股関節インプラント市場の規模、シェア、需要予測(2034年まで)

股関節インプラント市場規模と予測(2021年~2034年)、世界および地域別シェア、トレンド、成長機会分析レポートの対象範囲:製品タイプ別(全股関節置換術、部分股関節置換術、股関節表面置換術、股関節再置換術)、材料タイプ別(金属-ポリエチレン、セラミック-セラミック、セラミック-金属、セラミック-ポリエチレン、その他)、エンドユーザー別(病院、整形外科クリニック、外来手術センター、その他)、地域別(北米、ヨーロッパ、アジア太平洋、中東およびアフリカ、南米および中米)

- ステータス : 出版

- レポートコード : TIPMD00002030

- カテゴリー : ライフサイエンス

- ページ数 : 252

- 利用可能なレポート形式 :

- 最終更新日 : May 29, 2026

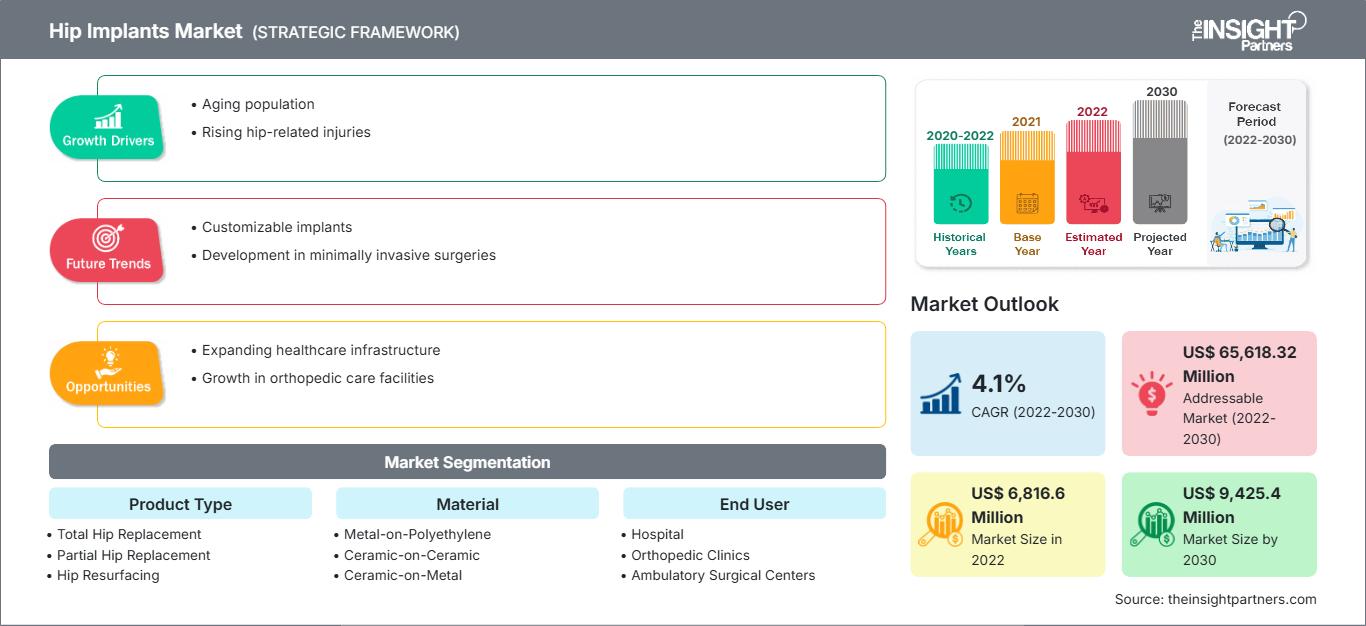

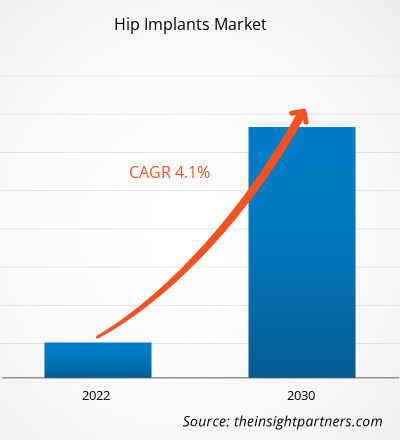

股関節インプラント市場の規模は、2025年の82億7000万米ドルから2034年には120億4000万米ドルに達すると予測されている。同市場は2026年から2034年にかけて年平均成長率(CAGR)4.3%を記録すると見込まれている。

股関節インプラント市場分析

世界の股関節インプラント市場は、変形性関節症や股関節骨折の増加、そして高齢者人口の増加によって牽引されています。肥満の蔓延と生活習慣病による関節疾患の増加は、股関節置換手術の需要を高めています。インプラント用のセラミックおよびチタン材料の開発は、インプラントの耐久性と患者の治療成績の向上に貢献しています。低侵襲手術を選択する人が増え、手術技術も向上しています。新興国では医療費の上昇と整形外科サービスへのアクセス向上が見られます。

股関節インプラント市場の概要

世界の股関節インプラント市場は、可動性を回復し生活の質を向上させるための高度な整形外科ソリューションへの需要の高まりにより、着実に拡大しています。高齢化の進展に加え、変性骨疾患や外傷性損傷の罹患率の上昇に伴い、手術件数が増加しています。インプラント設計におけるカスタマイズ医療機器や3Dプリント医療機器の開発は、精度向上と耐用年数の延長につながっています。発展途上地域における医療施設の整備は、患者が治療を受ける機会を増やしています。関節置換手術の利点についてより多くの人々が認識し、各国がより優れた医療費償還制度を整備していることから、病院や整形外科センターにおける股関節インプラント手術の導入は増加の一途をたどっています。

お客様のご要望に合わせてこのレポートをカスタマイズしてください

無料カスタマイズ股関節インプラント市場:戦略的洞察

-

本レポートの主要市場トレンドをご覧ください。この無料サンプルには、市場動向から予測、見通しまで、幅広いデータ分析が含まれています。

股関節インプラント市場の推進要因と機会

市場の推進要因:

- 高齢化人口の増加:高齢者人口の急増は、股関節置換手術の需要増加につながります。なぜなら、高齢者は関節の変性、骨折、および運動機能障害を発症する可能性が高いためです。

- 変形性関節症の有病率の上昇:変形性関節症の発生率の上昇は、患者が痛みを軽減し、関節の機能を回復するために外科的治療を必要とするため、股関節インプラントの需要増加につながります。

- 外傷、肥満、生活習慣に関連する怪我の急増:交通事故の発生件数の増加、肥満率の上昇、座りがちな生活習慣の蔓延は、より重篤な股関節損傷につながり、外科的インプラント手術の必要性を高めています。

市場機会:

- 新興市場における拡大:新興経済国は、医療制度が拡大し、人々が手頃な価格で高度な股関節インプラントソリューションにアクセスしやすくなっているため、有望な成長の可能性を秘めている。

- パーソナライズされた3Dプリント製カスタムインプラント:3Dプリンティング技術の発展により、患者一人ひとりの身体的ニーズに合わせたパーソナライズされた股関節インプラントの作成が可能になり、手術結果の向上と精密な整形外科ソリューションの利用拡大につながります。

- 外来および日帰り手術への移行:外来手術を選択する人が増えていることで入院期間が短縮され、医療費の削減と、日帰り手術センターでの低侵襲股関節インプラント手術の利用増加につながっています。

股関節インプラント市場レポートのセグメンテーション分析

股関節インプラント市場は、その事業内容、成長可能性、および現在のトレンドをより明確に理解するために、いくつかの明確なカテゴリーに分類されています。以下は、業界レポートで一般的に使用されているセグメンテーション手法です。

製品タイプ別:

- 人工股関節全置換術:重度の関節炎や骨折など、関節全体の置換が必要となる場合が、人工股関節全置換術の主な理由です。高齢者人口の増加と、インプラントの耐久性の向上に伴い、この手術法が広く普及しています。

- 部分股関節置換術:部分股関節置換術は、大腿骨頸部骨折を患う高齢患者にとって効果的な治療法です。この手術は、手術時間の短縮、患者の早期回復、手術合併症のリスク低減といった利点があります。

- 股関節表面置換術:金属対金属インプラントシステムの開発により、活動的な若い患者は股関節表面置換術を選択することが多くなりました。この手術は骨構造の大部分を温存し、より良い動きを可能にするためです。

- 人工股関節再置換術:初回人工股関節の故障率が高く、人々の寿命が延びているため、関節の機能と安定性を回復するための手術件数が増加しており、人工股関節再置換術の需要は増加し続けています。

材質別:

- 金属とポリエチレン

- セラミック・オン・セラミック

- セラミック・オン・メタル

- ポリエチレン上のセラミック

- その他

エンドユーザー別:

- 病院

- 整形外科クリニック

- 外来手術センター

- その他

地域別:

- 北米

- ヨーロッパ

- アジア太平洋地域

- 南米および中央アメリカ

- 中東およびアフリカ

股関節インプラント市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2025年の市場規模 | 82億7000万米ドル |

| 2034年までの市場規模 | 120億4000万米ドル |

| 世界の年間平均成長率(2026年~2034年) | 4.3% |

| 履歴データ | 2021年~2024年 |

| 予測期間 | 2026年~2034年 |

| 対象分野 |

製品タイプ別

|

| 対象地域および国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

股関節インプラント市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

股関節インプラント市場は、消費者の嗜好の変化、技術革新、製品の利点に対する認識の高まりといった要因によるエンドユーザー需要の増加を背景に、急速に成長しています。需要の高まりに伴い、企業は製品ラインナップを拡充し、消費者のニーズに応えるべく革新を進め、新たなトレンドを活用することで、市場の成長をさらに促進しています。

股関節インプラント市場の地域別シェア分析

アジア太平洋地域は市場が最も急速に成長している地域です。南米、中東、アフリカの新興市場には、股関節インプラント供給業者にとって事業拡大のための未開拓の機会が存在します。

股関節インプラント市場の成長は、高齢化の進展、医療インフラの改善、手術件数の増加、医療ツーリズムの急増などにより、地域によって大きく異なります。以下に、地域別の市場シェアと動向の概要を示します。

1. 北アメリカ

- 市場シェア:世界市場のかなりの部分を占めている

- 主な推進要因:北米は、高度な医療インフラ、高い手術率、革新的な股関節インプラント技術の普及率の高さにより、成長を牽引している。

- トレンド:ロボット支援による股関節置換術の普及拡大、外来手術センターへの移行の加速、リアルタイムモニタリング機能を備えたスマートインプラントの使用増加。

2. ヨーロッパ

- 市場シェア:相当な市場シェア

- 主な推進要因:高齢化の進行、充実した公的医療制度、整形外科治療に対する高い意識。

- トレンド:生体適合性と耐久性に優れたインプラント材料の拡大、規制強化によるイノベーション(EU MDR)、治療最適化のためのデータ駆動型整形外科レジストリの利用増加。

3. アジア太平洋

- 市場シェア:市場シェアが毎年増加している、最も成長率の高い地域

- 主な推進要因:高齢者人口の増加、医療へのアクセス改善、医療ツーリズムの増加、整形外科手術の増加。

- トレンド:費用対効果の高いインプラントの急速な普及、国内製造の拡大、低侵襲手術の増加、新興国におけるデジタル整形外科ソリューションの普及率の上昇。

4. 南米および中央アメリカ

- 市場シェア:着実に市場シェアを拡大

- 主な要因:医療施設の改善、外傷症例の増加、都市部における股関節置換手術の費用負担軽減。

- トレンド:民間病院への投資の増加、手頃な価格のインプラントの入手可能性の向上、外傷治療手順の拡大、および高度な外科手術技術の段階的な導入。

5. 中東とアフリカ

- 市場シェア:市場シェアは小さいが、急速に成長している

- 主な推進要因:医療インフラの整備、医療投資の増加、高度な整形外科手術ソリューションに対する需要の高まり。

- トレンド:医療ツーリズムの増加、GCC諸国における高度な整形外科センターの発展、政府の医療費支出の増加、都市部におけるインプラント手術へのアクセス改善。

市場密度の高さと競争の激しさ

Zimmer Biomet Holdings IncやStryker Corpといった老舗企業が存在するため、競争は激しい。地域密着型企業やニッチ市場の企業も、各地域における競争環境をさらに複雑にしている。

激しい競争環境下では、企業は他社との差別化を図るために以下のような施策を講じる必要がある。

- 先進的な製品とサービス

- 規制ガイドラインの遵守

機会と戦略的動き

- 股関節インプラント市場は、新興経済国、先進的なインプラント技術、個別化されたソリューション、そして低侵襲手術への需要の高まりを通じて成長が見込まれる。

- 企業は、競争優位性を得るために、製品イノベーション、病院との提携、地理的拡大、ロボット工学や3Dプリンティングの導入に注力している。

調査過程で分析されたその他の企業:

- メドトロニック社

- コンフォーミス株式会社

- グローバス・メディカル社

- NuVasive Inc.

- アートレックス社

- マイクロポート・サイエンティフィック・コーポレーション

- ヴァルデマール・リンク有限会社

- Orthofix Medical Inc.

- メダクタ・インターナショナルSA

- エスクラプインプラントシステム

- インテグラ・ライフサイエンス・ホールディングス株式会社

- LimaCorporate SpA

股関節インプラント市場のニュースと最新動向

- 2025年10月、世界的な医療技術リーダーであるZimmer Biomet Holdings, Inc.は、米国食品医薬品局(FDA)が同社初のヨウ素処理人工股関節置換システムに画期的医療機器指定(Breakthrough Device Designation)を付与したことを発表しました。これは、Zimmer Biometの歴史上、この指定を受けた初の製品となります。

- 2025年12月、手術ナビゲーション技術のグローバルリーダーであるOrthAlign社は、人工股関節全置換術(THA)における後方アプローチ支援を提供するLantern Hipプラットフォームの拡張を発表しました。このプラットフォームは臨床的有用性を向上させ、外科医は患者の体位(側臥位または仰臥位)の好みに関わらず、あらゆるTHA手術にLantern Hipを使用できるようになります。

股関節インプラント市場レポートの対象範囲と成果物

「股関節インプラント市場規模と予測(2026年~2034年)」レポートは、以下の分野を網羅した市場の詳細な分析を提供します。

- 股関節インプラント市場の規模と予測(グローバル、地域、国レベル)を、調査範囲に含まれるすべての主要市場セグメントについて分析します。

- 股関節インプラント市場の動向、および推進要因、阻害要因、機会などの市場ダイナミクス

- 詳細なPEST分析とSWOT分析

- 股関節インプラント市場の分析:主要トレンド、グローバルおよび地域的な枠組み、主要企業、規制、および最近の市場動向を網羅

- 股関節インプラント市場における市場集中度、ヒートマップ分析、主要企業、および最近の動向を網羅した業界概況と競争分析

- 詳細な企業プロフィール

ムリナル氏は、ライフサイエンス分野の市場インテリジェンスとコンサルティングで8年以上の経験を持つ、経験豊富なリサーチアナリストです。戦略的な思考と揺るぎない卓越性へのコミットメントに基づき、医薬品市場予測、市場機会評価、業界ベンチマークの開発において深い専門知識を培ってきました。彼女の業務は、クライアントが情報に基づいた戦略的意思決定を行えるよう、実用的なインサイトを提供することに重点を置いています。

ムリナル氏の強みは、複雑な定量データセットを有意義なビジネスインテリジェンスへと変換することにあります。彼女の分析力は、医薬品および医療機器分野における市場開拓(GTM)戦略の策定と成長機会の発掘に大きく貢献しています。信頼できるコンサルタントとして、ワークフロープロセスの合理化とベストプラクティスの確立に常に注力し、クライアントのイノベーションと業務効率の向上に貢献しています。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応