遺伝子検査サービス市場戦略、トッププレーヤー、成長機会、分析、2031年までの予測

遺伝子検査サービス市場の規模と予測(2021年 - 2031年)、世界および地域のシェア、傾向、成長機会分析レポートの対象範囲:サービスタイプ(予測検査、キャリア検査、出生前検査、新生児スクリーニング、診断遺伝子検査など)、疾患(がん、心血管疾患、代謝性疾患、その他の疾患)、サービスプロバイダー(病院ベースの研究所、診断研究所など)、および地域別

- ステータス : 出版

- レポートコード : TIPHE100001383

- カテゴリー : ライフサイエンス

- ページ数 : 247

- 利用可能なレポート形式 :

- 最終更新日 : December 18, 2024

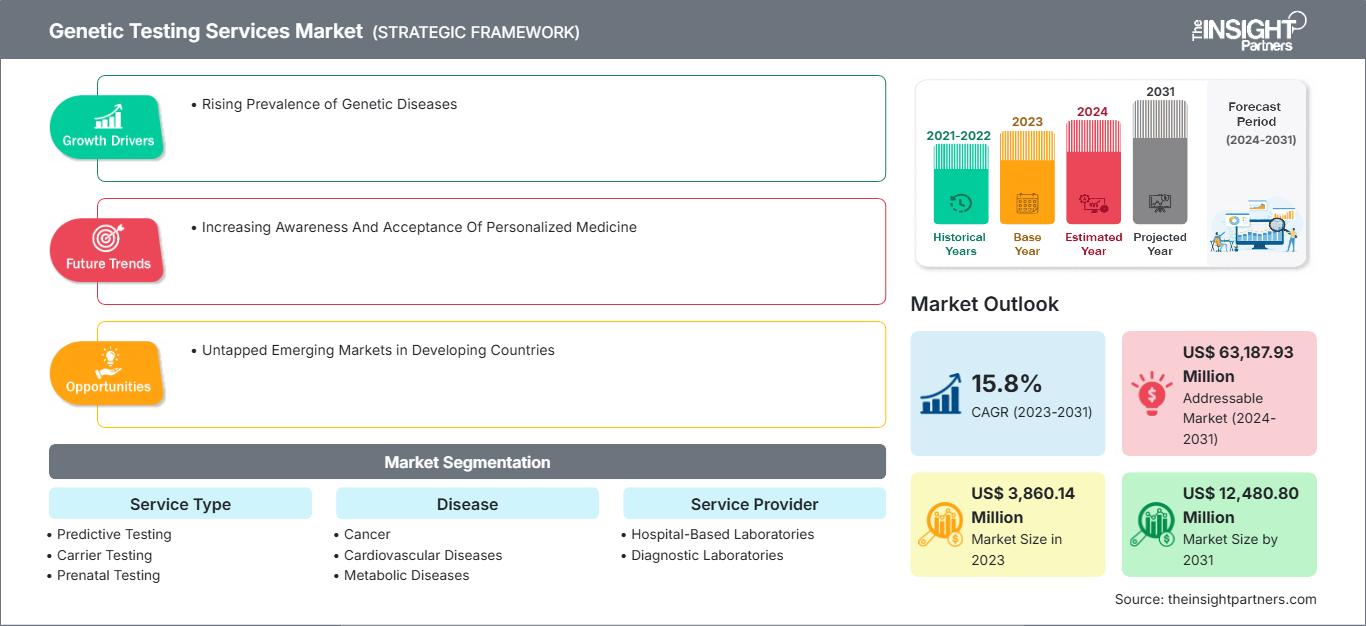

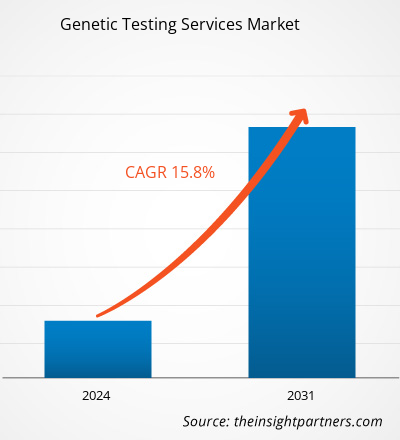

遺伝子検査サービス市場規模は、2023年の38億6,014万米ドルから、2031年には124億8,080万米ドルに達すると予測されています。市場は2023年から2031年の間に15.8%のCAGRを記録すると予想されています。人工知能を活用した遺伝子検査は、今後数年間で遺伝子検査サービス市場に新たなトレンドをもたらすと見込まれます。

遺伝子検査サービス市場分析

遺伝子検査サービス市場を牽引する要因には、償還プログラムの導入、効率的な治療法の選択肢に対する需要の高まり、研究センターにおける革新的技術の実装などが挙げられます。遺伝子検査の利点に対する認識の高まりとヘルスケアに対する消費者支出の増加が、遺伝子検査サービス市場の成長を後押ししています。慢性疾患の診断を目的とした遺伝子検査の需要増加は、新サービスの開発と拡大戦略への投資においてプレーヤーを支援してきました。さらに、遺伝性疾患やがんの発生率の増加は、遺伝子検査業界の発展に重要な役割を果たしています。

遺伝子検査サービス市場概要

遺伝子検査は、個人のDNAを検査・分析し、遺伝子構成や遺伝情報を理解するための医学的・科学的手法です。英国の遺伝子検査サービス市場は、遺伝性疾患やがんの罹患率の上昇により、大幅に成長すると予想されています。例えば、Genetic Alliance UK 2021によると、希少疾患は英国で350万人、つまり17人に1人が罹患しています。 Gene People UK 2023によると、25人に1人の子供が遺伝性疾患を患っていると推定されています。これは、英国で毎年3万人の乳幼児が新たに診断され、240万人以上の子供と成人が遺伝性疾患を患っていることを意味します。

ドイツでは、2022年に非侵襲性出生前検査が公的に償還される検査として利用可能になりました。さらに、ゲノミクスの大きな進歩により、個別化医療へのアクセス向上への道が開かれています。英国は、臨床サービスを提供するゲノム研究所とゲノム医療センターの全国ネットワークを含む、ゲノム検査へのアクセス向上を支援するインフラストラクチャを構築しました。2019年には、政府が早期疾患検出研究プロジェクトUKを発表しました。これは、すべてのがん、心血管疾患、その他の同様の疾患を含む、成人の主要な慢性疾患に焦点を当てた重要な新しいイニシアチブです。

要件に合わせてレポートをカスタマイズ

レポートの一部、国レベルの分析、Excelデータパックなどを含め、スタートアップ&大学向けに特別オファーや割引もご利用いただけます(無償)

遺伝子検査サービス市場: 戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

遺伝子検査サービス市場の推進要因と機会

遺伝性疾患の罹患率の上昇が市場成長を後押し

遺伝性疾患の罹患率は世界中で上昇しており、人々の健康に深刻な影響を及ぼしています。遺伝性疾患は、まれで、ほとんどが治癒不可能な症状を多く示します。世界保健機関(WHO)2021によると、1,000人中10人が単一遺伝子疾患に罹患しており、世界中で7,000万人から8,000万人が何らかの単一遺伝子疾患を抱えて生活していることを示しています。Global Genesによると、世界中で約7,000の希少疾患や障害が特定されており、毎年さらに多くの疾患が発見されています。2022年には、MJH Life Sciences(米国)のレポートで、世界中で毎年30万人の新生児が鎌状赤血球症を持って生まれており、これは世界人口の約5%に相当すると推定されています。ノバルティスAG(スイス)の報告によると、2020年6月、英国では15,000人が鎌状赤血球症に罹患しており、毎年270人の新生児がこの病気と診断されています。このように、遺伝性疾患の有病率の上昇は遺伝子検査の需要を促進し、それが今度は遺伝子検査サービス市場の成長を促進します。

発展途上国の未開拓の新興市場

中国、インド、ブラジル、メキシコなどの新興国は、市場プレーヤーに大きな成長機会を提供しています。遺伝子サービスの質と利用可能性は、高所得国と低所得国から中所得国で異なる場合があります。たとえば、米国、オーストラリア、カナダ、英国、その他のヨーロッパ諸国では、遺伝子サービスは十分に進歩し、確立されており、広範です。これらのサービスには、新生児スクリーニング、キャリア識別スクリーニング、出生前診断が含まれます。しかし、多くの高所得国では、複数の環境で提供されている遺伝子サービスには、依然として改善された評価システムが必要です。主要な市場プレーヤーは、これらの国々での製品の入手可能性、アクセス性、流通ネットワークを改善するための契約、協力、パートナーシップ、拡張などの戦略とイニシアチブに重点を置いています。これは、高まる早期診断と治療のニーズに対応するのに役立ちます。

中国政府は、国の経済と社会の発展のための第14次5カ年計画(2016~2020年)において、ゲノミクスを重要な戦略分野と位置付けています。2016年、中国科学院は、2030年までに1億人以上のヒトゲノムの配列を決定することを目指す、92億ドル規模の14年間のプロジェクトである精密医療イニシアチブを開始しました。2017年12月、中国科学技術部は、10万人の遺伝子構成を記録するためのヒトゲノム研究プロジェクトと協力しました。研究者たちは、9つの異なる少数民族の遺伝子データを用いて、遺伝子内の遺伝情報を解読したいと考えています。したがって、開発途上国の新興市場は、予測期間中に遺伝子検査サービス市場の成長に有利な機会を提供すると予想されます。

遺伝子検査サービス市場レポートのセグメンテーション分析

遺伝子検査サービス市場分析の導出に貢献した主要なセグメントは、サービスタイプ、疾患、およびサービスプロバイダーです。

- サービスタイプに基づいて、遺伝子検査サービス市場は、予測検査、キャリア検査、出生前検査、新生児スクリーニング、診断遺伝子検査などに分類されます。予測検査セグメントは2023年に市場で最大のシェアを占め、2023年から2031年にかけて市場で最高のCAGRを記録すると予想されます。

- 疾患別に、遺伝子検査サービス市場は、がん、心血管疾患、代謝性疾患、その他の疾患に分類されます。がん分野は2023年に最大の市場シェアを占め、2023~2031年には市場で最も高いCAGRを記録すると予測されています。

- サービスプロバイダーの観点から見ると、遺伝子検査サービス市場は、病院ベースの検査室、診断検査室、その他に分類されます。病院ベースの検査室セグメントは2023年に最大の市場シェアを占め、2023~2031年には市場で最も高いCAGRを記録すると予想されています。

遺伝子検査サービス市場シェアの地域別分析

遺伝子検査サービス市場レポートの地理的範囲は、主に北米、アジア太平洋、ヨーロッパ、中東およびアフリカ、南米および中米の5つの地域に分かれています。 2023年には北米が市場シェアを大きく伸ばしました。市場の成長は、近年の米国とカナダにおけるがん患者数の増加、政府資金の増加、そして人口における遺伝性疾患の発症率の上昇によって牽引されています。2021年10月に発表された米国会計検査院の推計によると、米国では約2,500万人から3,000万人が希少疾患に苦しんでおり、希少疾患患者の約50%は小児です。希少疾患は遺伝子変異に起因することが多く、希少疾患の80%は遺伝性であると推定されています。

さらに、医療における高度な手法の導入への関心の高まり、精密医療の推進に向けた政府および民間の取り組み、そして政府および民間団体からの遺伝子研究への巨額の資金提供が、この地域における遺伝子検査サービス市場の成長を加速させると予測されています。

遺伝子検査サービス市場の地域別分析

予測期間を通じて遺伝子検査サービス市場に影響を与える地域的な動向と要因については、The Insight Partnersのアナリストが詳細に解説しています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東・アフリカ、中南米における遺伝子検査サービス市場のセグメントと地域についても解説しています。

遺伝子検査サービス市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| の市場規模 2023 | US$ 3,860.14 Million |

| 市場規模別 2031 | US$ 12,480.80 Million |

| 世界的なCAGR (2023 - 2031) | 15.8% |

| 過去データ | 2021-2022 |

| 予測期間 | 2024-2031 |

| 対象セグメント |

By サービスの種類

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

遺伝子検査サービス市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

遺伝子検査サービス市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認知度の高まりといった要因によるエンドユーザーの需要増加に牽引され、急速に成長しています。需要の増加に伴い、企業はサービスを拡大し、消費者ニーズを満たすための革新を進め、新たなトレンドを活用しており、これが市場の成長をさらに促進しています。

- 入手 遺伝子検査サービス市場 主要プレーヤーの概要

遺伝子検査サービス市場のニュースと最近の動向

遺伝子検査サービス市場は、一次調査と二次調査後の定性的および定量的データを収集することで評価されます。これには、重要な企業の出版物、協会データ、データベースが含まれます。遺伝子検査サービス市場のいくつかの動向を以下に示します。

- GeneDx は、診断を迅速化し、患者の診断の旅を短縮することを目指して、全ゲノム配列決定 (WGS) サービスを強化しました。これらの新機能には、迅速な全ゲノム配列決定 (rWGS)、口腔サンプル、および反復拡張のターンアラウンド時間の短縮が含まれます。業界をリードするデータセットと製品の機能強化を組み合わせることで、GeneDx は診断目的での全ゲノム配列決定のアクセシビリティと有効性を改善し、最終的には一般的な病気とまれな病気の両方の進行を阻止または軽減することに取り組んでいます。 (出典: GeneDx、プレスリリース、2024年7月)

- 米国に本社を置く世界的に有名な遺伝子検査ブランドであるProgenesisは、ニューデリーに最初の遺伝子研究所、チェンナイに人工知能(AI)およびバイオインフォマティクスデータセンターを開設し、インド市場に参入しました。同ブランドは、地元の医療提供者、不妊治療クリニック、医療従事者と協力して事業範囲を拡大し、高度な遺伝子検査ソリューションをより幅広い層に提供できるようにしています。(出典: Progenesis、プレスリリース、2023年12月)

遺伝子検査サービス市場レポートの対象範囲と成果物

「遺伝子検査サービス市場規模および予測(2021~2031年)」このレポートでは、以下の分野を網羅した市場の詳細な分析を提供しています。

- 遺伝子検査サービス市場の規模と予測(対象範囲に含まれるすべての主要市場セグメントについて、世界、地域、国レベルで)

- 遺伝子検査サービス市場の動向、および推進要因、制約、主要な機会などの市場動向

- 詳細なPEST分析とSWOT分析

- 主要な市場動向、世界および地域の枠組み、主要プレーヤー、規制、最近の市場動向を網羅した遺伝子検査サービス市場分析

- 市場集中、ヒートマップ分析、主要プレーヤー、遺伝子検査サービス市場の最近の動向を網羅した業界状況と競争分析

- 詳細な企業プロファイル

ムリナル氏は、ライフサイエンス分野の市場インテリジェンスとコンサルティングで8年以上の経験を持つ、経験豊富なリサーチアナリストです。戦略的な思考と揺るぎない卓越性へのコミットメントに基づき、医薬品市場予測、市場機会評価、業界ベンチマークの開発において深い専門知識を培ってきました。彼女の業務は、クライアントが情報に基づいた戦略的意思決定を行えるよう、実用的なインサイトを提供することに重点を置いています。

ムリナル氏の強みは、複雑な定量データセットを有意義なビジネスインテリジェンスへと変換することにあります。彼女の分析力は、医薬品および医療機器分野における市場開拓(GTM)戦略の策定と成長機会の発掘に大きく貢献しています。信頼できるコンサルタントとして、ワークフロープロセスの合理化とベストプラクティスの確立に常に注力し、クライアントのイノベーションと業務効率の向上に貢献しています。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応