Analisi e previsioni di mercato dei dispositivi di sutura chirurgica per dimensione, quota, crescita, tendenze 2028

Previsioni di mercato dei dispositivi di sutura chirurgica fino al 2028 - Impatto del COVID-19 e analisi globale per prodotto (suturatrici chirurgiche elettriche e suturatrici chirurgiche manuali), tipo (suturatrici chirurgiche monouso e suturatrici chirurgiche riutilizzabili), applicazione (chirurgia ortopedica, chirurgia endoscopica, chirurgia cardiaca e toracica, chirurgia addominale e pelvica e altre) e utente finale (ospedali e centri chirurgici ambulatoriali)

- Stato : Edito

- Codice del report : TIPRE00005203

- Categoria : Scienze della vita

- Numero di pagine : 190

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 14, 2024

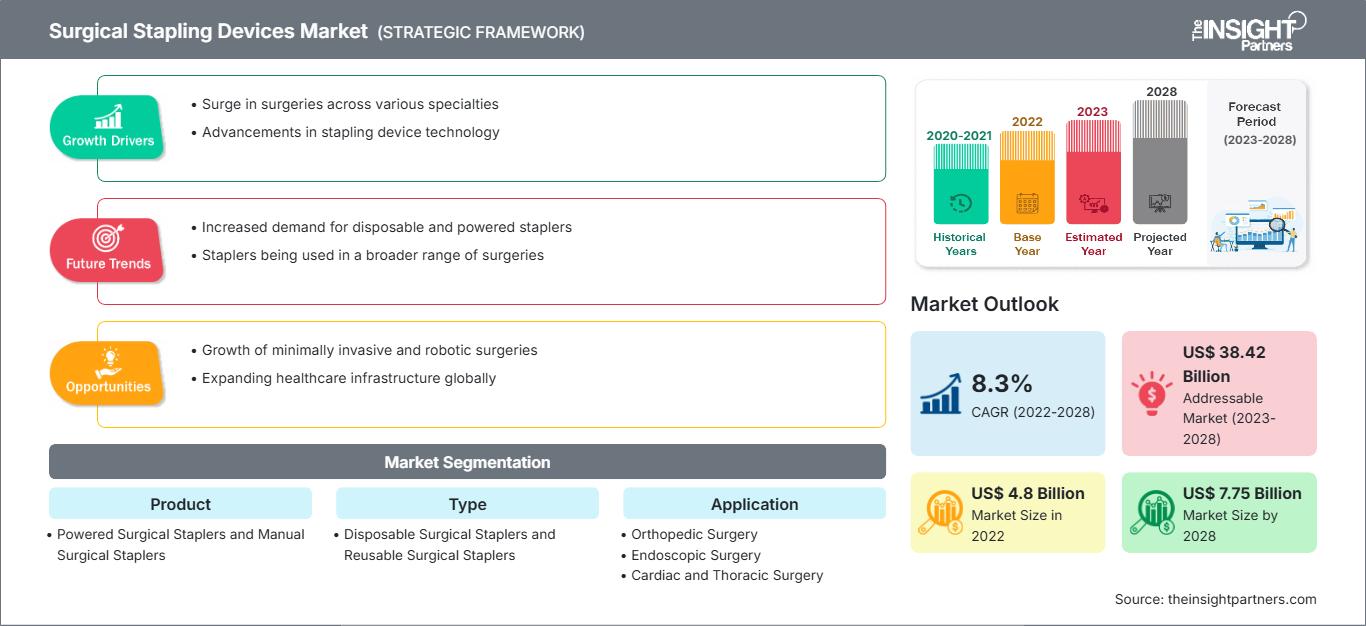

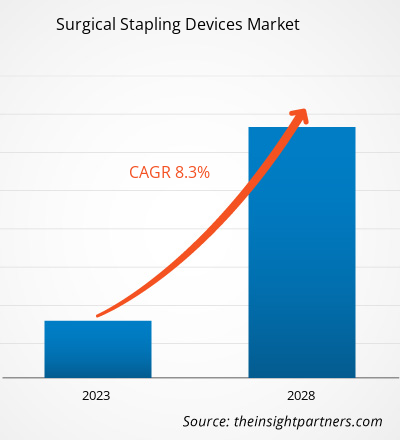

Si prevede che il mercato delle suturatrici chirurgiche raggiungerà i 7.747,1 milioni di dollari entro il 2028, rispetto ai 4.795,8 milioni di dollari del 2022; si stima una crescita a un CAGR dell'8,3% dal 2022 al 2028.

Una suturatrice chirurgica o graffette è un dispositivo utilizzato al posto di una sutura per chiudere rapidamente ferite o incisioni di grandi dimensioni. Sono meno dolorose dei punti di sutura e possono essere utilizzate nella chirurgia mininvasiva. I dispositivi possono essere utilizzati anche in interventi chirurgici per rimuovere organi o ricollegare organi interni, nonché per chiudere ferite in cui la pelle è tesa contro l'osso.

Il mercato delle suturatrici chirurgiche è segmentato in base a prodotto, tipo, applicazione, utente finale e area geografica. Per area geografica, il mercato delle suturatrici chirurgiche è ampiamente segmentato in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa e Sud e Sud America. America Centrale. Il rapporto offre approfondimenti e analisi approfondite del mercato, ponendo l'accento su parametri quali tendenze di mercato, progressi tecnologici e dinamiche di mercato, insieme all'analisi del panorama competitivo dei principali attori del mercato mondiale.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato dei dispositivi di sutura chirurgica: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

Approfondimenti di mercato - Mercato delle suturatrici chirurgiche

Progressi tecnologici

L'enorme crescita della popolazione di pazienti in tutto il mondo ha creato una domanda di dispositivi medici avanzati ed efficaci per trattamenti e risultati migliori, costringendo i produttori di dispositivi medici a innovare e sviluppare nuove tecnologie per l'aggiornamento dei dispositivi esistenti. Questi prodotti innovativi e tecnologicamente avanzati mirano anche a semplificare il lavoro degli operatori sanitari. Le aziende utilizzano tecnologie robotiche e automatizzate che accelerano l'efficienza operativa e riducono i tempi chirurgici, riducendo al contempo le impostazioni manuali, con conseguente ulteriore riduzione delle complicazioni e dei danni ai tessuti. Ad esempio, nel 2021, Intuitive lancia la prima suturatrice chirurgica con tecnologia robotizzata che facilita le regolazioni automatiche durante l'applicazione dei punti e offre anche un'articolazione di 120° in tutte le direzioni. Ciò ha anche ampliato le aree di applicazione di questi dispositivi di sutura chirurgica in varie procedure, in particolare in procedure mini-invasive come laparoscopia e artroscopia. Inoltre, nel 2017, Medtronic ha lanciato una suturatrice chirurgica intelligente denominata Signia Stapling System, che rileva lo spessore dei tessuti e regola automaticamente la velocità di sutura. Questo aiuterà gli operatori sanitari a posizionare punti di sutura uniformi e uniformi dopo l'intervento chirurgico o durante la sutura delle ferite. Si prevede che tale progresso tecnologico nei dispositivi di sutura chirurgica ridurrà ulteriormente gli errori manuali e le perdite, migliorando la guarigione e rendendoli più facili da raggiungere anche in punti difficili. Pertanto, è probabile che i fattori sopra discussi anticipino la crescita del mercato dei dispositivi di sutura chirurgica.

Approfondimenti per gli utenti finali

In base al prodotto, il mercato globale dei dispositivi di sutura chirurgica è suddiviso in suturatrici chirurgiche elettriche e suturatrici chirurgiche manuali. Il segmento delle suturatrici chirurgiche elettriche ha detenuto una quota maggiore del mercato dei dispositivi di sutura chirurgica nel 2022 e si prevede che registrerà un CAGR più elevato durante il periodo di previsione. Le suturatrici chirurgiche motorizzate sono preferite alle suturatrici manuali grazie alla facilità d'uso, al basso rischio di problemi come perdite di sangue o fuoriuscite, ai tempi operatori più brevi e ai minori costi ospedalieri. Il segmento delle suturatrici chirurgiche motorizzate è guidato da diversi vantaggi, come la chiusura precisa della ferita, la stabilità, la riduzione delle perdite e la minore forza di compressione. Attualmente, due tipi di sistemi di sutura motorizzati sono prevalentemente utilizzati nella pratica clinica: il GST di Ethicon e il Signia Stapling System (SIG) di Medtronic. Il GST, lanciato nel 2015, presenta superfici ricaricate con estensioni tascabili proprietarie per stabilizzare e mantenere in posizione il tessuto e posizionare i punti con un'altezza uniforme. Il SIG, lanciato nel 2017, combina un'impugnatura per suturatrice motorizzata Medtronic e altri componenti (come l'adattatore lineare, il guscio di alimentazione, la guida di inserimento della suturatrice e lo strumento di retrazione manuale), rappresentando una riprogettazione rispetto alla suturatrice motorizzata Endo-GIATM iDrive originale, pur mantenendo le stesse ricariche originali con tecnologia Tri-Staple. Nel 2021, Ethicon ha lanciato la suturatrice ECHELON+ con ricariche GST, una nuova suturatrice chirurgica motorizzata progettata per aumentare la sicurezza della linea di sutura e ridurre le complicanze grazie a una compressione tissutale più uniforme e a una migliore formazione dei punti, anche in situazioni difficili.

Lanci di prodotti, fusioni e acquisizioni sono le strategie più adottate dai player che operano nel mercato globale delle suturatrici chirurgiche. Di seguito sono elencati alcuni dei recenti sviluppi chiave dei prodotti:

- A giugno 2022, Ethicon ha lanciato la suturatrice Echelon 3000 di nuova generazione, progettata per un accesso e un controllo eccezionali. Si tratta di un dispositivo digitale che offre ai chirurghi un'articolazione motorizzata semplice e con una sola mano, per aiutarli a soddisfare le esigenze specifiche dei loro pazienti. Progettato con un'apertura della mascella maggiore del 39% e un'ampiezza di articolazione maggiore del 27%,3,4 ECHELON 3000 offre ai chirurghi un migliore accesso e controllo su ogni transezione, anche in spazi ristretti e su tessuti difficili.

- A dicembre 2021, Intutive Surgical Inc ha ricevuto l'autorizzazione della FDA per la suturatrice a punta curva SureForm 30 da 8 mm e le relative ricariche per l'uso in chirurgia generale, toracica, ginecologica, urologica e pediatrica.

- A marzo 2021, Ethicon ha lanciato la suturatrice ECHELON+ con ricariche GST, una nuova suturatrice chirurgica motorizzata progettata per aumentare la sicurezza della linea di sutura e ridurre le complicazioni attraverso una compressione dei tessuti più uniforme e una migliore formazione delle suture, anche in situazioni difficili.

La pandemia di COVID-19 ha portato alla chiusura mondiale delle catene di domanda e offerta, con conseguente calo delle vendite nel settore sanitario durante la fase iniziale del lockdown. Secondo l'articolo intitolato "Cancellazioni di interventi chirurgici elettivi a causa della pandemia di COVID-19: modelli predittivi globali per informare i piani di recupero chirurgico", pubblicato sul British Journal of Surgery a maggio 2020, sulla base di 12 settimane di massima interruzione dei servizi ospedalieri a causa del COVID-19, circa 28,4 milioni di interventi chirurgici elettivi in tutto il mondo sono stati cancellati o rinviati nel 2020. Tuttavia, in futuro, si prevede che il mercato registrerà una ripresa dopo l'allentamento delle restrizioni imposte dal lockdown. La Società Italiana di Urologia (SIU), l'Associazione Urologica Spagnola (AEU), la Società Tedesca di Urologia (DGU), l'Associazione Francese di Urologia (AFU) e la British Association of Urological Surgeons (BAUS) hanno collaborato per sviluppare linee guida per l'esecuzione di procedure diagnostiche e chirurgiche selettive.

Approfondimenti regionali sul mercato dei dispositivi di sutura chirurgica

Le tendenze regionali e i fattori che influenzano il mercato delle suturatrici chirurgiche durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione analizza anche i segmenti e la distribuzione geografica del mercato delle suturatrici chirurgiche in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America Meridionale e Centrale.

Ambito del rapporto di mercato sui dispositivi di sutura chirurgica

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2022 | US$ 4.8 Billion |

| Dimensioni del mercato per 2028 | US$ 7.75 Billion |

| CAGR globale (2022 - 2028) | 8.3% |

| Dati storici | 2020-2021 |

| Periodo di previsione | 2023-2028 |

| Segmenti coperti |

By Prodotto

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato dei dispositivi di sutura chirurgica: comprendere il suo impatto sulle dinamiche aziendali

Il mercato delle suturatrici chirurgiche è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Mercato dei dispositivi di sutura chirurgica Panoramica dei principali attori chiave

Dispositivi di sutura chirurgica - Segmentazione del mercato

In base al prodotto, il mercato dei dispositivi di sutura chirurgica è suddiviso in suturatrici chirurgiche elettriche e suturatrici chirurgiche manuali. Per tipologia, il mercato dei dispositivi di sutura chirurgica è segmentato in suturatrici chirurgiche monouso e suturatrici chirurgiche riutilizzabili. Per applicazione, il mercato dei dispositivi di sutura chirurgica è segmentato in chirurgia ortopedica, chirurgia endoscopica, chirurgia cardiaca e toracica, chirurgia addominale e pelvica e altri. Il mercato per utente finale è segmentato in ospedali e centri chirurgici ambulatoriali. In base all'area geografica, il mercato è suddiviso in Nord America (Stati Uniti, Canada, Messico), Europa (Francia, Germania, Regno Unito, Italia, Spagna e resto d'Europa), Asia Pacifico (Cina, Giappone, India, Australia, Corea del Sud e resto dell'Asia Pacifico), Medio Oriente e Africa. Africa (Arabia Saudita, Sudafrica, Emirati Arabi Uniti e resto del Medio Oriente e dell'Africa), America meridionale e centrale (Brasile, Argentina e resto dell'America meridionale e centrale)

Profili aziendali - Mercato dei dispositivi di sutura chirurgica

- Intuitive Surgical Inc.

- Medtronic Plc

- Ethicon USA LLC

- Frankenman International Ltd

- PantherHealthcare Medical Equipment Co Ltd

- B. Braun SE

- Grena Ltd

- Conmed Corp

- 3M Co

- Purple Surgical UK Ltd

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative