CSF Shunts Dominated Product Segment in Cerebrospinal Fluid Management Market

According to our new research study on "Cerebrospinal Fluid Management Market Forecast to 2030 – COVID-19 Impact and Global Analysis – by Product and End User," the market was valued at US$ 1,911.37 million in 2022 and is expected to reach US$ 2,892.54 million by 2030. It is estimated to register a CAGR of 5.3% during 2022–2030.

Cerebrospinal fluid safeguards the brain and spinal cord mechanically and immunologically. Management devices such as CSF shunts and CSF drainage systems are used to manage the flow of CSF in a controlled manner within the body away from ventricles, thus preventing the abnormal accumulation of CSF or hydrocephalus.

The cerebrospinal fluid management market, by product, is bifurcated into CSF shunts and CSF drainage systems. In 2022, the CSF shunts segment held a larger share of the market by product and is estimated to register a significant CAGR of 5.5% during the forecast period (2022-2030) due to growing product launches, increasing demand for advanced CSF shunts, and increasing incidences of hydrocephalus.

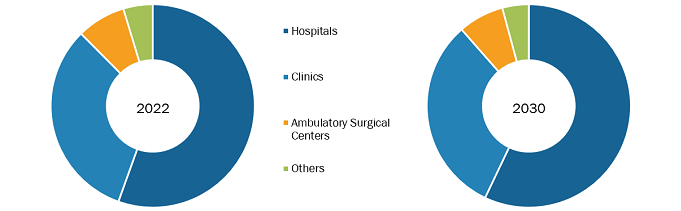

Cerebrospinal Fluid Management Market, by End User – 2022 and 2030

Cerebrospinal Fluid Management Market Strategies by 2030

Download Free SampleCerebrospinal Fluid Management Market Size and Forecasts (2020 - 2030), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Product (CSF Shunts and CSF Drainage Systems), End User (Hospitals, Clinics, Ambulatory Surgical Centers, and Others), and Geography

The growth of the cerebrospinal fluid management market is widely driven by the presence of well-established and budding players across the world. In May 2020, Aesculap Inc., along with The Christoph Miethke GmbH & Co. KG (MIETHKE), launched the M.blue valve for the treatment of hydrocephalus. M.blue, enabled with gravitational technology, is integrated with a fixed differential pressure unit in one valve, which unlocks a simple, position-dependent solution. Thus, product developments are likely to foster the market growth during the forecast period.

Ventriculoperitoneal shunts divert CSF from brain ventricles into the peritoneal cavity (space in the abdomen). The shunt is attached with a distal catheter tip resting in the peritoneal cavity near the loops of the intestine and bowel, but it is placed inside them. The CSF leaks shunted to the cavity are reabsorbed into the bloodstream and passed out of the body through urination. Companies in the cerebrospinal fluid management market are proactively developing newer technologies to enhance their products to offer better care and make them more user-friendly and suitable for in-home usage. Ventriculoatrial shunts divert CSF leaks from the brain ventricles into the right atrium of the heart. The distal catheter of this shunt is placed into a vein in the neck and is gently passed through the vein into the right atrium of the heart. Through this shunt, the CSF leaks are directly passed into the bloodstream, and the drain is excreted through urination. Ventriculoatrial shunts involve cardiac atrium, pleural space, and gallbladder, unlike ventriculoperitoneal shunts. The potential drawbacks of ventriculoatrial shunts include limited catheter placing options, which require further monitoring in children; higher risk of infections; the possibility of hampering cardiac conditions that can lead to hypertension; thromboembolic complications due to distal catheter; and the chances of causing nephritis. Thus, ventriculoatrial shunts are generally considered as the second option after the ventriculoperitoneal shunts. However, the failure rates of these shunts are not much different than ventriculoperitoneal shunts. Therefore, the cerebrospinal fluid management market for ventriculoatrial shunts is likely to grow steadily in the coming years.

Region Analysis – Cerebrospinal Fluid Management Market

Geographically, the cerebrospinal fluid management market is segmented into North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America. The North America cerebrospinal fluid management market is segmented into the US, Canada, and Mexico. The US held the largest share of the market in this region. The market in this region is expected to continue its dominance during the forecast period due to the increasing hydrocephalus, traumatic brain injury, and other neurological condition incidences, rapid technological innovations, and developing healthcare infrastructure.

According to the latest March 2023 update by the National Institutes of Health (NIH), 2 in every 1,000 babies are diagnosed with hydrocephalus in the US. The incidence of hydrocephalus in children in the country is as common as that of Down syndrome. The incidence rate of pediatric hydrocephalus is ~0.1–0.6% of live births. The incidence of hydrocephalus in children is a prime factor resulting in an elevated demand for cerebrospinal fluid management devices in the US. A research article “Management of Hydrocephalus in Children: Anatomic Imaging Appearances of CSF Shunts and Their Complications,” published in the American Journal of Roentgenology in October 2020, states hydrocephalus affects 1–2% of the US population. It results in nearly 70,000 hospital admissions, resulting in the insertion of 18,000–33,000 CSF shunts annually. Such high stats indicate that the country is witnessing a rising number of brain surgeries, which require the placement of cerebrospinal fluid (CSF) management devices. In addition, it is not known how many people develop hydrocephalus after birth. It is diagnosed as one progresses in age. Thus, the demand for CSF shunts is likely to grow and lead to the market growth.

CSF devices play a significant role in treating traumatic brain injuries (TBIs). ~1.5–2 million adults and children suffer a TBI each year. According to the Centers for Disease Control and Prevention (CDC), TBIs were the leading cause of death and disability in 2021; more than 69,000 TBI-related deaths were registered in 2021 in the US. However, a large percentage of people, especially those belonging to the age group of 15–19, survive a TBI. The sustainability of patients over TBIs indicates a large demand for CSF management of devices in the US.

Impact of COVID-19 Pandemic on Cerebrospinal Fluid Management Market

Before the COVID-19 pandemic, the cerebrospinal fluid management market growth experienced steady growth and was influenced by various factors that shaped its dynamics. Sudden onset of the pandemic led to the shutdown of neurological wards and clinics across numerous countries. At the same time, hospitals ran out of resources owing to a huge number of COVID-19 patients. Consequently, according to one study, many diagnostic and treatment procedures were canceled or postponed worldwide.

Medtronic plc; Integra LifeSciences Corporation; B. Braun Melsungen AG; Argi Group Health Services Ltd Sti; Sophysa SA; BeckerSmith Medical; Biometri, Spiegelberg GmbH & Co; Moller Medical GmbH, and Delta Surgical are among the leading companies operating in the cerebrospinal fluid management market.

The report segments the cerebrospinal fluid management market as follows:

The cerebrospinal fluid management market is segmented into product and end user. By product, the cerebrospinal fluid management market is bifurcated into CSF shunts and CSF drainage systems. CSF shunts are further segmented into ventriculoperitoneal shunts, ventriculoatrial shunts, ventriculopleural shunts, and lumboperitoneal shunts. CSF drainage systems are further bifurcated into external ventricular drainage (EVD) systems and lumbar drainage (LD) systems. Based on end user, the cerebrospinal fluid management market is segment into hospitals, clinics, ambulatory surgical centers, and others. Geographically, the cerebrospinal fluid management market is segmented into North America (the US, Canada, and Mexico), Europe (the UK, Germany, France, Italy, Spain, and the Rest of Europe), Asia Pacific (China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific), the Middle East & Africa (the UAE, Saudi Arabia, South Africa, and the Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and the Rest of South & Central America).

Contact Us

Phone: +1-646-491-9876

Email Id: sales@theinsightpartners.com