Sandwich Panel Market Share, Growth & Forecast by 2034

Sandwich Panel Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Material (Polyurethane, Polyisocyanurate, Mineral Wool, and Others), Application (Wall Panels, Roof Panels, and Others), and End Use (Residential and Non-Residential)

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Report Date : Apr 2026

- Report Code : TIPRE00017588

- Category : Chemicals and Materials

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

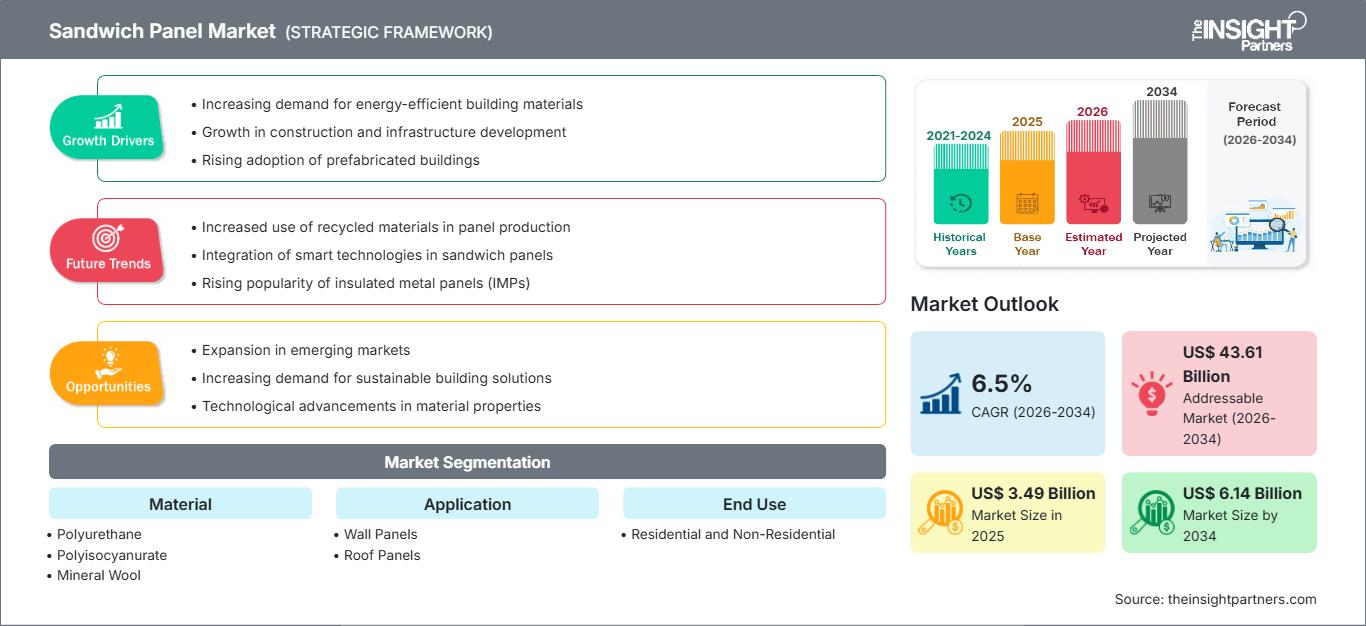

The global Sandwich Panel market size is projected to reach US$ 6.14 billion by 2034 from US$ 3.49 billion in 2025. The market is anticipated to register a CAGR of 6.5% during the forecast period 2026–2034. Key market dynamics include an intensifying global focus on energy-efficient building envelopes, rising demand for rapid construction techniques in the industrial sector, and stringent government regulations regarding fire safety and thermal insulation. Additionally, the market is expected to benefit from the expansion of the cold storage industry, driven by e-commerce, the surge in modular and prefabricated construction projects, and the increasing integration of sustainable, recyclable core materials in high-performance panels.

Sandwich Panel Market Analysis

The sandwich panel market analysis indicates a strategic pivot toward high-performance insulation cores as developers prioritize long-term energy savings and carbon footprint reduction. Procurement trends suggest a growing preference for Polyisocyanurate (PIR) and Mineral Wool over traditional options due to their superior fire resistance and R-values. Strategic opportunities are emerging in the renovation and retrofit segment, where lightweight sandwich panels offer a cost-effective solution for upgrading the thermal efficiency of aging commercial structures without compromising structural integrity. The analysis also highlights that market success is increasingly dependent on "installation-ready" innovations, such as interlocking joint systems that reduce onsite labor costs. To remain competitive, manufacturers must focus on localized production to mitigate logistics expenses and develop product lines that meet specific regional green building certifications, such as LEED or BREEAM.

Sandwich Panel Market Overview

Sandwich panel is evolving from a specialized industrial component into a mainstream solution for modern sustainable architecture. Historically utilized for cold storage and warehouse roofing, these composite units are now widely adopted in commercial, residential, and institutional projects. The sector is characterized by a mix of global building material conglomerates and specialized regional fabricators, all responding to the global push for "Net Zero" buildings. Increasing urbanization in emerging economies is driving the demand for quick-to-install wall and roof systems, while mature markets are focusing on the aesthetic versatility of architectural panels. As a versatile "all-in-one" product providing structural support, insulation, and weather protection, sandwich panels are becoming a cornerstone of the modular construction revolution, particularly in the Asia-Pacific and European regions. For instance, the market in the US is driven by a robust expansion of logistics hubs and data centers requiring high thermal stability. American builders are increasingly adopting these panels to meet rigorous energy codes and reduce onsite construction timelines. The growth of specialized cold-chain infrastructure remains a primary catalyst for domestic demand.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONSandwich Panel Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Sandwich Panel Market Drivers and Opportunities

Market Drivers:

- Surging Demand for Energy-Efficient Building Envelopes: Global initiatives to reduce carbon emissions have led to stricter building codes requiring superior thermal insulation. Sandwich panels, particularly those with PIR and PUR cores, provide high R-values that significantly lower heating and cooling costs, driving their adoption in sustainable construction.

- Rapid Expansion of Cold Chain and Logistics Infrastructure: The exponential growth of e-commerce and the pharmaceutical sector has necessitated massive investments in temperature-controlled warehouses. Sandwich panels are the primary choice for these facilities due to their airtightness, moisture resistance, and ability to maintain precise thermal stability.

- Acceleration of Modular and Prefabricated Construction: As labor shortages and rising onsite costs impact the construction industry, the shift toward off-site manufacturing has intensified. The lightweight and "plug-and-play" nature of sandwich panels allows for drastically reduced project timelines, making them essential for fast-track industrial and commercial developments.

Market Opportunities:

- Growth in High-Tech Data Center Construction: The global boom in cloud computing and AI requires specialized facilities with stringent fire safety and acoustic control requirements. This presents a significant opportunity for mineral wool and PIR panel manufacturers to supply high-performance envelopes that protect sensitive hardware.

- Retrofitting and Renovation of Aging Building Stock: In mature markets like Europe and North America, there is a substantial opportunity to utilize sandwich panels for the energy-efficient retrofitting of older industrial buildings. Lightweight panels can be installed over existing structures to improve thermal performance without the need for extensive structural reinforcement.

- Innovation in Bio-Based and Low-Carbon Materials: There is a rising demand for "green" sandwich panels featuring recycled steel skins and bio-polyol-based cores. Producers who prioritize environmental product declarations (EPDs) and low-embodied carbon can capture high-margin segments among eco-conscious developers and institutional investors.

Sandwich Panel Market Report Segmentation Analysis

The Sandwich Panel Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Material:

- Polyurethane (PUR): A widely utilized core material known for its excellent thermal insulation properties and lightweight nature, making it a standard choice for temperature-controlled environments.

- Polyisocyanurate (PIR): A high-performance evolution of polyurethane that offers enhanced fire resistance and thermal stability, increasingly favored in commercial and industrial applications.

- Mineral Wool: A non-combustible material preferred for projects with stringent fire safety requirements, providing both thermal insulation and superior acoustic dampening.

- Others: Includes materials such as Expanded Polystyrene (EPS) and Aluminum Honeycomb, catering to niche requirements in lightweight aerospace or budget-conscious residential projects.

By Application:

- Wall Panels: The dominant application segment, utilized for external cladding and internal partitioning to provide structural integrity and aesthetic appeal in modern buildings.

- Roof Panels: Engineered to withstand environmental loads while ensuring airtight insulation, these panels are essential for large-scale industrial and warehouse facilities.

- Others: Encompasses specialized applications such as ceiling panels for cleanrooms and specialized flooring for cold storage units.

By End Use:

- Residential: Includes the use of panels in modular housing, social housing projects, and modern sustainable homes where speed of construction and energy efficiency are paramount.

- Non-Residential: The primary volume driver, covering industrial warehouses, commercial offices, retail centers, cold storage facilities, and public infrastructure.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Sandwich Panel Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 3.49 Billion |

| Market Size by 2034 | US$ 6.14 Billion |

| Global CAGR (2026 - 2034) | 6.5% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Material

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Sandwich Panel Market Players Density: Understanding Its Impact on Business Dynamics

The Sandwich Panel Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Sandwich Panel Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for industrial developers and cold-chain logistics providers to expand.

The sandwich panel market is undergoing a significant transformation, moving from a traditional industrial staple to a global high-value building solution. Growth is driven by the rising demand for energy-efficient envelopes, a surge in "prefabricated" construction demand, and the expansion of the hyperscale data center and cold storage sectors. Below is a summary of market share and trends by region:

North America

- Market Share: A mature yet steadily growing segment driven by the massive expansion of e-commerce fulfillment centers and institutional infrastructure.

- Key Drivers:

- Implementation of stringent ASHRAE energy performance standards.

- Rapid scaling of the domestic "Life Sciences" sector requires specialized cleanroom panels.

- Increased focus on "disaster-resilient" construction in hurricane-prone coastal regions.

- Trends: High adoption of architectural panels for commercial facades and a significant shift toward FM-approved (Factory Mutual) fire-resistant cores to lower insurance premiums.

Europe

- Market Share: Historically, the largest market for sandwich panels, anchored by sophisticated green building regulations and a long-standing culture of modular assembly.

- Key Drivers:

- EU "Renovation Wave" strategy mandating energy upgrades for the continent's aging building stock.

- Strong government subsidies for thermally efficient cladding and carbon-neutral construction.

- Established presence of global market leaders with advanced continuous production lines.

- Trends: A strategic move toward "circularity," with manufacturers prioritizing low-embodied carbon steel and bio-based insulation to meet the 2030 Net Zero goals.

Asia-Pacific

- Market Share: The largest and fastest-growing region globally, with China and India acting as the primary engines for regional consumption.

- Key Drivers:

- Massive urbanization and "Smart City" initiatives require rapid, cost-effective building materials.

- Rapid industrialization and the establishment of global manufacturing hubs in Southeast Asia.

- Explosive growth in the organized retail and cold-chain sectors due to shifting consumer habits.

- Trends: Heavy reliance on automated production to meet the high volume of "low-cost, high-speed" housing projects and the increasing integration of IoT sensors within panels for structural health monitoring.

South and Central America

- Market Share: An emerging market with a growing artisanal and industrial sector in countries like Brazil, Argentina, and Chile.

- Key Drivers:

- The increasing modernization of agricultural export facilities requires temperature-controlled storage.

- Rising interest in affordable modular housing to address urban density challenges.

- Modernization of small-scale industrial parks into commercial-grade logistics centers.

- Trends: Expansion of regional manufacturing footprints to mitigate import tariffs and the introduction of cement-board facing panels for improved moisture resistance in tropical climates.

Middle East and Africa

- Market Share: Developing market with significant growth in high-end construction projects, transitioning toward formalized commercial standards.

- Key Drivers:

- "Giga-projects" in the GCC region focusing on sustainable tourism and non-oil economic diversification.

- High demand for superior thermal insulation to combat extreme arid temperatures and reduce HVAC loads.

- Strategic investments in food security infrastructure, including massive refrigerated silos and distribution hubs.

- Trends: Adoption of the latest international fire and life safety codes, leading to a surge in demand for non-combustible Mineral Wool and PIR-based panel systems.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Kingspan Group, Assan Panel, Isopan, Tata Steel, Arcelormittal, Lattonedil, Italpannelli S.R.L., Dana Group of Companies, Zhongjie Group, which also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Fire Safety and Certification: Obtaining global certifications (e.g., FM Global, UL) to position panels as premium, insurance-friendly building components.

- Digital Integration: Utilizing Building Information Modeling (BIM) files to assist architects in seamlessly integrating sandwich panels into complex digital designs.

- Sustainability Branding: Emphasizing the use of recycled steel and halogen-free insulation to appeal to the growing "green" construction market.

- System Solutions: Offering complete building envelopes, including flashings, fasteners, and gutters, to provide a single-source warranty for developers.

Opportunities and Strategic Moves

- Partner with modular construction firms and 3D-printing building startups to integrate sandwich panels into the next generation of automated housing production.

- Invest in R&D for vacuum insulation panels (VIPs) and aero-gel cores to provide ultra-thin panels with unprecedented thermal performance for space-constrained urban markets.

Major Companies operating in the Sandwich Panel Market are:

- Kingspan Group

- Assan Panel

- Isopan

- Tata Steel

- Arcelormittal

- Lattonedil

- Italpannelli S.R.L.

- Dana Group of Companies

- Zhongjie Group

- Multicolor Steels India Pvt Ltd.

Disclaimer: The companies listed above are not ranked in any particular order.

Sandwich Panel Market News and Recent Developments

- In April 2025, ArcelorMittal Construction expanded its high-performance range with the launch of the Litetherm™ 1001 roof sandwich panel. This new product was specifically engineered to meet essential load-bearing requirements while maintaining high thermal efficiency, which further strengthened the company's portfolio in the European industrial roofing market.

- In February 2024, Owens Corning, a leader in global building and construction materials, and Masonite International Corporation, a leading global provider of interior and exterior doors, entered into a definitive agreement under which Owens Corning acquired all outstanding shares of Masonite for US$ 133.00 per share in cash. This transaction, valued at approximately US$ 3.9 billion, was strategically designed to integrate Masonite's door systems with Owens Corning's broader building envelope offerings, including their high-performance sandwich panel solutions, to provide a more comprehensive portfolio for residential and commercial customers.

Sandwich Panel Market Report Coverage and Deliverables

The "Sandwich Panel Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Sandwich Panel Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Sandwich Panel Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Sandwich Panel Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Sandwich Panel Market.

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For