Asia Pacific Military Protected Vehicles Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Coverage: By Vehicle Type [Armored Personnel Carriers, Infantry Fighting Vehicles, Mine-Resistant Ambush Protected (MRAP) vehicles, Main Battle Tanks, Light Protected Vehicles, and Others], Mobility (Wheeled and Tracked), Propulsion Type (Conventional and Hybrid), Onboard Weapon System (Machine Guns, Missiles, and Others), Protection Level (Ballistic Protection, Mine or IED Protection, and Chemical and Biological Warfare Protection), and Operation (Non-Amphibious Vehicles and Amphibious vehicles)

- Status : Published

- Report Code : TIPRE00042522

- Category : Aerospace and Defense

- No. of Pages : 293

- Available Report Formats :

- Last update date : June 10, 2026

2024 Market Size

US$ 10,931.5 Mn

Base year value

2031 Forecast

US$ 15,836.6 Mn

Projected by 2031

CAGR 2025-2031

5.6 %

Growth rate

Addressable Market

US$ 95,721.41 Mn

(2025-2031)

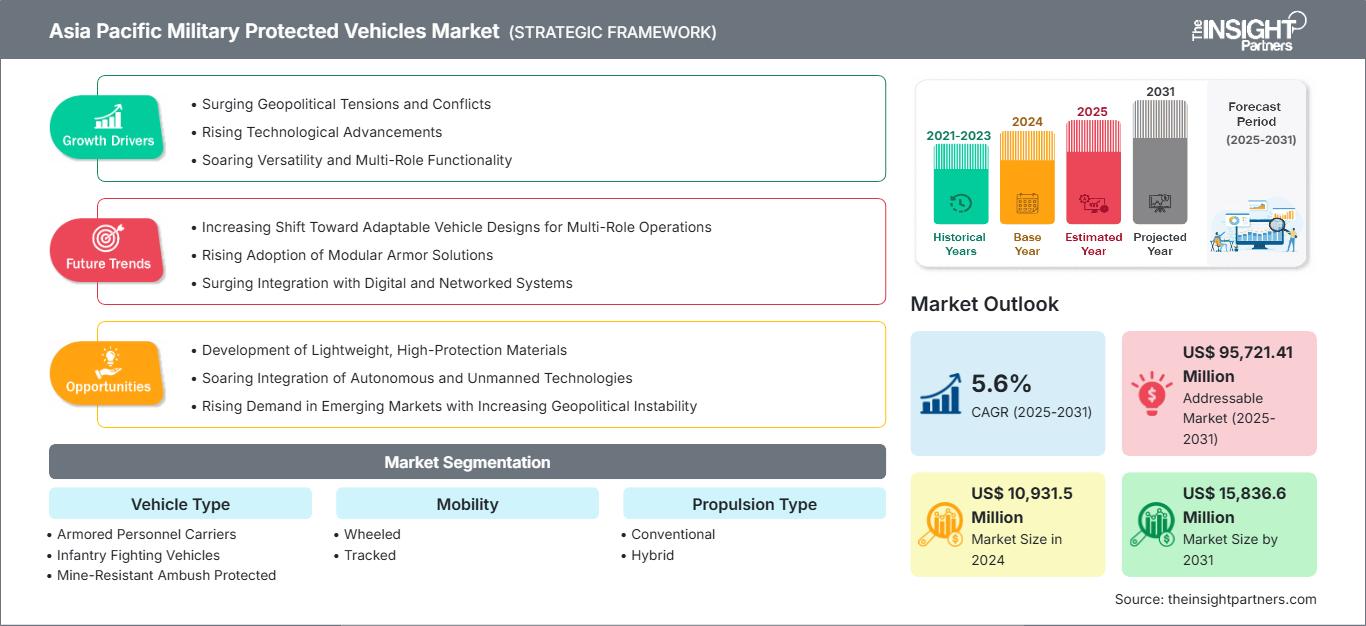

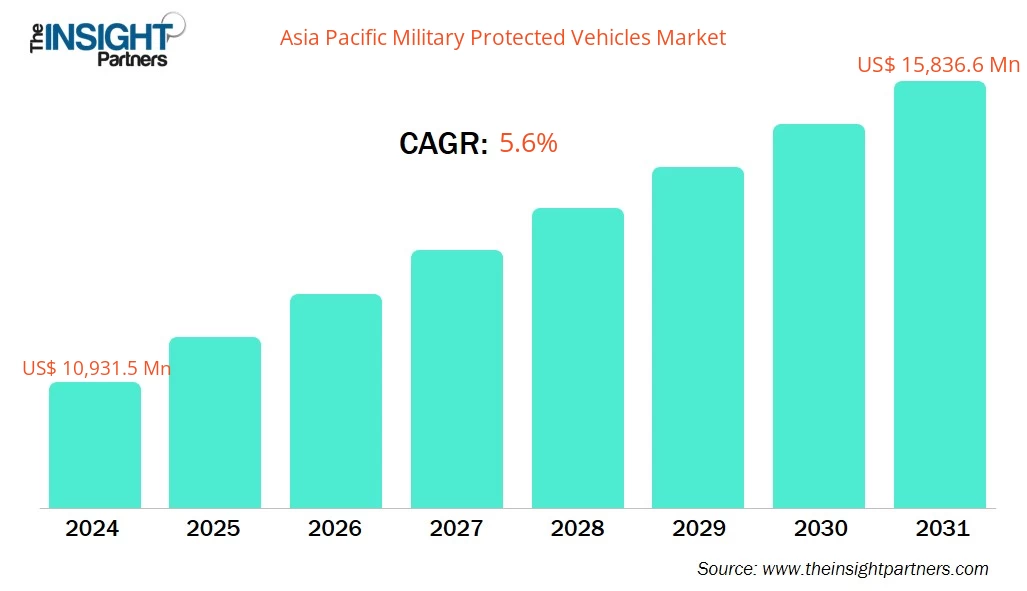

The Asia Pacific Military Protected Vehicles Market size is expected to reach US$ 15,836.6 Million by 2031 from US$ 10,931.5 Million in 2024. The market is estimated to record a CAGR of 5.6% from 2025 to 2031.

Executive Summary and Asia Pacific Military Protected Vehicles Market Analysis:

The region is characterized by increased military expenditures by major countries, including China, India, Japan, South Korea, and Australia. These nations are actively updating and expanding their military fleets with advanced protected vehicles capable of addressing evolving battlefield threats, reflecting a strategic focus on enhancing operational mobility, protection, and technological superiority.

The rising regional security challenges and cross-border conflicts are compelling nations to augment their armored capabilities. The surge in defense budgets facilitates substantial funding for the procurement and development of infantry fighting vehicles (IFVs), armoured personnel carriers (APCs), main battle tanks (MBTs), and light multi-role vehicles (LMVs). Technological advancements, such as the integration of artificial intelligence, improved materials sciences for armor protection, and Internet of Things (IoT)-enabled vehicle systems, increase the operational effectiveness and survivability of these vehicles in extreme battle environments.

Local defense manufacturing capabilities and government initiatives bolster self-reliance in defense production. Presently, the Asia Pacific defense industry is witnessing collaborations and contracts that support the indigenous production of military-protected vehicles, which leads to stimulating innovations and reducing reliance on foreign suppliers.

Overall, the Asia Pacific market's growth trajectory is propelled by enhanced military expenditure, regional geopolitical tensions, technological upgrades, and government-driven defense production efforts, making it a central hub for the global military protected vehicles industry.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Asia Pacific Military Protected Vehicles Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Asia Pacific Military Protected Vehicles Market Segmentation Analysis:

- By Vehicle Type, the Asia Pacific Military Protected Vehicles Market is segmented into Armored Personnel Carriers, Infantry Fighting Vehicles, Mine-Resistant Ambush Protected (MRAP) vehicles, Main Battle Tanks, Light Protected Vehicles, and Others. The Infantry Fighting Vehicles segment dominated the market in 2024.

- By Mobility, the Asia Pacific Military Protected Vehicles Market is segmented into Wheeled and Tracked. The Wheeled segment dominated the market in 2024.

- By Propulsion Type, the Asia Pacific Military Protected Vehicles Market is segmented into Conventional and Hybrid. The Conventional segment dominated the market in 2024.

- By Onboard Weapon System, the Asia Pacific Military Protected Vehicles Market is segmented into Machine Guns, Missiles, and Others. The Machine Guns segment dominated the market in 2024.

- By Protection Level, the Asia Pacific Military Protected Vehicles Market is segmented into Ballistic Protection, Mine or IED Protection, and Chemical and Biological Warfare Protection. The Ballistic Protection segment dominated the market in 2024.

- By Operation, the Asia Pacific Military Protected Vehicles Market is segmented into Non-Amphibious Vehicles and Amphibious vehicles. The Non-Amphibious Vehicles segment dominated the market in 2024.

Asia Pacific Military Protected Vehicles Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 10,931.5 Million |

| Market Size by 2031 | US$ 15,836.6 Million |

| CAGR (2025 - 2031) | 5.6% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Vehicle Type

|

| Regions and Countries Covered |

Asia Pacific

|

| Market leaders and key company profiles |

|

Asia Pacific Military Protected Vehicles Market Players Density: Understanding Its Impact on Business Dynamics

The Asia Pacific Military Protected Vehicles Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Asia Pacific Military Protected Vehicles Market Outlook

Modern armed forces are increasingly striving to enhance mobility, efficiency, and adaptability on the battlefield. Traditional armor materials, while providing strong protection, add significant weight to vehicles, limiting their speed, range, and maneuverability. The development of advanced materials such as composite armors, nano-engineered metals, ceramics, and hybrid laminates offers a solution to this challenge by achieving high levels of ballistic and blast protection while reducing vehicle weight.

Lightweight protection technologies enable military vehicles to operate effectively across a broader range of terrains and missions, including reconnaissance, rapid deployment, and urban warfare. Likewise, enhanced mobility improves survivability and enables forces to react more quickly to changing combat conditions. Reduced vehicle weight translates to lower fuel consumption and maintenance costs, thereby improving operational efficiency and extending the vehicle's lifespan. The integration of lightweight, high-protection materials facilitates better payload management, allowing the addition of new communication and weapon systems without compromising performance or safety.

The shift toward lightweight yet robust protection technologies is opening a new window of opportunity for manufacturers and defense contractors. Defense companies worldwide, investing in research and development of next-generation armor systems, will gain a competitive edge as defense agencies prioritize agility and performance over sheer mass. Nations modernizing their defense fleets are expected to favor platforms incorporating these materials, creating demand across new production and upgrade programs. This trend encourages collaborations between the defense and materials science sectors, leading to technological convergence that accelerates innovation. The development of lightweight, high-protection materials is likely to create new opportunities for the market in the upcoming years.

Asia Pacific Military Protected Vehicles Market Country Insights

By country, the Asia Pacific Military Protected Vehicles Market is segmented into Australia, China, India, Japan, South Korea, Rest of APAC. The Rest of APAC held the largest share in 2024.

The military protected vehicle market in the rest of the Asia-Pacific (APAC) region, including countries such as Malaysia, Singapore, Thailand, and others, is witnessing gradual growth driven by modernization programs and domestic defense initiatives. Governments in the region are increasingly investing in locally developed or customized armored vehicles to enhance mobility, protection, and operational readiness, while reducing dependence on imports. Both public and private sector manufacturers are contributing to these modernization efforts, reflecting a strategic focus on indigenous production and technological upgrades.

Malaysia is set to launch one of its most ambitious land systems modernization programs with the phased induction of the locally developed HMAV 4×4 Tarantula armored vehicle into the Malaysian Armed Forces beginning in 2027. A total of 136 vehicles will be delivered under a five-year program, with the first batch of 60 vehicles expected between early and late 2027. In Singapore, the Army commissioned a new variant of the Hunter armored fighting vehicle in January 2025, specifically designed for battlefield engineering missions, highlighting the focus on versatile and specialized platforms in the region.

The rest of the APAC military protected vehicle market is characterized by steady growth, local production initiatives, and modernization programs. Countries in the region are increasingly adopting advanced, domestically produced vehicles to enhance operational capabilities and maintain strategic autonomy.

Asia Pacific Military Protected Vehicles Market Company Profiles

Some of the key players operating in the market include BAE Systems Plc, General Dynamics Corp, Lockheed Martin Corp, Mahindra & Mahindra Ltd, Singapore Technologies Engineering Ltd, Otokar Otomotiv ve Savunma Sanayi A.Ş., Oshkosh Corp, Iveco Group NV, Patria Group, Paramount Group, BMC Automotive Industry and Trade Inc, ND Defense LLC, NIMR Automotive, Nurol Makina, Inguar Defence, Tata Advanced Systems Limited, Lenco Industries, Inc, Roshel Inc.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

Asia Pacific Military Protected Vehicles Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends