Rising Utilization of Nickel-Based Superalloys in Aircraft Engine Forging Processes Boosts Aircraft Engine Forging Market Growth

According to our latest market study on "Aircraft Engine Forging Market Size and Forecast (2021–2031), Global and Regional Share, Trend, and Growth Opportunity Analysis – by Forging Type, Aircraft Type, Material Type, and Application," the market was valued at US$ 3,787.15 million in 2024 and is anticipated to reach US$ 5,966.86 million by 2031; it is estimated to register a CAGR of 6.84% during 2025–2031. The report includes prospects in light of current aircraft engine forging market trends and driving factors propelling the market growth.

The aerospace sector is turning to nickel‑based superalloys for forging critical components in modern jet engines, driven by a demand for materials that withstand extreme thermal and mechanical stress. As engines push the limits of temperature and pressure—boosting fuel efficiency and reducing emissions—materials must deliver uncompromised performance. Nickel‑based superalloys, known for exceptional strength, oxidation resistance, and high-temperature creep stability, are essential in this context. In July 2025, Hindustan Aeronautics Limited (HAL) placed a ₹600 crore (US$75 million) order with Mishra Dhatu Nigam Limited (MIDHANI) to supply high-performance superalloys. The superalloys procured under this contract will support the production and maintenance of jet engines such as the Russian-origin AL31, which powers the frontline Su-30MKI fighter aircraft.

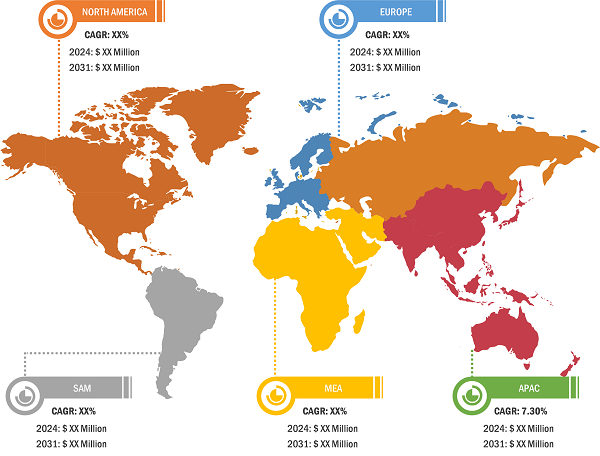

Aircraft Engine Forging Market Analysis – by Geography, 2024

Aircraft Engine Forging Market Forecast (2021 - 2031), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Forging Type (Closed Die Forging and Seamless Rolled Ring Forging), Aircraft Type (Commercial Aircraft, Military Aircraft, General Aviation), Material Type (Nickel Alloys, Titanium Alloys, Aluminum and Others), Application ( Rotor, Turbine Disc, Combustion Chamber Outer Case, Fan Case, and Others) and Geography

Aircraft Engine Forging Market Size & Trends by 2031

Download Free Sample

Source: The Insight Partners Analysis

Manufacturers are leveraging improvements in alloy composition and forging techniques, enabling the production of simpler parts with tighter tolerances, improved yield, and reduced waste. As engine pressures mount, these alloys retain structural strength, resisting mechanical creep even at elevated temperatures. This shift dovetails with industry-wide goals around sustainability and operational efficiency. Regulatory pressures to reduce carbon emissions incentivize OEMs to explore materials that support next-gen engine designs. Nickel-based superalloys address this need, facilitating higher operating temperatures without compromising safety or performance.

The rise in nickel‑based superalloy adoption—exemplified by innovations such as ATI 718Plus—signals a strategic move toward materials that combine high-temperature robustness, structural integrity, and cost efficiency. This trend will continue as aerospace manufacturers respond to evolving performance criteria and environmental directives, driving the future of aircraft engine forging.

The scope of the aircraft engine forging market report focuses on North America (the US, Canada, and Mexico), Europe (the UK, Germany, France, Italy, Russia, and the Rest of Europe), Asia Pacific (South Korea, China, India, Japan, Australia, and the Rest of Asia Pacific), Middle East and Africa (South Africa, Saudi Arabia, the UAE, and the Rest of Middle East and Africa), and South America (Brazil, Argentina, and the Rest of South America). Asia Pacific (APAC) registered a significant aircraft engine forging market share in 2024 and is expected to grow at a CAGR of 7.3% during the forecast period. APAC plays a crucial role in the global aircraft engine forging industry, driven by the region's expanding aerospace sector and rising commercial and military aircraft demand. China, India, Japan, and South Korea invest in aerospace manufacturing infrastructure, including advanced forging capabilities for producing high-performance engine components such as turbine discs, shafts, and compressor blades. China's state-backed aerospace programs and India's "Make in India" initiative spur local development and foreign collaborations, boosting domestic forging capacities. Japan and South Korea lead in high-precision forging technologies, supplying components for major engine manufacturers such as Rolls-Royce, GE Aviation, and Pratt & Whitney. The region benefits from a robust supply chain, lower labor costs, and government incentives that attract global OEMs and tier-1 suppliers. As aircraft orders surge to meet growing travel demand and fleet modernization, the Asia-Pacific aircraft engine forging market is witnessing sustained growth, technological advancement, and increased localization of critical component manufacturing.

Throughout 2024, industry engagements intensified. India's Safran–HAL joint venture began producing critical turbine parts for the LEAP engine, expanding Bengaluru and Hyderabad assembly plants. Godrej Aerospace and Azad Engineering advanced India's indigenous Kaveri‑derivative engine program: Godrej delivered early modules in April 2025, following initial manufacturing in 2023, with full deliveries by August 2025. South Korea's Hanwha Aerospace announced plans to develop a KF‑21 fighter engine by 2036, supported by a ₩5 trillion (~US$ 3.7 billion) investment and new R&D and factory infrastructure. In 2025, the momentum continues. Queensland, Australia, augmented its regional role by expanding its MRO infrastructure to include engine overhauls, aiming to serve the regional fleet, which is projected to grow by 4% annually. Additionally, India began receiving GE-404 engines for its LCA‑Mark 1A fighter program, with 12 units expected this financial year.

China's aircraft engine forging industry is evolving as part of the country's broader ambition to develop a self-reliant aerospace sector. Historically reliant on foreign technology and imports, the nation is enhancing its domestic forging capabilities to support the production of advanced aircraft engines used in military and civil aviation. The industry produces high-strength, precision-forged components such as turbine disks, compressor blades, and shafts, which are critical to engine performance and reliability. State-owned enterprises and research institutes lead efforts to advance forging techniques, including superalloy processing, precision machining, and quality control systems. In November 2024, the China Forging Association's 9th Aviation Materials conference in Wuxi emphasized the development of superalloys, titanium, and aluminum-lithium forging processes—a testament to China's efforts to close technology and talent gaps. In late April 2025, the Beijing Institute of Aeronautical Materials, affiliated with the Aero Engine Corporation of China (AECC), secured a patent for an innovative manufacturing process for alloy turbine blades. These blades are engineered to endure temperatures approximately 15% higher than existing models, representing a key technological advancement. This development is expected to drive improvements in engine thrust, fuel efficiency, and durability, positioning the company for enhanced competitive advantage in the aerospace sector.

All Metals & Forge Group, OTTO FUCHS KG, Pacific Forge Incorporated, Precision Castparts Corp., Safran SA, VSMPO-AVISMA Corp, Farinia Group, Doncasters Group, LISI GROUP, and Allegheny Technologies Inc are among the key players profiled in the aircraft engine forging market report. The report also studied and analyzed other players to get a holistic view of the market and its ecosystem. The aircraft engine forging market forecast can help stakeholders plan their growth strategies. The market study provides detailed market insights, which help the key players strategize their growth.

Contact Us

Phone: +1-646-491-9876

Email Id: sales@theinsightpartners.com