AI PC Market Demand, Share & Growth by 2034

AI PC Market Size and Forecasts (2021–2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage : By Product (Desktops & Notebooks, Workstations), Operating System (Windows, macOS, Chrome), Compute Type (GPU, NPU- <40 TOPs, 40-60 TOPS) Compute Architecture (X86, ARM)

- Status : Data Released

- Report Code : TIPRE00039715

- Category : Electronics and Semiconductor

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 10, 2026

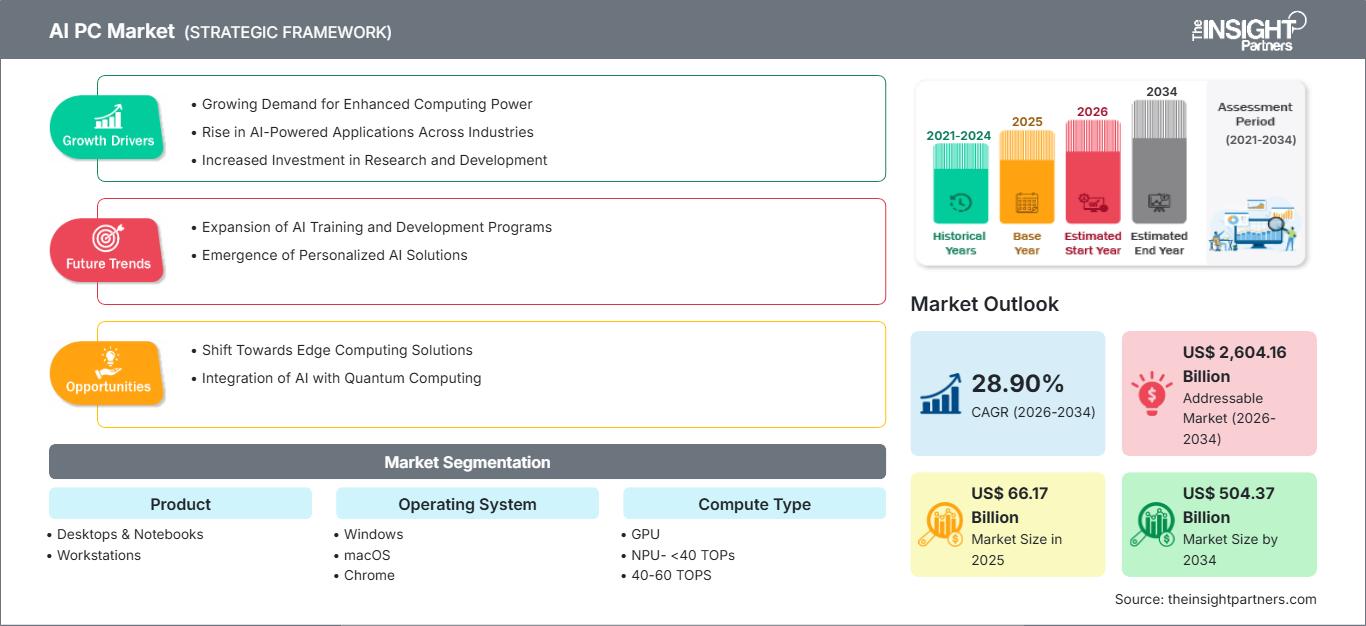

2025 Market Size

US$ 66.17 Bn

Base year value

2034 Forecast

US$ 504.37 Bn

Projected by 2034

CAGR 2026-2034

28.90 %

Growth rate

Addressable Market

US$ 2,604.16 Bn

(2026-2034)

The AI PC Market was valued at US$ 66.17 Billion in 2025 and is projected to reach US$ 504.37 Billion by 2034, expanding at a CAGR of 28.90% from 2026 to 2034. The market is being shaped by dedicated neural processing units, stronger graphics acceleration, and operating systems that move generative AI inference closer to the endpoint while improving responsiveness, privacy, and energy efficiency.

North America is expected to record a CAGR of 27.5%–29.5% during 2026–2034, supported by enterprise refresh cycles, Windows 11 migration, and early adoption of Copilot+ PC experiences. The region benefits from a dense ecosystem of silicon suppliers, operating-system owners, OEMs, and commercial channel partners that can convert AI PC Market report insights into scalable enterprise deployments.

AI PC Market Assessment and Insights

- North America: Held 36%–40% share in 2025 and is projected to grow at 27.5%–29.5% CAGR between 2026–2034, supported by enterprise fleets, Copilot+ adoption, and advanced software ecosystems.

- US: Accounted for 78%–84% of North America in 2025 and is projected to grow at 28.0%–30.0% CAGR between 2026–2034, led by commercial notebooks and developer systems.

- Europe: Held 20%–25% share in 2025 and is projected to grow at 26.0%–28.0% CAGR between 2026–2034, with Germany, the UK, and France leading AI-ready endpoint adoption.

- Asia Pacific: Held 28%–34% share in 2025 and is projected to grow at 30.0%–33.0% CAGR between 2026–2034, led by China, Japan, South Korea, and India.

- Largest Segment: Desktops & Notebooks held 82%–88% market share in 2025 and are projected to grow at 27.0%–29.0% CAGR between 2026–2034.

- High Growth Segment: Workstations held 12%–18% market share in 2025 and are projected to grow at 29.0%–31.5% CAGR between 2026–2034.

- Key companies analyzed in detail: Apple Inc.; Dell Technologies Inc.; HP Inc.; Lenovo Group Limited; ASUSTeK Computer Inc.; Intel Corporation; Advanced Micro Devices, Inc.; NVIDIA Corporation; Acer Incorporated; Microsoft Corporation.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The AI PC Market share is evolving from a device-refresh theme into a platform transition. Buyers now evaluate local inference capability, NPU TOPS, GPU acceleration, memory architecture, battery behavior, application compatibility, and manageability alongside conventional specifications. This shift is altering production dynamics as OEMs redesign premium notebooks, mainstream commercial laptops, desktops, and workstations around AI-ready silicon and tighter operating-system integration.

Forward demand will be strongest where enterprises can link AI PC Market size expansion to productivity, security, and lower cloud dependence. Emerging geographies will benefit as lower-cost AI notebooks arrive, while regulatory emphasis on data protection encourages local processing. Investments in software-defined endpoints, small language models, and AI-enabled collaboration tools will expand the AI PC Market scope beyond premium early adopters.

AI PC Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 66.17 Billion |

| Market Size by 2034 | US$ 504.37 Billion |

| Global CAGR (2026 - 2034) | 28.90% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

AI PC Market Analysis

The demand is shaped by hybrid work, generative AI, privacy-conscious inference, and a reduction in cloud reliance for AI applications. Businesses are investigating the potential of AI PCs to create meeting minutes, perform semantic searches, provide translation services, generate images, provide coding help, analyze security data, and automate workflows. The customers’ appeal lies in fast creativity tools, efficient battery assistants, and responsive personalization.

The value chain includes processor manufacturers, operating system holders, OEMs, memory makers, software developers, cloud companies, enterprise IT departments, and channel players. The companies that shape this value chain through highly integrated hardware, silicon roadmaps, and AI-enabled software experiences include Apple Inc., Dell Inc., HP Development Company L.P., Lenovo, ASUSTeK Computer Inc., Intel Corporation, Advanced Micro Devices Inc., NVIDIA Corporation, Acer Inc., and Microsoft.

Competition is intensifying across Windows, macOS, and Chrome platforms as vendors seek to define what an AI-native PC should deliver. Microsoft’s Copilot+ framework, Apple’s on-device intelligence strategy, Intel and AMD x86 roadmaps, NVIDIA’s GPU ecosystem, and ARM-based efficiency gains are creating multiple routes to differentiation. OEMs are positioning AI PCs by use case, price tier, and manageability. The AI PC Market forecast indicates continued innovation and competitive differentiation as vendors accelerate the integration of AI-ready hardware, software, and user experiences across consumer and enterprise computing platforms.

Trends in investments are in favor of NPUs greater than 40 TOPS, improved integration of GPUs, unified memory architectures, local optimization of models, and fleets of devices supporting AI functionality with security. The positioning of players is becoming more and more dependent on software partnerships, enabling developers, and evidence of running AI workloads locally with sufficient performance. Companies offering silicon, OS, and deployment capabilities will take the lead.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

AI PC Market: Strategic Insights

Regional Insights

North America AI PC Market

The North America AI PC market is anticipated to grow around 27.5%–29.5% owing to the readiness of enterprise software, high-quality notebooks, experience with cloud AI, as well as early implementation of Copilot+ and Apple Intelligence. Buyers are placing importance on inference security, productivity at the endpoints, and refresh programs in conjunction with the transition to Windows 11.

North America enjoys vendor density, channel strength, and procurement capabilities in financial services, technology, education, healthcare, and public sectors. Key players include Microsoft, Dell Inc., HP Development Company L.P., Apple Inc., Intel Corporation, Advanced Micro Devices Inc., and NVIDIA Corporation. Other key players, such as Lenovo and ASUS, participate actively in commercial and creator markets.

U.S. AI PC Market

The United States contributes approximately 78%–84% of the demand for AI PCs in North America and is projected to grow at around 28.0%–30.0%. The highest adoption rates are seen in enterprise notebooks, developer workstations, educational deployments, and premium consumer laptops that have the capability to enhance search, collaboration, security, programming, and creativity.

The company landscape is strong, including players such as Apple Inc., Dell Inc., HP Development Company L.P., Microsoft, Intel Corporation, Advanced Micro Devices Inc., and NVIDIA Corporation are impacting hardware design, silicon, and software enablement. Applications include copilots, meeting intelligence, AI-enabled design, endpoint security analytics, and offline productivity for regulated industries.

Europe AI PC Market

Europe accounts for an estimated 20%–25% global share and is expected to grow at around 26.0%–28.0%. Germany is the leading country, supported by industrial automation, engineering software, data-protection priorities, and enterprise interest in running AI workloads closer to endpoints. Sustainability and lifecycle cost also influence procurement.

The UK Artificial Intelligence Personal Computing market is driven by financial services, professional services, creative industries, and public sector modernization. Purchasers concentrate on security, productivity, collaboration, and easy management of commercial fleets of devices. Availability of good channels from suppliers like Lenovo, Dell Inc., HP Development Company L.P., Apple Inc., and Microsoft devices partners supports the adoption of such products.

Germany drives regional demand, and other countries like France, Italy, and Spain add to that via enterprise modernization, education modernization, and small business notebook replacement. In France, data sovereignty and productivity are key drivers; in Italy, there is demand for AI PCs in design and manufacturing clusters, while Spain gains from investments in a digital work environment.

APAC AI PC Market

APAC is the fastest-growing AI PC market, with an estimated CAGR of 30.0%–33.0% and a global share range of 28%–34%. China is the leading country, supported by domestic PC manufacturing scale, large enterprises, and education fleets, AI software localization, and industrial policy attention around semiconductors and digital productivity.

Japan and South Korea focus on top-end performance, reliability, and high-quality AI PCs used in electronics, automobiles, gaming, creation, and enterprise use. The demand is more towards ultra-thin notebooks, creator workstations, and premium workstations with excellent performance and energy efficiency. Korean parts supply and Japanese enterprise modernization help in adopting AI-enabled endpoint devices.

India and Australia contribute to the movement via IT services, education, start-ups, government digitization, and hybrid work models. Indian markets that tend to be price sensitive might adopt the AI notebook from Windows at first, whereas Australia focuses on commercial use and security use cases.

Middle East & Africa AI PC Market

The Middle East & Africa AI PC market is projected to grow at about 25.5%–28.5%, with the UAE as the leading country. Demand is linked to government digital transformation, smart-city programs, education modernization, cloud adoption, and enterprise investment in AI-enabled productivity across financial services, aviation, logistics, healthcare, and energy.

Saudi Arabia and the UAE are putting significant investment into AI infrastructures, data centers, digital governments, and technology ecosystems and this is leading to a need for a fleet of AI-ready endpoints. End-users in the energy sector appreciate the security of local AI computing, engineering workstations, and mobility productivity. Purchase is strongest wherever premium notebooks and workstations can help drive national transformation and automation.

South Africa and other countries in MEA are adopting slowly in banks, telecoms, education, public services, and international corporations. This will depend on affordability, channel availability, service availability, and connectivity. AI PCs are expected to get market share wherever vendors launch affordable PCs, and companies want productivity improvement without increasing cloud spending disproportionately.

Segmentation Analysis

Product

- Desktops & Notebooks: Desktops and notebooks dominate AI PC demand because enterprise refresh cycles, hybrid work, creator workloads, and consumer upgrades are concentrated around general-purpose systems.

- Workstations: Workstations serve developers, engineers, designers, and researchers requiring higher GPU capability, larger memory capacity, and reliable local AI performance for complex professional workloads.

Operating System

The operating system segment is projected to grow at 28.0%–30.0% CAGR during 2026–2034. Windows leads through broad OEM participation and enterprise manageability, macOS benefits from Apple silicon and integrated intelligence features, and Chrome supports cloud-first education and managed-device environments where lightweight AI assistance can scale quickly.

- Windows: Windows leads through Copilot+ PCs, broad OEM participation, enterprise manageability, x86 and ARM processor choice, and deep compatibility with commercial productivity applications.

- macOS: macOS gains traction through Apple silicon, unified memory, Apple Intelligence integration, strong creative adoption, and high-performance notebooks optimized for efficient on-device AI workflows.

- Chrome: Chrome-based AI PCs target education, cloud-first enterprises, and cost-sensitive users seeking simplified management, browser-native AI tools, and secure, lightweight endpoint deployment.

Compute Type

The compute type segment is projected to grow at 29.0%–31.0% CAGR during 2026–2034. GPU-enabled systems remain important for creators and developers, while NPUs below 40 TOPS support entry-level acceleration. The 40–60 TOPS class is becoming the mainstream benchmark for richer local AI features and operating-system eligibility.

- GPU: GPU-based AI PCs address graphics, model acceleration, creative software, gaming, and developer workloads where parallel compute remains essential for performance-intensive tasks.

- NPU- <40 TOPs: NPU models below 40 TOPS support entry-level AI acceleration, lightweight inference, battery-efficient assistants, and transitional devices where full Copilot+ class capability is limited.

- 40-60 TOPS: The 40-60 TOPS range is becoming the mainstream benchmark for AI PCs, enabling richer local features, stronger responsiveness, and broader operating-system support.

Compute Architecture

The compute architecture segment is projected to grow at 27.0%–29.5% CAGR during 2026–2034. X86 remains central to enterprise compatibility, device management, and Windows commercial deployments. At the same time, ARM gains relevance through power efficiency, battery life, and integrated AI acceleration in premium notebooks and cloud-connected productivity devices.

- X86: X86 architecture remains central to enterprise AI PCs due to software compatibility, manageability, broad OEM support, and strong roadmaps from Intel Corporation and Advanced Micro Devices Inc.

- ARM: ARM architecture is gaining relevance through power efficiency, long battery life, integrated AI acceleration, and growing adoption across premium notebooks and cloud-connected productivity devices.

Opportunity Snapshot

| Operating System | Revenue Contribution | Trend Tag | Adoption Stage |

| Windows | High | Copilot+ PCs | Scaling |

| macOS | Medium | Apple Intelligence | Scaling |

| Chrome | Low | Cloud AI | Emerging |

AI PC Market Growth Drivers and Impact Analysis

On-Device AI Becomes a Procurement Requirement

It is becoming increasingly common for enterprises to make having AI on-premises a tangible procurement criterion instead of an experimental option. AI PCs have the ability to perform chosen tasks of inference right on the device itself, thus offering lower latency, reduced exposure to sensitive prompts, and better responses when there are limitations to connectivity. This tangible market impact can be seen in terms of refreshing notebooks commercially, where IT professionals benchmark NPU performance and OS support, among others.

This driver shifts vendor communication from compute speed to workflow result. Microsoft-based fleets talk about the features of Copilot+, Windows, security, and cross-OEM selection, whereas Apple Inc. stresses close silicon, Mac OS, and intelligent privacy. Dell Inc., HP Development Company L.P., Lenovo, ASUSTeK Computer Inc., and Acer Inc. need to convert AI requirements into procurement value in terms of lower cloud computing burden, employee productivity improvement, and longer useful life of the devices.

NPU Performance Reshapes PC Platform Differentiation

The performance capabilities of NPU have transformed the PC market for AI, where accelerators will ensure that the repetitive tasks of AI can be performed effectively and without placing a burden on the CPU or draining laptop batteries due to constant use of the GPU. The systems ranging from 40-60 TOPS have become very significant as most of the advanced AI requires a minimum inference threshold locally. The market consequence of this situation is that the competition amongst silicon providers is based on balanced platform TOPS, memory bandwidth, software runtimes, thermals, and sustained performance.

Companies like Intel Corporation, Advanced Micro Devices Inc., Apple Inc., and ARM-based platforms have been making the acceleration capability of AI part of the identity of PCs. In addition to this, the significance of NVIDIA Corporation lies in the fact that the GPU-accelerated AI requires more parallel processing capabilities.

Enterprise Refresh Cycles Align with AI-Ready Workflows

Enterprise refresh cycles are a major driver because many organizations are replacing aging fleets while reassessing endpoint requirements for hybrid work, cybersecurity, collaboration, and automation. AI PCs create a stronger upgrade rationale by promising better local search, meeting intelligence, translation, image processing, coding assistance, and policy-controlled AI use. The real-world impact is a higher likelihood that commercial buyers will standardize on AI-ready configurations rather than purchase conventional laptops with shorter strategic relevance.

Procurement decisions will still be disciplined because IT teams need evidence of application readiness, security controls, and user productivity gains. Vendors that provide pilot programs, deployment guidance, lifecycle services, and clear differentiation between entry-level and Copilot+ class systems will be better positioned. This driver strengthens demand for Windows commercial notebooks, macOS professional systems, and workstation-class devices used by developers, engineers, designers, and analysts.

AI PC Market Future Trends

AI PCs Move Toward Agentic Personal Computing

AI PCs are expected to move beyond isolated features toward agentic personal computing, where local assistants understand files, meetings, applications, and user intent with stronger contextual awareness. This trend will require tighter coordination between operating systems, application developers, NPUs, GPUs, and security frameworks. Forward-looking demand will depend on whether users trust local agents to summarize, retrieve, draft, automate, and act across workflows without exposing sensitive information unnecessarily.

The implication is that AI PC value will increasingly come from software orchestration rather than hardware alone. Microsoft can extend Copilot+ experiences across Windows devices, Apple Inc. can leverage its integrated ecosystem, and Chrome-based systems can build cloud-connected AI management for education and enterprise users. OEMs must design devices that sustain AI workloads quietly, securely, and efficiently while keeping pricing accessible across mainstream and premium tiers.

Hybrid CPU-GPU-NPU Computing Becomes Standard

Hybrid CPU-GPU-NPU computing will become standard as AI applications mature beyond simple productivity features. Future systems will route workloads across the most efficient compute engine depending on latency, power, model size, and graphics intensity. This trend will make software optimization as important as hardware specification. Developers will need frameworks that select accelerators automatically, while enterprises will demand predictable performance, battery efficiency, and security policies across mixed fleets. The AI PC Market trends will therefore favor vendors that combine silicon, firmware, operating-system support, and application certification into a coherent endpoint platform.

Forward-looking competition will favor vendors that make hybrid compute invisible to users. Developers will need frameworks that route workloads efficiently, while enterprises will want predictable performance and manageable security policies. NVIDIA Corporation’s GPU ecosystem, Intel Corporation's and Advanced Micro Devices Inc. platform roadmaps, and Apple Inc.’s unified architecture will shape how quickly AI applications become broadly optimized for local execution across different PC classes.

AI PC Market Opportunities

Commercial Fleet Migration to AI-Ready Devices

Commercial fleet migration offers one of the clearest AI PC Market opportunities because organizations are already reassessing endpoint standards around hybrid work, cybersecurity, collaboration, and automation. Vendors can convert replacement demand by offering pilots that demonstrate local meeting summaries, semantic search, translation, image processing, policy-controlled AI access, and reduced dependence on cloud inference. The investment case is strongest where AI features can be tied to measurable employee productivity, regulated data handling, and longer device relevance.

Suppliers should package AI-ready devices with deployment guidance, lifecycle services, security configuration, and application-readiness assessment. Dell Technologies Inc., HP Inc., Lenovo Group Limited, Microsoft Corporation, Intel Corporation, Advanced Micro Devices, Inc., and NVIDIA Corporation can strengthen adoption by helping IT buyers distinguish entry AI PCs from Copilot+ class platforms. This opportunity also improves channel value because resellers can support migration planning, employee training, and fleet segmentation by role.

AI Workstations for Creators and Developers

AI workstations create a high-value opportunity because engineers, researchers, designers, media professionals, and developers need stronger local compute than mainstream notebooks can provide. Systems with advanced GPUs, larger memory pools, professional software certification, and stronger cooling can support local model testing, rendering, simulation, code generation, data analysis, and design automation. This opportunity is attractive because these buyers usually prioritize performance reliability and workflow continuity over the lowest upfront device price.

Investment strategies should focus on validated application stacks, GPU acceleration, upgradeable configurations, and partnerships with software providers. NVIDIA Corporation, Apple Inc., Dell Inc., HP Development Company L.P., Lenovo, and ASUSTeK Computer Inc. can differentiate by targeting vertical workflows such as media production, architecture, engineering, product design, AI development, and scientific computing. The opportunity expands as organizations seek local AI capability for sensitive intellectual property and faster iteration cycles.

Recent Developments

- May 2026: NVIDIA unveiled NVIDIA RTX Spark™, a new superchip that reinvents Windows PCs for the era of personal AI agents — offering a new class of computer that moves from tool to teammate. Designed for AI, creating, and gaming, RTX Spark brings together 30 years of NVIDIA innovation — including NVIDIA CUDA®, NVIDIA RTX™, DLSS, FP4, NVIDIA TensorRT™, NVIDIA OptiX™, Reflex, and G-SYNC® — to slim Windows laptops with all-day battery life and small, ultra-efficient desktop PCs.

- March 2025: Microsoft Corporation — Expanded Copilot+ PC experiences across AMD Ryzen AI 300 series, Intel Core Ultra 200V, and Snapdragon X Series devices, adding Live Captions, Cocreator, Restyle Image, and Image Creator availability across a broader Windows AI PC ecosystem.

- January 2025: Dell Technologies Leads AI PC Movement with New, Redesigned PC Portfolio. The company's unified branding across its PC portfolio simplifies the process of identifying and selecting the right PCs, accessories, and services. Powered by the latest processors from Intel®, AMD, and Qualcomm Technologies, Dell AI PCs deliver improved performance and advanced AI capabilities to support a wide range of computing needs. Additionally, Dell Pro AI Studio, the newest addition to the Dell AI Factory, provides a comprehensive toolkit that enables developers to build, optimize, and deploy AI applications on Dell AI PCs with greater speed and efficiency.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends