断熱包装材料市場の動向、需要、成長(2034年まで)

断熱包装材市場の規模と予測(2021年 - 2034年)、世界および地域のシェア、傾向、成長機会分析レポートの対象範囲:材料タイプ(プラスチック、木材、段ボール、その他)、タイプ(使い捨ておよび再利用可能)、およびエンドユーザー(医薬品、食品および飲料、化粧品、工業用、その他)別

- ステータス : 公開されたデータ

- レポートコード : TIPRE00024959

- カテゴリー : 化学薬品および材料

- ページ数 : 150

- 利用可能なレポート形式 :

- 最終更新日 : February 13, 2026

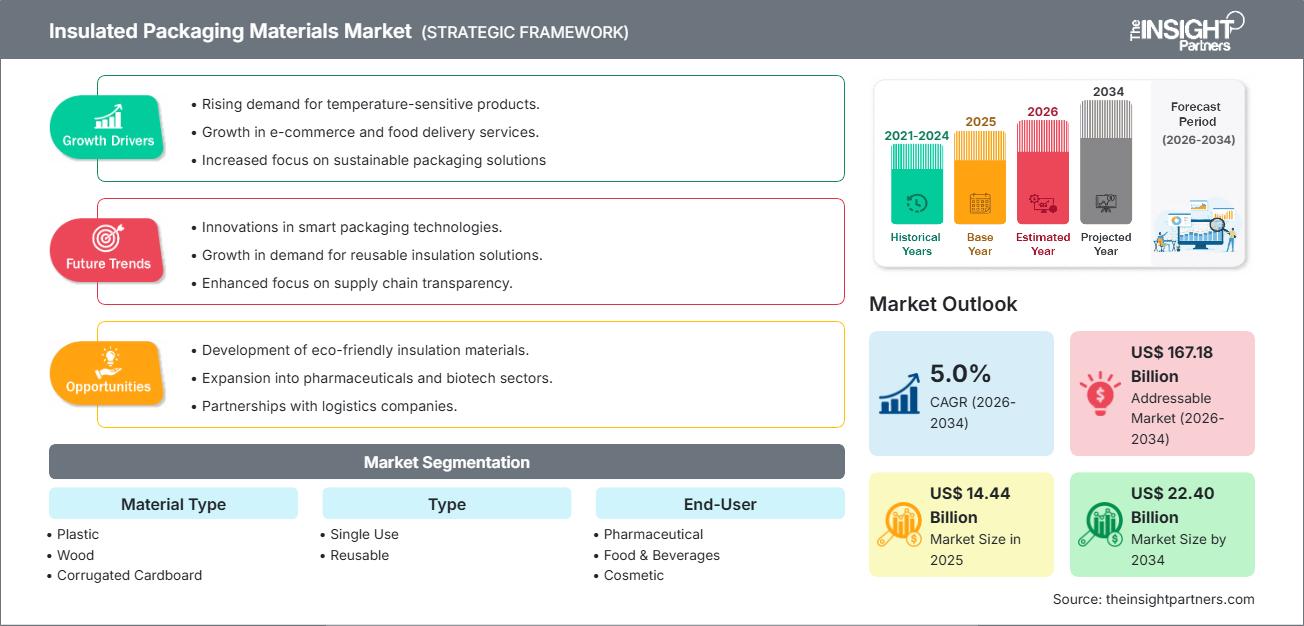

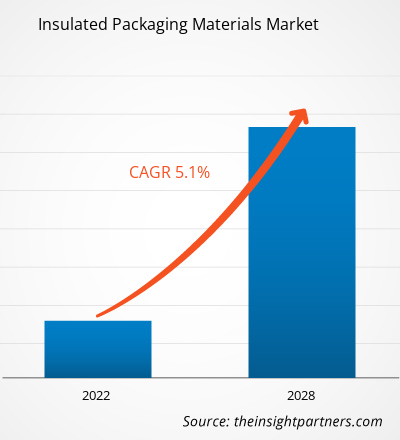

世界の断熱包装材市場規模は、2025年の144億4,000万米ドルから2034年には224億米ドルに達すると予測されています。市場は2026年から2034年の予測期間中、年平均成長率(CAGR)5.0%で成長すると見込まれています。市場の主要な動向としては、バイオ医薬品および特殊医薬品におけるコールドチェーンの完全性への世界的な関心の高まり、新鮮な食料品の直送に対する消費者需要の高まり、そして持続可能な循環型経済に基づく包装モデルへの大きな転換などが挙げられます。さらに、新興国におけるeコマースの拡大、高性能真空断熱材の革新、そして長期的な運用コストと環境への影響を軽減するための再利用可能な配送システムの導入増加も、市場の成長を後押しすると予想されます。

断熱包装材料市場分析

断熱包装材市場分析では、業界が基本的な断熱対策から包括的なコールドチェーン管理へと移行する中で、高性能で多機能なソリューションへの移行が見られています。調達動向は、市場が食料品eコマース向けの大量使い捨てセクターと、医薬品物流向けの高価値の再利用システムに分かれつつあることを示しています。IoT対応センサーを断熱容器に統合することで、リアルタイムの温度追跡が利益率の高い生物学的輸送において明確な競争優位性をもたらすという戦略的機会が生まれています。また、市場拡大は、耐熱性と路上リサイクル性を両立させる材料科学のイノベーションにかかっていると分析されています。持続可能性認証、材料の循環性、受動冷却効率を強調したブランディングによって、競争上の差別化が際立っており、競争の激しい業界環境において、優良ベンダーはより高い価格設定を可能にしています。

断熱包装材料市場の概要

断熱包装材は、特殊な産業必需品から世界的な小売商品へと移行しつつあります。バルク食品輸送において、断熱包装材は高級化粧品やパーソナライズ医薬品といった付加価値の高い分野へと拡大しています。大手包装コングロマリットとニッチな熱工学企業はともに、先進的なポリマーや繊維ベースの複合材料を活用し、ネットゼロ目標の達成に取り組んでいます。北米とアジア太平洋地域では、健康志向が高くハイテクに精通した消費者が、農場から食卓までの鮮度と、温度管理が重要なヘルスケアへの即時アクセスを求めており、これが断熱包装がラストマイル配送エコシステムの重要な構成要素として普及する一因となっています。欧州は依然として持続可能な規制のリーダーですが、特に中国とインドにおけるコールドチェーンインフラの急速な成長により、アジア太平洋地域が市場規模を牽引する主要な原動力となっています。

例えば米国では、市場は主に医薬品セクターの拡大と成熟したeコマース環境によって牽引されています。州レベルの厳格な環境規制と消費者の循環型社会への需要の高まりに対応するため、スマートモニタリング技術の統合と、使い捨てプラスチックから路上リサイクル可能な繊維ベースの素材への移行に重点が置かれています。

要件に合わせてレポートをカスタマイズ

無料カスタマイズ断熱包装材料市場:戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

断熱包装材料市場の推進要因と機会

市場の推進要因:

- 医薬品コールドチェーン要件の急増: mRNA ワクチンと生物製剤の世界的な展開には、長期間にわたって厳しい温度範囲を維持できる高精度の断熱材が必要です。

- 電子食料品と食事キットの急速な拡大: 消費者行動がオンラインでの食料品ショッピングへと移行したことにより、軽量でコスト効率に優れた保温ライナーと段ボール梱包材に対する需要が急増しました。

- 厳格な規制基準: 食品安全 (HACCP) および医薬品流通 (GDP) に関する世界基準がますます厳格化しているため、標準以下のパッケージを段階的に廃止し、検証済みの断熱材を導入する動きが進んでいます。

市場機会:

- バイオベースおよびリサイクル可能な絶縁体の開発: 生産者にとって、従来の EPS (発泡スチロール) を生分解性の木質繊維複合材またはキノコベースの包装に置き換えて、環境に配慮したブランドにアピールする大きなチャンスがあります。

- 再利用可能なサービス モデルの成長: 再利用可能なコンテナの回収と消毒に関する戦略的パートナーシップを形成することで、物流プロバイダーに高利益率のサービス チャンスが生まれます。

- 新興アジア太平洋産業ハブへの拡大: 東南アジアの急成長中の医薬品および化粧品製造部門に参入することで、コールドチェーン インフラの近代化が現在進められている高成長市場へのアクセスが容易になります。

断熱包装材料市場レポート:セグメンテーション分析

断熱包装材市場シェアは、様々なセグメントにわたって分析され、その構造、成長の可能性、そして新たなトレンドをより明確に理解するのに役立ちます。以下は、ほとんどの業界レポートで使用されている標準的なセグメンテーション手法です。

素材の種類別:

- プラスチック:EPS、ポリウレタン(PUR)、ポリエチレンなどの材料を使用する主要な材料セグメントです。優れた断熱性と耐湿性から好まれています。

- 木材: 天然の断熱性と構造的耐久性が求められる特殊な重量物輸送や高級な職人による食品輸送に主に使用されます。

- 段ボール: 電子商取引分野で急成長している分野で、断熱ライナーと組み合わせることで、プラスチックフォームに代わる路上リサイクル可能な代替品として利用されることが増えています。

タイプ別:

- 使い捨て: 初期費用が低いため、特に電子商取引の食料品や個人消費者への配達部門で、引き続き最大の販売量を生み出しています。

- 再利用可能: 長期的なコスト効率と持続可能性のプロファイルにより、製薬業界やクローズドループ B2B 物流で好まれる高成長セグメントです。

エンドユーザー別:

- 医薬品: ワクチン、血液サンプル、生物製剤の輸送に不可欠な、最も急速に成長しているエンドユーザーセグメント。

- 食品および飲料: 生鮮食品の世界的な取引とクイックコマース食料品アプリの増加により、数量ベースで最大のアプリケーションセグメントとなっています。

- 化粧品: 成分の劣化を防ぐために安定した環境を必要とする高級オーガニックスキンケア製品や温度に敏感な美容製品の新たなニッチ市場。

- 工業:温度に敏感な特殊化学物質や電子部品の輸送が含まれます。

地理別:

- 北米

- ヨーロッパ

- アジア太平洋

- 南米と中央アメリカ

- 中東・アフリカ

断熱包装材料市場の地域別分析

断熱包装材料市場に影響を与える地域動向は、主要な地域全体で分析されています。

断熱包装材料市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2025年の市場規模 | 144億4000万米ドル |

| 2034年までの市場規模 | 224億米ドル |

| 世界のCAGR(2026年~2034年) | 5.0% |

| 履歴データ | 2021-2024 |

| 予測期間 | 2026~2034年 |

| 対象セグメント |

素材の種類別

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

断熱包装材料市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

断熱包装材市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認知度の高まりといった要因によるエンドユーザーの需要増加に牽引され、急速に成長しています。需要の増加に伴い、企業は製品ラインナップの拡充、消費者ニーズへの対応のための革新、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

断熱包装材料市場シェア分析(地域別)

アジア太平洋地域は今後数年間で最も急速に成長すると予想されています。南米、中米、中東、アフリカの新興市場にも、高級乳製品メーカーや乳児用調合乳メーカーにとって、事業拡大のための未開拓の機会が数多く存在します。

断熱包装材市場は、従来のバルク断熱材から、高付加価値でテクノロジーを活用した断熱材へと大きく変貌を遂げつつあります。この成長を牽引しているのは、eコマースにおける食料品需要の急増、世界的なバイオ医薬品への転換、そしてプラスチック発泡材に代わる持続可能な繊維ベースの代替品の普及です。以下は、地域別の市場シェアとトレンドの概要です。

北米

- 市場シェア: 成熟したバイオテクノロジー業界と高い電子商取引の浸透により、世界最大の収益シェアを維持しています。

-

主な推進要因:

- 温度に敏感な生物製剤および細胞・遺伝子治療に対する高い需要。

- IoT 接続による温度モニタリングを備えたスマート パッケージングの迅速な導入。

- 温度管理された医療品の出荷に対する厳格な FDA 要件。

- トレンド: 州レベルの厳しい環境規制を満たすために、路上でリサイクル可能な繊維ベースの素材を統合します。

ヨーロッパ

- 市場シェア: 持続可能で循環型経済のパッケージングに重点を置いた規制が根付いており、世界的に大きなシェアを占めています。

-

主な推進要因:

- 厳格なEUの環境規制により、使い捨てプラスチックの代替が推進されている。

- ワイン、チーズ、医薬品などの高価値輸出品向けの管理された物流を必要とする新興市場に近接しています。

- 包装におけるグリーンディールの取り組みに対する政府の強力な支援。

- トレンド: 食品サプライチェーンにおける廃棄物を最小限に抑えるために、バイオベースのエアロゲルと再利用可能なマクロ包装材への戦略的転換。

アジア太平洋

- 市場シェア: 最も急速に成長している地域であり、中国、インド、日本が成長の主な原動力となっています。

-

主な推進要因:

- 中国やインドの人口密集地では、利便性を重視した加工食品や冷凍食品が求められています。

- 政府支援による冷蔵倉庫インフラと医薬品製造拠点の拡張。

- インドは肉、乳製品、果物の主要輸出国であるため、広範囲にわたるコールドチェーン物流が必要です。

- トレンド: ラストマイルの温度管理が重要な食料品の配達では、真空断熱パネル (VIP) と電子商取引プラットフォームへの依存度が高まっています。

南米と中央アメリカ

- 市場シェア: ブラジルとアルゼンチンの工業食品および職人食品の輸出部門が成長する新興市場。

-

主な推進要因:

- 食品の安全性と賞味期限の延長に対する意識が高まります。

- 小規模サプライチェーンを商用グレードのコールドチェーンに近代化します。

- トレンド: 繊細な工業製品の輸出を保護するための柔軟な断熱ブランケットと金属化バリアフィルムの増加。

中東およびアフリカ

- 市場シェア: 極端な周囲温度に対抗する高性能断熱材に重点を置いた発展途上の市場。

-

主な推進要因:

- 乾燥気候における常温保存可能な冷蔵食品物流の需要が高まっています。

- 地元の食糧安全保障を改善するためのスマート農業への戦略的投資。

- トレンド: 高効率の硬質容器と高栄養価の医薬品流通システムの導入。

高い市場密度と競争

Sealed Air Corporation、Sonoco Products Company、Amcor PLCといった確立されたリーダーの存在により、競争は激化しています。Cold Chain TechnologiesやPeli BioThermalといった地域専門企業に加え、RanpakやSofrigamといったイノベーターも、多様な市場環境に貢献しています。

この競争環境により、ベンダーは次のような差別化を迫られています。

- IoT センサーと QR コードを組み込んで温度変化をリアルタイムで追跡し、医薬品向けの検証済みのコールド チェーンを提供します。

- 標準的なフォームからリサイクル可能な繊維、バイオベースのエアロゲル、r-PET に移行することで、企業は持続可能性プレミアムを請求できるようになります。

- 真空パネルと相変化材料 (PCM) を組み合わせて温度安定性を最大 96 時間以上に延長する輸送容器を設計します。

- 倫理的でクリーンなラベル基準を確保するために、原材料(バイオフォームなど)の生産と物流サービスを管理します。

機会と戦略的動き

- 主要プラットフォームと連携し、急増する食料品や食事キットの配達分野向けに、大容量で環境に優しいサーマルシッパーを提供します。

- 環境に配慮した企業にアピールし、出荷コストを削減するために、高級医薬品の出荷業者向けに回収および再利用プログラムを実施します。

断熱包装材料市場で事業を展開している主要企業:

- 密閉空気

- FEURERグループGmbH

- サンセル

- ウールパッケージングカンパニーリミテッド

- クールパック

- カスケーズ株式会社

- ICEEコンテナーズ株式会社

- テンパーパック

- アイサーテック

免責事項:上記の企業は、特定の順序でランク付けされているわけではありません。

断熱包装材料市場のニュースと最近の動向

- 2024年8月、Sealed AirはBUBBLE WRAP®ブランドのロール状エンボス加工紙の発売を発表しました。輸送中の優れた保護を実現する、繊維ベースの新しい梱包ソリューションです。

- 2024年6月、フレキシブル包装と材料科学のリーダーであるProAmpacは、特許出願中のProActive Recyclable® FiberCoolカーブサイドリサイクル可能な断熱バッグの発売を誇りを持って発表しました。FiberCoolは、標準的なセルフオープニングサック(SOS)の先を行く、カーブサイドリサイクルの利便性と食品・食料品の配達市場における温度保持ソリューションを提供します。FiberCoolは、食品・食料品の配達市場におけるカーブサイドリサイクル可能なパッケージの新たな基準を確立します。

断熱包装材料市場レポートの対象範囲と成果物

断熱包装材料市場の規模と予測(2021〜2034年)レポートは、以下の分野をカバーする市場の詳細な分析を提供します。

- 断熱包装材料市場規模と予測は、対象範囲に含まれるすべての主要市場セグメントについて、世界、地域、国レベルで調査します。

- 断熱包装材料市場の動向、および推進要因、制約、主要な機会などの市場動向

- 詳細なPEST分析とSWOT分析

- 断熱包装材料市場分析では、主要な市場動向、世界および地域の枠組み、主要プレーヤー、規制、最近の市場動向を網羅しています。

- 市場集中、ヒートマップ分析、主要プレーヤー、断熱包装材料市場の最近の動向を網羅した業界の展望と競争分析。

- 詳細な企業プロフィール

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応