Marine Engines Market Demand, Share & Growth by 2034

Coverage: By Power Range (Up to 1000 HP, 1001-5000 HP, 5001-10000 HP, 10001-20000 HP, Above 20000 HP); Vessel (Commercial Vessel, Offshore Support Vessel, Others); Fuel (Heavy Fuel Oil, Intermediate Fuel Oil, Marine Diesel Oil, Marine Gas Oil, Others); Engine (Propulsion Engine, Auxiliary Engine); Type (Two-Stroke, Four-Stroke) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00004338

- Category : Automotive and Transportation

- No. of Pages : 150

- Available Report Formats :

- Last update date : March 27, 2026

2025 Market Size

US$ 12.1 Bn

Base year value

2034 Forecast

US$ 14.5 Bn

Projected by 2034

CAGR 2026-2034

2.1 %

Growth rate

Addressable Market

US$ 121.00 Bn

(2026-2034)

The global marine engines market size is projected to reach US$ 14.5 billion by 2034 from US$ 12.1 billion in 2025. The market is anticipated to register a CAGR of 2.1% during the forecast period 2026–2034.

Key market dynamics include a heightening global focus on decarbonization through IMO Tier III compliance, rising investments in naval fleet modernization, and a significant shift toward dual-fuel propulsion systems. Additionally, the market is expected to benefit from the expansion of international maritime trade, growing demand for specialized offshore support vessels for wind farm installations, and the increasing adoption of digital engine monitoring to optimize fuel consumption.

Marine Engines Market Analysis

The marine engines market analysis shows a shift toward high-efficiency propulsion as shipowners prioritize fuel flexibility and emission reduction. The market is moving into traditional heavy-fuel sectors for long-haul shipping and high-growth alternative-fuel markets utilizing LNG and methanol. Strategic opportunities are emerging in the retrofit segment, where existing vessels require engine upgrades to meet stringent sulfur limits. The analysis also notes that market expansion depends on global shipbuilding capacity and the development of bunkering infrastructure for green fuels. Competitive differentiation now stands out depending on the ability to integrate hybrid-ready designs and remote diagnostic services, helping operators lower the total cost of ownership.

Marine Engines Market Overview

Marine engines have transitioned from isolated mechanical units into highly connected, data-generating assets that form the heart of Smart Shipping. The market emphasizes the convergence of autonomous navigation technologies with advanced propulsion, where engines are designed to interface seamlessly with AI-driven bridge systems. The market is seeing a rapid diversification in power architectures, notably the integration of energy storage systems (ESS) and battery-assisted buffers that allow engines to operate at a constant, optimal load, significantly cutting specific fuel consumption. While diesel remains the baseline for intercontinental transit, the rise of unmanned intelligent ships and specialized vessels for offshore renewable is creating a high-growth niche for modular, high-speed engines. This evolution is particularly evident in Asia-Pacific region, which continues to consolidate its position as the global hub for next-generation vessel assembly, while European innovators focus on pioneering zero-emission auxiliary power units for green port corridors.

The US market is a mature and highly regulated market, primarily driven by the expansion of coastal logistics and the renewal of domestic fishing and cargo fleets. Significant demand stems from naval modernization programs and the flourishing recreational boating industry, particularly in Florida and California. The industry is rapidly pivoting toward sustainable propulsion, including LNG-ready and hybrid-electric systems, to meet stringent national emission standards.

Market Assessment and Insights

- Global market for Marine Engines was valued at US$ 12.10 Billion in 2025

- Annual market size is expected to reach US$ 14.50 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 121.00 Billion

- Market is anticipated to register a CAGR of 2.1% during the forecast period

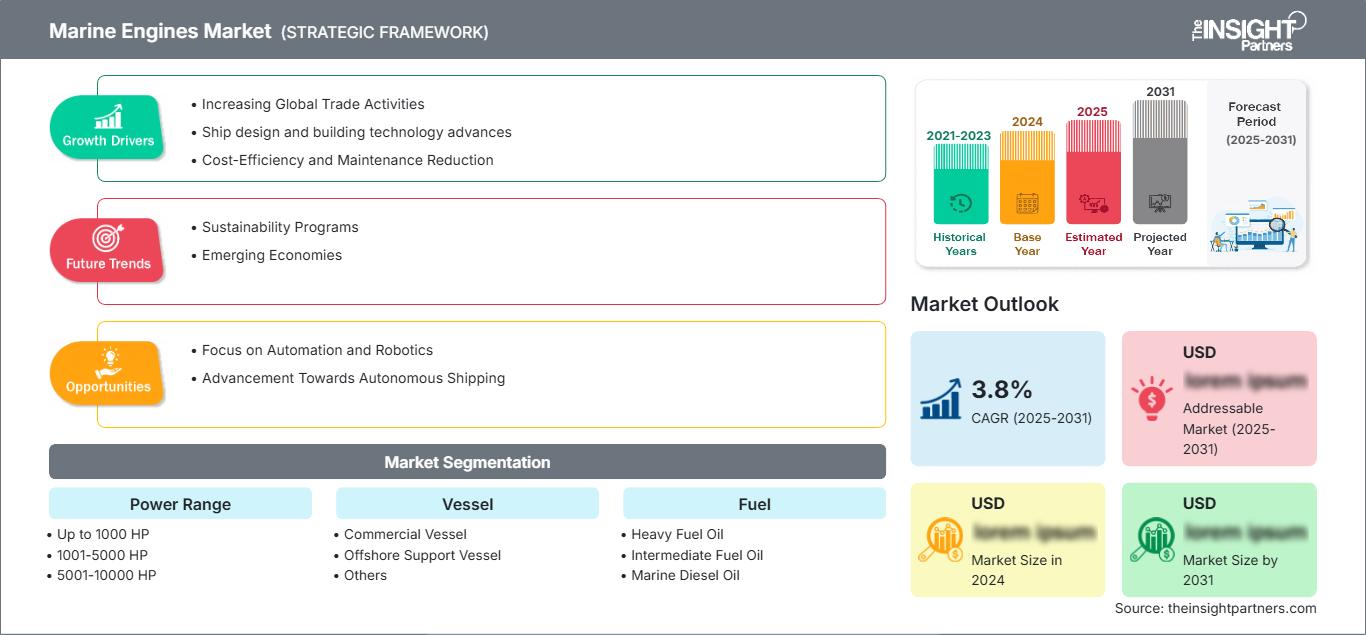

- The United States represents a key market, supported by Increasing Global Trade Activities, Ship design and building technology advances, Cost-Efficiency and Maintenance Reduction, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Focus on Automation and Robotics, Advancement Towards Autonomous Shipping are expected to influence market dynamics and addressable market

- Report profiles industry participants, including AB Volvo, Caterpillar, Cummins Inc, Deere and Company, Deutz AG, Hyundai Heavy Industries [ Engine and Machinery Division], Kongsberg Maritime, MAN SE, Mitsubishi Heavy Industries Marine Machinery and Equipment Co., Ltd., Wartsila, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Marine Engines Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Marine Engines Market Drivers and Opportunities

Market Drivers:

- Expansion of Seaborne Trade: The rise in global merchandise trade volumes sustains a consistent demand for newbuild commercial vessels and replacement engines.

- Stringent Environmental Mandates: Regulations like MARPOL Annex VI and the IMO 2030 targets drive the adoption of low-emission engines and scrubbers.

- Modernization of Naval and Defense Fleets: Increased geopolitical focus on maritime security is fueling government contracts for high-performance naval propulsion systems.

Market Opportunities:

- Transition to Future Fuels: Significant opportunities exist for manufacturers developing engines capable of running on green ammonia or hydrogen.

- Offshore Renewable Energy Support: The growth of offshore wind farms creates a specialized market for engines in service operation vessels and cable layers.

- Digital and Smart Engine Solutions: Integrating AI-driven predictive maintenance allows OEMs to offer high-value service contracts and improve engine uptime.

Marine Engines Market Report Segmentation Analysis

The Marine Engines Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Power Range:

- Up to 1000 HP: Primarily serves the recreational boating, small fishing vessels, and light harbor craft segments.

- 1001–5000 HP: A high-volume segment used in tugs, ferries, and various offshore support vessels.

- 5001–10000 HP: Widely adopted for medium-sized cargo ships and large offshore construction vessels.

- 10001–20000 HP: Essential for regional tankers and bulk carriers requiring steady propulsion.

- Above 20000 HP: The dominant segment by value for ultra-large container ships and tankers operating on international routes.

By Vessel:

- Commercial Vessel: The largest segment, driven by the global demand for container ships, bulkers, and oil tankers.

- Offshore Support Vessel: A vital segment for the oil, gas, and renewable energy, focusing on high maneuverability and reliability.

- Others: Includes navy vessels, cruise ships, and luxury yachts where noise reduction and high power density are prioritized.

By Fuel:

- Heavy Fuel Oil: Traditional dominant fuel, now often used in conjunction with scrubbers to meet emission standards.

- Intermediate Fuel Oil: Provides a balance of cost and performance for medium-speed engines.

- Marine Diesel Oil: Preferred for its reliability and thermal stability in medium and high-speed engines.

- Marine Gas Oil: Rising in popularity due to its low sulfur content and compliance with emission control areas.

- Others: Includes emerging fuels like LNG, Methanol, and Biofuels which are the fastest-growing niche.

By Engine:

- Propulsion Engine: The primary revenue driver, responsible for moving the vessel and accounting for the bulk of engine costs.

- Auxiliary Engine: Critical for providing onboard electricity, heating, and powering cargo-handling equipment.

By Type:

- Two-Stroke: Predominantly used for large-scale propulsion due to high thermal efficiency and low-speed direct drive.

- Four-Stroke: Favored for auxiliary power and smaller vessel propulsion due to its compactness and versatility.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Marine Engines Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 12.1 Billion |

| Market Size by 2034 | US$ 14.5 Billion |

| Global CAGR (2026 - 2034) | 2.1% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Power Range

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Marine Engines Market Players Density: Understanding Its Impact on Business Dynamics

The Marine Engines Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Marine Engines Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years, primarily due to the concentration of major global shipyards in China, South Korea, and Japan. Emerging markets in South & Central America, the Middle East, and Africa also present numerous untapped opportunities as regional governments invest in port expansion and offshore energy infrastructure.

The marine engines market is undergoing a significant transformation, moving from traditional heavy-fuel reliance to high-value, multi-fuel propulsion systems. Growth is driven by the expansion of global seaborne trade, a surge in decarbonization mandates, and the modernization of naval fleets. Below is a summary of market share and trends by region:

North America

- Market Share: A steady and technologically advanced segment, with the US market projected to exceed.

- Key Drivers:

- High demand for naval and military vessel engines under long-term defense procurement plans.

- Expansion of the Jones Act fleet and modernization of inland waterway towboats.

- Rising popularity of water-based recreational activities driving the outboard and small engine segments.

- Trends: Increased domestic focus on LNG bunkering infrastructure and the scaling of Tier III-compliant diesel engine solutions.

Europe

- Market Share: A major player in high-value, specialized engines.

- Key Drivers:

- Leadership in the cruise ship and luxury yacht manufacturing sectors.

- Early adoption of stringent green corridor policies and emission control areas.

- Robust R&D ecosystems for alternative fuels like hydrogen and ammonia.

- Trends: Strategic shift toward zero-emission auxiliary power for port zones and a rise in hybrid-electric retrofits for regional ferry fleets.

Asia-Pacific

- Market Share: Holds the largest global share and is the primary hub for marine production and consumption.

- Key Drivers:

- Dominance in the global shipbuilding industry, particularly for container ships and bulk carriers.

- Significant investments in naval modernization programs in countries like India and China.

- Rapid urbanization and industrialization in Southeast Asia are driving freight transport demand.

- Trends: A heavy focus on smart shipbuilding and the integration of dual-fuel platforms to comply with international environmental trajectories.

South and Central America

- Market Share: Emerging market with a growing focus on riverine and coastal logistics in countries like Brazil.

- Key Drivers:

- Rising mineral exports necessitate efficient bulk carrier propulsion.

- Modernization of aging fishing fleets to improve operational cost-efficiency.

- Strategic investments in offshore oil and gas production facilities.

- Trends: Growth in demand for reliable, shallow-draft compatible engines and simplified maintenance regimes for remote maritime operations.

Middle East and Africa

- Market Share: Developing market with significant growth potential linked to energy exports.

- Key Drivers:

- Massive commodity flows and port expansion projects in the GCC region.

- High demand for durable engines capable of operating under harsh, high-load conditions.

- Investments in offshore support vessels to service regional subsea energy assets.

- Trends: Implementation of port logistics, coupled with a focus on high-efficiency auxiliary engines for offshore production units.

High Market Density and Competition

Competition is intensifying as established leaders like MAN Energy Solutions, Wärtsilä, and Caterpillar face pressure from a rapidly evolving regulatory landscape. Regional specialists and shipbuilding giants like HD Hyundai Heavy Industries and Mitsubishi Heavy Industries also contribute to a diverse and technologically dense market landscape.

This competitive environment pushes vendors to differentiate through:

- Alternative Fuel Readiness: Positioning engines as future-proof by offering dual-fuel capabilities for LNG, methanol, and ammonia-ready designs to appeal to eco-conscious shipowners.

- Digital Ecosystems: Companies now offer more than just hardware; they provide digital twins, AI-driven performance monitoring, and predictive maintenance tools to reduce the total cost of ownership.

- Vertical Integration: Producers often manage the entire lifecycle, from design and shipyard integration to global aftermarket service networks, ensuring high asset uptime and ethical supply chain standards.

Opportunities and Strategic Moves

- Partner with Shipyards for Turnkey Solutions: Form strategic alliances with major Asian and European shipbuilders to integrate advanced propulsion systems during the initial construction phase.

- Invest in Retrofit and Repowering Services: Tap into the surging demand for emission-compliance upgrades by offering SCR, EGR, and dual-fuel conversion kits for the thousands of existing vessels needing to meet IMO 2030 targets.

- Expand Digital Aftermarket Portfolios: Use IoT and remote diagnostic data to transition from traditional maintenance to proactive, performance-guaranteed service contracts.

Major Companies operating in the Marine Engines Market are:

- AB Volvo

- Caterpillar

- Cummins Inc

- Deere and Company

- Deutz AG

- Hyundai Heavy Industries [ Engine and Machinery Division]

- Kongsberg Maritime

- MAN SE

- Mitsubishi Heavy Industries Marine Machinery and Equipment Co., Ltd.

- Wartsila

Disclaimer: The companies listed above are not ranked in any particular order.

Marine Engines Market News and Recent Developments

- In March 2025, Cummins Inc. announced DNV Approval in Principle (AIP) for its methanol-ready QSK60 IMO II and IMO III engines, available from 2000 - 2700 hp (1491 - 2013 kW). The AIP validates Cummins' retrofittable methanol dual-fuel solution for the global marine market, ensuring it meets the highest standards of safety and performance.

- In January 2025, Deere & Company announced the unveiling of new engines, the JD14 and JD18 marine engines. With the addition of these engines, John Deere will be able to offer marine customers heavier-duty cycles and a more comprehensive power range, from 298 up to 599 kW

Marine Engines Market Report Coverage and Deliverables

The Marine Engines Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Marine Engines Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Marine Engines Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Marine Engines Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Marine Engines Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends