航空宇宙用光ファイバーケーブル市場の概要、成長、傾向、分析、調査レポート(2019-2027)

2027年までの航空宇宙用光ファイバーケーブル市場予測 - COVID-19の影響とモード別(シングルモードおよびマルチモード)、用途別(レーダーシステム、フライトマネジメントシステム、キャビンマネジメントシステム、機内エンターテイメントシステム、電子戦、アビオニクス、その他)、取り付けタイプ別(ラインフィットおよびレトロフィット)、エンドユーザー別(商用および軍事)のグローバル分析

- ステータス : 出版

- レポートコード : TIPRE00006619

- カテゴリー : 航空宇宙および防衛

- ページ数 : 203

- 利用可能なレポート形式 :

- 最終更新日 : June 17, 2024

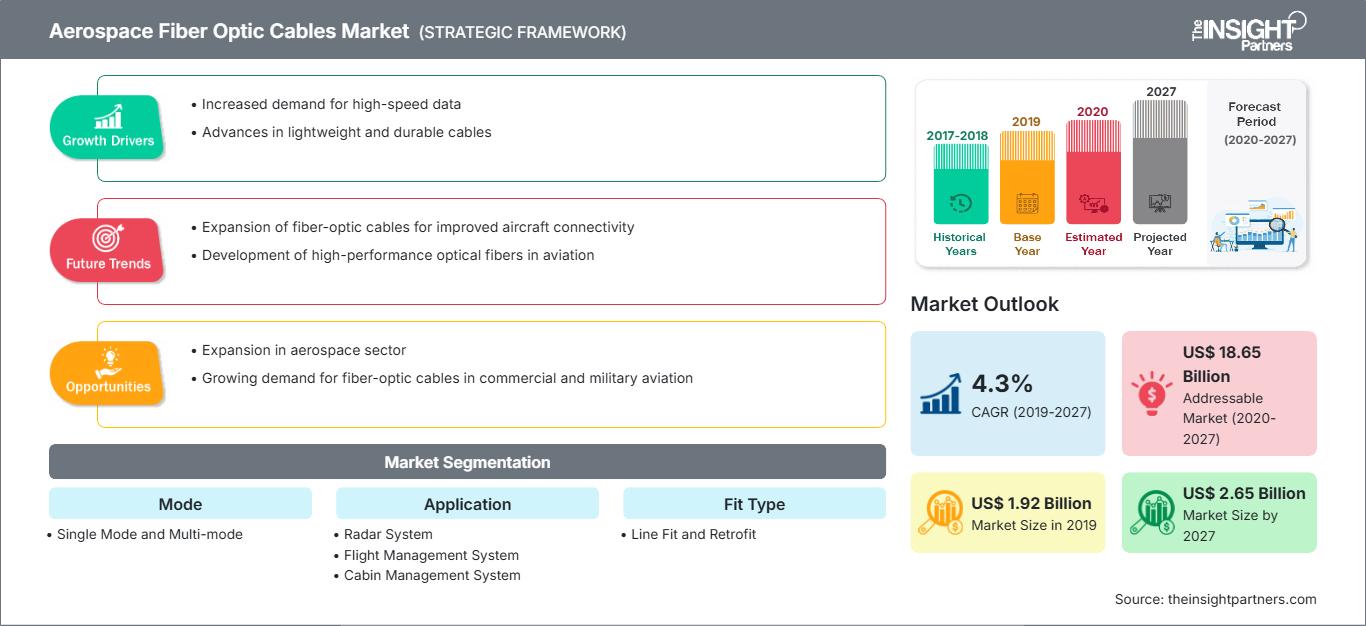

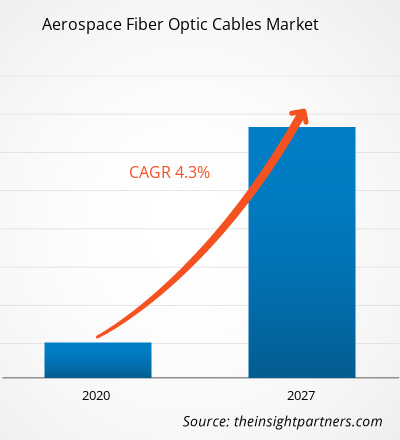

収益面では、航空宇宙用光ファイバーケーブル市場は2019年に19億2,465万米ドルと評価され、2027年には26億4,586万米ドルに達すると予測されています。予測期間中、CAGR 4.3%で成長すると見込まれています。

航空宇宙用光ファイバーケーブル市場の成長は、主に航空宇宙産業における先端技術への多額の投資によるものです。過去数十年にわたり、航空(商業および軍事)産業は飛躍的に成長し、技術革新の速度は目覚ましく、さまざまな製品やサービスの需要を刺激してきました。光ファイバーケーブルが先行技術の課題を克服し、軍事航空業界で大きなメリットを示していることに関連して、民間航空業界での需要が高まっており、航空宇宙用光ファイバーケーブル市場の成長を牽引しています。

地理的に見ると、航空宇宙用光ファイバーケーブル市場は、北米、ヨーロッパ、アジア太平洋、中東およびアフリカ、南米の 5 つの戦略的地域に基づいて分析されています。北米の航空宇宙産業には、多数の航空機メーカー、MRO サービスプロバイダー、および米国国防総省が存在します。この地域では先進技術に対する需要が非常に高く、上記のすべてのエンドユーザーは新しい技術を十分に認識しています。米国国防総省は、任務遂行能力を維持する目的で、既存の航空機の改良と堅牢な技術の航空機の開発に継続的に時間と金額を投資しています。このため、この地域では数十年前に軍用機への光ファイバーケーブルの導入が始まり、現在も新型軍用機への導入が続いています。同様に、この地域の民間航空宇宙部門はボーイングが主流で、同社もB787およびB777モデルに光ファイバーケーブルを導入しています。この導入は、コックピットおよび客室からの高速データ転送の需要の高まりと関係しています。MROサービスプロバイダーや社内MROセンターを持つ航空会社は、古い航空機に光ファイバーケーブルを後付けする取り組みを開始しており、これも北米の航空宇宙用光ファイバーケーブル市場の触媒となっています。この地域には多数の光ファイバーケーブルメーカーが存在するため、高まる需要を支え、航空宇宙用光ファイバーケーブル市場を押し上げています。

要件に合わせてレポートをカスタマイズ

レポートの一部、国レベルの分析、Excelデータパックなどを含め、スタートアップ&大学向けに特別オファーや割引もご利用いただけます(無償)

航空宇宙用光ファイバーケーブル市場: 戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

航空機製造業界は、ロボット技術にもかかわらず、手作業に大きく依存しています。いくつかの国で課された厳しいロックダウン規制の結果、航空機製造部門は、それぞれの航空機および部品製造施設で労働力不足に陥っています。航空機製造部門は主に北米とヨーロッパに集中しており、両地域は発生中の製造ペースを維持するという大きな課題に直面しています。ヨーロッパ諸国はさまざまな航空機部品を製造していますが、COVID-19感染者の増加は、ヨーロッパ諸国の大部分にとって大きな課題となっています。世界中の航空機メーカーは部品調達の深刻な落ち込みを目の当たりにしており、これは航空機生産の落ち込みを反映しています。

航空宇宙用光ファイバーケーブル市場のプレーヤーが北米、ヨーロッパ、およびAPAC地域に分散していることから、これらの地域での発生は、光ファイバーケーブルとサプライチェーンの適切な製造量の混乱をもたらしました。これは、航空宇宙用光ファイバーケーブル市場に悪影響を及ぼしています。

市場洞察:長距離での高帯域幅の需要の高まりが、航空宇宙用光ファイバーケーブル市場の成長を促進

近年、民間航空会社は、長距離路線の乗客数の増加により、長距離飛行を選択しています。長距離飛行では高速接続が求められます。イーサネットは、その高性能、信頼性、広く受け入れられているオープンスタンダードにより、長年にわたり民間航空会社の間でネットワークインフラストラクチャプロトコルとして最良の選択となっています。ただし、イーサネットネットワーク接続では、高帯域幅のデータを長距離で伝送するには限界があります。このため、いくつかの航空機ケーブルシステムメーカーが光ファイバーケーブル業界に参入し、近年、民間航空会社に利益をもたらしています。これは、航空宇宙用光ファイバーケーブル市場にプラスの影響を与えています。

モードベースの洞察

モード別では、マルチモードセグメントが2019年に世界の航空宇宙用光ファイバーケーブル市場で最大のシェアを獲得しました。シングルモード光ファイバーケーブルでは、一度に1種類の光モードしか分散できません。一方、マルチモード光ファイバーケーブルでは、光を複数のモードで分散させることができます。シングルモード光ファイバーケーブルとマルチモード光ファイバーケーブルの違いは、主にファイバーコア径、帯域幅、波長と光源、距離、コストによって異なります。

アプリケーションベースの洞察

アプリケーション別では、アビオニクスセグメントが2019年に世界の航空宇宙用光ファイバーケーブル市場で最大のシェアを獲得しました。アビオニクスアプリケーションに強く求められる技術の進歩には、曲げに強いファイバー、コネクタの互換性、帯域幅の広いファイバー、高密度相互接続、高出力レーザービーム伝送、市販の既製コンポーネントの受け入れなどがあります。航空電子機器の設計者は、ナビゲーション、通信、その他の重要な機能を処理できる組み込みシステムに、より多くのコンピューティング能力を搭載することに継続的に注力しています。これにより、重量が軽減され、データ伝送速度と帯域幅が高速化されるとともに、堅牢性とセキュリティが向上します。

取り付けタイプに基づく洞察

取り付けタイプに基づいて、航空宇宙用光ファイバーケーブル市場は、ライン取り付けとレトロフィットに分類されます。2019年、レトロフィットは世界の航空宇宙用光ファイバーケーブル市場で大きなシェアを獲得しました。航空宇宙用光ファイバーケーブルは、エアバスA380やボーイングB787などの新しい航空機モデルに既に完全に導入されています。航空会社は、高帯域幅のニーズの高まりを受けて、他のいくつかの古いモデルの商用航空機を運航しており、従来の銅線ケーブルを光ファイバーケーブルに置き換えています。この傾向は、従来の銅線ケーブルと比較してパフォーマンスが向上した、小型で軽量な配線に対する継続的な需要によって推進されています。高帯域幅の航空機の需要が高まるにつれて、光ファイバーの導入は、古い軍用機だけでなく民間航空機でも増加すると予想されます。

エンドユーザーベースの洞察

エンドユーザーに基づいて、航空宇宙光ファイバーケーブル市場は、商用と軍用に分割されています。 2019年、軍事セグメントは世界の航空宇宙光ファイバーケーブル市場で大きなシェアを獲得しました。 ファイバーネットワークとケーブルアセンブリのプロバイダーは、潜在的な敵に対する改善を維持するために、新しい能力と改善されたパフォーマンスに対する絶え間ないニーズを満たすために、軍用機の設計者を支援しています。 これらのファイバーネットワークは、新世代の高度なビジョンシステム、航空電子機器、およびその他の新興技術をサポートするために、徐々に高度化しています。

世界中の航空宇宙光ファイバーケーブル市場に多数の確立されたプレーヤーと新興企業が存在することは、エンドユーザーからの高まる需要を支えています。航空機メーカー、航空機部品メーカー、および改修エンドユーザーへの光ファイバーケーブルの継続的な供給は、成熟しつつある航空宇宙用光ファイバーケーブル市場で重要な役割を果たしています。 航空宇宙用光ファイバーケーブル市場における最近の買収のいくつかを以下に示します。

2019 年:Amphenol Aerospace は、Samtec と提携して新しい Centaur 高速ケーブル アセンブリを設計および開発しました。このアセンブリは、Amphenol の幅広いミルスペック コネクタのポートフォリオと最新の高速コンタクトおよびコネクタ技術の両方の利点と、Samtec の ExaMAX 高速バックプレーン システムを活用して、航空宇宙、軍事、その他の堅牢なアプリケーションに最適な、耐久性があり完全にテストされた高帯域幅接続を提供します。 2018 年:WL Gore & Associates UK Ltd. は、軍用高速航空電子工学ネットワーク上でミッションクリティカルなデータを毎秒 10 ギガビットの速度で転送するための、耐久性の高い 1.8 ミリメートル シンプレックス航空宇宙用光ファイバー ケーブルを発表しました。

航空宇宙用光ファイバーケーブル市場の地域別分析

予測期間全体を通して航空宇宙用光ファイバーケーブル市場に影響を与える地域的な動向と要因については、The Insight Partnersのアナリストが詳細に解説しています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東・アフリカ、中南米における航空宇宙用光ファイバーケーブル市場のセグメントと地域についても解説しています。

航空宇宙用光ファイバーケーブル市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| の市場規模 2019 | US$ 1.92 Billion |

| 市場規模別 2027 | US$ 2.65 Billion |

| 世界的なCAGR (2019 - 2027) | 4.3% |

| 過去データ | 2017-2018 |

| 予測期間 | 2020-2027 |

| 対象セグメント |

By モード

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

航空宇宙用光ファイバーケーブル市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

航空宇宙用光ファイバーケーブル市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認知度の高まりといった要因によるエンドユーザーの需要増加に牽引され、急速に成長しています。需要の増加に伴い、企業は製品ラインナップの拡充、消費者ニーズへの対応のための革新、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

- 入手 航空宇宙用光ファイバーケーブル市場 主要プレーヤーの概要

- シングルモード

- マルチモード

航空宇宙用光ファイバーケーブル市場 – 用途別

- レーダー システム

- フライト マネジメント システム

- キャビン マネジメント システム

- 機内エンターテイメント システム

- 電子戦

- 航空電子機器

- その他

航空宇宙用光ファイバーケーブル市場 – 取り付けタイプ別

- ライン フィット

- レトロフィット

航空宇宙用光ファイバーケーブル市場 –エンドユーザー別

- 商業

- 軍事

地域別航空宇宙光ファイバーケーブル市場

-

北米

- 米国

- カナダ

- メキシコ

-

ヨーロッパ

- フランス

- ドイツ

- イタリア

- 英国

- ロシア

- その他ヨーロッパ

-

アジア太平洋地域 (APAC)

- 中国

- インド

- 韓国

- 日本

- オーストラリア

- その他APAC地域

-

中東・アフリカ (MEA)

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- MEAの残りの部分

-

南アメリカ(SAM)

- ブラジル

- アルゼンチン

- SAMの残りの部分

航空宇宙光ファイバーケーブル市場で紹介されている企業は次のとおりです。以下:

- Amphenol Corporation

- AFL

- Carlisle Interconnect Technologies

- Collins Aerospace (Raytheon Technologies Corp.)

- Nexans SA

- WL Gore & Ltd. Associates, Inc.

- Timbercon, Inc.

- TE Connectivity

- Prysmian Group

- OFS Fitel, LLC

Naveenは、カスタム、シンジケート、コンサルティングの各プロジェクトにおいて9年以上の実績を持つ、経験豊富な市場調査およびコンサルティングのプロフェッショナルです。現在はアソシエイトバイスプレジデントを務め、プロジェクトバリューチェーン全体にわたるステークホルダー管理を成功させ、100件以上の調査レポートと30件以上のコンサルティング案件を執筆しています。産業および政府機関のプロジェクトに幅広く携わり、クライアントの成功とデータに基づく意思決定に大きく貢献しています。

Naveenは、カルナータカ州VTUで電子通信工学の学位を取得し、マニパル大学でマーケティング&オペレーションズのMBAを取得しています。IEEEの会員として9年間活動し、会議や技術シンポジウムへの参加、セクションレベルおよび地域レベルでのボランティア活動に積極的に取り組んでいます。現職以前は、IndustryARCでアソシエイト戦略コンサルタント、Hewlett Packard(HP Global)で産業用サーバーコンサルタントを務めていました。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応