Middle East & Africa Military Vehicle Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Middle East & Africa Military Vehicle Market Size and Forecast (2021 - 2031), Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Tanks, Military Trucks, Amphibious Military Vehicles, Armored Vehicles, Reconnaissance Vehicles, Special Purpose Vehicles, and Other Types), Application (Ground Support Vehicles, Tactical Warfare, ISR, Military Transportation, and Other Applications), By Technology (Autonomous Vehicles and Manual Driven Vehicles)

Historic Data: 2021-2023 | Base Year: 2024 | Forecast Period: 2025-2031- Status : Published

- Report Code : TIPRE00041762

- Category : Aerospace and Defense

- No. of Pages : 187

- Available Report Formats :

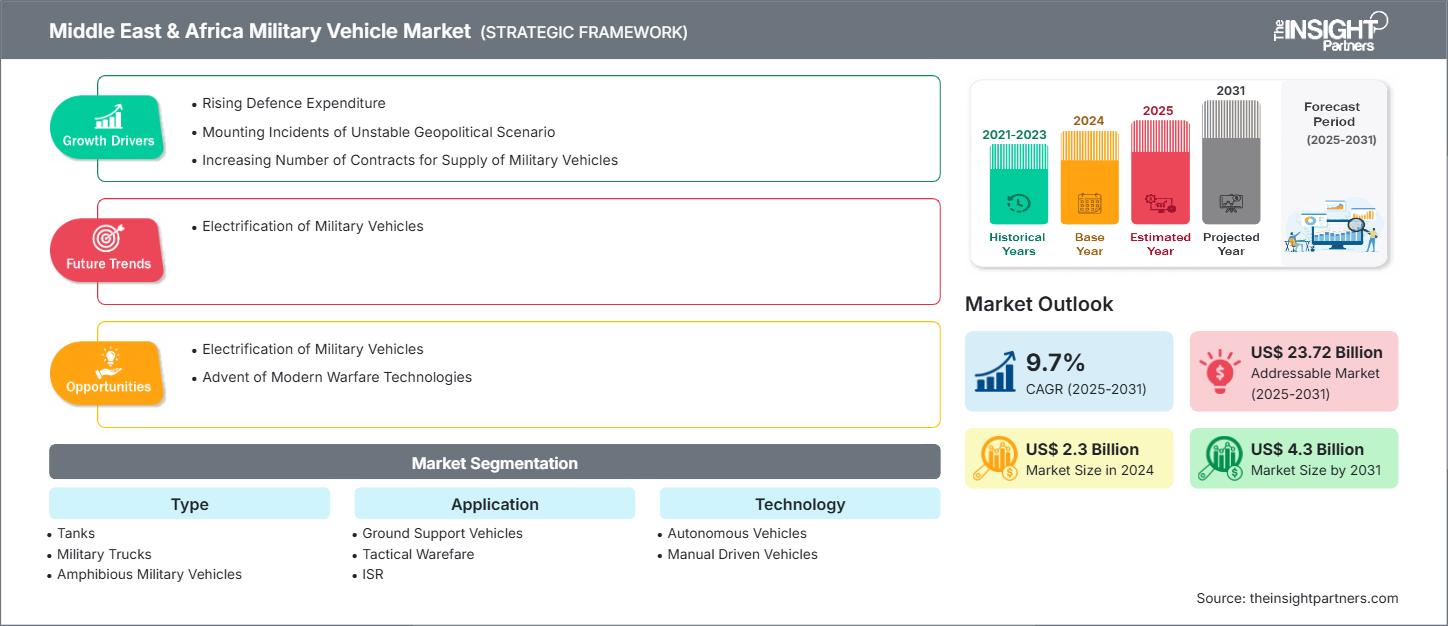

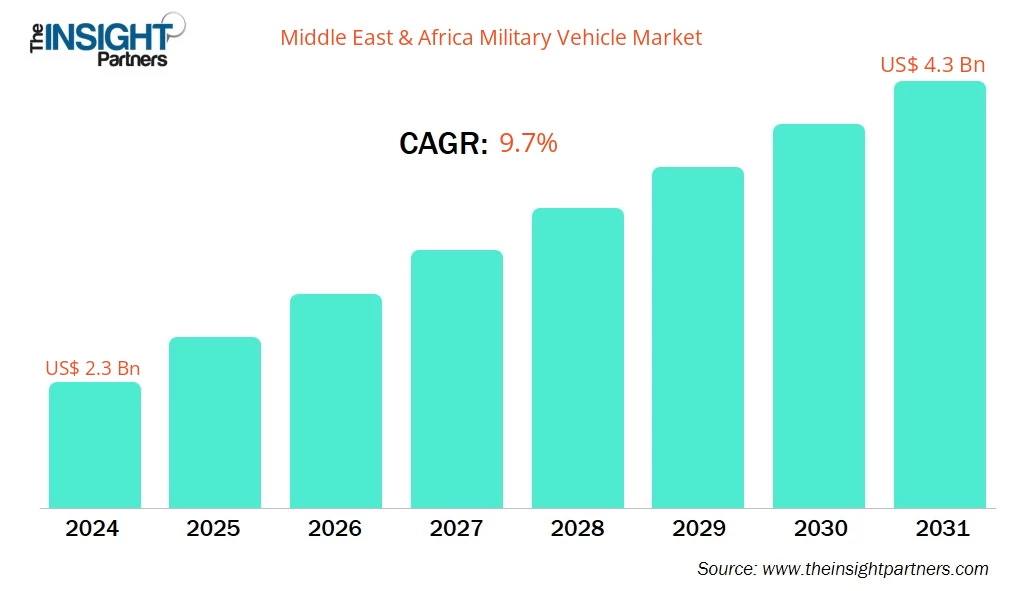

The Middle East & Africa Military Vehicle Market size is expected to reach US$ 4.3 Billion by 2031 from US$ 2.3 Billion in 2024. The market is estimated to record a CAGR of 9.7% from 2025 to 2031.

Executive Summary and Middle East & Africa Military Vehicle Market Analysis:

The UAE, Saudi Arabia, Turkey, and South Africa are a few of the prominent countries in the military vehicle market across the Middle East & Africa. In 2021, the military expenditure was US$ 223.0 billion, which increased to US$ 224 billion in 2022. In 2023, the Middle East & Africa's military expenditure was US$ 248.9 billion. In 2023, Saudi Arabia dominated the market in the region in terms of military expenditure, followed by the UAE and South Africa. A prominent share of military expenditure is dedicated to the requirement for advanced multi-purpose vehicles, equipment, devices, aircraft, ships, and armored vehicles in modern war, which is anticipated to boost the demand for military vehicles during the forecast period. In 2024, the South African National Defence Force (SANDF) obtained half a dozen SVI MAX 3 armored vehicles along with surveillance equipment to help combat border violations during Operation Corona deployments. In 2024, Paramount, the leading global aerospace and defence technology company, today announced a series of new additions to its battle-proven next-generation 6andtimes;6 Infantry Combat Vehicle (ICV), the Mbombe 6.. In 2024, the Kenyan government obtained a series of Springbuck armored personnel carriers from DCD Protected Mobility. The growing number of military vehicle orders is positively impacting the military vehicle market in the Middle East & Africa.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONMiddle East & Africa Military Vehicle Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Middle East & Africa Military Vehicle Market Segmentation Analysis:

- By Type, the Middle East & Africa Military Vehicle Market is segmented into Tanks, Military Trucks, Amphibious Military Vehicles, Armored Vehicles, Reconnaissance Vehicles, Special Purpose Vehicles, and Others. Armored Vehicles held the largest share of the market in 2024.

- By Application, the Middle East & Africa Military Vehicle Market is segmented into Ground Support Vehicles, Tactical Warfare, ISR, Military Transportation, and Others. Military Transportation held the largest share of the market in 2024.

- By Technology, the Middle East & Africa Military Vehicle Market is segmented into Autonomous Vehicles and Manual Driven Vehicles. Manual Driven Vehicles held the largest share of the market in 2024.

Middle East & Africa Military Vehicle Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 2.3 Billion |

| Market Size by 2031 | US$ 4.3 Billion |

| CAGR (2025 - 2031) | 9.7% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

Middle East and Africa

|

| Market leaders and key company profiles |

|

Middle East & Africa Military Vehicle Market Players Density: Understanding Its Impact on Business Dynamics

The Middle East & Africa Military Vehicle Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Middle East & Africa Military Vehicle Market Outlook

Advanced military vehicles with progressive communication and surveillance systems accelerate the development of a comprehensive and accurate analysis, aiding more precise threat measurements and target engagements. Modern warfare scenarios emphasize heightened situational awareness, rapid data sharing, integrated defense systems, improved target engagement, electronic warfare capabilities, and compliance with evolving threats. Thus, the growing adoption of advanced military vehicles equipped with the latest warfare devices and equipment further drives the growth of military vehicles to meet modern battlefield requirements. For instance, in 2024, BAE Systems Australia unveiled an advanced uncrewed ground vehicle (UGV) that offers military commanders an additional tactical option while keeping soldiers safe. The Autonomous Tactical Light Armour System (ATLAS) Collaborative Combat Variant (CCV) is cost efficient, modular, 8x8 UGV, which has been designed and developed by leveraging BAE Systems' autonomous technology. In 2024, General Dynamics Mission Systems incorporated its electronic warfare kit into the Infantry Squad Vehicle. The electronic warfare kit is part of the Tactical Electronic Warfare System-Infantry Brigade Combat Team (TEWS-I), which was primarily a quick-reaction competence built by General Dynamics, presenting a smaller system proposed for infantry vehicles. It was a prototype activity to assist as a risk reduction and requirement guide for the Army's program of record, the Terrestrial Layer System-Brigade Combat Team (TLS-BCT). Further, Ashok Leyland has made its venture into the armored vehicles segment with the Mine Protected Vehicle (MPV). The vehicle presents high mobility and rigorous levels of protection. Its design extends the ability to survive a 14 kg TNT blast under the hull and a 21 kg TNT blast under the wheel. In addition, the vehicle comes with side blast protection of 11 kg TNT and a lethal nitrate-driven emulsion blast of 50 kg. In 2024, General Dynamics UK introduced a new variant of its Foxhound Light Protected Patrol Vehicle (LPPV), the Foxhound General Multi-Role Vehicle (GMRV). With its advanced design and modular compliance, the GMRV indicates versatility on the battlefield. In 2023, Ashok Leyland won a US$ 97.5 million contract to supply 4x4 and 6x6 logistics support vehicles for towing light and medium guns and ammunition carriage. Thus, the advent of modern warfare technologies is expected to be one of the major growth-driving trends in the military vehicle market across the globe

Middle East & Africa Military Vehicle Market Country Insights

By country, the Middle East & Africa Military Vehicle Market is segmented into South Africa, Saudi Arabia, United Arab Emirates, Turkey, Rest of Middle East & Africa. The Rest of Middle East & Africa held the largest share in 2024.

Israel, Iran, and Egypt are a few of the major countries in the Rest of Middle East & Africa. In 2023, Israel was a notable country in defense spending, with expenditures amounting to US$ 27,498.5million. Kuwait followed with US$ 7,755.0 million, while Iran had US$ 10283.1million. In 2024, the Israeli Ministry of Defense approved several procurement and modernization projects for the Israel Defense Forces (IDF). These projects include replacing the Nirit (Saar 4.5) fleet and purchasing hundreds of Joint Light Tactical Vehicles (JLTVs) labeled locally as "Para." In addition, the Israeli army utilized remotely controlled explosive-laden armored personnel carriers to defuse improvised explosive devices and traps set by Palestinian resistance groups. In January 2025, the US State Department granted a request from Egypt to upgrade 555 of its General Dynamics Land Systems M1A1 Abrams main battle tanks into M1A1SA configuration under a contract that could be worth ~US$ 4.7 billion. Thus, the growing emphasis on upgrading and modernizing military vehicles and increasing instances of geopolitical disturbances are driving the demand for military vehicles.

Middle East & Africa Military Vehicle Market Company Profiles

Some of the key players operating in the market include BAE Systems Plc, General Dynamics Corp, Thales SA, Lockheed Martin Corp, Rheinmetall AG, Tata Motors Ltd, Ashok Leyland Ltd, Oshkosh Corp, KMW+NEXTER Defense Systems NV, NORINCOGROUP.com Inc., Patria Group, and Soframe.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

Middle East & Africa Military Vehicle Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Unlock Exclusive Report Discounts

Enquire Now

Get Free Sample For

Get Free Sample For