臨床試験市場の分析と予測 - 規模、シェア、成長、トレンド 2031 年

臨床試験市場の規模と予測(2021年 - 2031年)、世界および地域別のシェア、トレンド、成長機会分析レポートの対象範囲:研究デザイン別(介入試験および拡大アクセス試験)、適応症別(自己免疫疾患/炎症、疼痛管理、腫瘍学的状態、神経疾患、糖尿病、肥満、代謝性疾患、心血管疾患、その他)、フェーズタイプ別(フェーズI、フェーズII、フェーズIII)、および地域別(北米、ヨーロッパ、アジア太平洋、南米および中米、中東およびアフリカ)

- ステータス : 出版

- レポートコード : TIPRE00006203

- カテゴリー : ライフサイエンス

- ページ数 : 211

- 利用可能なレポート形式 :

- 最終更新日 : October 10, 2024

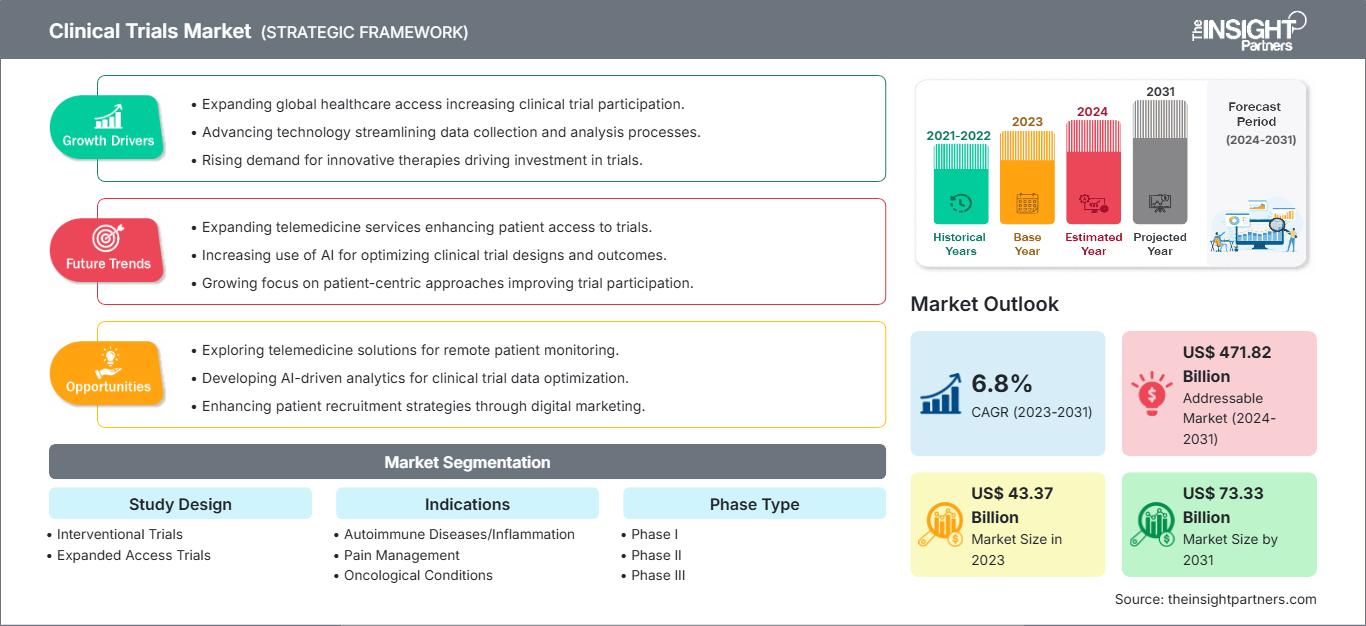

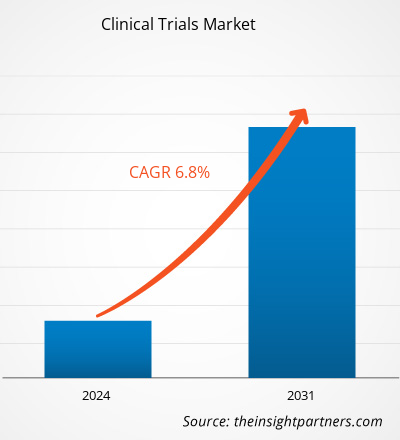

臨床試験市場規模は、2023年の433.7億米ドルから2031年には733.3億米ドルに達すると予測されています。市場は2023年から2031年にかけて6.8%のCAGRで成長すると予想されています。AIを活用した臨床試験は、今後数年間、市場のトレンドとなる可能性が高いでしょう。

臨床試験市場分析

臨床試験市場は、主に製薬会社、バイオテクノロジー企業、医療機器企業による製品イノベーションへの継続的な取り組みによって牽引されています。市場の発展に貢献するその他の要因としては、臨床試験のグローバル化、関連技術の急速な進歩、臨床試験実施のためのCROに対する需要の増加などが挙げられます。さらに、「Global Clinical Trials Connect 2022」などのカンファレンスは、この市場の企業に臨床試験や臨床研究の進歩を把握するためのプラットフォームを提供しています。

臨床試験市場の概要

製品発売、合併・買収、提携、地理的拡大といった企業による戦略的取り組みの増加は、臨床試験市場に利益をもたらします。2023年9月、ICON plcは次世代の臨床試験トークン化ソリューションをリリースしました。独自のトークン化エンジン、リアルワールドデータへのアクセス、高度な臨床分析の専門知識を組み合わせることで、ICONは統合的でシームレスな運用モデルを提供し、製品開発ライフサイクル全体を通じて医薬品の安全性と有効性に関する貴重な長期的な洞察を提供します。2023年2月、Labcorpは臨床開発事業の分社化に伴い、新会社Fortreaを設立する計画を発表しました。 Labcorp からのスピンオフが完了すると、Fortrea は独立した上場グローバル CRO として運営され、包括的な医薬品および医療機器開発サービスを提供します。

要件に合わせてレポートをカスタマイズ

レポートの一部、国レベルの分析、Excelデータパックなどを含め、スタートアップ&大学向けに特別オファーや割引もご利用いただけます(無償)

臨床試験市場: 戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

臨床試験市場の推進要因と機会

臨床試験のアウトソーシングの慣行と試験数の大幅な増加が市場を活性化

臨床試験は、新しい形態の医療製品(薬剤、食事療法、医療機器など)が安全で効果的かどうかを判断するために実施されます。試験は主に全体的な医薬品開発プロセスの一部です。国立医学図書館(NLM)によると、2020年には約52,000件の新しい研究がNLM(ClinicalTrials.gov)に登録され、その数は2023年に約58,000件に増加しました。2023年1月、NLMは米国で38,837件、世界中で105,172件の臨床試験が実施されていると報告しました。欧州医薬品庁によると、欧州連合(EU)では年間約4,000件の臨床試験が承認されており、そのうち約60%の研究は製薬業界に関連しています。臨床試験数の急増は、世界中で慢性疾患の有病率が増加し、より効果的な治療法への大きな需要が生じていることに起因しています。

臨床試験の複雑さが増すにつれて、研究ベースの組織で行われる業務の適切な実行と監督の重要性が増しています。不適切な実行によるエラーを回避するために、多くの研究ベースの組織は臨床試験を臨床研究組織(CRO)に外注しています。CROは、高品質の施設と深い専門知識から提供するサービスを通じて、臨床試験の成功を支援します。試験スポンサーに利益をもたらす効率的で費用対効果の高い運用を通じて、CROは徐々に臨床試験業界のバックボーンになってきました。サーモフィッシャーサイエンティフィックが公開したブログによると、2022年には、医薬品開発者の臨床プログラムを安心させ、豊富な専門知識を提供し、時間とコストの効率を促進し、カスタマイズされた高品質のデータを提供するために、CROが約4件中3件の臨床試験を実施しました。したがって、臨床試験の数の増加と、費用対効果を高めエラーを減らすためにCROに試験をアウトソーシングする慣行は、臨床試験市場の成長を牽引する主な要因です。

分散型臨床試験とハイブリッド臨床試験の採用が市場に機会を提供

分散型臨床試験(DCT)に登録された被験者は、病院ベースの試験サイトに頻繁にアクセスする必要はありません。DCTでは、デジタル技術を使用して、リモートデータの収集とモニタリング、および調査員と参加者間の合理化されたコミュニケーションを可能にします。ハイブリッド臨床試験のアプローチは、在宅ベースとオンサイトの活動を組み合わせ、最高の患者体験をもたらし、複雑なプロトコル体制を満たすため、さまざまな治療領域と試験フェーズの過程で普及しています。患者のプライバシー、データセキュリティ、規制上の障壁、複雑なプロトコル体制などの課題は、過去にDCTの採用を妨げていました。しかし、COVID-19パンデミックにより、健康危機の中で対面研究が実行不可能になったため、臨床試験のスポンサーは、医薬品の開発に分散型およびハイブリッド臨床技術を採用せざるを得なくなりました。通勤に制限が課されたため、データを収集して試験を継続する唯一の方法は、リモートで作業し、プロセスを加速するテクノロジーを最適に活用することでした。マッキンゼーが提供したデータによると、臨床試験の潜在的な参加者の約70%は試験実施施設から離れた場所に居住しています。したがって、分散化により試験へのアクセスが広がり、より多様な患者プールで構成される可能性のあるより多くの被験者に到達できます。ハイブリッド臨床試験により、スポンサーはDCT要素を試験設計に戦略的に組み込むことができます。そのため、ハイブリッド試験に関心を示す企業が増えており、業界の状況が再定義されています。ObvioHealthによると、FDAは将来の臨床研究の信頼性を高めるために、2023年にDCT法の使用をサポートするプロトコルを発表する予定でした。したがって、従来の臨床試験方法よりも分散型およびハイブリッド臨床試験の使用への関心が高まっているため、予測期間中に臨床試験市場に有利な機会が提供されると予想されます。

臨床試験市場レポートのセグメンテーション分析

臨床試験市場分析の導出に貢献した主要なセグメントは、研究デザイン、適応症、およびフェーズです。

- 研究デザインに基づいて、臨床試験市場は介入試験と拡大アクセス試験に分かれています。介入試験セグメントは2023年に大きな市場シェアを占めました。

- 適応症別に見ると、市場は心血管疾患、腫瘍学的状態、神経疾患、自己免疫疾患/炎症、疼痛管理、糖尿病、肥満、代謝障害などに区分されています。腫瘍学的状態セグメントは2023年に最大の市場シェアを占めました。

- フェーズに基づいて、臨床試験市場はフェーズI、フェーズII、フェーズIIIに分かれています。フェーズIIセグメントは2023年に最大の市場シェアを占めました。

地域別の臨床試験市場シェア分析

臨床試験市場レポートの地理的範囲は、主に北米、アジア太平洋、ヨーロッパ、南米および中米、中東およびアフリカの5つの地域に分かれています。2023年には北米が市場を支配しました。米国は臨床試験の最大かつ最も急速に成長している市場です。米国は臨床研究の主要な拠点として台頭しており、様々な企業が革新的な臨床試験サービスを提供しています。米国は主要な臨床研究の拠点となっており、臨床試験の約半数が米国で実施されています。さらに、確立された医療インフラ、迅速な承認期間、好ましい規制枠組み、そして臨床試験で得られたデータが世界的に認められていることから、多くの製薬研究企業は米国での臨床試験の実施を好んでいます。世界保健機関(WHO)の報告書によると、2021年には米国で157,618件の臨床試験が実施され、世界最多の件数を記録しました。

臨床試験

臨床試験市場の地域別洞察

予測期間を通じて臨床試験市場に影響を与える地域的な傾向と要因は、The Insight Partnersのアナリストによって詳細に説明されています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東・アフリカ、中南米における臨床試験市場のセグメントと地域についても説明します。

臨床試験市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| の市場規模 2023 | US$ 43.37 Billion |

| 市場規模別 2031 | US$ 73.33 Billion |

| 世界的なCAGR (2023 - 2031) | 6.8% |

| 過去データ | 2021-2022 |

| 予測期間 | 2024-2031 |

| 対象セグメント |

By 研究デザイン

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

臨床試験市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

臨床試験市場は、消費者の嗜好の変化、技術の進歩、製品のメリットに対する認知度の高まりといった要因によるエンドユーザーの需要増加に牽引され、急速に成長しています。需要の増加に伴い、企業は提供内容の拡大、消費者ニーズへの対応のための革新、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

- 入手 臨床試験市場 主要プレーヤーの概要

臨床試験市場のニュースと最近の動向

臨床試験市場は、一次調査と二次調査後の定性的および定量的データを収集することで評価されます。これには、重要な企業の出版物、協会データ、データベースが含まれます。市場におけるいくつかの動向を以下に示します。

- Oracle は、Oracle Clinical One Randomization and Trial Supply Management (RTSM) の新機能を発表しました。使用、アクセス、地域化に関する新しい機能強化により、Clinical One RTSM ユーザーは、動的な国固有の規制要件に対応し、開始から終了までの試験のスピード、信頼性、透明性を向上させることができます。(出典: Oracle Corp、企業 Web サイト、2024 年 5 月)

- Parexel と人工知能 (AI) システムの大手構築企業である Palantir Technologies Inc.この提携により、パレクセルはパランティアのファウンドリーと人工知能プラットフォーム(AIP)を活用し、最高レベルの安全性と規制の厳格さを維持しながら臨床試験の効率性を高めることに重点を置いた臨床データ プラットフォームを強化します。 (出典:Parexel International Corp、企業ウェブサイト、2024年4月)

臨床試験市場レポートの対象範囲と成果物

「臨床試験市場規模と予測(2021~2031年)」レポートは、以下の分野を網羅した詳細な市場分析を提供します。

- 対象範囲に含まれるすべての主要市場セグメントにおける、世界、地域、国レベルでの臨床試験市場規模と予測

- 臨床試験市場の動向、および推進要因、制約要因、主要な機会などの市場動向

- 詳細なPEST分析とSWOT分析

- 主要な市場動向、世界および地域の枠組み、主要プレーヤー、規制、および最近の市場動向を網羅した臨床試験市場分析

- 市場集中、ヒートマップ分析、主要プレーヤー、および臨床試験市場の最近の動向を網羅した業界展望と競合分析

- 詳細な企業プロファイル

ムリナル氏は、ライフサイエンス分野の市場インテリジェンスとコンサルティングで8年以上の経験を持つ、経験豊富なリサーチアナリストです。戦略的な思考と揺るぎない卓越性へのコミットメントに基づき、医薬品市場予測、市場機会評価、業界ベンチマークの開発において深い専門知識を培ってきました。彼女の業務は、クライアントが情報に基づいた戦略的意思決定を行えるよう、実用的なインサイトを提供することに重点を置いています。

ムリナル氏の強みは、複雑な定量データセットを有意義なビジネスインテリジェンスへと変換することにあります。彼女の分析力は、医薬品および医療機器分野における市場開拓(GTM)戦略の策定と成長機会の発掘に大きく貢献しています。信頼できるコンサルタントとして、ワークフロープロセスの合理化とベストプラクティスの確立に常に注力し、クライアントのイノベーションと業務効率の向上に貢献しています。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応