzate e celle personalizzate), settore di utilizzo finale (automotive, manifatturiero, aerospaziale e difesa) e geografia.

- Stato : Edito

- Codice del report : TIPRE00012000

- Categoria : Produzione e costruzione

- Numero di pagine : 215

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : December 05, 2024

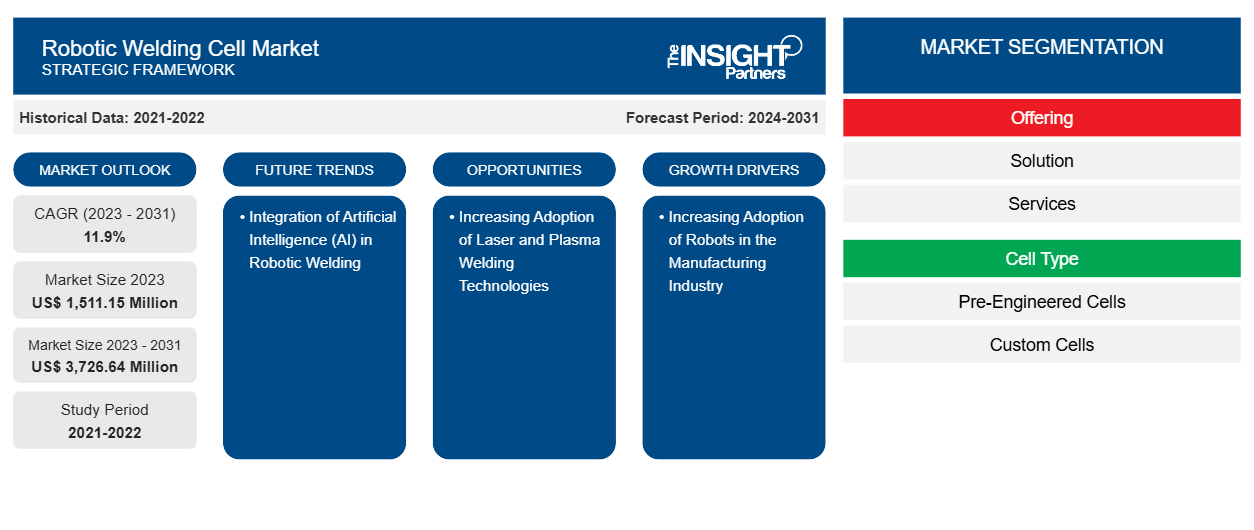

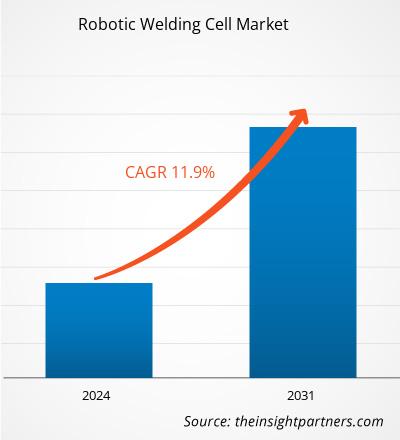

Si prevede che la dimensione del mercato delle celle di saldatura robotizzate raggiungerà i 3.726,64 milioni di dollari entro il 2031, rispetto ai 1.511,15 milioni di dollari del 2023. Si prevede che il mercato registrerà un CAGR dell'11,9% nel periodo 2023-2031. È probabile che la crescente adozione delle tecnologie dell'Industria 4.0 porti nuove tendenze chiave nel mercato nei prossimi anni.

Analisi del mercato delle celle di saldatura robotizzate

Una cella di saldatura robotizzata è composta da diversi componenti che lavorano insieme per saldare le parti. Le celle di saldatura robotizzate forniscono operazioni di saldatura di livello mondiale e sono progettate secondo gli standard globali per risparmiare tempo e costi per gli operatori. Le celle pre-ingegnerizzate sono celle di saldatura robotizzate economiche e includono solo i componenti essenziali di base richiesti per i processi di saldatura. Questa struttura di base delle celle può essere installata rapidamente; consente ai produttori di ridurre i tempi di produzione delle celle e di consegnare il prodotto finale il prima possibile. Le celle personalizzate sono costose rispetto alle celle pre-ingegnerizzate poiché includono attrezzature uniche insieme a componenti essenziali di base. Queste sono principalmente prodotte in base agli interessi specifici del cliente. Pertanto, il tempo necessario per produrre e consegnare una cella di saldatura robotizzata personalizzata è superiore a quello di una cella pre-ingegnerizzata. I robot di saldatura sono ampiamente utilizzati nell'industria automobilistica. La domanda di veicoli sta aumentando notevolmente. La crescente spesa dei consumatori è uno dei fattori che sta guidando la domanda di veicoli in tutto il mondo, in particolare nei paesi asiatici. Secondo i dati pubblicati dall'Organizzazione Internazionale dei Costruttori di Veicoli a Motore nel 2024, la produzione complessiva di veicoli ha raggiunto i 93 milioni nel 2023, con un aumento del 12% dal 2021 al 2023. L'aumento della costruzione di nuove strutture ha portato a una maggiore domanda di robot di saldatura in queste nuove strutture automobilistiche, guidando in ultima analisi il mercato delle celle di saldatura robotizzate.

Panoramica del mercato delle celle di saldatura robotizzate

I principali stakeholder nell'ecosistema del mercato globale delle celle di saldatura robotizzata includono fornitori di materie prime/componenti, produttori di celle di saldatura robotizzata, organizzazioni governative, enti normativi e clienti finali. I fornitori di componenti e hardware forniscono vari componenti e parti ai produttori di celle di saldatura robotizzata. I principali produttori di celle di saldatura robotizzata inclusi in questo rapporto sono Abb Ltd, Acieta LLC, Carl Cloos Schweisstechnik Gmbh, Kawasaki Heavy Industries, Ltd; Kuka AG; Phoenix Industrial Solutions; The Lincoln Electric Company; Wec Group Ltd.; e Yaskawa America, Inc.; tra gli altri. Dopo i produttori di celle di saldatura robotizzata, ci sono diversi stakeholder periferici nel mercato globale delle celle di saldatura robotizzata, che svolgono un ruolo cruciale nel consentire i progressi tecnologici e l'adozione di celle di saldatura robotizzata.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato delle celle di saldatura robotizzate: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità del mercato delle celle di saldatura robotizzate

Crescente adozione di robot nell'industria manifatturiera

I robot svolgono un ruolo importante nel settore manifatturiero. I robot aiutano ad aumentare l'efficienza e la produttività complessive nelle operazioni di produzione. Vengono utilizzati nel settore manifatturiero per varie applicazioni come assemblaggio e distribuzione, movimentazione e prelievo, lavorazione e taglio, saldatura e brasatura, fusione e stampaggio, finitura e levigatura, verniciatura e rivestimento, pulizia e igiene, logistica e stoccaggio e imballaggio e pallettizzazione. Secondo i dati pubblicati dalla Federazione Internazionale dei Robot nel 2024, circa 4,2 milioni di robot operavano nelle fabbriche in tutto il mondo nel 2023, un aumento rispetto ai 3,9 milioni del 2022. Come affermato dalla Federazione Internazionale dei Robot nel 2021, metà del totale dei robot che lavorano nelle fabbriche sarà utilizzato per applicazioni di saldatura. Pertanto, la crescente adozione di robot nel settore manifatturiero sta spingendo la crescita del mercato delle celle di saldatura robotizzate.

Crescente adozione di tecnologie di saldatura laser e al plasma

La domanda di saldatura laser sta aumentando rapidamente. La tecnologia di saldatura laser utilizza raggi laser ad alta energia sviluppati utilizzando anidride carbonica, azoto ed elio. Ciò aiuta a unire i materiali con elevata precisione e velocità. La popolarità della saldatura laser sta aumentando grazie alle distorsioni minime e alla capacità di saldare materiali diversi. Inoltre, migliorando l'efficienza laser e ottimizzando il processo di saldatura, è possibile ottenere un risparmio energetico complessivo con questo tipo di tecnologia di saldatura. Questo è uno dei fattori importanti che sta aumentando la domanda di saldatura laser, poiché la riduzione del consumo energetico è una delle principali preoccupazioni in tutto il mondo.

Inoltre, se integrata con tecnologie avanzate come AI e ML, questa tecnologia di saldatura può funzionare in modo efficiente. Pertanto, la domanda di tecnologia di saldatura laser sta aumentando notevolmente. Allo stesso modo, la tecnologia di saldatura al plasma offre vari vantaggi, tra cui elevata densità di potenza, saldature pulite e lisce, elevata velocità di saldatura, bassa distorsione e miglioramento del bridging degli spazi. Le saldature prodotte tramite saldatura al plasma sono molto resistenti e meno visibili.

Analisi della segmentazione del rapporto di mercato delle celle di saldatura robotizzate

I segmenti chiave che hanno contribuito alla derivazione dell'analisi di mercato delle celle di saldatura robotizzata sono l'offerta, il tipo di cella e il settore di utilizzo finale.

- In base all'offerta, il mercato globale delle celle di saldatura robotizzata è suddiviso in soluzioni e servizi. Il segmento delle soluzioni ha rappresentato una quota di mercato maggiore nel 2023 e si prevede che registrerà un CAGR più elevato durante il periodo di previsione. Le soluzioni delle celle di saldatura robotizzata aiutano i produttori a raggiungere la loro capacità produttiva aggiuntiva e ad attenuare i problemi di carenza di manodopera. Tali vantaggi delle celle di saldatura robotizzata rispetto ai processi di saldatura manuale stanno guidando la domanda di celle di saldatura robotizzata.

- In base al tipo di cella, il mercato globale delle celle di saldatura robotizzata è suddiviso in celle pre-ingegnerizzate e celle personalizzate. Il segmento delle celle pre-ingegnerizzate ha dominato il segmento del tipo di cella con una quota di mercato del 68,3% nel 2023 e si stima che il segmento delle celle personalizzate registrerà un CAGR più elevato durante il periodo di previsione. Le celle di saldatura robotizzata pre-ingegnerizzate sono celle di saldatura robotizzata standard che hanno uno spazio di lavoro più ampio con un manipolatore robot più lungo e due piani di lavoro più grandi. D'altro canto, le celle personalizzate sono prodotte in base ai requisiti dell'utente finale e sono personalizzate per settori specifici.

- In base al settore di utilizzo finale, il mercato globale delle celle di saldatura robotizzata è segmentato in automotive, manifatturiero e aerospaziale e difesa. Il segmento automotive ha rappresentato la seconda quota di mercato più grande e si prevede che registrerà il tasso di crescita più elevato durante il periodo di previsione. Uno dei fattori che guidano la domanda da parte dell'industria automobilistica è la crescente produzione e vendita di veicoli in tutto il mondo. Si prevede che l'industria manifatturiera registrerà un notevole CAGR durante il periodo di previsione. Uno dei fattori che guidano la domanda di celle di saldatura robotizzate nel segmento manifatturiero è la crescente tendenza all'industrializzazione in tutto il mondo, in particolare nei paesi in via di sviluppo.

Analisi della quota di mercato delle celle di saldatura robotizzate

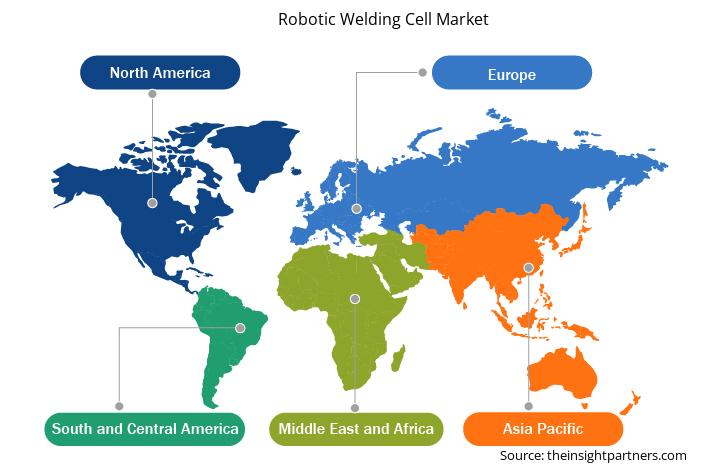

L'ambito geografico del rapporto sul mercato delle celle di saldatura robotizzate offre un'analisi dettagliata a livello regionale e nazionale. Nord America, Europa e Asia Pacifico sono le principali regioni che stanno assistendo a una crescita significativa nel mercato delle celle di saldatura robotizzate. La Cina ha rappresentato quasi il 60% della quota di mercato nel numero totale di installazioni di robot nel 2022. La Cina ha installato circa 0,2 milioni di robot nel 2022, mentre il Giappone ha installato più di 50.000 unità nel 2022, il secondo mercato più grande a livello mondiale. Oltre a Cina e Giappone, Singapore, India e Thailandia sono alcuni dei principali mercati dell'Asia Pacifico.

L'Europa ha rappresentato la seconda quota di mercato più grande nelle installazioni di robot industriali e nel settore delle celle di saldatura robotizzate. La Germania è stata il mercato più grande in Europa per le celle di saldatura robotizzate e i robot industriali nel 2023. Uno dei fattori che guidano la domanda di celle di saldatura robotizzate è l'attenzione all'aumento dell'adozione delle tecnologie dell'Industria 4.0 in Germania. Germania, Francia, Regno Unito e Italia sono alcune delle quote notevoli nel mercato delle celle di saldatura robotizzate.

Il Nord America è uno dei mercati più importanti per le celle di saldatura robotizzate, grazie alla presenza di alcune importanti aziende manifatturiere in tutti i settori, alla crescente necessità di Industria 4.0 e all'aumento della domanda di tecnologia avanzata. Gli Stati Uniti hanno rappresentato la quota maggiore del mercato grazie alle tendenze di industrializzazione e digitalizzazione nel paese. Inoltre, gli Stati Uniti ospitano alcune importanti aziende manifatturiere automobilistiche e aerospaziali, come Tesla, Boeing e Ford Motors.

Approfondimenti regionali sul mercato delle celle di saldatura robotizzate

Le tendenze regionali e i fattori che influenzano il mercato delle celle di saldatura robotizzata durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato delle celle di saldatura robotizzata in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato delle celle di saldatura robotizzate

Ambito del rapporto di mercato sulle celle di saldatura robotizzate

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 1.511,15 milioni di dollari USA |

| Dimensioni del mercato entro il 2031 | 3.726,64 milioni di dollari USA |

| CAGR globale (2023-2031) | 11,9% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

Offrendo

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità dei player del mercato delle celle di saldatura robotizzate: comprendere il suo impatto sulle dinamiche aziendali

Il mercato delle celle di saldatura robotizzate sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato delle celle di saldatura robotizzate sono:

- ABB Ltd.

- Acieta

- Carl Cloos Schweisstechnik GmbH

- Lincoln Electric Holdings Inc.

- Azienda Kuka

- Azienda

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato delle celle di saldatura robotizzate

Notizie e sviluppi recenti sul mercato delle celle di saldatura robotizzate

Il mercato delle celle di saldatura robotizzate viene valutato raccogliendo dati qualitativi e quantitativi dopo la ricerca primaria e secondaria, che include importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito sono elencati alcuni degli sviluppi nel mercato delle celle di saldatura robotizzate:

- La nuova cella OmniVance FlexArc Compact di ABB consente di risparmiare spazio e aggiunge flessibilità alle applicazioni di saldatura. ABB Ltd. ha lanciato OmniVance FlexArc Compact, una nuova cella per applicazioni di saldatura più piccola con maggiore flessibilità, facilità d'uso e migliore integrazione per aiutare le aziende a far fronte alla carenza di manodopera nella saldatura. OmniVance FlexArc Compact è la cella di saldatura ad arco più piccola della sua categoria. Il suo innovativo design di montaggio del robot a portale a 45 gradi massimizza i parametri di lavoro del robot posizionandolo al centro di una tavola girevole a tre assi, avvicinandolo al pezzo in lavorazione. (ABB Ltd., sito Web aziendale, giugno 2022)

Copertura e risultati del rapporto sul mercato delle celle di saldatura robotizzate

Il rapporto "Dimensioni e previsioni del mercato delle celle di saldatura robotizzate (2021-2031)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato delle celle di saldatura robotizzate a livello nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Tendenze del mercato delle celle di saldatura robotizzate, nonché dinamiche di mercato quali driver, vincoli e opportunità chiave

- Analisi PEST e SWOT dettagliate

- Analisi di mercato delle celle di saldatura robotizzate che copre le principali tendenze di mercato, il quadro nazionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa termica, i principali attori e gli sviluppi recenti per il mercato delle celle di saldatura robotizzate

- Profili aziendali dettagliati

Nivedita è una ricercatrice affermata con oltre 9 anni di esperienza in ricerche di mercato e consulenza aziendale. Attualmente Project Manager nel settore ICT presso The Insight Partners, vanta una profonda esperienza nella gestione e nell'esecuzione di incarichi di ricerca sindacati, personalizzati, in abbonamento e di consulenza in diversi settori tecnologici.

Con una comprovata esperienza nell'analisi basata sui dati e nella fornitura di insight fruibili, Nivedita ha contribuito in modo determinante a diversi progetti critici. Il suo lavoro include l'esecuzione end-to-end dei progetti, dalla comprensione degli obiettivi del cliente all'analisi delle tendenze di mercato, fino alla formulazione di raccomandazioni strategiche. Ha collaborato ampiamente con aziende leader nel settore ICT, aiutandole a identificare opportunità di mercato e a gestire i cambiamenti del settore.

Nivedita ha conseguito un MBA in Management presso IMS, Dehradun. Prima di entrare in The Insight Partners, ha maturato una preziosa esperienza presso MarketsandMarkets e Future Market Insights a Pune, dove ha ricoperto diversi ruoli di ricerca e ha costruito solide basi nell'analisi di settore e nel coinvolgimento dei clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative