The left ventricular assist device market is expected to reach US$ 1,806.19 million by 2028 & registering at a CAGR of 5.1% from 2022 to 2028, according to a new research study conducted by The Insight Partners.

A significant increase in the prevalence of target diseases and a rise in the global geriatric population drive the market growth. However, a surge in product recalls and complications associated with left ventricular assist devices hamper the market growth.

According to the World Health Organization (WHO), cardiovascular disease (CVD) is one of the leading causes of death across the world. A few main contributors that are increasing the prevalence of CVD and stroke are family history, ethnicity, and age. The prevalence of CVD is also growing due to tobacco use; high blood pressure (hypertension); high cholesterol; exercise lack; unhealthy diet; excessive alcohol consumption; and diseases such as dyslipidemia, obesity, and diabetes. As per the American Heart Association, ~41.4% of adults in the US will have hypertension by 2030 (an 8.4% increase from 2012). The organization also estimates that the global cost burden of CVD will reach US$ 1,044 billion by 2030, which was US$ 863 billion in 2010. Moreover, according to the WHO estimates, deaths due to CVD across the world will rise from ~17.9 million in 2016 to 23.6 million by 2030. Emory Healthcare report states that the US recorded ~5 million cases of congestive failure in 2022, and ~550,000 new cases were diagnosed every year in the country. Also, the country reports ~287,000 deaths due to heart failure every year.

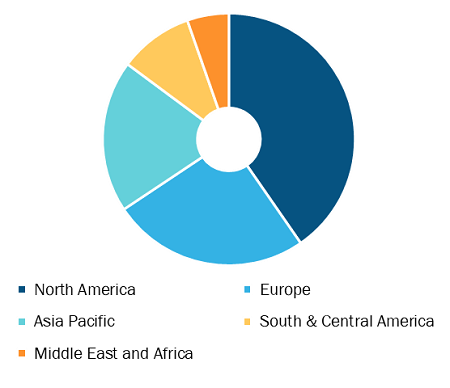

Left Ventricular Assist Device Market, by Region, 2021 (%)

Left Ventricular Assist Device Market Forecast to 2028 - Analysis By Type of Flow (Pulsatile and Non-Pulsatile), Design (Implantable Ventricular Assist Devices and Transcutaneous Ventricular Assist Devices), and Application (Bridge-to-Transplantation, Destination Therapy, Bridge-to-Recovery, and Bridge-to-Candidacy)

Left Ventricular Assist Device Market by Size, Share & Trend Analysis 2028

Download Free Sample

As per Temple Health, 70.9% of patients received heart transplants within a year, and the shortest waitlist average was 55.2% in the US in 2021. The increasing the heart transplant waiting list globally has propelled the use of left ventricular assist devices (LVADs) for end-stage heart failure patients to increase the ejection fraction and prevent organ failure. Therefore, the rising prevalence of CVD and heart failure and the long waiting list for a heart transplant propel the adoption of LVADs, which drives the growth of the left ventricular assist devices market.

Impact of COVID-19 Pandemic on global left ventricular assist device market

In 2020, the implementation of stringent lockdown regulations across several countries due to the effects of the COVID-19 pandemic disrupted the production and procedures of left ventricular assist devices. Also, many countries and cities were shut down amid the lockdown, causing the cancellation of treatments and doctor appointments. Patients suffering from critical issues need physical attention in the clinics. Cardiac issues are one of the most preventable public health challenges in all regions. Due to the rising intensity of the COVID-19 pandemic, the patients could not visit the clinics. Moreover, there was shortage of staff. Hence, the COVID-19 pandemic negatively impacted the global left ventricular assist device market.

During the COVID-19 outbreak, healthcare systems were overburdened, and the delivery of medical care to all patients became a challenge across the world. In addition, the medical device industry was facing the negative impact of COVID-19 pandemic. As the pandemic unfolded, medical device companies found difficulties managing their operations. This disrupted and restricted the companies’ ability to distribute products and resulted in the temporary closures of their facilities. However, hospitals gradually resumed elective procedures as the COVID-19 recovery rate increased. Hence, the demand for medical equipment, including left ventricular assist device, is expected to increase in the coming years.

ABIOMED Inc, Abbott Laboratories, Medtronic Plc, LivaNova Plc, Jarvik Heart Inc, Terumo Corp, Berlin Heart GmbH, BiVACOR Inc, Evaheart Inc, and BioVentrix Inc are among the left ventricular assist device market players.

The report segments the left ventricular assist device market as follows:

The left ventricular assist device market is segmented on the basis of type of flow, design, application, and geography. Based on type of flow, the market is segmented into non-pulsatile flow and pulsatile flow. Based on design, the market is bifurcated into transcutaneous ventricular assist devices and implantable ventricular assist devices. By application, the left ventricular assist device market is segmented into destination therapy, bridge-to-transplantation, bridge-to-candidacy, and bridge-to-recovery. Based on geography, the global left ventricular assist device market is segmented into North America (the US, Canada, and Mexico), Europe (France, Germany, the UK, Spain, Italy, and the Rest of Europe), Asia Pacific (China, India, Japan, Australia, South Korea, and the Rest of APAC), the Middle East & Africa (Saudi Arabia, the UAE, South Africa, and the Rest of the MEA), and South & Central America (Brazil, Argentina, and the Rest of South and Central America).

Contact Us

Phone: +1-646-491-9876

Email Id: sales@theinsightpartners.com