Teleradiology Services Market Growth Opportunities and Forecast by 2030

Coverage: Deployment Type (Cloud-based, Web-based), Modality (MRI, CT-Scan, X-ray, Ultrasound, Others), Application (Musculoskeletal System, Gastroentrology, Cardiology, Oncology, Neurology, Others), End User (Hospitals and Clinics, Diagnostic and Imaging Centers, Others), and Geography

- Status : Published

- Report Code : TIPHE100001380

- Category : Life Sciences

- No. of Pages : 168

- Available Report Formats :

- Last update date : July 26, 2024

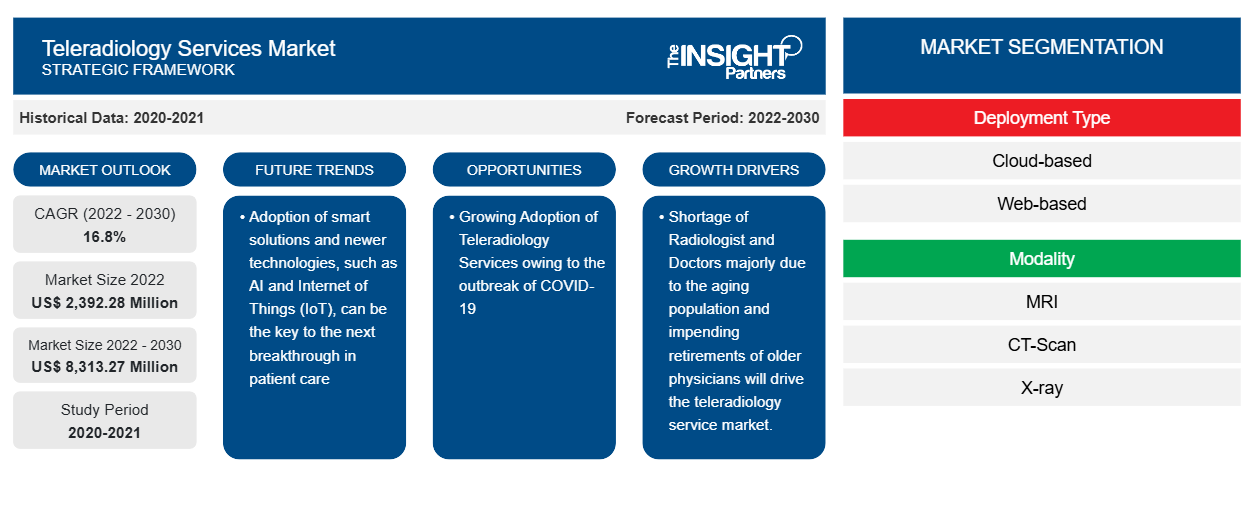

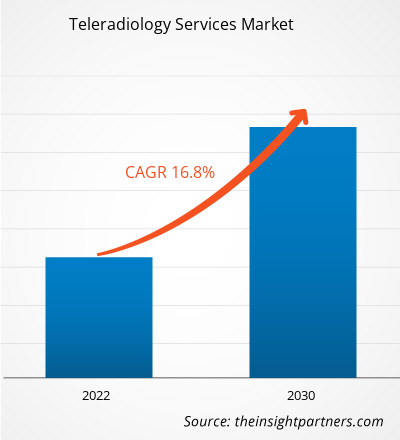

2022 Market Size

US$ 2,392.28 Mn

Base year value

2030 Forecast

US$ 8,313.27 Mn

Projected by 2030

CAGR 2022-2030

16.8 %

Growth rate

Addressable Market

US$ 40,976.69 Mn

(2022-2030)

The teleradiology services market is expected to grow from US$ 2,392.28 million in 2022 to US$ 8,313.27 million by 2030; it is anticipated to record a CAGR of 16.8% from 2022 to 2030. With increasing medical device connectivity usage, the need for a better network and technology also arises, and 5G is one such technology that is likely to remain a key trend in the market.

Teleradiology Services Market Analysis

The factors driving the market include a shortage of radiologists and doctors and a growing adoption of teleradiology services. Furthermore, adopting artificial intelligence (AI) in teleradiology has created growth opportunities for the teleradiology services market over the upcoming forecast period. Although it is difficult in the near term to create and train the number of radiologists required to meet the demand, the adoption of intelligent solutions and newer technologies, such as AI and the Internet of Things (IoT), can be the key to the next breakthrough in patient care.

Teleradiology Services Market Overview

There has been a substantial shortage of healthcare professionals, such as radiologists, physicians, and doctors worldwide. According to the article ‘Minding the Gap: Strategies to Address the Growing Radiology Shortage,’ published in July 2023, about 80% of the health systems report shortages in their radiology department. In addition, as per the Association of American Medical Colleges analysis, the shortage of radiologists and other specialists could exceed 35,000 by 2034. As per the article ‘Workforce Crisis in Radiology in the UK and the Strategies to Deal With It: Is Artificial Intelligence the Saviour?’ published by the National Library of Medicine, there was a shortfall of 33% in the radiology workforce in the UK in 2020, which is expected to rise to 44% by 2024. As per the same article, about 71% of clinical directors of UK radiology departments feel that they do not have sufficient radiologists to deliver safe and effective patient care.

Market Assessment and Insights

- North America dominated the market with 44.1% share in 2022.

- Asia Pacific is poised to grow at a CAGR of 17.1% over the forecast period.

- United States market is projected to grow at a CAGR of 17% over the forecast period.

- By Deployment Type, the Cloud-based segment accounted for the largest market share of 68.9% in 2022.

- By Modality, the MRI segment is anticipated to witness the fastest growth, registering a CAGR of 17.5% over the forecast period

- By Application, the Musculoskeletal segment accounted for the largest market share of 25.9% in 2022.

- By End User, the Hospitals and Clinics segment is anticipated to witness the fastest growth, registering a CAGR of 17.4% over the forecast period

- The report profiles key industry players such as Envision Healthcare Corp, Aster Medical Imaging LLC, RAYUS Radiology network, ONRAD Inc, Teleradiology Solutions Inc, medavis GmbH, TeleDiagnosys LLC, Vital Radiology Services, Real Radiology LLC, Agilus Diagnostics Ltd, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Teleradiology Services Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Teleradiology Services Market Drivers and Opportunities

Growing Adoption of Teleradiology Services

Teleradiology is a branch of telemedicine that involves transmitting radiological medical images in multiple modalities from one location to another to share studies with other radiologists and physicians for analysis and interpretation purposes. Due to the outbreak of COVID-19 in November 2019, the Centers of Disease Control and Prevention (CDC) issued guidance in February 2020 for healthcare providers and persons in the affected areas to maintain social distancing and offer clinical services through virtual means such as telehealth. The CDC conducted a study of the frequency of use of telehealth services during the early pandemic period, analyzing visits from four of the largest US telehealth providers that offer services in all states.

Adoption of Artificial Intelligence (AI) in Teleradiology

The emergence of the IoT has propelled the development of various health practices to improve population health. These services have been extensively informative and can be used for a variety of purposes across single condition and cluster condition management, including allowing healthcare professionals to track and monitor patient progress remotely, improving self-management of chronic conditions, assisting in the early detection of abnormalities, and accelerating symptom identification and clinical diagnoses. Further, IoT-powered apps have the potential to make better use of healthcare resources while providing high-quality, low-cost medical treatment. For instance, the Mobile MIM app was the first medical app in Apple's App Store. It is used to view, register, fuse, and show medical images from SPECT, PET, CT, MRI, X-ray, and ultrasound examinations for diagnosis purposes. Mobile MIM enhances physicians' access to pictures and allows them to consult with peers by providing wireless and portable access to medical images. AI can assist in creating an inbuilt system that prioritizes cases based on protocol requirements.

Teleradiology Services Market Report Segmentation Analysis

Key segments that contributed to the derivation of the teleradiology services market analysis are product and end user.

- Based on deployment type, the teleradiology services market is segmented cloud-based, web-based. The cloud-based segment held a largest market share in 2023.

- Based on modality, the teleradiology services market is segmented by MRI, CT-SCAN, X-Ray, ultrasound, others. The CT-SCAN segment held a largest market share in 2023.

- By application, the market is segmented into musculoskeletal system, gastroentrology, cardiology, oncology, neurology, others. The mucoskeletal segment held the largest share of the market in 2023.

- Based on end user, the teleradiology services market is segmented by hospitals and clinics, diagnostic and imaging centers, and others. The hospitals and clinics segment held a largest market share in 2023.

Teleradiology Services Market Share Analysis by Geography

The geographic scope of the teleradiology services market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

In North America, the US is the largest market for teleradiology services. Teleradiology has emerged as a potential solution, with small stroke experts guiding local emergency physicians through a thorough neurological exam, imaging review, and management decisions. According to IntechOpen, stroke is the fifth leading cause of death in the US, with one stroke occurring approximately every 40 seconds and stroke-related death occurring roughly every 4 minutes. Teleradiology networks use digital technology for two-way, high-definition video teleconferencing to bridge these differences by providing safe, efficient, and affordable care to underserved communities across the US.

Teleradiology networks, such as traditional practices, must comply with the Health Insurance Portability and Accountability Act (HIPAA), which regulates the protection of health information in the country. The increased use of teleradiology nationwide provides more extensive access to acute care expertise without delay and helps fill gaps in regional access to stroke care.

Teleradiology Services Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 2,392.28 Million |

| Market Size by 2030 | US$ 8,313.27 Million |

| Global CAGR (2022 - 2030) | 16.8% |

| Historical Data | 2020-2021 |

| Forecast period | 2022-2030 |

| Segments Covered |

By Deployment Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Teleradiology Services Market Players Density: Understanding Its Impact on Business Dynamics

The Teleradiology Services Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Teleradiology Services Market News and Recent Developments

The Teleradiology Services Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the teleradiology services market are listed below:

- Yellowcross Healthcare Commerce, a telemedicine practice management organization, launched a new consultancy service to help medical groups and health care facilities expand their remote care capabilities. (Source: Yellowcross, Company Website, February 2024)

Teleradiology Services Market Report Coverage and Deliverables

The “Teleradiology Services Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Teleradiology services market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Teleradiology services market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Teleradiology services market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments.

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the teleradiology services market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends